1.2- Price determination in a competitive market

1/66

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced |

|---|

No study sessions yet.

67 Terms

what is demand

the quantity of a good or service that consumers are able and willing to buy at a given price during a given period of time

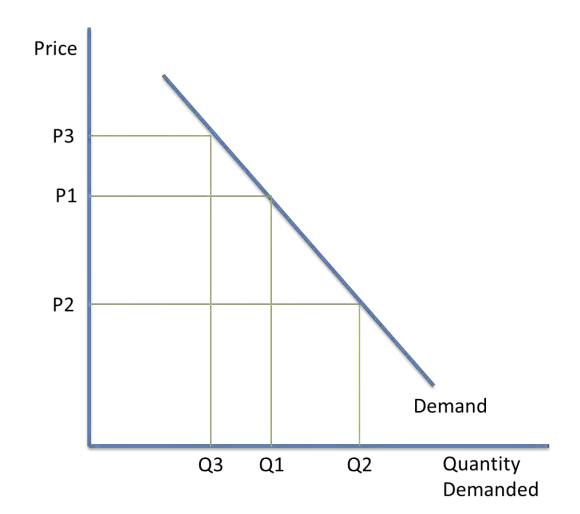

describe movements along the demand curve (explain)

at price p1, a quantity of q1 is demanded. At a lower price of p2, a larger quantity of q2 is demanded. this is an expansion of the demand.

at a higher price of p3, a lower quantity of q3 is demanded. this is a contraction of demand

only changes in price cause movements along the demand curve

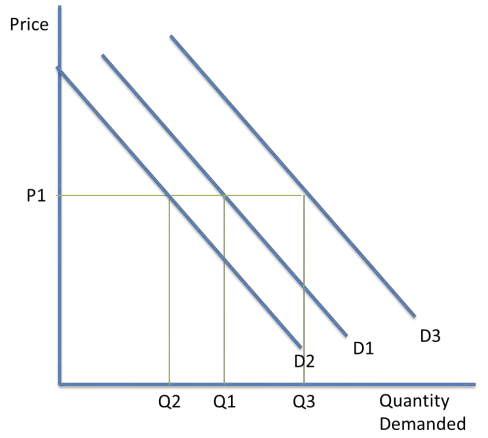

shifting the demand curve (explain)

price changes do not shift the demand curve

a shift from d1 to d2 is an inward shift in demand, so a lower quantity of goods is demanded at the market price of p1

a shift from d1 to d3 is an outward shift in demand where more goods are demanded at the market price of p1

what are the factors that shift the demand curve

P- population (higher pop. = more demand)

I- income

R- related goods (substitutes/complements)

A- advertising

T- tastes/ fashions

E- expectations

S- seasons

how does income shift the demand curve

consumers have more disposable income

able to afford more goods, so demand increases

wealth effect occurs, as consumers spend more they perceive their wealth to increase

how do expectations shift demand curve

if people expect the price of shares in a company to increase in the future, demand is likely to increase in the present

what is the law of diminishing marginal utility

states that as an extra unit of good is consumed, the marginal utility (benefit derived from consuming the good) falls. therefore, consumers are willing to pay less for the good

why is the demand curve downward sloping

the number of units demanded increase with a fall in price

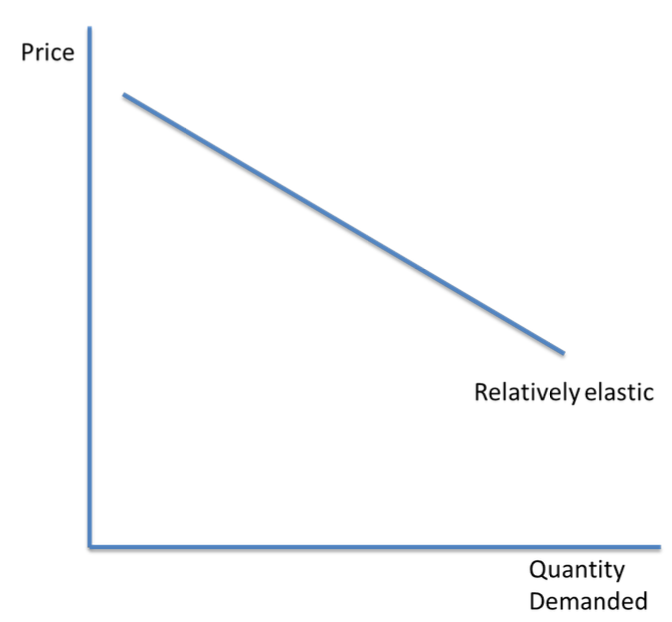

explain what price elastic mean

a price elastic good is very responsive to a change in price

change in price leads to an even bigger change in demand

PED is >1

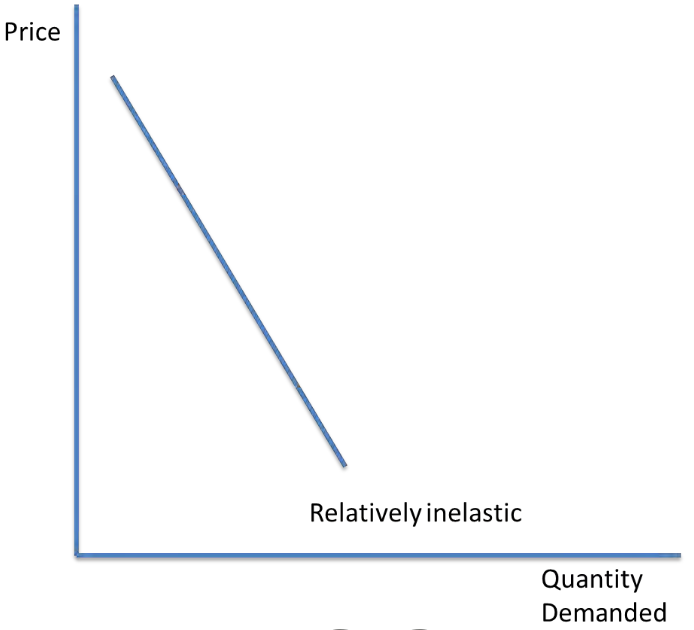

explain what price inelastic mean

a price inelastic good has a demand that is relatively unresponsive to a change in price

PED is <1

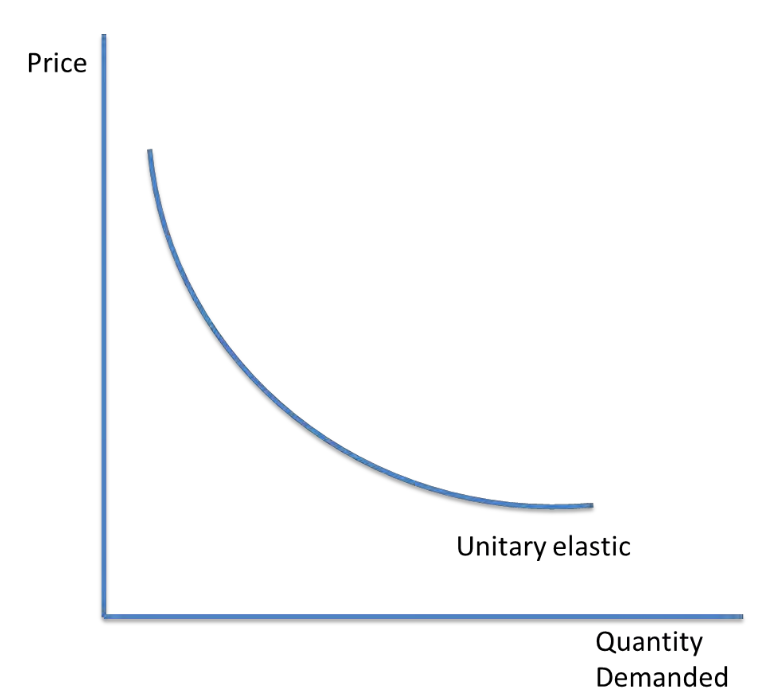

explain unitary elasticity

a unitary elastic good has a change in demand which is equal to the change in price

PED = 1

explain perfect inelastic goods

has a demand which does not change when price changes

PED = 0

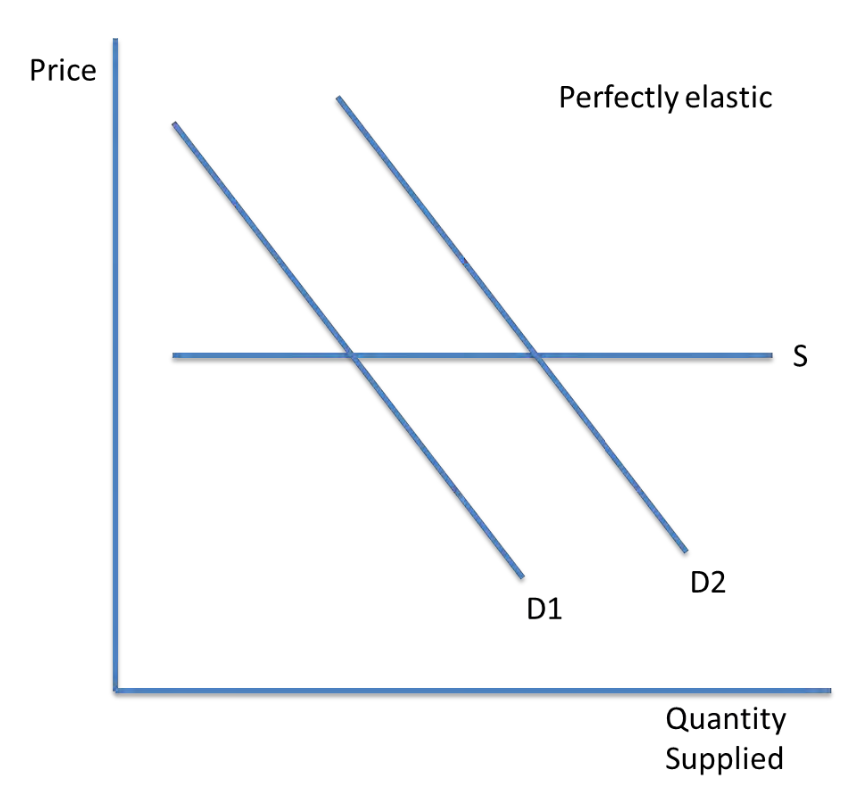

explain perfectly elastic goods

has a demand which falls to zero when price changes

PED = infinity

what are the factors influencing PED

necessity, substitutes, addictiveness, proportion of income spent, durability, peak and off-peak demand

how does necessity influence PED

a necessary good will have a relatively inelastic demand

Even if the price increases significantly, consumers will still demand. it because they need it

Luxury goods are more price elastic, if price rapidly increases, the demand will fall significantly

how does substitutes influence PED

if the good has several substitutes, the demand is more price elastic

The elasticity can change within markets

e.g. market for bread is less elastic than the market for white bread. This is because there are fewer substitutes for bread in general but several for white bread

how does elasticity change in the short run and long run

in the long run, consumers have time to respond and find a substitute, so demand becomes more price elastic

In the short run, consumers do not have time, so demand is more inelastic

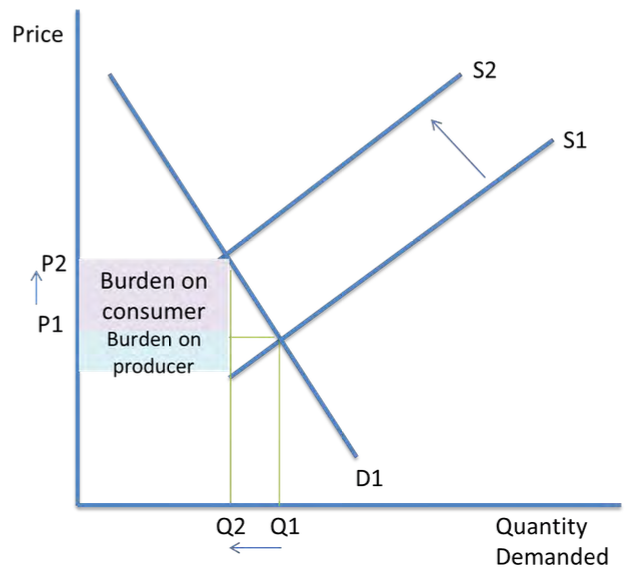

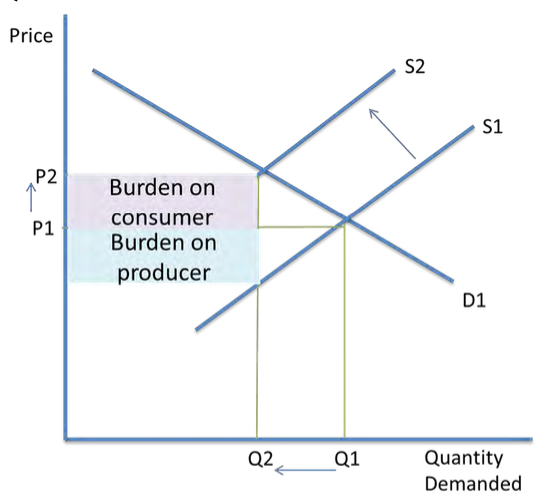

burden of indirect tax on consumers/ firms(explain)

if a firm sells a good with inelastic demand, tax burden mostly on consumers because they know a price increase will not cause demand to fall significantly

if a firm sells a good with an elastic demand, firms take most of the tax burden because they know if the price of a good increases, demand will likely fall, lowering overall revenue

what maximises government revenue

a good with inelastic demand

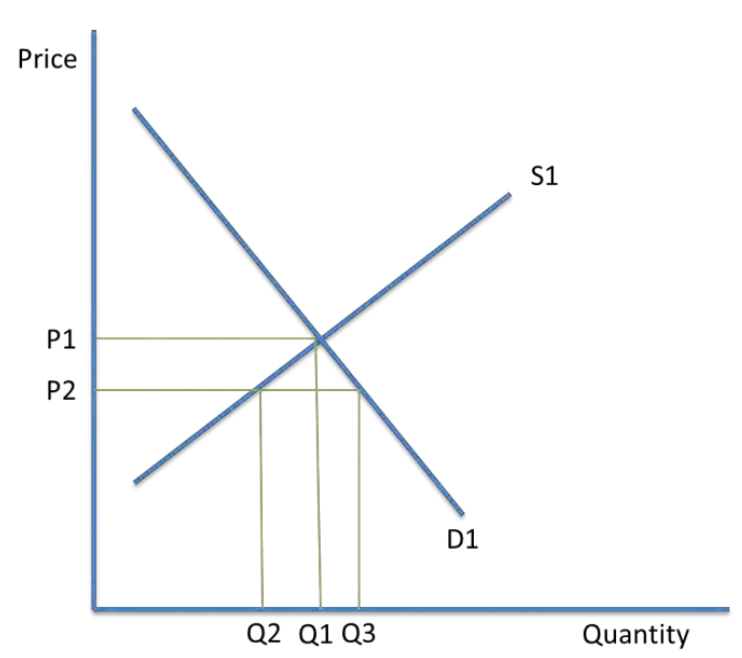

analysis of elasticity of demand and tax revenue diagram (price inelastic)

an increase in tax will decrease supply from s1 to s2, which increases price from p1 to p2

demand contracts from q1 to q2

effective in raising gov. revenue

analysis of elasticity of demand and tax revenue diagram (price elastic)

not effective in raising gov. revenue, but reduces demand of a particular good

an increase in tax will decrease supply from s1 to s2, which increases price from p1 to p2

demand contracts from q1 to q2

what is a subsidy

a payment from the government to firms tp encourage the production of a good to lower their average costs

advantages of subsidies

benefit can go to both the producer in the form of increased revenue or to the consumer in the form of lower prices

calculation of total revenue

average price x quantity

how does elastic demand affect total revenue

if a good has elastic demand and the firm raises it price, quantity sold will fall, reducing overall revenue

what is income elasticity of demand

income elasticity of demand is the responsiveness of a change in demand to a change in income

how to calculate income elasticity of demand

YED = % change in QD/ % change in income

what is an inferior good

goods which see a fall in demand as income increases. A income increases, consumers switch to branded goods

YED <0

YED of normal goods

YED is >0

how does income elasticity affect luxury goods

an increase in income causes an even bigger increase in demand

YED > 1

Luxury goods are also normal goods, and they have an elastic income

how do firms react to real incomes rising

firms might switch to producing more luxury goods and fewer inferior goods

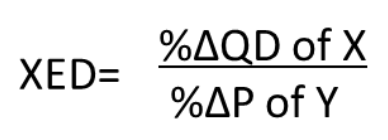

what is cross elasticity of demand

the responsiveness of a change in demand of one good to a change in price of another good

formula for cross elasticity of demand

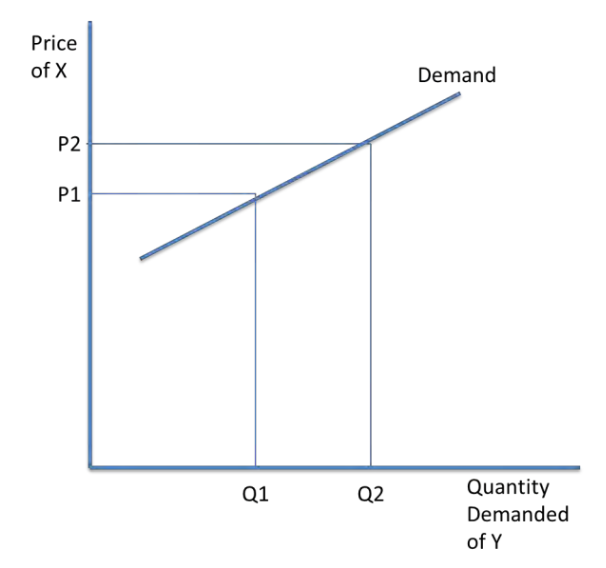

XED and complementary goods (explain)

complementary goods have a negative XED

If one good becomes more expensive, the quantity demanded for both goods will fall

Close complements- a small fall in price x leads to a large increase in QD of Y

weak complements- a large fall in the price of good x leads to only a small increase in QD of Y

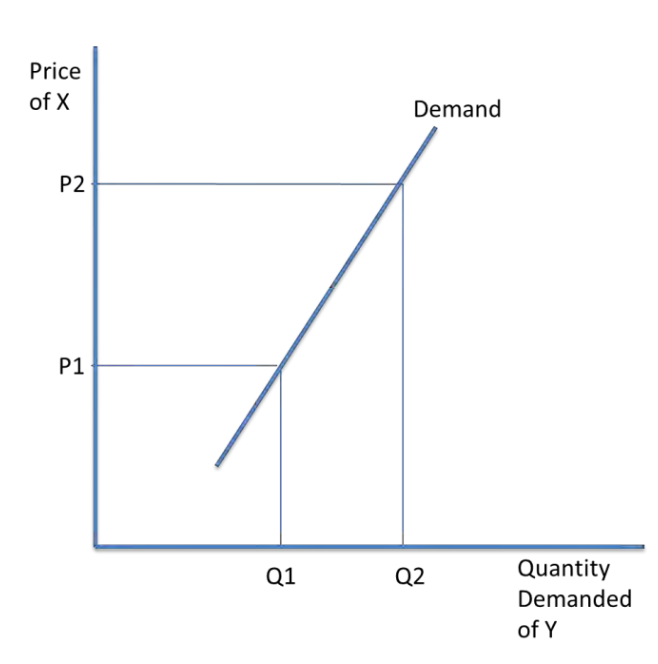

relationship between XED and substitutes

substitutes can replace another good, so the XED is positive and demand curve is upward sloping

close substitutes- a small increase in price of good X leads to a large increase in QD of Y

weak substitutes- a large increase in the price of good c ;eads to a smaller increase in QD of Y

relationship between unrelated goods and XED

has a XED of 0

why are firms interested in XED

allows them to see how many competitors they have. therefore, they are less likely to be affected by price changes by other firms, if they are selling complementary goods or substitutes

define supply

the quantity of a good or service that a producer is willing and able to supply at a given price during a given period of time

why are supply curves upward sloping

if price increases, more profitable for firms to supply the good so supply increases

High prices encourage new firms to enter the market, because it seems profitable so supply increases

with larger outputs, firm’s costs increase, so they need to charge a higher price to cover the costs

movements along the supply curve analysis

price p1, quantity of q1 is supplied

at the lower price of p2, q2 is supplied (contraction)

if prices increase from q2 to q1

price mechanism of rising demand (explain)

Price rises

Signals excess demand and need for greater resources

Incentivises firms to increases their output to increase profit

Ration resources discouraging consumption

Allocate resources efficiently at equilibrium

price mechanism of rising supply (explain)

Prices fall

Signals excess supply and need for fewer resources

Incentivises firms to decrease their output to increase profit

Ration resources encouraging consumption

Allocate resources efficiently at equilibrium

factors that shift the supply curve

Productivity

Indirect taxes

Number of firms

Technology

Subsidies

Weather

Costs of production

how does productivity affect supply

Higher productivity causes an outward shift in supply, becuase average costs for the firm fall

how do indirect taxes affect supply

inward shift in supply

how does technology affect supply

more advanced technology causes an outward shift in supply

how do costs of production affect supply

if costs of production fall, the firm can afford to supply more

If costs rise such as with higher wages, there will be an inward shift in supply

shifting along the supply curve analysis

price changes do not shift the supply curve

shift from 21 to s2 is an outward shift, larger quantities of goods are supplied at the market price of p1

a shift from s3 to s1 is an inward shift in supply -more goods are supplied at the market price of p1

define price elasticity of supply

the responsiveness of a change in supply to a change in price

formula for PES

PES = % change in quantity supplied / % change in price

elastic supply

firms increase supply quickly at little cost

PES >1

inelastic supply

expensive for firms to take a long time

PES <1

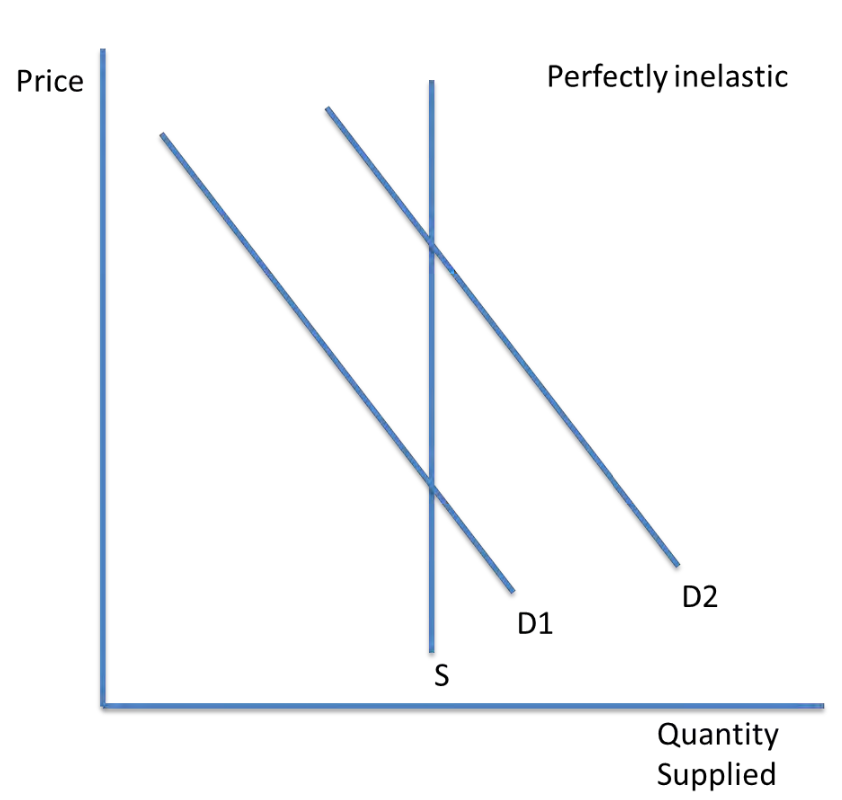

perfectly inelastic

PES = 0

Supply is fixed, so there is a change in demand, it cannot be met easily

perfectly elastic

PES = Infinity

any quantity demanded can be met without changing price

factors influencing PES

time scale

spare capacity

level of stocks

substitute factors

barriers to entry to market

how does substitute factors affect PES

if labour and capital are more mobile, supply is more price elastic because resources can be allocated to where extra supply is needed

how do barriers affect PES

High barriers to entry means supply is more price inelastic, because it is difficult for new firms to enter and supply the market

where is the equilibrium on a diagram

when supply meets demand

excess demand diagram analysis

at q2, price is at p2 which is below market equilibriumDemand is now greater than supply, which can be calculated by q3-q2. This is a state of disequilibrium

demand price does not equal supply price and quantity demaded does not equal quantity supplied

what is the result of excess demand on markets

there is a shortage in the market

prices increase, so firms supply more

As prices increase, demand will contract

excess demand diagram analysis

supply is now at q2 and demand is at q1

there is a surplus of q2-q1

prices will fall back to p1 as firms lower their prices and try to sell their goods

the market will clear and return to equilibrium

when are new market equilbriums made

when the demand or supply curves shift due to PIRATES or PINTSWC reasons

what are the different types of demand

derived, composite, joint

what is derived demand

this is when demand for one good is linked to the demand of a related good

e.g demand for bricks is derived from demand of building new houses

what is composite demand

when a good demanded has more than one use

e.g milk

what is joint demand

when goods are bought together

e.g a digital camera and sd card

what does joint supply mean

increasing the supply of one good causes an increase or decrease in supply of another good