MICRO EXAM #2

1/81

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced |

|---|

No study sessions yet.

82 Terms

excludable

others can be prevented from use

rivalrous

my use prevents your use

private goods

rivalrous and exclusive

cars, food, most economic goods

common resources

rivalrous and nonexclusive

fish in the ocean, the environment

club goods

nonrivalrous and exclusive

netflix, museum, theme park, sporting events

public goods

nonrivalrous and nonexclusive

fireworks, public radio, vaccines, lighthouses

positive externalities

public goods and club goods

negative externality

common resources → associated with overconsumption

free rider problem

beneficiaries of public goods often don’t need to pay for them, so they won’t do so voluntarily, and the good will be underprovided

explicit costs

on the books → equipment, raw materials, license

implicit costs

opportunity costs → what else one could be doing with money/ time

marginal product of labor

increase in output from hiring 1 additional input of labor

marginal product of labor equation

Δoutput/ Δinputs

diminishing marginal product

marginal product falls as input increases

total cost equation

fixed costs + variable costs

average fixed cost equation

fixed costs/ quantity

average variable costs equation

variable costs/ quantity

average total cost equation

total costs/ quantity or AFC + AVC

marginal cost equation

Δ total cost/ Δ quantity

What does the space between AVC and ATC on SR graph represent?

The average fixed cost

Where does the marginal cost intersect ATC and AVC?

at there minimums

Where are average costs minimized?

where they meet marginal costs

Does diminishing marginal product occur in the long run?

No, because there are no fixed inputs

economies of scale

decreasing long-run ATC, 1 or few firms

constant return

flat long-run ATC, large and small firms

diseconomies of scale

increase in ATC, many small firms

What causes a decrease in LRATC?

specialization

What causes an increase in LRATC?

organizational costs, consequences of not being organized increase

marginal cost

cost of producing an extra unit of output

When is average cost rising and falling?

rising→ marginal costs above AC

falling → marginal costs below AC

Profit equation

total revenue - total costs or (P-ATC)*Q

assumptions of perfect competition

many buyers or sellers → price takers

homogenous product

firms can freely enter and exit the market

Where is profit maximized in perfect competition?

Where marginal revenue meets marginal costs

Average revenue for perfect competition

(total revenue/ quantity) or price

variable costs equation

AVC * Q

fixed costs equation

AFC * Q

marginal revenue for perfect competition

Δtotal revenue/ Δquantity

What does marginal revenue equal in PC only?

price

PC MR>MC

next unit the firm sells will be profitable, so they should produce more

PC MR<MC

last unit a firm produced was a loss, so the firm should produce less

"Stopping point” for profit maximization in PC

marginal cost = marginal revenue

profit in PC SR

P>ATC at Q* where MR = MC

losses in PC SR

P<ATC at Q* where MR = MC

demand curve in PC

perfectly elastic, MR=P=d

P < ATC in LR for PC

firm taking economic losses → exit market

P = ATC in LR for PC

zero economic profits (long run equilibrium) → stay in market

P > ATC in LR for PC

making economic profits → enter

TR > VC in SR for PC

firm will be more profitable by remaining open than shutting down (P > AVC)

TR < VC in SR for PC

firm should shut down because they are taking losses

Where does supply come from?

supply curve is the marginal cost curve above the point where it meets AVC

LR equilibrium for PC gains

P > ATC → profits → entry → increased supply → decrease in price till P = ATC

LR equilibrium for PC losses

P < ATC → losses → exit → decrease supply → increase in price till P =ATC

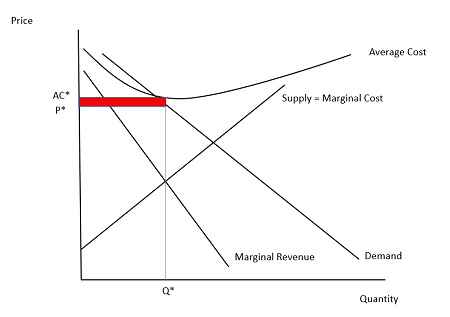

long run equilibrium characteristics

firms produce at efficient scale (minimum ATC)

firms earn zero economic profit (stay)

LR supply curve in PC

generally flat (relatively more elastic) or flatter than SR supply; it follows efficient scales of the firms

monopoly

controls the entire market, price makers

resource monopoly

control source of a natural resource

std oil, DeBeers, utilities

government-created monopoly

intellectual property

trademark, patent

natural monopoly

naturally occurring, outcompete smaller companies

economies of scale ← LR ATC declining

Where is total revenue maximized for monopoly?

where marginal revenue = 0

Elastic region on monopoly graph

area above isoelastic point (MR > 0)

isoelastic point on monopoly graph

where MR is maximized, where MR hits x-axis

inelastic region on monopoly graph

area below isoelastic point (MR < 0)

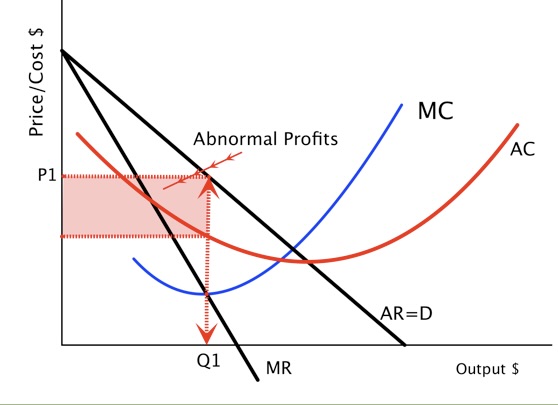

Profit maximization for monopoly

maximized where MR = MC

P > ATC

area between ATC and P is profit

What do monopolies price off of?

the demand curve

Losses in monopoly SR

P < ATC

if losses persist, the monopoly will exit the market

unique characteristics of monopolies

can make profit in the long run

lower consumer surplus and has deadweight loss

less production and higher prices (maximize profits)

Does a monopolist have a supply curve?

Supply is a unique relationship between price and quantity supplied. The optimal quantity supplied and the price for monopolists depends on the demand curve, and it is possible there is the same Q* for 2+ prices or the same P* for 2+ quantities. Meaning monopolists DO NOT have supply curve.

price discrimination

a firm charges different prices to different people or different prices for different quantities

consequences of price discrimination

consumer surplus turns to profit

deadweight loss turns to profit or CS (rare)

requirements for price discrimination

pricing power (non-competitive)

knowledge of WTP varying

segment the market (prevent resale)

examples of price discrimination

student/ senior discounts

airline prices

quantity discounts

coupons

public policy towards monopolies

make monopolies more competitive (break them up)

regulations (marginal cost pricing)

public ownership

no nothing

Monopolistic competition in SR

they are monopolies

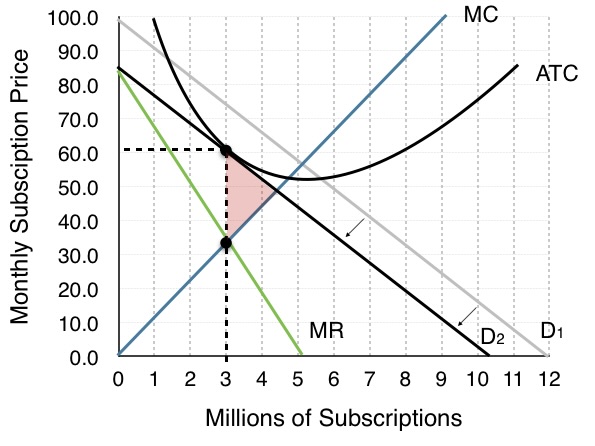

Monopolistic competition from SR to LR if making profits

entry to market → decrease demand (new close substitutes increase)

stops when P = ATC

Monopolistic competition from SR to LR if making losses

a firm or competitor leaves market → increase in demand (due to exit of close substitutes)

stops when P = ATC

Monopolistic competition vs Monopoly long run

monopolistic competition unique in that:

barrier to exit and entry are low

close substitutes are available

characteristics of monopolistic competition in the LR

M.Cs produce at less than efficient scale (excess capacity)

mark up over marginal cost: P > MC

has deadweight loss

P = ATC

advertising function

help a monopolistic competitor “steal” customers from competitors

reduce transaction costs (information)

inform consumers

brand signalling

Oligopoly

few sellers of identical productions or close substitutes

soda, cigarettes, tech giants

game theory

the study of decision making in strategic situations (outcomes depend on own decisions and decisions of others)

Nash equilibrium

both players best respond to what the other might do ← mutually best response

dominant strategy

the best response is the same irrespective of what other player does