3.3.2 Costs (in the short run)

1/11

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

12 Terms

Definition & Formulae of total cost

Total cost = cost of producing a given level of output

TC = FC + VC

Note that fixed costs only happen in the short run as it can only happen when at least one factor or production is fixed

Variable costs can happen in both short run & long run

What are the 2 types of total costs (every type of cost, there’s a fixed & a variable)

Total fixed costs (TFC)

cost that remains the same as output increases or decreases (ie. rent)

TFC = TC - TVC

Total variable costs (TVC)

cost that changes with the level of output (ie. cost of ingredients)

TVC = TC - TFC

Note: wages (per output produced) so variable

salary (same every month, has a contract) so fixed

Definition & Formulae of average cost

Average (total) cost = cost per unit of output

TC / Q

OR ATC = AFC + AVC

Definition & Formulae of average fixed cost

Average fixed cost = fixed cost per unit of output

AFC = TFC / Q

Definition & Formulae of average variable cost

Average variable cost = variable cost per unit of output

AVC = TVC / Q

Definition & Formulae of marginal cost

Marginal cost = cost of producing one more unit of output

So not affected by a change in FC

affected by a change in level of output so affected by changes in variable cost

MC = change in TC / change in Q

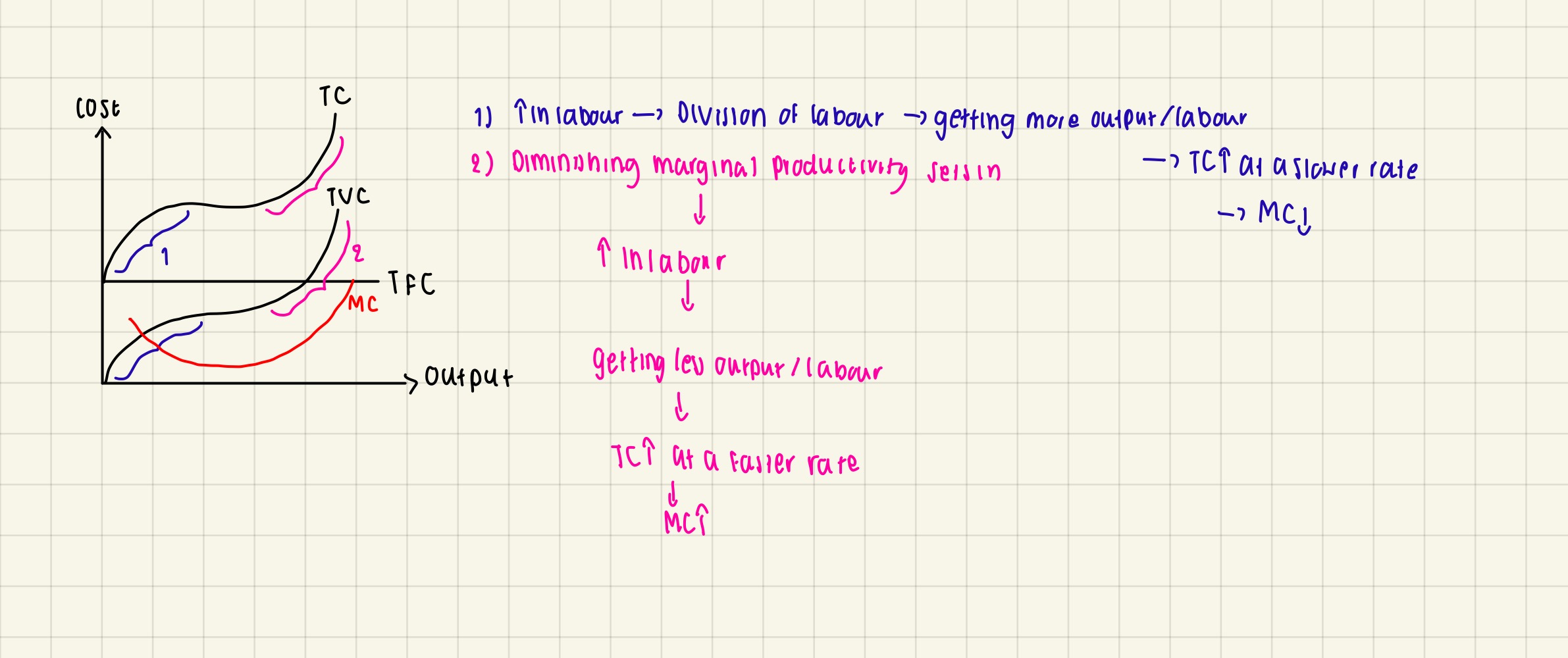

Derivation of short-run cost curves from the assumption of diminishing marginal productivity

The reason that the cost curves are going down and up again like a parabola is because of diminishing marginal productivity :

Fixed factors of production: land of the bakery shop

Variable factors of production: number of workers

Diminishing marginal productivity = for an additional unit of labour, the additional increase in productivity declines

→ MC increase

Example of the law:

ie when making cake: at first, when workers are added, they may become specialized - efficient → an additional unit of labour →increasing marginal productivity → more additional output→ MC falls (less cost to produce one more unit of output)

After some point: diminishing marginal productivity sets in → an additional unit of labour → MP falls → less additional output (as more crowded) → cost more to produce an extra output → MC increases at a faster rate

This only happens in the short run because in the long run, they can expand the space in the shop

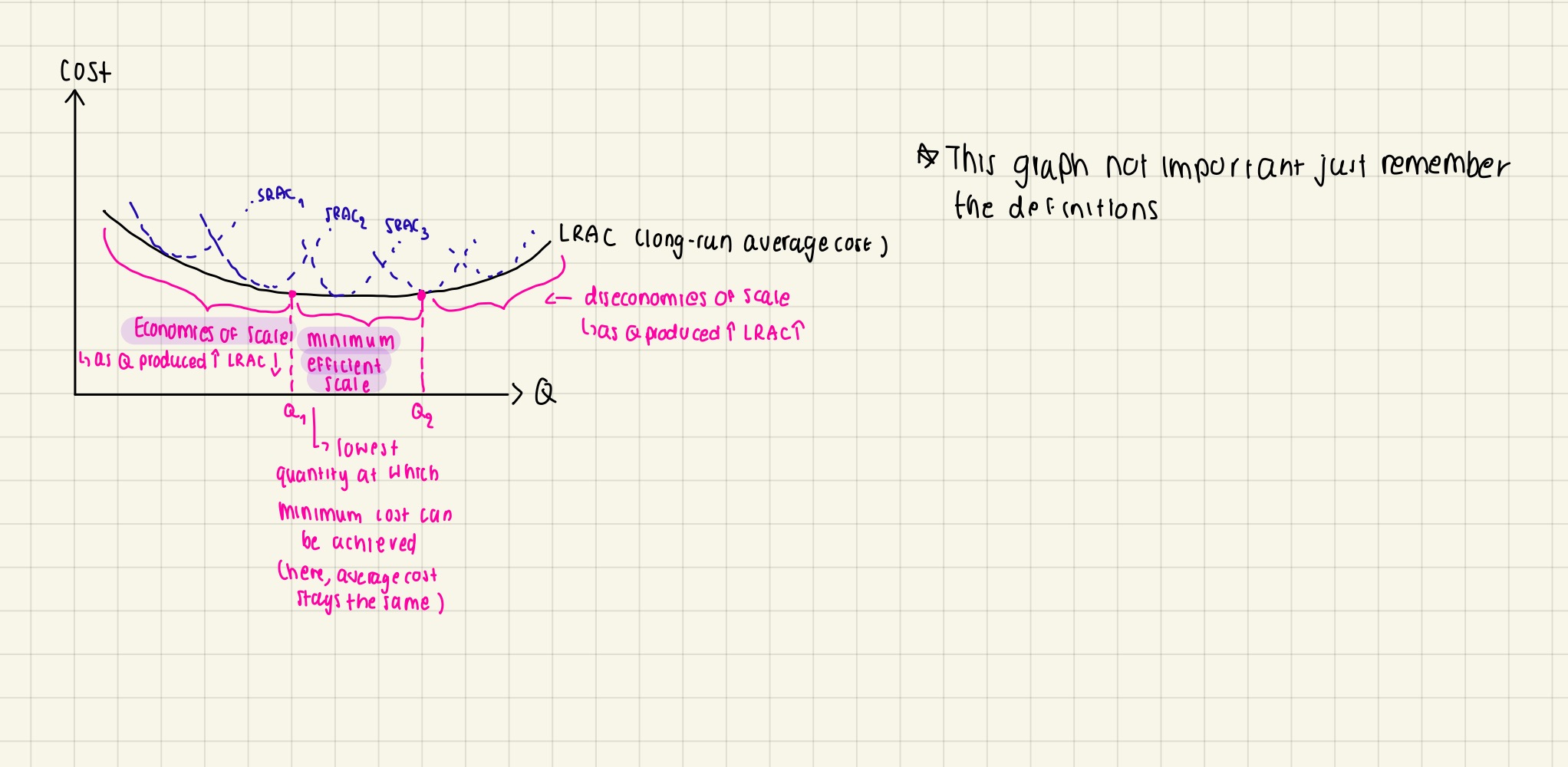

The relationship between short-run & long-run average cost curves

In the short run, at least one factor of production is fixed

output only increases when additional units of variable factors (ie. labour) are added to the fixed factor (ie. land) until diminishing marginal productivity sets in where output starts to fall

In the long run, all factors of production are variable, not fixed so won’t experience diminishing marginal productivity. Therefore, the cost curve will be slightly different

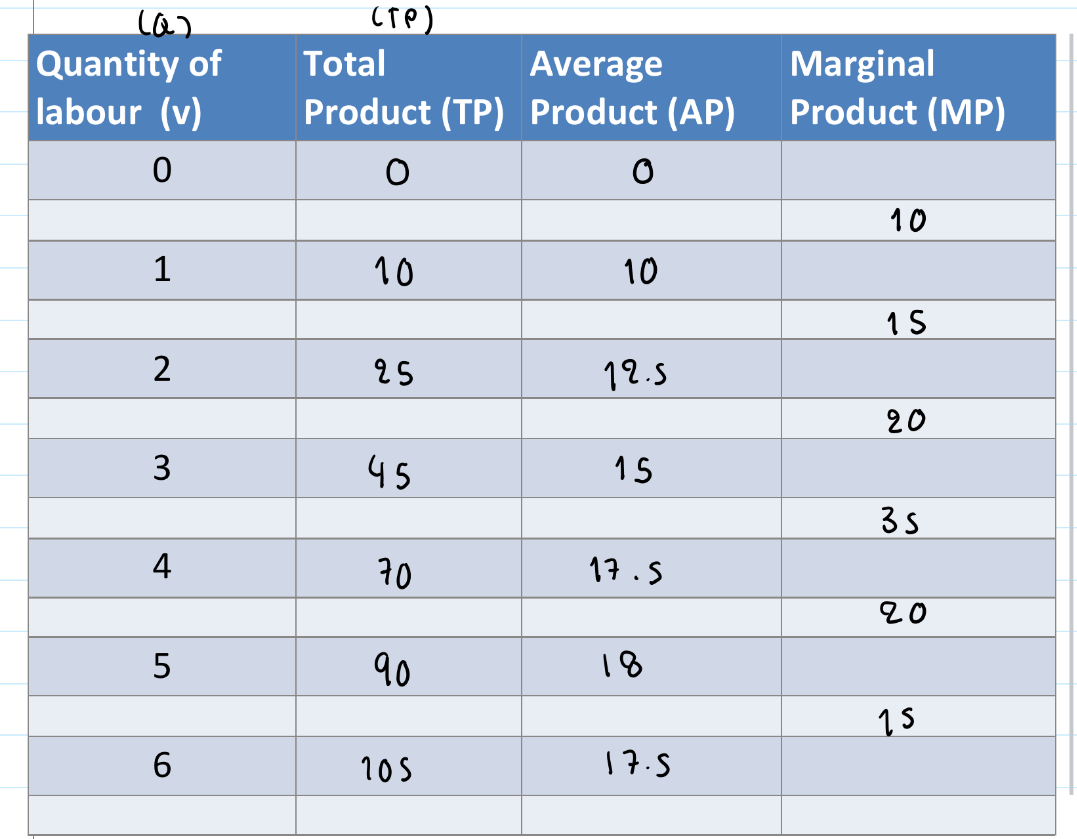

Example of production in the short run shown in a table

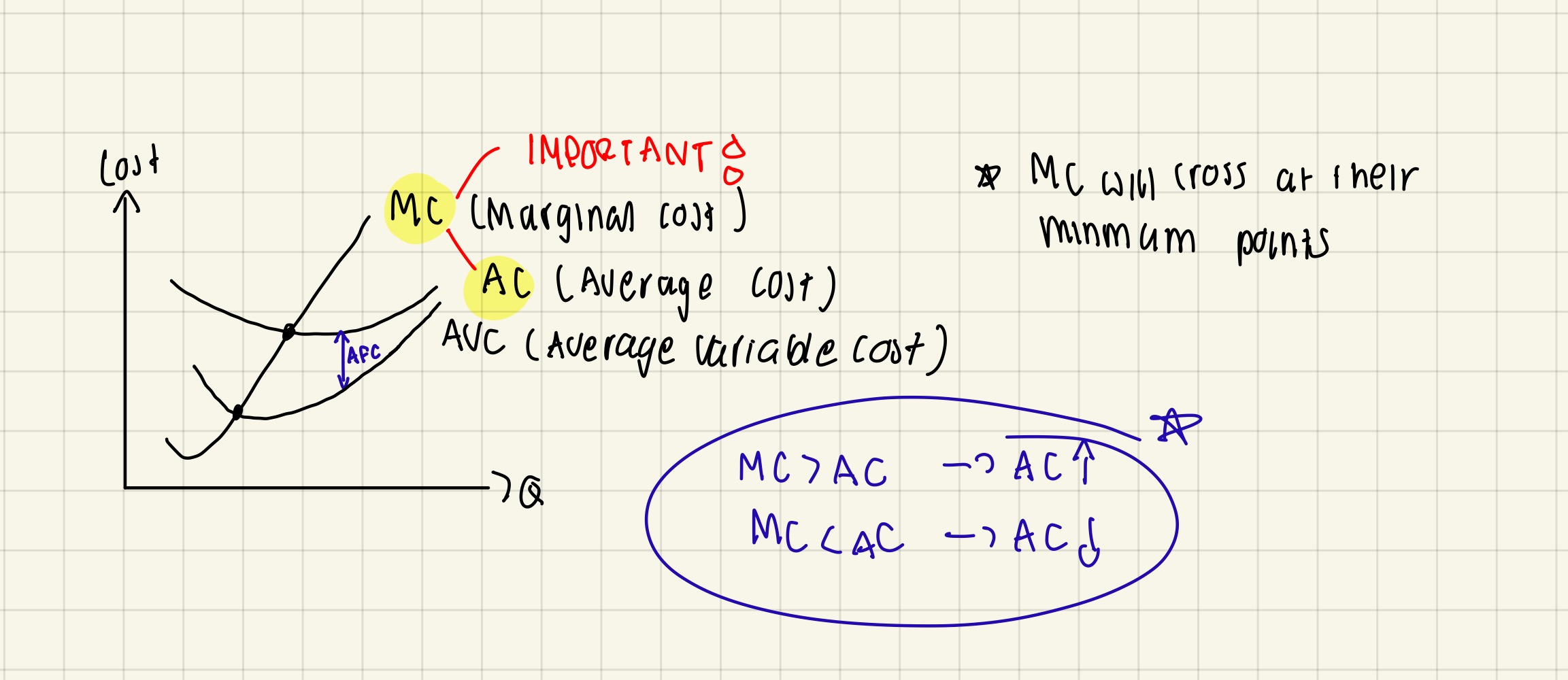

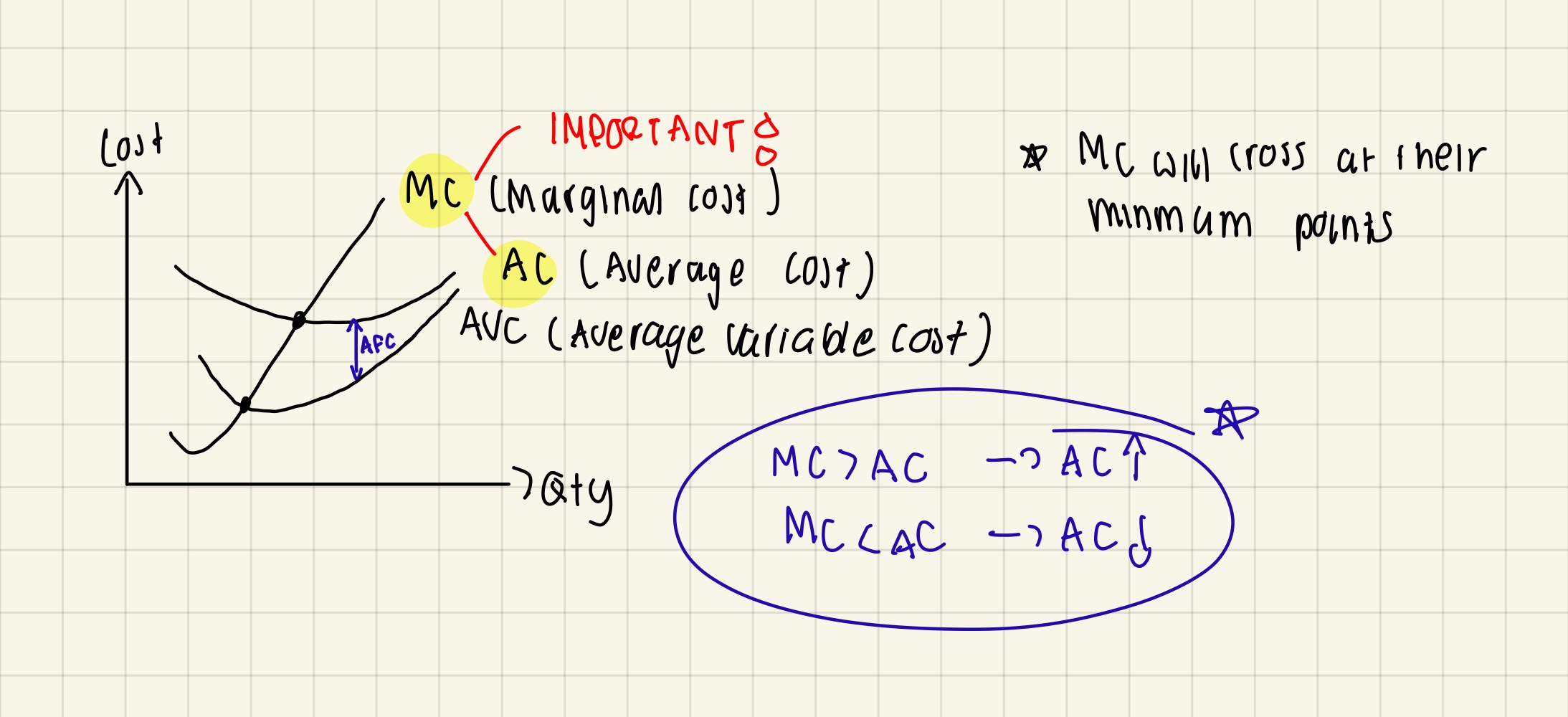

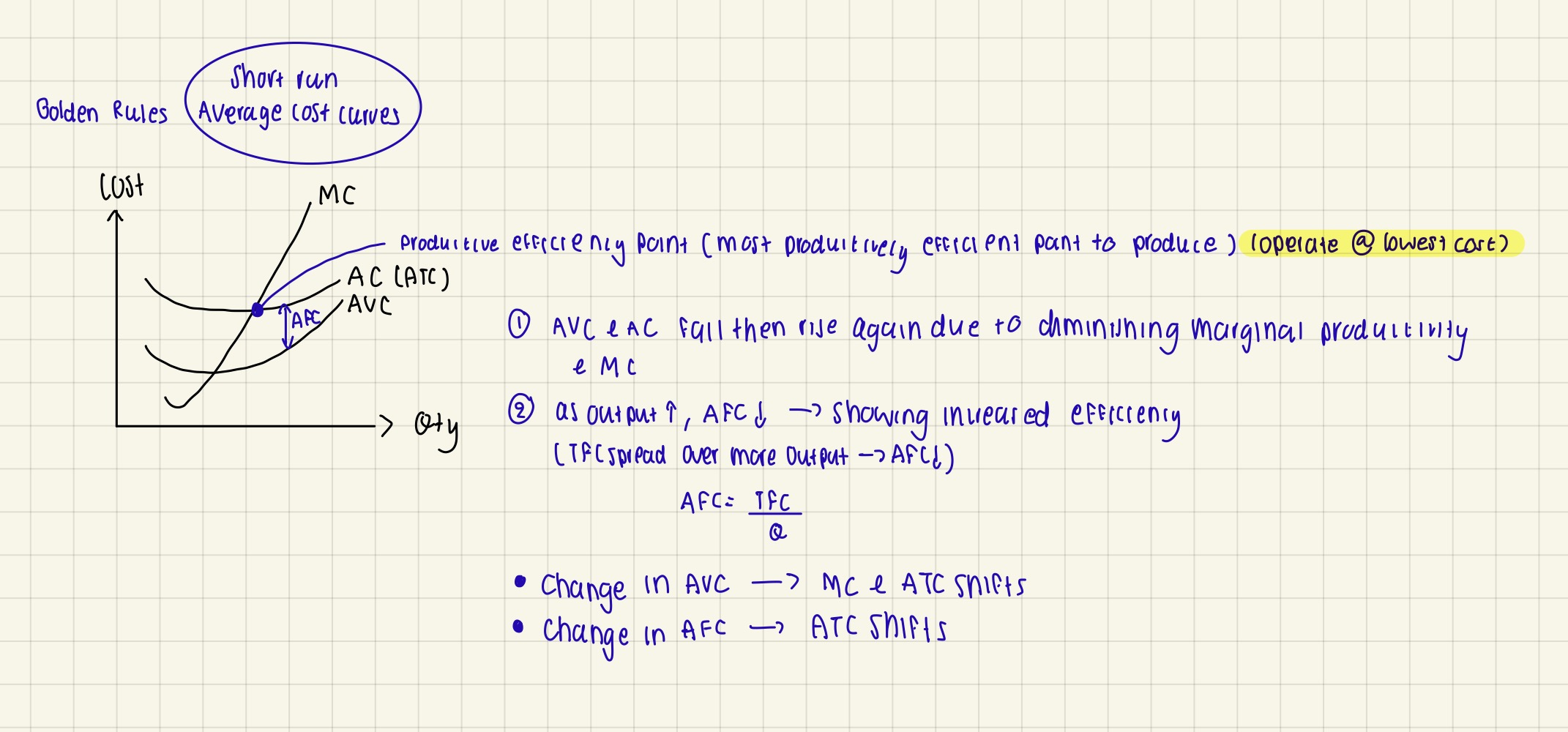

Relationship between average cost & marginal cost & TC

IMPORTANT: MC always cut AC at its lowest point which can be explained by the following:

If marginal cost above average cost → average cost rise → TC increases at a faster rate

If marginal cost below average cost → pulls down average cost → average cost fall

If marginal cost = average cost → average cost stays the same

asks a lot in exam

Golden rule when drawing short run average cost curves

Diminishing marginal returns question (3) + mcq

1) Law (use this as definition): As variable factors are added to a fixed factor, MC eventually rise

2) Only happens in the short run only where there is atleast one fixed factor (as in the long run, these these fixed factors can become variable)

2) Definition of MC