Looks like no one added any tags here yet for you.

Aggregate Demand

The quantity demanded of all goods and services at different price levels, ceteris paribus

Aggregate Supply

The quantity supplied of all goods and services at different price levels, ceteris paribus

Automatic Fiscal Policy (Non-Discretionary Fiscal Policy)

Changes in the government expenditures and/or taxes that occur automatically without (additional) congressional action

Budget Deficit

A shortfall of tax revenue from government spending

Contractionary Fiscal Policy

Decrease in government spending and/or increase in taxes to reduce economic growth

Crowding Out

The decrease in private expenditures that occurs as a consequence of increased government spending or the financing needs of a budget deficit

Discretionary Demand-Side Fiscal Policy

Deliberate changes of government expenditures and/or taxes to achieve particular economic goals

Expansionary Demand-Side Fiscal Policy

Increases in government expenditures and/or decreases in taxes to achieve particular economic goals

Fiscal Policy

Changes in government expenditures and/or taxes to achieve economic efficiency

Inflationary Gap

The condition where the Real GDP the economy is producing is greater than the Natural Real GDP and the unemployment rate is less than the natural unemployment rate

Interest Rate Effect

The changes in household and business buying as the interest rate changes

International Trade Effect (Net Export Effect)

The change in foreign sector spending as the price level changes.

Marginal Propensity to Consume (MPC)

The ratio of the change in consumption to the change in disposable income.

1 - MPS

Marginal Propensity to Save (MPS)

The ratio of the change in saving to the change in disposable income.

1 - MPC

Menu Costs

The cost of changing prices

Multiplier

The number that is multiplied by the change in autonomous (new) spending to obtain the overall change in total spending

Public (National) Debt

The total amount the federal government owes its creditors

Real Balance Effect

The changes in the purchasing power of dollar-dominated assets that results from a change in the price level

Recessionary Gap

The condition where the Real GDP the economy is producing is less than the Natural Real GDP and the unemployment rate is great than the natural unemployment rate

Say's Law

Supply creates its own demand. Production creates demand sufficient to purchase all goods and services produced.

Short-Run Equilibrium

The condition that exists in the economy when the quantity demanded of Real GDP equals the (short-run)quantity supplied of Real GDP. Shown by where the AD curve intersects the SRAS

Stagflation

The simultaneous occurrence of high rates of inflation and unemployment

Supply-Side Fiscal Policy

Fiscal policy centered on tax reductions targeted to aggregate supply so that real GDP increases with very little or no inflation. The main justification is that lower taxes on individuals and firms increase incentives to work, save, invest, and take risks

Autonomous Change in Aggregate Spending

Is an initial rise or fall in aggregate spending that is the cause, not the result, of a series of income in spending changes

Wealth Effect

The change in the consumer spending caused by the altered purchasing power of consumer assets

Monetary Policy

The central banks use the changes in the quantity of money or the interest rate to stabilize the economy

Aggregate Supply Curve

Shows the relationship between the aggregate price level and the quantity of aggregate output supplied in the economy

Nominal Wage

Dollar amount of the wage paid

Sticky Wages

Nominal wages that are slow to fall even in the face of high unemployement and slow to rise even in the face of labor shortages

Short-run Aggregate Supply Curve

relationship between the aggregate price level and the quantity of aggregate output supplied that exists in the short run, the time period when many production costs can be taken as fixed

Long-run Aggregate Supply Curve

shows the relationship between the aggregate price level and the quantity of aggregate output supplied that would exist if all prices, including nominal wages, were fully flexible

Potential Output

the level of real GDP the economy would produce if all prices, including nominal wages, were fully flexible

AD-AS model

aggregate supply curve and aggregate demand curve are used together to analyze economic fluctuations

Short-run Macroeconomic Equilibrium

when the quantity of aggregate output supplied is equal to the quantity demand

Short-run Equilibrium Aggregate Price Level

the aggregate price level in the short run macroeconomic equilibrium

Short-run Equilibrium Aggregate Output

is the quantity of aggregate output produced in the short-run macroeconomic equilibrium

Demand Shock

An event that shifts the aggregate demand curve

Supply Shock

An event that shifts the short-run aggregate supply curve is a supply shock

Long-run Macroeconomic Equilibrium

when the point of short-run macroeconomic equilibrium is on the long-run aggregate supply curve

Output Gap

percentage difference between actual aggregate output and potential output

Self-Correcting

When the shocks to aggregate demand affect aggregate output in the short run, but not the long run

Stabilization Policy

The use of government policy to reduce the severity of recessions and rein in excessively strong expansion

Expansionary Fiscal Policy

Increases aggregate demand

Lump-Sum Taxes

are taxes that don't depend on the taxpayers income

Tax Multiplier

tax increase = -MPC / MPS; tax cut MPC / MPS. Always 1 less than comparable spending multiplier.

Recognition Lag

The time it takes for policy makers to recognize the existence of a boom or a slump.

Administrative Lag

The time it takes for Congress to agree on a course of action with the president.

Operational Lag

Spending/planning takes time to organize and execute (changing taxing is quicker).

Crowding-Out Effect

Government spending might cause unintended effects that weaken the impact of the policy.

Net Export Effect

Works through international trade to reduce the effectiveness of fiscal policy.

Beliefs of Classical Theory

1. A change in AD will not change output even int he short run because prices of resources (wages) are very flexible.

2. AS is vertical so AD can't increase without causing inflation.

Classical Theory

The economy self-adjusts to deviations from its long-term growth trend. No government involvement is required.

Beliefs of Keynesian Theory

1. A decrease in AD will lead to a persistent recession because prices of resources (wages) are NOT flexible.

2. Increase in AD during a recession doesn't cause inflation.

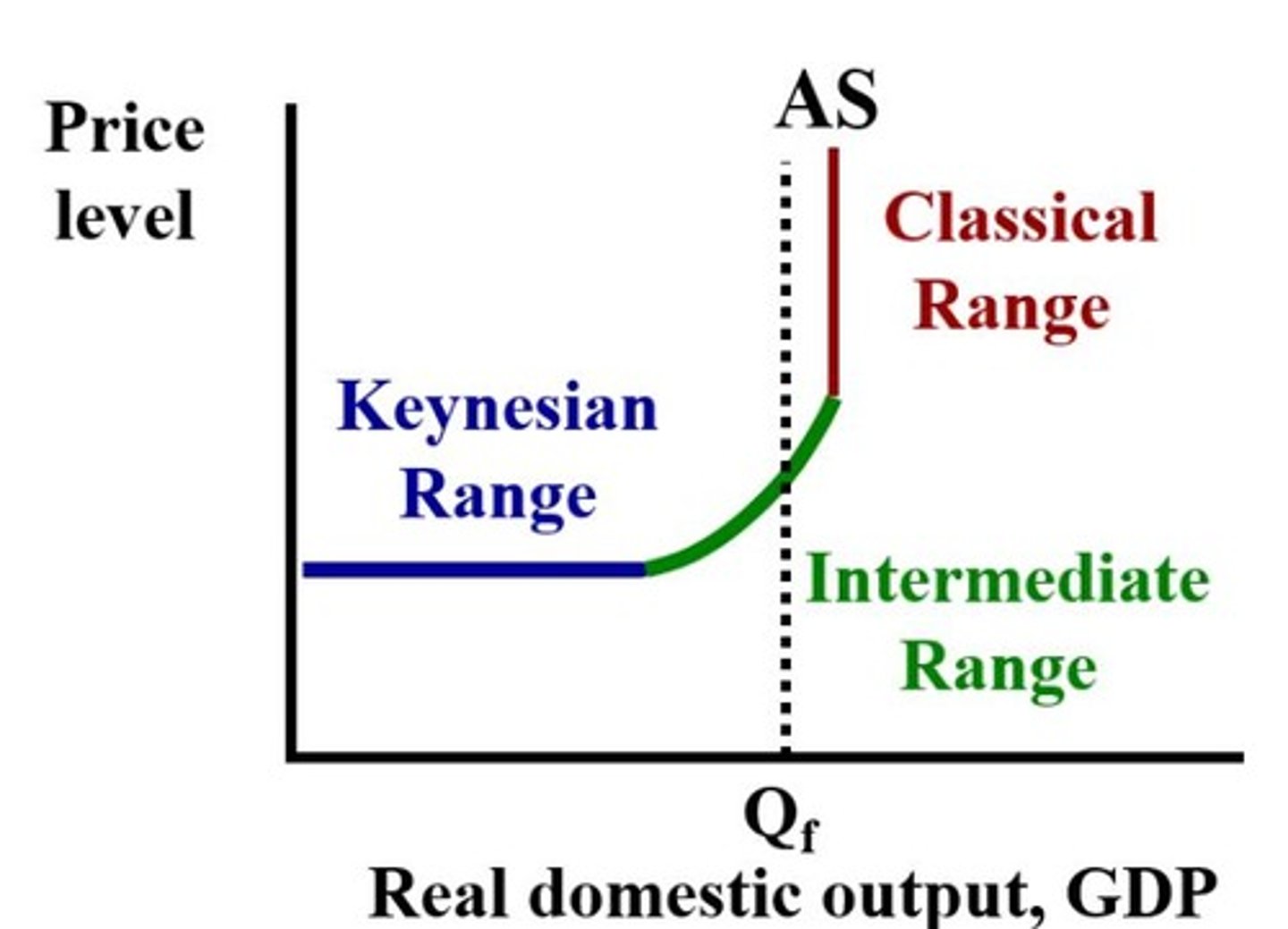

Keynesian's 3 Ranges of Aggregate Supply Curve

1. Keynesian Range - Horizontal at low output.

2. Intermediate Range - Upward sloping

3. Classical Range - Vertical at physical capacity

Keynesian Range of Keynesian AS Curve

Shifts of the aggregate demand curve in this range lead to changes in the aggregate output, but not changes in price level.

Intermediate Range of Keynesian AS Curve

The positively-sloped segment of the Keynesian aggregate supply curve that reflects the trade-off between aggregate output and the price level. Shifts of the aggregate demand curve in this range lead to changes in both aggregate output and the in price level.

Classical Range of Keynesian AS Curve

The vertical segment of the Keynesian aggregate supply curve that reflects the independence of full-employment aggregate output (or gross domestic product) to the price level. Shifts of the aggregate demand curve in this range lead to changes in the price level, but not changes in aggregate output.

Aggregate Demand Curve

Shows the relationship between the aggregate price level and the quantity of aggregate output demanded by households, businesses, government and the rest of the world (C+I+G+Xn).