Market failure and socially undesirable outcomes 3

1/88

Earn XP

Description and Tags

Profit maximisation, perfect competition, monopolies

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

89 Terms

revenues definition

payments that firms receive when they sell the goods and services that they produce.

total revenue vs average revenue

total revenue = PxQ → amount of money a firm gets when they sell a g/s

average revenue = TR/Q = P → revenue per unit output sold

marginal revenue

formula = change in TR/ change in quantity

additional revenue from producing one more unit of output

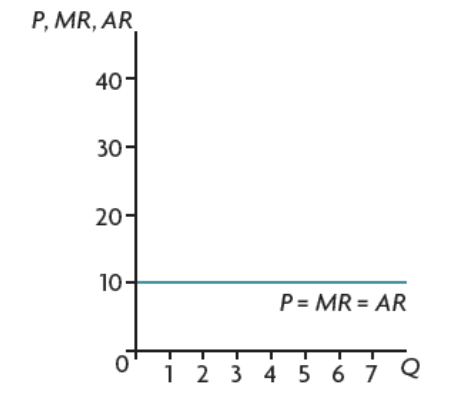

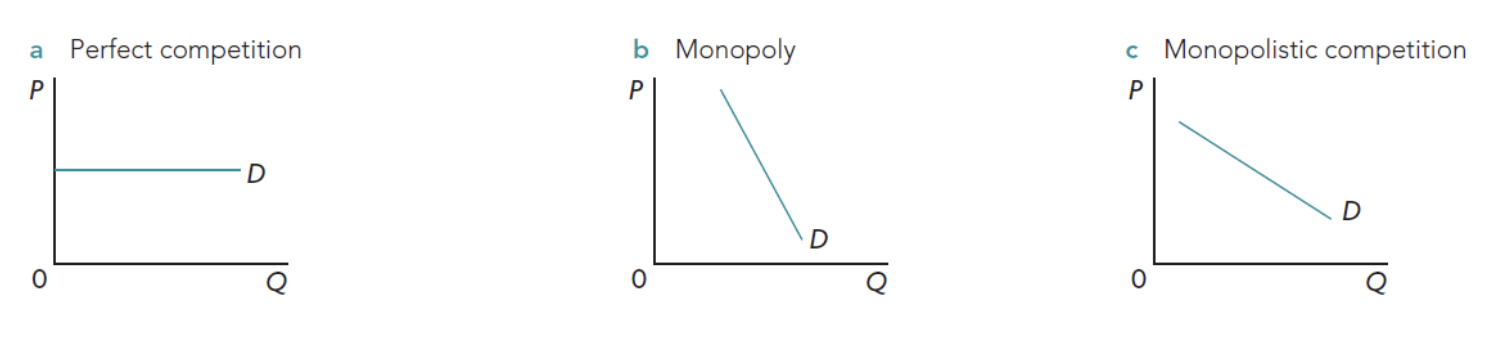

average + marginal revenue for price taker firms

AR=MR=P

straight horizontal line → price is constant

price taker vs price maker

price taker → cannot control the price → exists with perfect competition (price does not change with output)

price maker → can set their own price → monopoly, oligopoly, monopolistic competition (price changes with output)

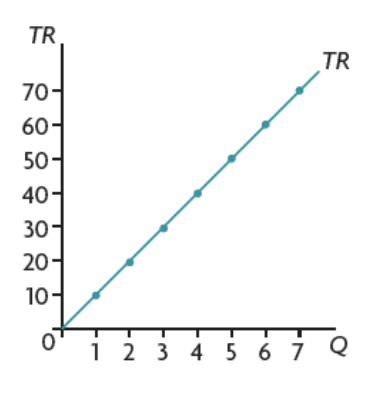

total revenue for price taker firms

increases by the same amount

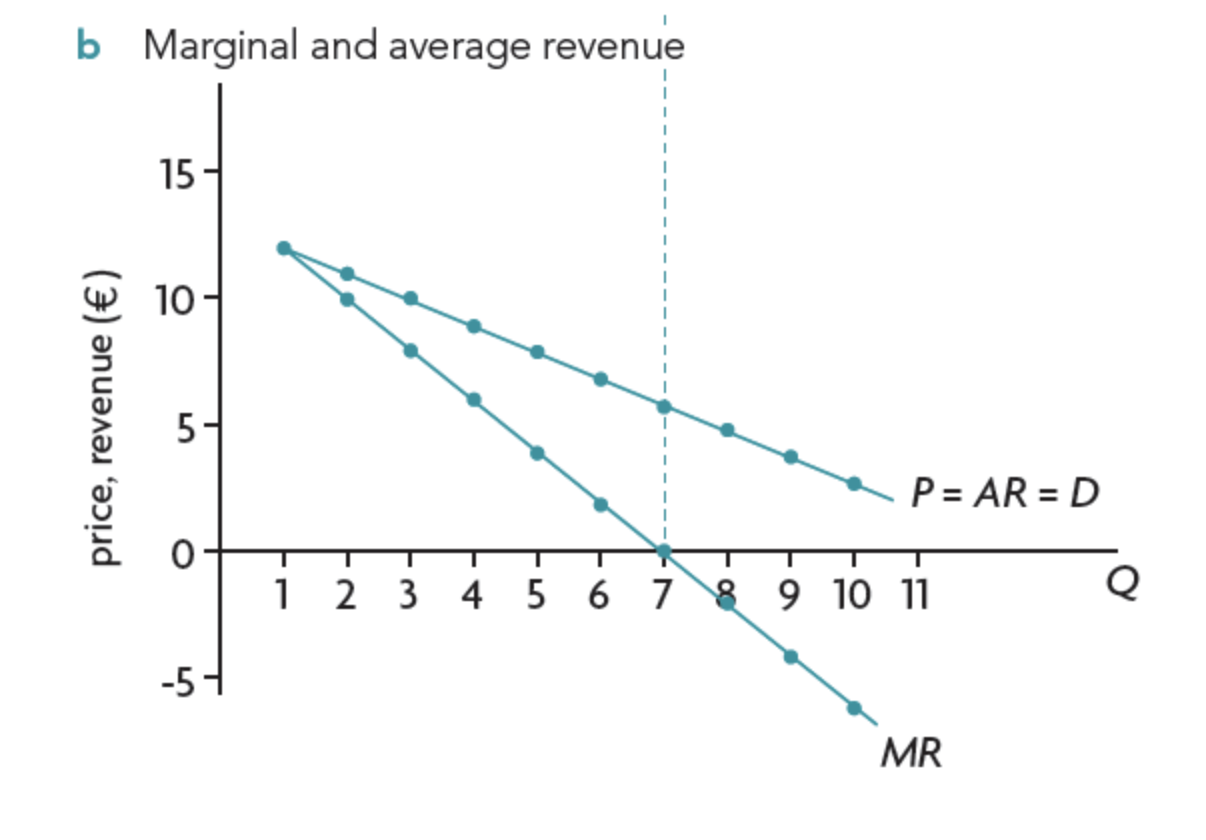

Average revenue + marginal revenue for price maker firms

MR is twice as steep as AR

MR is negative → firm is loosing revenue with each extra unit of output

when MR = 0 TR is at maximum

Total revenue for price maker firms

revenue is maximized at the local maximum (where MR=0)

PED and TR

PED is rel. elastic → price increases → TR increases

PED is rel. inelastic → price increases → TR decreases

costs of production definition

payments by firms to obtain and use factors of production in their production process

fixed vs variable costs definition

fixed - costs that don’t change with output (short run)

variable - costs that change with output

Total costs

total amount of money spent on producing a certain quantity

= fixed + variable costs

Average costs

costs per unit output produced

average fixed costs + average variable costs

Marginal cost

additional costs to produce an extra unit of output

= change in total costs / change in quantity

the relationship between average costs + marginal costs in the short run

MC<AC → average cost is falling

MC>AC → average cost is rising

MC intersect AC at AC’s minimum

what is meant by short run vs long run

short run - at least one factor of production is fixed

long run - all factors of production are variable

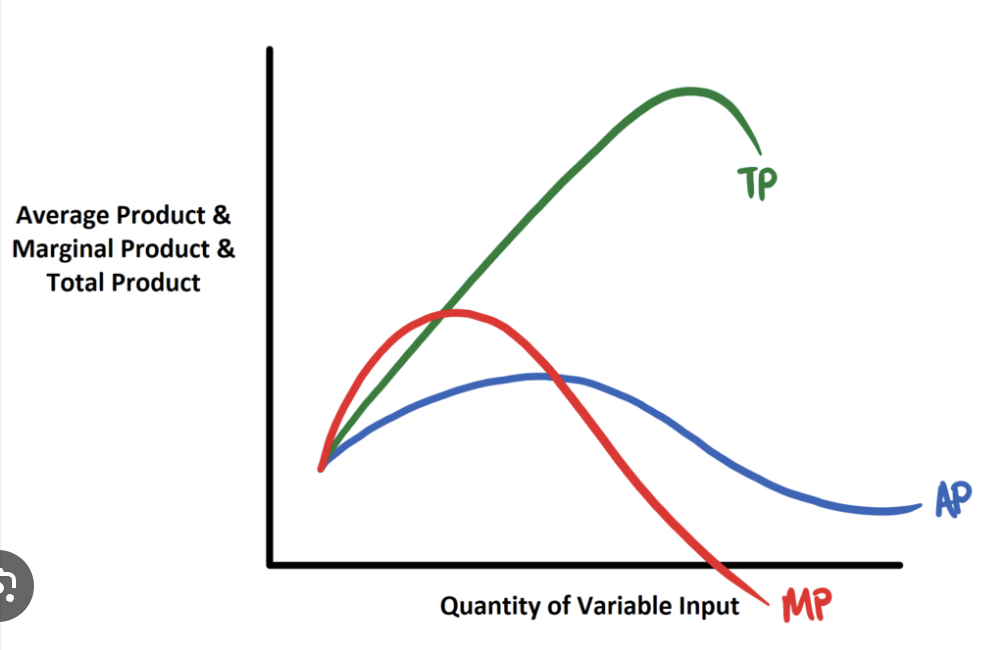

total product vs marginal product

total - the total quantity of output produced by a firm

marginal - the additional output that results from one additional variable input

relationship between marginal and total product

when MP=0, TP is maximized

when MP is rising TP rises faster

when MP is falling TP falls slower

relationship between marginal and average product

MP>AP → AP increases

MP<AP → AP decrease

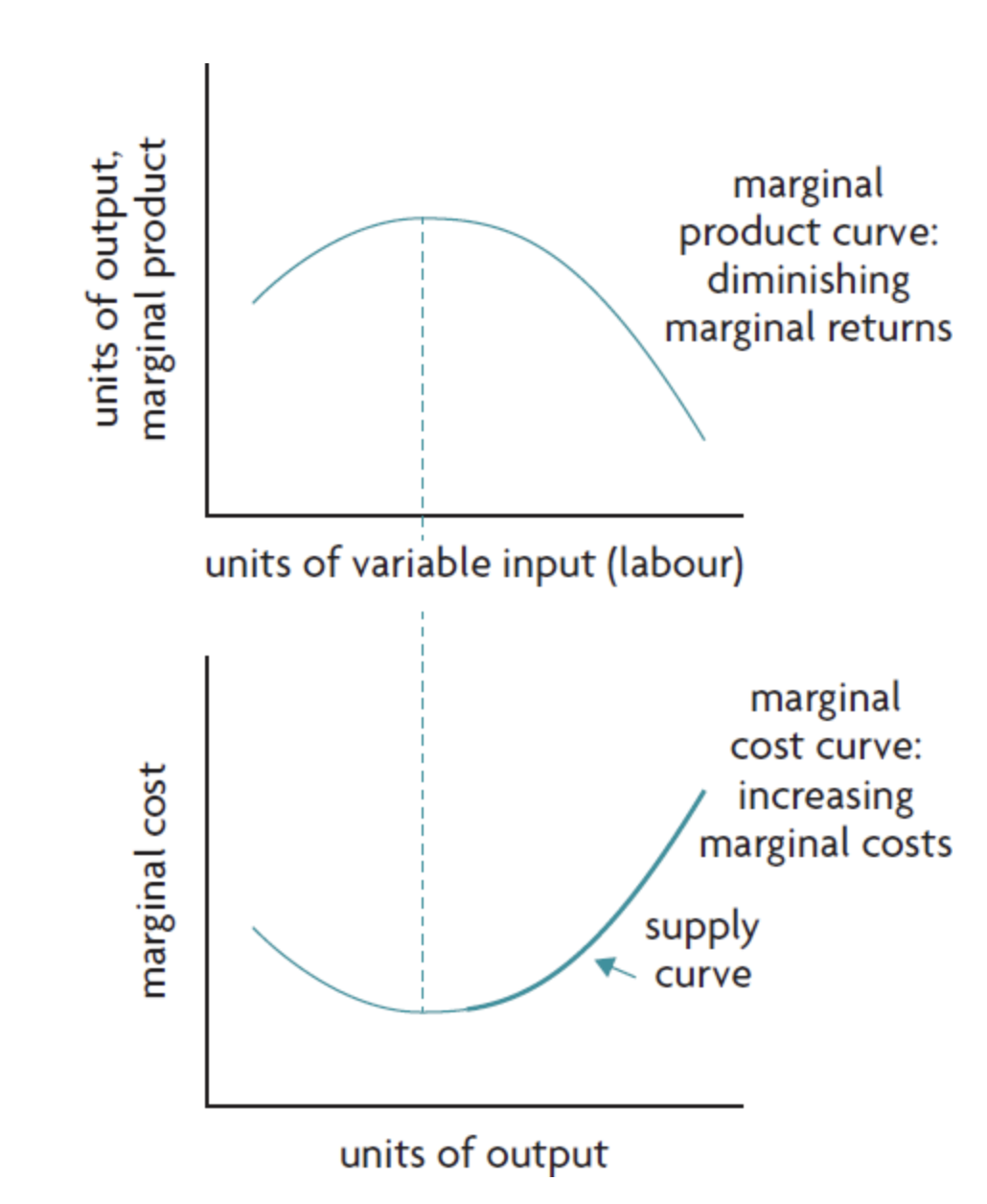

law of diminishing marginal returns

as more and more units of a variable input are added to one or more fixed inputs the marginal product of the variable input at first increases, but then it reaches a point after which the marginal product of the variable input starts to decrease

relation of marginal costs to diminishing marginal returns

marginal product increases → marginal cost decreases

when marginal product is at maximum → marginal costs is at minimum

when marginal product falls → marginal costs increase

marginal costs and the firms supply curve

upward sloping part of MC curve = supply curve

the firm can only produce more output if the price of the good increases to cover the extra cost of each extra unit produced

explicit vs implicit costs

explicit - direct, out-of-pocket payments that businesses actually make, e.g wages, rent, materials, and utility bills.

implicit - opportunity costs - value of resources the firm already owns but could have used elsewhere (not used when calculating accounting profit)

profit formulas

revenue - costs of production

economic profit = total revenues - economic costs

total revenue - sum of explicit costs - implicit costs

(economic costs = implicit + explicit costs)

profit maximization

producing a level of output where the difference between total revenue and total costs is the largest

largest amount of profit

rewards for f.o.p

land - rent

labour - wages

capital - interest

enterprise - profit

→ the costs of a business

normal profit

the minimum amount of revenue that the firm must receive in order to keep the business running

TR=TC

normal profit also = the opportunity cost of running the business instead of doing something else.

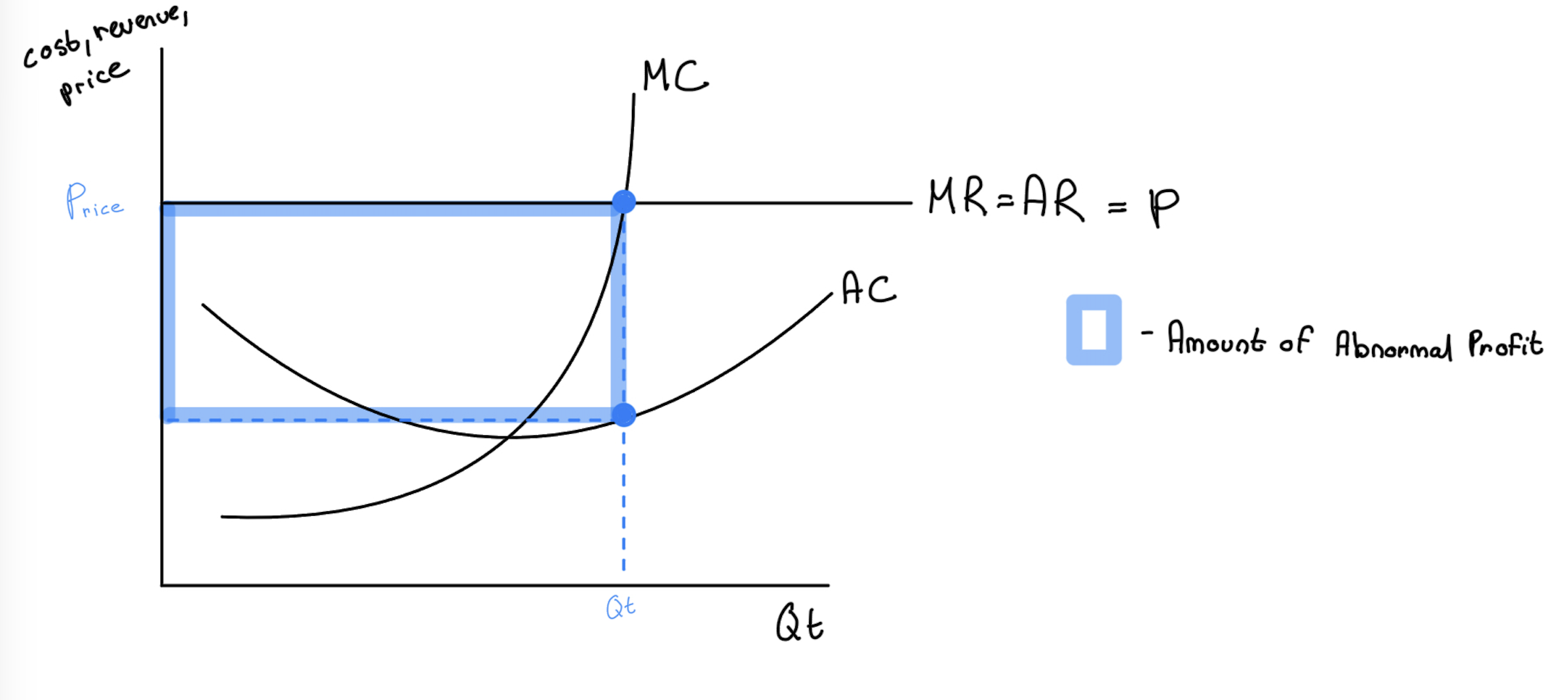

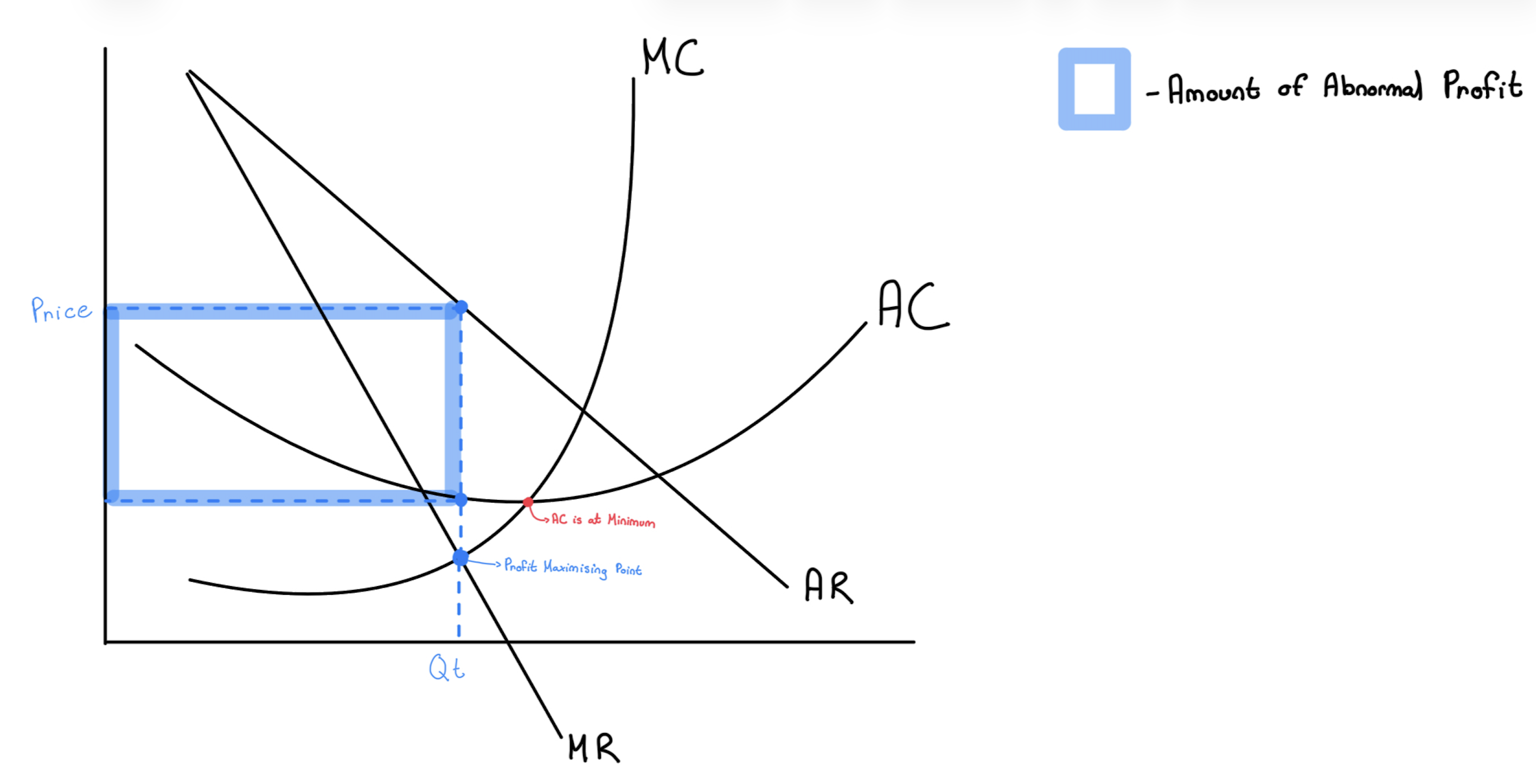

abnormal/supernormal profit

TR>TC

more than normal profit is made

losses

TR<TC

less than normal profit is made

profit maximization - price takers

AR>AC → abnormal profit

AR=AC → normal profit

MC=MR → profit maximization

minimizing loss - price takers

when AR<AC

MC=MR → minimize loss

profit maximization - price makers

MR=MC

as long as MR>MC the profit can be increased by producing more units until the last unit of output brings not more profit (MC=MR)

types of market structure

perfect competition

monopolies

oligopoly

monopolistic competition

(monopolies, oligopoly, monopolistic competition → imperfect competition)

conditions for normal profit + profit maximization

normal profits : AC=AR

Profit maximisation : MC=MR

conditions for productive + allocative efficiency

productive efficiency - AC=MC

allocative efficiency= S=D/MC=AR

Assumptions for perfect competition

large number of small firms + many small households/consumers

no barriers to market entry/exit

firms are price takers : AR=MR=P

homogenous/identical products → perfect substitutes for each other

perfect information about costs, revenues, etc.

examples of perfect competition

there are no existing perfectly competitive markets but a few come close:

agricultural markets (wheat,corn)

online market places - eBay, Amazon

Raw material markets

what happens in the market when businesses in perfect competition are making abnormal profit

more businesses enter the market due to perfect information + no barriers to entry → lowers price

This happens until the AR curve is a tangent to the AC curve

effect of more firms entering the market in perfect competition

increase in supply → increase in competition as goods are perfect substitutes for each other → fall in price due to excess supply → expansion of demand

each firm now has lower AR + MR → abnormal profit falls

perfect competition short run - allocative efficiency, normal profit, profit maximization, productive efficiency

Yes:

allocative efficiency

profit maximisation

No:

normal profit

productive efficiency

perfect competition long run - allocative efficiency, normal profit, profit maximization, productive efficiency

all are present

allocative efficiency

normal profit

profit maximisation

productive efficiency

→ stable

benefits of perfect competition

allocative efficiency

low prices for consumers due to absence of abnormal profits

closing down of inefficient producers due to competition

market responds to consumer tastes - changes in consumer tastes → change in market demand + market price

limitations of perfect competition

relies unrealistic assumptions that are rarely met in the real world

no economies of scale - firms are too small

lack of product variety - firms produce homogenous products but consumers prefer variety

limited ability to engage in product development - lack of abnormal profit → cannot fund research + innovation

Monopoly definition

A market structure with a single supplier of a good or service and that has control over the market price. The firm sells a unique product and is protected by high barriers to entry

characteristics/assumptions of a monopoly

single supplier = market supply

price maker

High barriers to entry + exit

Differentiated goods and services without close substitutes.

Average revenue curve for monopolies

= market demand due to monopoly being the single supplier.

Why do barriers of entry + exit arise in monopolies

economies of scale

legal barriers

control of essential resources

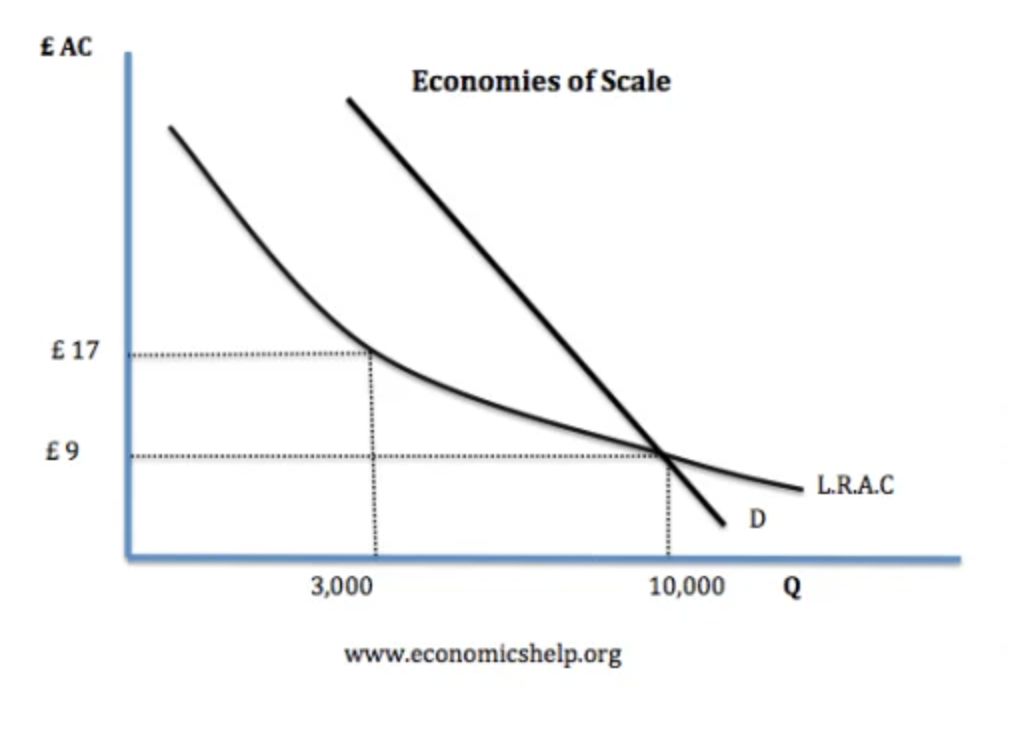

natural monopoly

Aggressive tactics

economies of scale - Monopolies

= lower average costs of production in the long run resulting from being a large firm.

occurs in the downward sloping part of a firms long run average revenue curve.

Occurs due to :

bulk buying

specialisation of labour

lower costs for marketing

lower borrowing costs

legal barriers - Monopolies

applies to all imperfect competition

patent = temporary monopoly for an inventor

Licences - granted by governments for a certain profession/industry

copyrights = temporary monopoly for artistic output

tariffs/quotas

all limit competition and so create market power

aggressive tactics (limit pricing) - Monopolies

monopolist sets a price with which any new market entry cannot compete with and therefore preventing entry to the market

illegal

natural monopoly

a situation where a single firm will be able to supply a greater amount of output at a lower price than if more than one firm were to compete

due to high capital costs + high economies of scale enjoyed by monopolist.

Example of natural monopoly

Bratislava water company (BVS)

builds an expensive pipeline network. If multiple firms were to compete each firm would have to build its own pipelines leading to higher costs, inefficiencies and waste of resources.

how to know if a firm is a natural monopoly on a graph

market demand for a g/s intersects LRAC (long-run average costs) whilst it is falling.

how can natural monopolies stop being ‘natural’

if changing technologies create conditions which allow new competitor firms to enter the industry and begin production at a relatively low cost.

advantages of monopolies

abnormal profit → funds for R&D→ can boost innovation

economies of scale → lower costs of production (see graph in notes)

Natural monopolies - can supply a greater amount + at lower price

disadvantages of monopolies

limited choice for consumers due to lack of competition

Higher prices for consumers (profit maximising monopolist)

Allocatively inefficient → creates DWL

Productively inefficient market outcome

X inefficiency → average costs are not as low as AC curve due to lack of competition

Mylan (Epipens) monopoly

Pharmaceutical monopoly (over 90% market share)

ad : abnormal profits allow for R&D which helps improve epipens

dis : increased the price by over 400% → low income earners struggle to afford Epipens

why are monopolies allocatively inefficient

P>MC at profit-maximising level of output

there is an underallocation of resources

market power definition

the ability of a firm to charge a price greater than marginal costs (P>MC)

can only occur when a firm experiences a downwards sloping demand curve (imperfect competition)

characteristics of an oligopoly

small number of large firms

high barriers to entry - all barriers as in monopoly + high start up costs (spend a lot on product differentiation + advertising)

interdependence - decisions made by one firm greatly impact other firms in the industry

products are differentiated

imperfect information

Quite strong market power (depends on concentration of market which can be found through concentration ratio)

affect of interdependence on oligopoly behaviour

Strategic behaviour

Conflicting incentives : incentive to cheat, incentive to collude

strategic behaviour oligopoly

Firms use analysis (like game theory) to predict competitor reactions, deciding whether to cooperate or compete.

conflicting incentives - oligopoly

incentive to collude - fix price + reduce quantity → maximize profits for industry as a whole

incentive to cheat - want to capture a portion of rivals’ market share + profits → increasing profits at the expense of other firms

Types of oligopoly

collusive oligopoly : firms overcome uncertainty by charging the same price or splitting the market geographically → act like a monopolist.

non-collusive oligopoly : businesses charge similar prices (competitive pricing) use non-price competition e.g design,durability,customer service

types of collusive oligopolies

formal collusion (cartel) : firms openly agree on a price to charge consumers.

tacit collusion : firms charge the same price without a formal agreement → price leadership (dominating firm decides the market price with other firms following). if price leadership is done to restrict competition = illegal.

advantages for firms in a cartel

increase in market power → can influence price

increased profits due to higher price

elimination of competition → remove uncertainty

game theory definition

a mathematical technique analysing the behaviour of decision-makers that are dependent on each other and who use strategic behaviour to try and anticipate the behaviour of their rivals.

prisoner’s dilemma

2 rational decision makers that use strategic behaviour to maximize profits collectively end up being worse off. (at Nash equilibrium)

prisoner’s dilemma oligopoly

the incentive to cheat for each firm makes it most likely that both firms will cut prices leading to price competition and a failure of the collusive agreement

payoff matrix definition

shows all the possible combinations of outcomes of different decisions made by the players in game theory

price war definition

competitive price cutting by firms (usually oligopoly) as each one tries to capture market shares from rival firms → lower profits for both firms

why are cartels difficult to maintain

incentive to cheat

cost differences between firms - AC differences make it hard to agree on a price

number of firms - a lot of firms → difficult to come to an agreement

possibility of price war -

non-collusive oligopolies and competition

avoid price competition due to wanting to avoid price wars

compete with non-price factors such as advertising, branding, warranty, packaging,etc. → create high barriers to entry through strong product differentiation

why is non-price competition important to oligopolies

oligopolies have large profits which they can use to fund things such as branding and R&D

development of new products → increase in market power → demand for firms’ product becomes less price elastic → increased sales + profits

product differentiation → increase in profit due to it taking time for rivals to develop new competitive products

oligopolies + stable prices

fear of loosing sales revenue/market share if price rises

fear of price war when cutting prices

“price a” may remain profit maximising price even if marginal costs increase

concentration ratio

a measure of how much an industry’s production is concentrated amongst the industry’s largest firms

measures percentage of output produced by the largest firms in an industry

used to indicate degree of competition/market power

higher ratio = more market power = less competition

market concentration

the degree to which a market is dominated by a small number of large firms controlling the market

measured using concentration ratio

concentration ratio disadvantages

do not reflect competition from abroad

do not reflect competition from other industries that act as substitutes

do not distinguish between sizes of largest firms

no indication of importance in global market

Advantages of oligopolies

economies of scale → lowers costs of production (only benefit consumers if producers lower price as a result)

promotes product + process innovation → dynamic efficiency → falling long run costs of production

advertising + other marketing activities create jobs + income

advertising provides information to consumers + reduces search costs

Disadvantages of oligopolies

allocative inefficiency + welfare loss

higher prices + lower quantities compared to perfect competition

loss in consumer surplus due to high price P>MC

less efficient/higher production costs due to lack of competition

too much product choice → consumers are overwhelmed + creates disutility

example of collusive oligopolies

OPEC - Organisation of the Petroleum Exporting Countries

price fixing + output restriction

limited firms : OPEC nations

examples of non-collusive oligopoly markets

smartphone market (apple vs samsung)

softdrinks market

assumptions of monopolistic competition

large number of firms + consumers

low barriers to entry

perfect knowledge

differentiated products (real/imagined) → price setting power

downward sloping demand curve that is relatively price elastic due to competition (more elastic than monopoly but less elastic than perfect competition)

how can product differentiation be achieved in monopolistic competition

physical differences

quality differences

location

services

product image

price vs non-price competition

price - firm lowers prices to attract customers from rival firms thus increasing sales at the expense of other firms. (occurs in monopolistic or perfect competition)

non-price - firms use methods other than price reductions to attract customers from rival firms (occurs in oligopoly or monopolistic competition)

SR vs LR of firms in monopolistic competition

abnormal profits attract new entries reducing AR/MR as demand is spread over more firms

short run losses → firms leave the industry → AR/MR increases due to demand being spread over less firms

both continue until AR=AC/AR is tangent to AC and all firms make normal profit.

market outcomes present in monopolistic competition

profit maximisation - yes

normal profit - yes

productive efficiency - no

allocative efficiency - no, P>MC/MB>MC → underallocation of resources

advantages of monopolistic competition

differentiated products → choice + gain in customer utility + satisfies needs + wants better

advertising provides information → reduces search costs

marketing activities + advertising create jobs + income

cheaper market entry → increases competition + the need to innovate in order for firms to stay competitive (dynamic efficiency)

disadvantages of monopolistic competition

productively inefficient

allocatively inefficient → DWL even in LR although less than in oligopoly

higher prices compared to perfect competition due to promotional activities which raise average costs

inability to generate economies of scale due to small size compared to oligopoly + monopoly

firms often lack sufficient funds for R&D → product development is difficult