Lvl2: Financial statement analysis

1/38

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai | Chat |

|---|

No analytics yet

Send a link to your students to track their progress

39 Terms

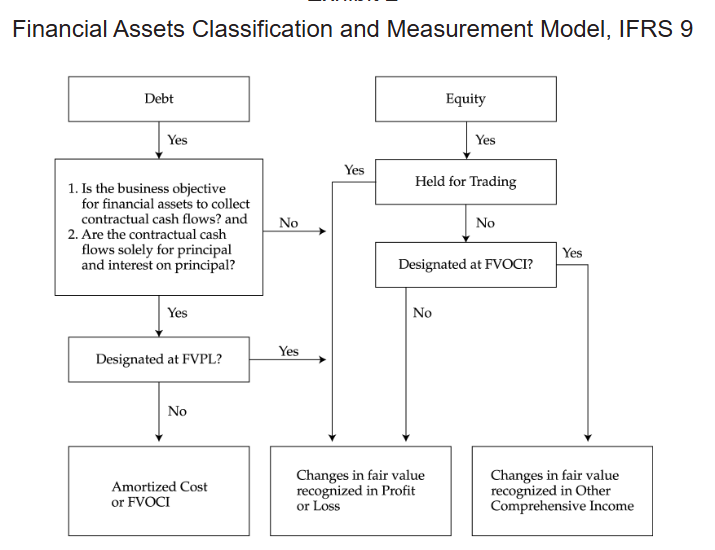

IFRS9 classification

IFRS9 reclassification

Reclassifications of debt instruments are permitted only when the business model changes. The choice to measure equity investments at FVOCI or FVPL is irrevocable.

Consolidation - contingent liabilities

recognize any contingent liability assumed in the acquisition if 1) it is a present obligation that arises from past events, and 2) it can be measured reliably.

IFRS include contingent liabilities if their fair values can be reliably measured. US GAAP includes only those contingent liabilities that are probable and can be reasonably estimated.

“Partial goodwill” vs “Full goodwill”

partial - fair value of consideration given) less the acquirer’s share of the fair value of all identifiable tangible and intangible assets, liabilities, and contingent liabilities acquired

full - fair value of the entity as a whole less the fair value of all identifiable tangible and intangible assets, liabilities, and contingent liabilities

IFRS either ; US GAAP only full

NCI

IFRS either full or partial ; US GAAP only full

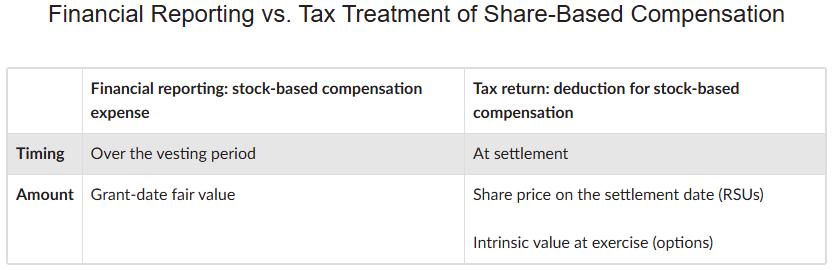

share based comp - tax

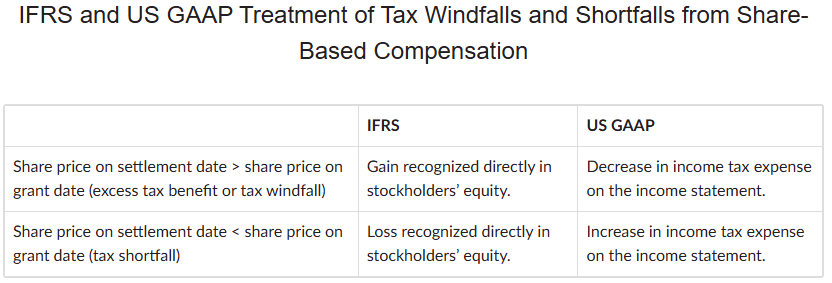

tax windfall from increase in share price

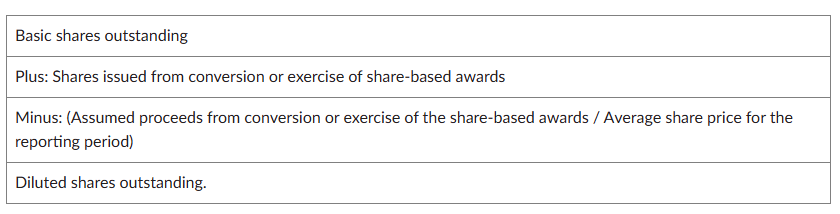

shares outstanding

Assumed proceeds from cash exercise + Average unrecognized share-based compensation expense

In-the-money options (average share price > strike price) are dilutive and included in diluted shares outstanding.

Out-of-the-money and at-the-money options are anti-dilutive and left out of diluted shares outstanding.

RSUs are dilutive except when the average stock price is materially below the stock price at the RSU grant date. This can result in anti-dilutive RSUs because the unrecognized stock-based compensation expense is based on grant date share prices.

Funded status

Funded status = Fair value of plan assets – Pension obligation

Pension obligation = The present value, without deducting any plan assets, of expected future payments required to settle the obligation resulting from employee service in the current and prior periods.

different plans’ funded statuses cannot be netted

Pension expense - IFRS

Service cost - PL operating- current (from service in current period); past

Net interest expense/income - PL financing - pension obligation accretion

Remeasurement - OCI - actuarial + actual vs assumed rate

Pension expense - GAAP

Current service cost - opex

Interest cost - int exp - gross - pension obligation unwinding

Expected return on plan - offset in earnings - expected rate of return

Amortization of past service cost - OCI

Amortization of net gains or losses - PL or OCI - actuarial + actual vs assumed

valuation of DB plan

underfunded plan is considered debt

overfunded plan is ignored in valuation

remove net interest expense if net pension balance is deducted from enterprise value

Basel III

minimum capital requirement - % of risk-weighted assets funded with equity capital

minimum liquidity - high-quality liquid assets - 30 day stress scenario

stable funding - tenor of deposits and type of depositor

Camels

Capital adequacy, Asset quality, Management capabilities, Earnings sufficiency, Liquidity position, and Sensitivity to market risk.

1-5 rating - 1 best

composite rating - weighted

Capital adequacy

absorb potential losses

risk weighted assets - cash 0%; corporate loans 100%

capital tiers - tier 1 common stock retained earnings, oci tier 2 subordinate

Asset quality

existing and potential credit risk of assets

Management capabilities

governance structure, internal controls, ability to identify and control risk

Earnings

adequate return on capital to capital providers

Liquidity Position

to pay liabilities

liquidity coverage ratio - min % of expected cash outflows that must be held in highly liquid assets

net stable funding ratio - min % of required stable funding sourced from available stable funding - liquidity

Concentration of funding - proportion obtained from a single source

Contractual maturity - maturity of assets compared to funding source

Snensitivity to market risk

interest rate, ex rate, equity prices, commodity prices

Other banking-specific considerations

Govt support

Govt ownership

Mission of banking entity

Corproate culture

Other considerations - bank

Competitive environment

Off-bs items

Segment information

currency exposure

risk factors

Basel III

combined ratio

insurance expenses / net premiums earned - low=hard insurance market > attracts new entrants

underwriting loss ratio + expense ratio

underwriting loss ratio: claims paid / net premiums written

expense ratio: underwriting + sales comm / net premiums earned

loss reserves

historical with estimate of future losses

if optimistic > priced too low

the longer the obligation runs > more difficult to estimate

profitability measure of health insurance

total benefits paid per net premium

commission & exp per net premium

net interest margin

diff between int income on loans - int paid on deposits

loans - LT

deposits - ST

reporting quality vs earnings quality

reporting - information in financial reports - decision useful; faithful rep

earnings - financial condition; sustainable activities

Beneish Model

probability of earnings manipulation

M-Score = DSR + GMI + AQI + SGI + DEPI - SGAI + Accruals - LEVI

DSR (days sales receivable index) = (Receivablest/Salest)/(Receivablest−1/Salest−1).

GMI (gross margin index) = Gross margint−1/Gross margint.

AQI (asset quality index) = [1 − (PPEt + CAt)/TAt]/[1 − (PPEt−1 + CAt−1)/TAt−1],

SGI (sales growth index) = Salest/Salest−1.

DEPI (depreciation index) = Depreciation ratet−1/Depreciation ratet, where Depreciation rate = Depreciation/(Depreciation + PPE).

SGAI (sales, general, and administrative expenses index) = (SGAt /Salest)/(SGAt−1/Salest−1)

Accruals = (Income before extraordinary items9 − Cash from operations)/Total assets.

LEVI (leverage index) = Leveraget/Leveraget−1, where Leverage is calculated as the ratio of debt to assets.

higher M score (less neg number) > increased prob

Earnings persistence

Earningst+1 = α + β1Earningst + ε

A higher coefficient (β1) represents more persistent earnings.

larger component of accruals would be less persistent and thus of lower quality.

Altman model

probability of bankruptcy

Z-score =

1.2 (Net working capital/Total assets) + : ST liq risk

1.4 (Retained earnings/Total assets) + : accum profitability & age

3.3 (EBIT/Total assets) + : profitability

0.6 (Market value of equity/Book value of liabilities) + : leverage ratio

1.0 (Sales/Total assets) : ability to generate sales

higher Z score better

bankruptcy <1.81 < unclear < 3 < low prob

shortcoming of Altman model

single period

past performance- going concern assumption

cash flow quality

positive OCF

OCF derived from sustainable sources

OCF adequate to cover capital expenditures, dividends, and debt repayments

OCF with relatively low volatility (relative to industry participants)

cash flow classification

FRS permits companies to classify interest paid either as operating or as financing.

IFRS also permits companies to classify interest and dividends received as operating or as investing.

US GAAP requires that interest paid, interest received, and dividends received all be classified as operating cash flow

balance sheet quality

completeness

unbiased measurement

clear presentation

balance-sheet-based and cash-flow-based accruals ratios

Balance sheet accruals ratio for time t = (NOAt − NOAt −1)/[(NOAt + NOAt−1)/2], and

Cash flow accruals ratio for time t = [NIt − (CFOt + CFIt)]/[(NOAt + NOAt−1)/2],

abs value - lower better

net asset balance sheet exposure

assets translated at the current exchange rate are greater than liabilities translated at the current exchange rate

Factors Considered in Determining the Functional Currency

sales price of goods and services

competitive forces and regulations

labor, material, cogs

financing

receipts

extension of parent or autonomy

large or small portion of parent

remitted to parent

need funds from parent

hyper inflation

cumulative 3-year inflation rate > 100%

IFRS - restated for local inflation > translate both BS and PL to parent presentation currency at current rate (monetary assets not restated, only non-monetary assets from date of revaluation; equity from beg of year or historical)

GAAP - remeasure as if functional currency is the reporting currency - temporal

current vs temporal method

current - foreign currency is the functional currency - translation adj in equity

temporal - parent presentation currency is functional currency - translation diff as gain/loss