Chapter 14: Firms in Competitive Markets

1/22

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

23 Terms

Rank the market types from most competitive (& least concentrated) to least competitive (& most concentrated)

Perfect competition

Monopolistic competition

Oligopoly

Monopoly

Characteristics of perfect competition (PC) (4)

Lots of sellers

identical products

price takers

free entry and exit

Common examples of perfectly competitive markets

Agricultural markets

Commercial bakeries

Industrial markets

Screw, nut, and bolt manufacturers

Marginal revenue (MR)

MR = change in Total Revenue/change in Quantity

In perfect competition, MR =

Equilibrium price

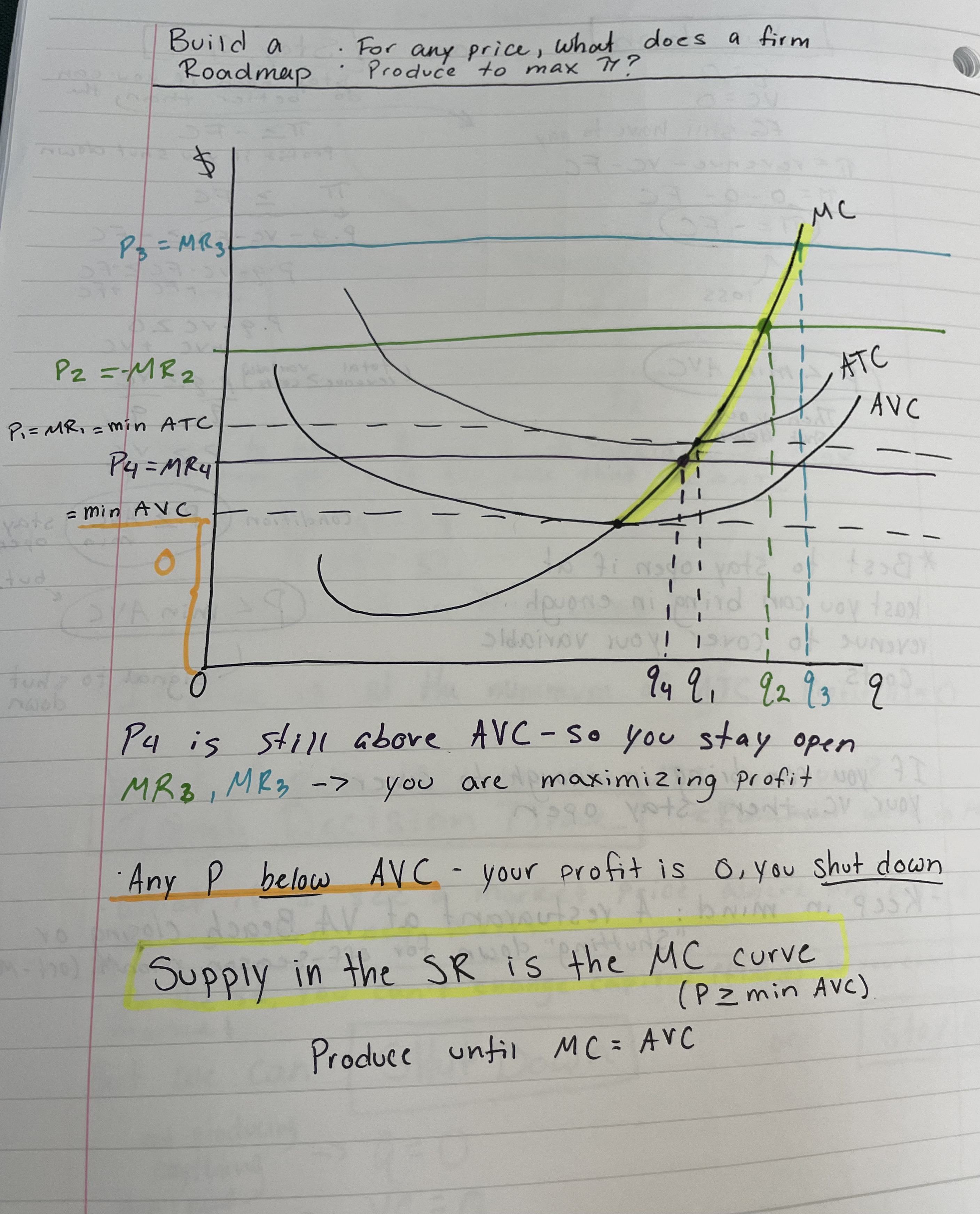

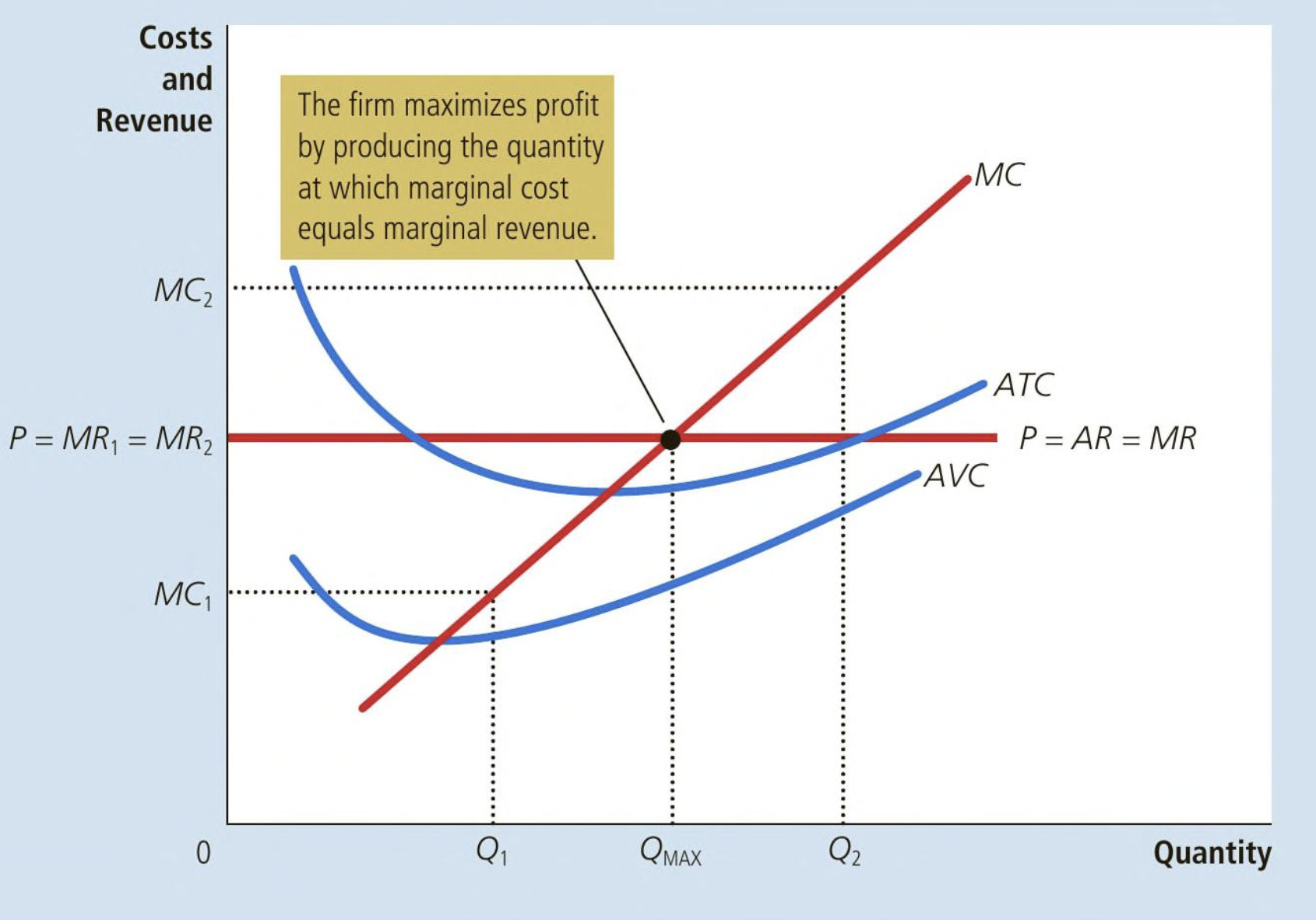

Profit-max rule & 3 rules for profit maximization

Keep producing until MR = MC

If MR > MC, firm should increase output

If MR < MC, firm should decrease output

At profit maximizing level, MR = MC

How to calculate/shade profit

profit = TR - TC

or profit = (P-ATC)q

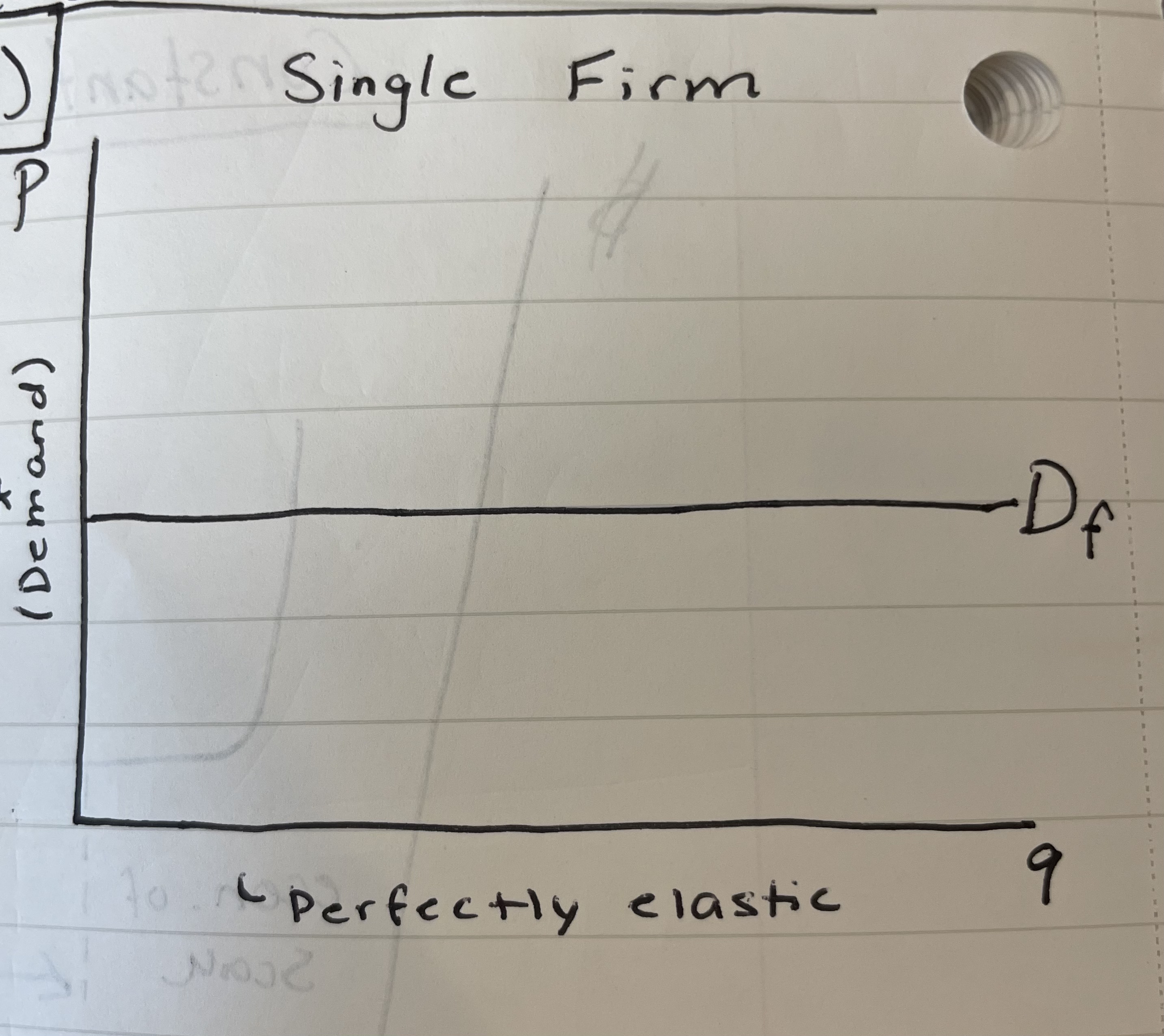

What does the demand for a single firm look like in perfect competition?

Perfectly elastic demand curve

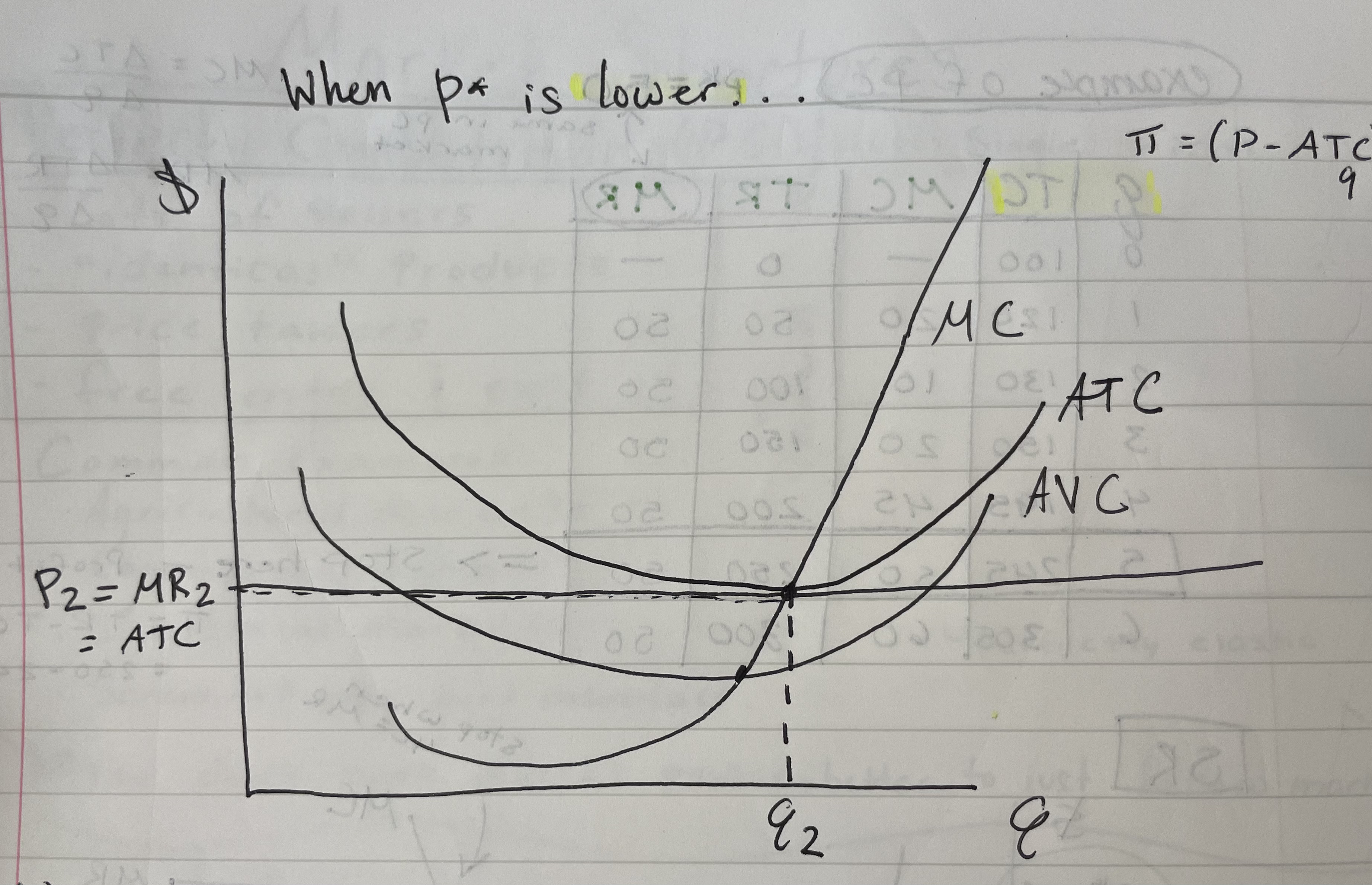

What happens when MR (marginal revenue)/price is equal to the ATC minimum?

Profit equals 0

When would you enact Tough Decision Time?

When price is below the ATC minimum

When should a firm shut down? How is this calculated?

q = 0

VC = 0

FC - still have to pay

profit = revenue - VC - FC

profit = 0 - 0 - FC

profit = -FC

Profit < minimum AVC, then you shut down

When should a firm stay open? How is this calculated?

If you can bring in enough profit to cover your VC, then stay open (profit ≥ -FC)

profit ≥ FC

p x q - VC - FC ≥ -FC

p x q - VC ≥ 0

p x q ≥ VC

p ≥ VC/q

(total revenue ≥ variable costs)

Stay open if p ≥ AVC min

For any price, what does a firm produce to maximize profit? (graph)

if firms are ____ and _____, the price of a good equals the ______ of making that good.

if firms are competitive and profit-maximizing, the price of a good equals the marginal cost of making that good.

if firms can freely enter and exit the market, the price also equals the _______________.

if firms can freely enter and exit the market, the price also equals the lowest possible average total cost (ATC) of production.

For all firms, ___ revenue equals the _____ of the good

For all firms, average revenue equals the price of the good

For competitive firms, ____ revenue equals the ____ of the good

For competitive firms, marginal revenue equals the price of the good

Profit maximizing for a competitive firm graph

In the long run, when should a firm exit the market?

P < ATC

A firm chooses to exit if the price of its good is less than the total average cost of production

If in the SR, profit is negative

Market supply shifts left, pushing prices up until profit = 0 again

In the long run, when should a firm enter the market?

P > ATC

In the SR, profit is positive

Market supply shifts right, pushing prices down until profit = 0 again

When does the process of entry and exit end in a market?

The process of entry and exit ends only when price and ATC are driven to equality.

In the long-run equilibrium of a competitive market with free entry and exit, firms must be operating at their _____.

In the long-run equilibrium of a competitive market with free entry and exit, firms must be operating at their efficient scale.

Because firms can enter and exit more easily in the long run than in the short run, the long-run supply curve is typically more elastic than the short-run supply curve.

True