Economics - Microeconomics

1/16

Earn XP

Description and Tags

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai | Chat |

|---|

No analytics yet

Send a link to your students to track their progress

17 Terms

What is Economics?

study of how humans use limited resources to satisfy unlimited wants

study of the production, consumption, and distribution of goods and services

Economics: Key Concepts

Scarcity

Choice

Efficiency

Equity

Economic Well-Being

Sustainability

Change

Interdependence

Factors of Production (FoPs)

Land: anything taken from the planet, grown or mined

Labor: workers

Capital: physical or financial resources used to produce value in an economy, any man-made tool, tangible and intangible

Entrepreneurship: people who invest time and effort and take on financial risks in the hope of profit

Ex: Disneyland Parks

Land: oil, cleared land, metal, food resources

Labor: cast, technicians, board members, ride conductors, security

Capital: electricity, employee training programmes

Entrepreneurship: expanding parks, production managers, advertisers, designers

Demand: Definition

the quantity of a product a consumer is willing and able to purchase at various prices

Law of Demand

when the price of a product increases, the quantity demanded decreases and vice versa, ceteris paribus

The Income Effect

change in consumer purchasing power from a change in price

when price increases, purchasing power decreases

The Substitution Effect

consumers will substitute goods/services that become relatively more expensive

The Law of Diminishing Marginal Utility

utility gained from the next unit is lower the utility gained from the previous unit

Ceteris paribus

all other factors held constant

Determinants of Demand

number of buyers

taste and preference

income (normal goods and inferior goods)

price of related goods (substitute goods or complementary goods)

Normal Goods

as income increases, the demand for a product increases

Inferior Goods

as income increases, the demand for a product decreases

Substitute Goods

two alternative goods that could be used for the same purpose

Ex: Coca-Cola vs Pepsi

Complementary Goods

goods that are purchased separately but are used together

Economic Assumptions

Ceteris Paribus: “all things being equal” to isolate the impact of one variable

Rational Consumers: assume that consumers make decisions based on logic and reason, aiming to maximize utility given available information

Utility Maximization: assumed to make choices that will give them the highest level of satisfaction or happiness

Perfect Knowledge: assume all consumers and producers have perfect knowledge

Dependence on Primary Sector: Impact

dependence on primary sector:

diversification of goods is limited, less focus on secondary and tertiary sector, which helps economic development more

labor force not proportional to GDP contribution

primary sector = low elasticity of demand

risk of droughts, agricultural input and output may be unequal → seasonal unemployment

Price Elasticity of Demand (PED): Equation

(% change in Quantity Demanded) / (% change in Price)

%∆Qd / %∆P

Price Elasticity of Supply (PES): Equation

(% change in Quantity Supplied) / (% change in Price)

%∆QS / %∆P

PED & PES: Indicators

PED or PES > 1 [Elastic]

PED or PES = 1 [Unit Elastic]

PED or PES < 1 [Inelastic]

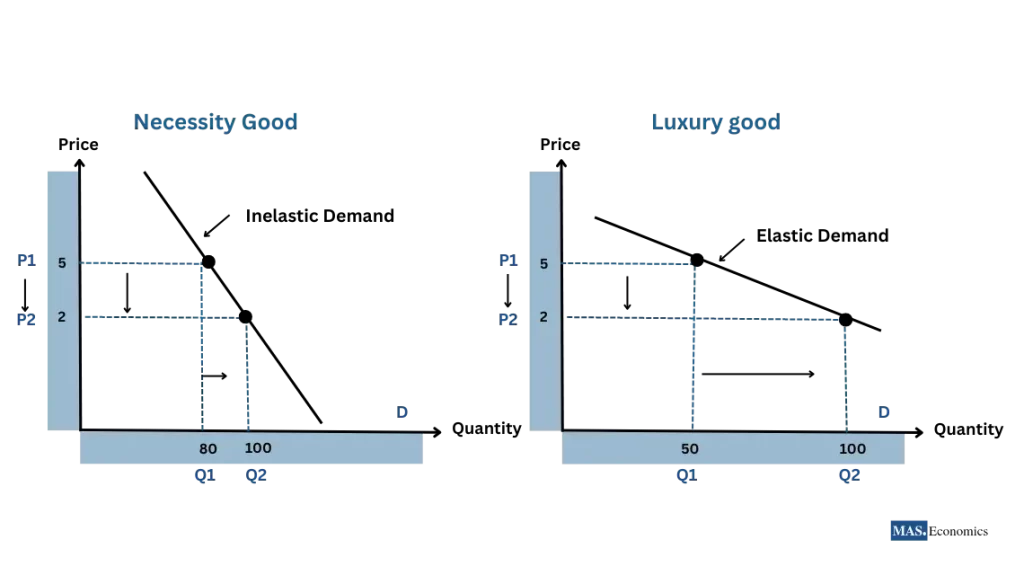

Price Inelastic vs Elastic Graph

Inelastic: necessities; medicine and prescriptions; addictive substances

Elastic: luxury goods; consumer discretionary (non-essential but desirable if affordable)