Looks like no one added any tags here yet for you.

Classes 1-4 (66 terms)

Classes 1-4 (66 terms)

Assemble Some Evidence (B&P)

Step #2 in the Eightfold Path:

You need evidence to assess the nature and extent of the problem, to assess particular features of concrete policy situation, policies that have been thought to have worked in situations similar to your own. Issues with this step are that assembling evidence is hard and costly

Comparative Advantage

the ability to produce a good at a lower opportunity cost. Implies that individuals, firms, and nations will specialize in producing goods for which they have the lowest opportunity costs when compared to other entities. i.e. the individual who can produce said product the cheapest/most efficient is the one who dominates said market.

Competition

a rivalry among buyers or sellers of outputs or among buyers or sellers of inputs. i.e. the struggle among producers for the dollars of consumers, and vice versa, the struggle among consumers for the best product(s) from said producers for the best/cheapest price.

Cost (MBN1)

the highest-valued (best) forgone alternative; the most valuable option that is sacrificed when a choice is made

Define the Problem (B&P)

Step #1 in the Eightfold Path: Most crucial step. This step frames your purpose. What do you want to investigate? What is going on, and what conditions cause the problems you want to alleviate?

Economic of Obesity (MBN7)

MBN ch. 7 on obesity. In the first sixty years of 20th century, incomes rose and cost of food declined, and people gained weight → initially this was a benefit as people were previously malnourished, but it has turned into a cost as more Americans and obese and obesity is associated with mortality Many more Americans are obese today. This is due to rising incomes meaning people could buy more food, too much junk food, little knowledge about nutrition, too much TV time complemented by more sedentary lifestyles, the automobile made it easier to go out to eat, women started working so there was no dedicated person to cook dinner. Economist believe Cheap food + Law of Demand = Weight gain, so price bad foods high to disincentivize consumption. Also, menu mandates were established to help counter this, but were virtually ineffective.

FDA (MBN1) (history, roles, lessons)

History--> created in 1906 through the Food and Drug Safety Act. Drug regulation became stricter after birth defects were caused by sleeping pills for pregnant women. The approval process changed in 1962. In 1992, the prescription drug user fee sped up the approval process as facilities and staff could be expanded with new fees paid from pharmaceutical companies.

Role--> approving drugs and products for public consumption

Lessons--> every policy has a cost, the cost of an action is the alternative that is sacrificed, brings up questions of how much safety we want

Full Cost (MBN7)

the total cost incurred in production and is comprised of business cost, opportunity cost, and normal profit

Full Price (MBN7)

Includes market price and the time that goes into producing and consuming the goods.

The combined measure of all of the things that must be given up to undertake an activity; i.e., the time it takes to produce, consume, includes both the money price, and the value of the time that must be sacrificed (i.e., other goods that must be sacrificed)

Generic Opportunities for Social Improvement (B&P, Box I‐1)

Creative policy improvement options-- Design the architecture of your choice (if you vary the ways in which choices are presented to people then that can create bias). People want to follow social norms. Internalizing the social effects of individual decisions. Adjust prices to reflect total costs. Two activities can be joined so like employing people to do public works. Input substitutions. System can be designed to have multiple functions

Independent Contractor case

i.e., Uber/Lyft;

- How: Prop 22 ensures that gig workers are classified as these

- Result: drivers pay their own expenses, such as gas, car maintenance, and insurance, and are not provided benefits like minimum wage, health insurance, or paid sick leave

THIS = the way that these companies exploits hundreds of thousands of workers

Inflation

Def: a general increase in prices and fall in the purchasing value of money.

In the context of the economy: the primary policy for reducing inflation is monetary policy -(i.e., gov't intervention), by price controlling, meaning raising interest rates and or decreasing bond prices to reduce demand/amount of money in the economy to help bring inflation under control. The gov't can also use/control wages and prices to fight inflation (i.e., new taxes/fewer taxes, setting a minimum wage, etc.), but it often does not work out according to most conservative economists. Meaning that gov't interventions such as these can lead to and cause Market Failures, such as recession and job losses. In the last decade or so, inflation has increased 7.5%, the highest its been since the '70s. (<-- as of Mar. 2022)

Inflation Corrected (MBN7)

Adjusted for the inflation that has taken place since a nominal price was originally measured. Takes into account the inflation rate over time

Labor Force Participation Rate (MBN7)

Definition: The sum of all people who are working or are available for and looking for work, divided by the population; both numerator and denominator are generally restricted to persons aged sixteen and above

Sub Idea: Labor force participation rate of women in recent years leads to less time to cook, turning to reduced time cost of unhealthy alternatives

Law of Demand

law stating the quantity demanded and price are inversely related-- meaning, more is bought at a lower price, while less is bought at a higher price (only when all things are considered equal). i.e., when the market is functioning at it's peak efficiency (EQ), consumers will buy more of a good when its priced lower, and less when it is priced higher.

Market Share (MBN18)

Definition: The proportion of total sales in an industry/market accounted for by a specific firm or group of firms in that industry

Connecting Idea: Winning in competition means increased market share and therefore increased profits. Can also allow for monopolies/oligopolies to form

Medallions (Taxi) (MBN18)

Definition: a city-issued metal shield affixed to the cab's hood.

Taxicabs are limited by law in NY - 1 car for every six hundred people → need medallion to operate taxi → market price = $600k/medallion→ Rate of return has always been highly favorable, comparable to stocks but now value has reduced with the emergence of companies like uber, lyft, etc.

Menu Mandates (MBN7)

in response to the rising obesity rates/health concerns among US citizens, through the ACA in 2010, the gov't passed/established a law requiring menus in restaurants, movie theaters, etc to have a calorie/nutritional facts label attached in order to inform individuals of what exactly they are eating. Connecting Idea: a form of a gov't intervention meant to address the adverse selection btwn sellers and buyers, which lead to a market failure, i.e., information asymmetry. The gov't hoped that if folks knew exactly what they were consuming, that they would be more motivated to take better care of themselves, making this a great way to address these growing health concerns. This is a perfect example of the gov't addressing a market failure, i.e., information asymmetry, in which one firm (i.e., the supplier) is withholding/has access to info that another party (i.e., the consumer) does not, and this can affect the market in negative ways leading to a market failure.

Rate of Return (MBN18)

(RoR) is the net gain or loss of an investment over a specified time period, expressed as a percentage of the investment's initial cost (i.e., the conversion btwn the present value of something from its original value, converted into a percentage). When calculating the rate of the return, you are determining the percentage change from the beginning of the period until the end. The formula is simple: the current or present value minus the original value divided by the initial value, times 100 (this expresses the rate of return as a percentage.

(e.g. if the investment of $1 yields a gross return of $1.20, the net benefit is $0.20 and the rate of return in $0.20 / $1.00 = 5 or 20 percent)

Profits (MBN 18)

income generated by selling something for a higher price than was paid for it; in production the income generated is the difference btwn total revenues received from consumers who purchase the goods minus the total cost of producing those goods. i.e., difference btwn a business's revenue and its expenses.

Connecting Idea: Profits are sure to rise if competition can be kept out → e.g., taxicab market informs what's at stake, meaning that Uber, Lyft, etc. cut into the profits of taxicabs, while also cutting into their market share, thus increasing their market power while diminishing that of taxicabs.

Scarcity (MBN1)

the demand for a good or service is greater than the availability of said good or service. i.e., the limited resources we have such as oil, gold, land, labor, money, capital, etc.

Supply (MBN18)

the total amount or quantity of a good or service that is available to consumers at a set price retailers want to sell it at. Time is closely associated with supply, e.g. when the price of an orange is 65 cents, the quantity supplied is 300 oranges a week.

Time Cost (MBN7)

The economic value of the time a person must sacrifice to engage in an activity

Connecting Idea: Time cost of food has been reduced from hours to minutes thanks to the industrial revolution and the increase in food production (i.e., more bad foods being consumed), which has lead to our obesity epidemic

Type I Error (MBN1)

occurs when a decisionmaker accepts as true a hypothesis that is in fact false.

e.g. when the FDA approves a "bad" drug

Type II Error (MBN1)

occurs when a decisionmaker rejects a hypothesis that is in fact true.

e.g. when the FDA fails to approve a drug that should have been approved.

Political Economy

the study of the relationship that forms btwn a nation's population and its government when public policy is enacted. i.e., the intersection of political, economic, and legal systems of a country, in which we study the causes and consequences of political decision being made

Potential Pareto Improvement

i.e., a "no-brainer" in which there are no losers. e.g. anytime the gov't steps in and implements a market regulatory which leads to market failures such as regulatory capture,

Price Discrimination

pricing strategy used by sellers to charge consumers different prices for the same good or service. Sellers may charge consumers the max price they'll pay or place consumers into different groups and charge based on said group. e.g. airline tickets, person who booked 3 months in advance is more likely to get a better deal than the individual who booked 3-days prior.

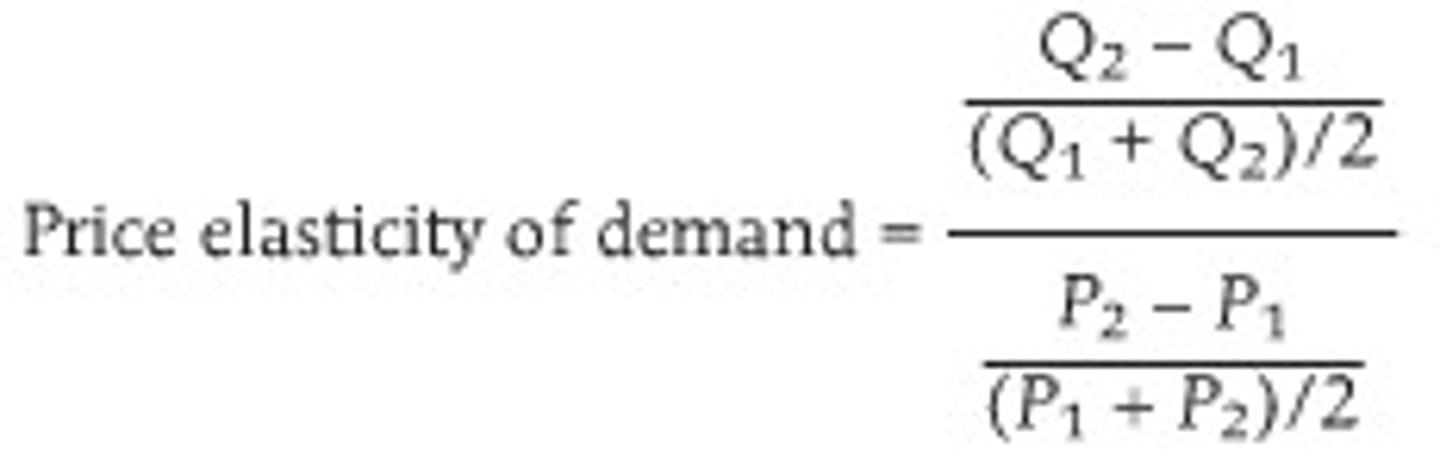

Price Elasticity of Demand (MBN17)

a measure of how much the quantity demanded of a good responds to a change in the price of that good, computed as the percentage change in quantity demanded divided by the percentage change in price. i.e., how responsive the quantity demanded or supplied is to changes in price; if the quantity of a product demanded or purchased changes more than the price itself changes, the product is considered to be elastic. e.g., when price is elastic, then demand will drop when price increases, vice versa.

Preference Ordering

think about a set of goods that you could consume. You could consume any combination of any number of goods. Call each such combination a "bundle". A preference ordering is a way to say "I like bundle A more than bundle B." A preference ordering must satisfy three properties:

1. Completeness: Assumption that individuals must have a preference relationship between any two sets of goods; either one is better than the other or both the sam (indifference). E.g. any two bundles A and B can be ordered. This means that no matter which two bundles A and B you are given, you can always say if you prefer one over the other or have exactly no preference. You can never say "I don't know."

2. Transitivity: the property where is one bundle, A, is preferred to another, B, and B is preferred to bundle C, then A is preferred over. E.g. if you prefer A over B and B over C, then you must prefer A over C, otherwise, the preference ordering is not transitive

3. Reflexivity: Can be applied when both sides of the relationship are the same; weak preferences are generally reflexive E.g. you must prefer A at least as much as A and A at most as much as A. It's almost like saying A <= A and A >= A, so A = A. If you think this sounds obvious and dumb, the meaning is very simple, but people use this property to formalize preference ordering so they can prove mathematical things about it.

Present Discounted Value

(PDV); the value today of future payments, adjusted for interest accrual determined by the date of valuation. i.e., current worth of a future sum of money or stream of cash flow given a specified rate of return-- meaning taking into account interest or other factors affecting future value.

Price Searcher

a seller that can sell some of its output at various prices; power to set their prices bc they are selling differentiated products; they are typically facing a downward-sloping demand curve. Single-pricing means the price for all units must be lowered just to sell one more unit, thus marginal revenue value will be lowered than the price e.g. Monopolies

Price-Taking Behavior

i.e., price-taker - any economic agent that takes the market price as given; often used as a synonym for a firm operating in a market characterized by pure competition (i.e., has a broad range of competitors who are selling the same products)

Private Benefit

the benefit derived by an individual or firm directly involved in a transaction as either buyer or seller. For consumers it can be expressed as utility, while to a firm it is expressed as profit. It is the opposite of external benefit or positive externalities.

Private Cost

the cost incurred by buyer or seller to purchase/produce said product/service. E.g. we pay for the cost to produce gas (i.e., an internal cost or tax) but we do not pay for the costs of burning that fuel, such as air pollution.

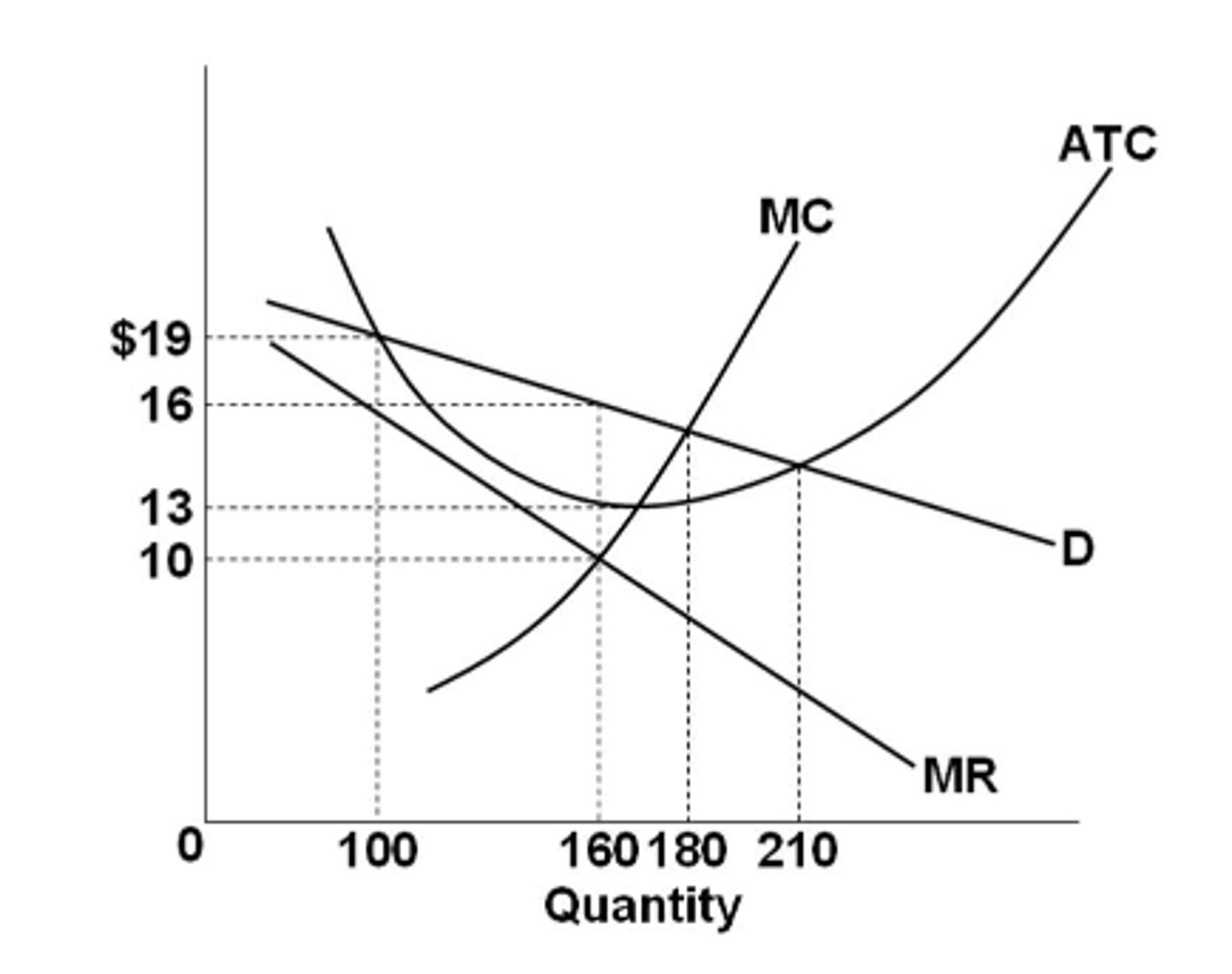

Profit-Maximizing Firm

Firms will maximize profit within the constraint of consumer demand and the technology of production. The firm maximizes profit when the amount of output equals the marginal revenue (i.e. MC=MR and fall within the line

Profits (MBN17)

The difference between total revenue and cost of production

i.e., difference btwn expenses and revenue

Proven vs. Probable Reserves

Proven reserves are the amount of oil or natural resources contained under a piece of land with a 90% or greater probability of profitable extraction.

Probable reserves are those with the likelihood of recovery for between possible and proved reserves, or over 50-percent but under 90-percent.

Public Goods

a product or service that any individual may consume without paying for/reducing its availability or quantity for another individual; i.e. a situation in which no one is excluded, often considered "nonrivalrous" and "nonexcludable" e.g. fireworks, national defense

Connecting Idea: individuals take advantage of public goods and oftentimes do not pay for it --> free rides and said goods being under produced and consumed

--> a market failure bc the true demand by consumers is not being expressed in the market

Quality-Adjusted Prices (MBN15)

trying to measure the price change for a product which has exhibited some changes in its characteristics from an earlier period or that has replaced another product, and estimating the different levels of utility it may provide to the consumer.

Quotas

Placing restrictions on the level of output of a firm in order to keep prices high since demand is low

Connecting Idea: a form of protectionism (i.e., effort to protect a subset of American producers at the expense of consumers and other producers through trade barriers)

Rate of Return

the gain or loss on an investment over a specified time period, expressed as a percentage of the investment's cost. Useful for present discounted value formula

Rational

decision-making process based on making choices that result in the optimal level of benefit or utility for an individual. Most conventional economic theories are based on the assumption that all individuals taking part in an action or activity are behaving this way

Rational Ignorance

ignorance about an issue is said to be "rational" when the cost of educating oneself about the issue sufficiently to make an informed decision can outweigh any potential benefit one could reasonably expect to gain from that decision, and so it would be irrational to waste time doing so. i.e., when the cost of acquiring information is greater than the benefits to be derived from the information, it is rational to be ignorant.

Connecting Idea: in deciding which brand of prepared food is most nutritious, a shopper might simply choose the one with (for example) the lowest amount of sugar, rather than conducting a research study of all the positive and negative factors in nutrition -->high obesity rates

Risk Neutrality

neither risk averse or risk seeking; an individual's decisions are not affected by the degree of uncertainty in a set of outcomes so they are indifferent about the choices with equal expected payoffs i.e., the outcome will be the same no matter the risk

Risk Non-preferring

i.e., Risk Aversion; individuals who attempt to lower their uncertainty in decision making i.e., chose the less risker option. e.g. taking a guaranteed $40 instead of gambling to get $80.

Risk Preferring

i.e., Risk Inclination; an individual who is willing to take more risks while investing in order to earn higher returns. e.g. taking the gamble to gain $80 instead of choosing the guaranteed $40.

Rivalrous Consumption

consuming a good/service prevents it from being used by other possible users. There are 2 types: Durable and Nondurable. Rivalrous = Nondurable

1. Nondurable: consumption destroys the good, allowing only one user to enjoy it entirely; e.g. coffee in a cup.

Nonrivalrous Consumption

consuming a good/service prevents it from being used by other possible users. There are 2 types: Durable and Nondurable.

Nonrivalrous = Durable

1. Durable: users may use them one at a time does not diminish the availability of that good or service for others to use; e.g. restrooms, national parks, roads, etc.

Scarce

i.e. scarcity; the limited resources we have e.g. oil, gas, land, money, labor, capital, etc.

"Sex, Booze, Drugs" reading (MBN6)

Limiting the consumption of drugs can lead to more deaths and bad consequences. Government usually targets sellers rather than buyers in crimes like selling drugs. People who have a comparative advantage in conducting illegal activities have more incentive to supply valuable drugs since they can smuggle less quantity. The current structure of the law incentivizes more potent drugs since it requires less quantity. If drugs became totally legal we could make the quality and price more well known. In places where prostitution is legal, they are tested for STIs and it is safer. More people die when drugs are illegal.

Short vs. Long Run

- Short Run: a period in which at least 1 of the firm's resources is fixed-- meaning, costs have fixed factors and variables that impact production e.g. rent, labour, etc.

- Long Run: where all factors of production are variable, and additional factors outside the control of the firm can change, e.g. technology, government policy. A period of several years.

Social Benefits

private benefits gained by individuals directly involved in a transaction together with the external benefits gained by a third parties not directly involved in the transaction e.g. social security

Social Cost

the full cost the society bears when a resource-using action occurs (e.g. the cost of driving a car is equal to all private costs plus any additional cost that other members of society bear, like air pollution and traffic congestion)

Tolls (MBN24)

People have to pay money to drive on a road. It can create traffic and you have to build the infrastructure and hire collectors, meaning it may not be the best solution to congestion.

Two-Sided Market

i.e. demand and supply; two-sided market gives space/has both sellers and buyers available to interact with each other to provides goods/services for money. e.g. our market place here

Utility

the usefulness or enjoyment a consumer can get from a service or good. Economic utility can decline as the supply of a service or good increases. Marginal utility is the utility gained by consuming an additional unit of a service or good.

Utility Function

a mathematical function that ranks alternatives according to their utility to an individual, i.e., measures the preferences consumers apply to their consumption of goods and services. Any function U(x) > U(y) means that you prefer bundle x over bundle y, while U(x) = U(y), means you have no preference between x and y. There are many possible utility functions that can represent the same preference ordering; normally, saying that your utility is more important than my utility for some bundle does NOT actually mean you like that bundle more than me; utilities cannot be compared across people, only compared among different bundles for one person

Variable Costs

costs that vary with the level of output; change in proportion to the good or service that a business produces; also the sum of marginal costs over all units produced e.g. raw materials, packing, wages

Widget

abstract unit of production (e.g. factories produce _____ using capital and labor)

Classes 5-10 (66 terms)

Classes 5-10 (66 terms)

Adverse Selection

occurs before the transaction, when either the buyer or seller has more information about the product or service than the other. In other words, the buyer or seller knows that the products value is lower than its worth. For example, a car salesman knows that he has a faulty car, which is worth $1,000 but sells it for $2,000.

Behavioral Economics

the study of situations in which people make choices that do not appear to be economically rational. apples psychological insights into human behavior to explain economic decision making. Taking inputs from psychology, behavioral economics incorporates the idea that we all have behavioral biases when making decisions and that some of those behaviors can be changed. Bringing this more realistic knowledge into the design of public policies can make them more effective.

Cartel

an association of manufacturers or suppliers, often on an international scale, with the purpose of maintaining prices at a high level and restricting competition, regulate supply in an effort to regulate or manipulate prices

Comparative Advantage Competition

i.e., Law of Competition; an economy's ability to produce a particular good or service at a lower opportunity cost than its trading partners. i.e., what you do best while also giving up the least. e.g. if you're a good babysitter and a great plumber, your comparative advantage is plumbing. That's because you'll make more money as a plumber. real world e.g. chinese labor vs. american labor, chinese labor produces products cheaper

Construct The Alternatives (B&P)

Apart of the 8th Fold Path, Step #3: By alternatives I mean something like "policy options," or "alternative courses of action," or "alternative strategies of intervention to solve or mitigate the problem." (p. 16)

Consumer Preferences

Subjective individual taste. Allows a consumer to rank different bundles of goods/services according to levels of utility, or the total satisfaction they give the consumer. Preferences are independent of income or prices i.e., defined as a set of assumptions that focus on consumer choices that result in different alternatives such as happiness, satisfaction, or utility.

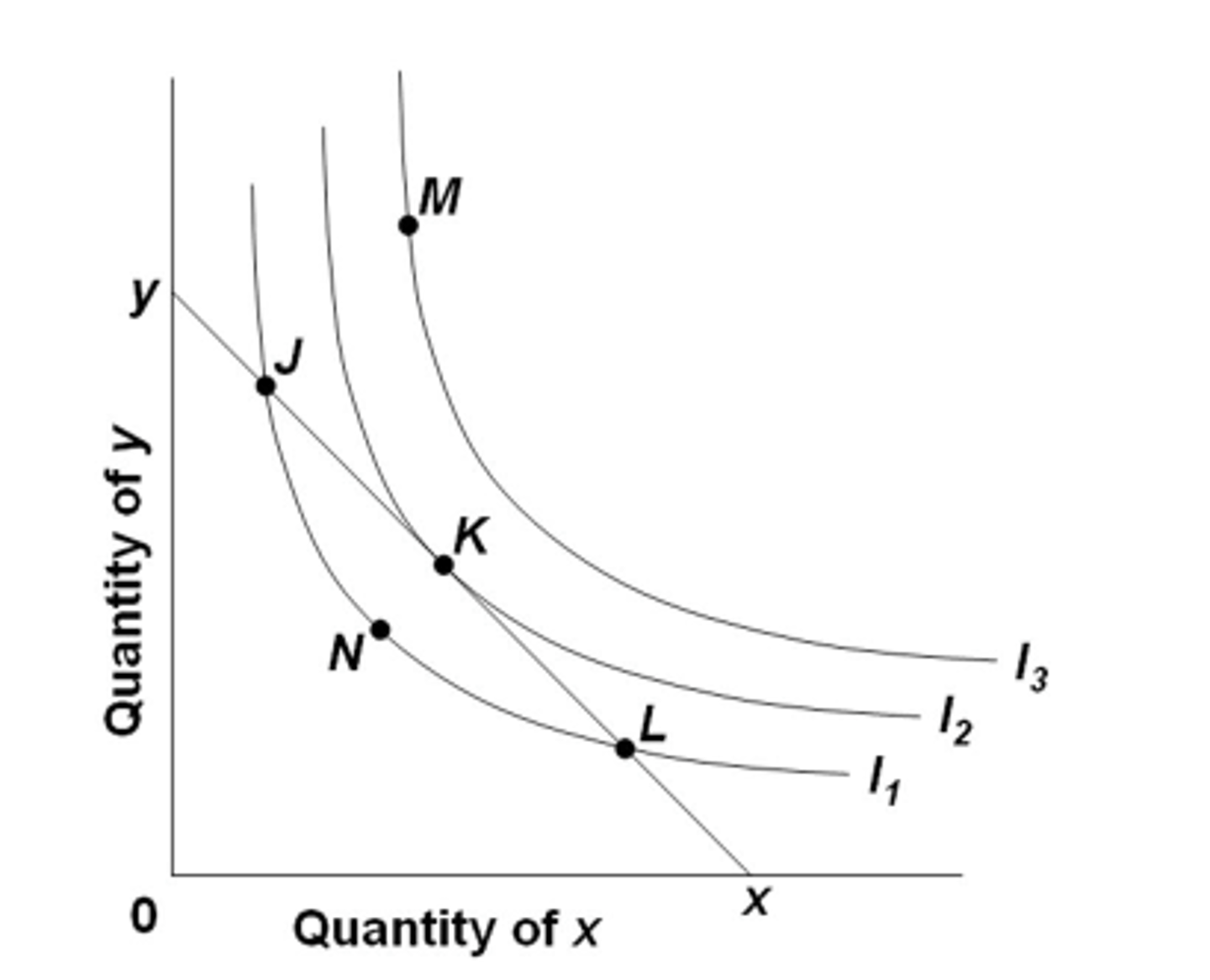

Consumer's Optimum Cost

using the information given by the indifference map and the information about the income constraint given by the budget line in order to show what combination of x and y maximizes the consumer's utility, subject to the constraint imposed by her income.

Total Cost

the total expense incurred in reaching a particular level of output

Marginal Cost

the increase in total cost that arises from an extra unit of production

Demand Curve

a negatively sloped line showing the inverse relationship between the price and the quantity demanded i.e., Downward slope.

Dominant-Firm Oligopoly (MBN15)

one large firm has a major share of total sales, and a group of smaller firms supplies the remainder of the market. The large firm has power to set a price that maximizes its own profits.

Economic Growth

the increase in the value (or inflation rate) of an economy's goods and services, which creates more profit for businesses over time e.g. Adding capital to the economy tends to increase productivity of labor. Newer, better, and more tools mean that workers can produce more output per time period.

Economies of Scale

Refers to the reduced costs per unit that arise from increased total output of a product i.e., factors that cause a producer's average cost per unit to fall as output rises, business runs more efficiently. e.g. it is easier to serve 1,00 guest at 2 restaurants than 1, so a company may open an additional one to increase output (i.e. helping more customers) and lower average costs (i.e. buying in bulk more bc more people are coming in).

Efficiency

the extent to which they are keeping costs down, especially monetary costs, as indicated by either total costs or a ratio that involves both benefits and costs.

Elastic

greater than 1; situation where producers need to find optimum level of production because changes in price affects the change in demand, vice versa. e.g. if the price of bell peppers were to increase by 10%, the demand would decrease by 20%, thus, the quantity demanded is very responsive to price changes and demand is described as elastic.

Inelastic

less than 1; consumers respond very little to changes in price; selling commodities at max price with the highest amount of consumers so efficiency rate is maximized i.e., describes demand that is not very sensitive to price changes e.g. luxury goods

Unitary Elastic

equal to 1; when a change in price of that good causes an equal change in quantity demanded i.e., demand whose elasticity is exactly equal to 1

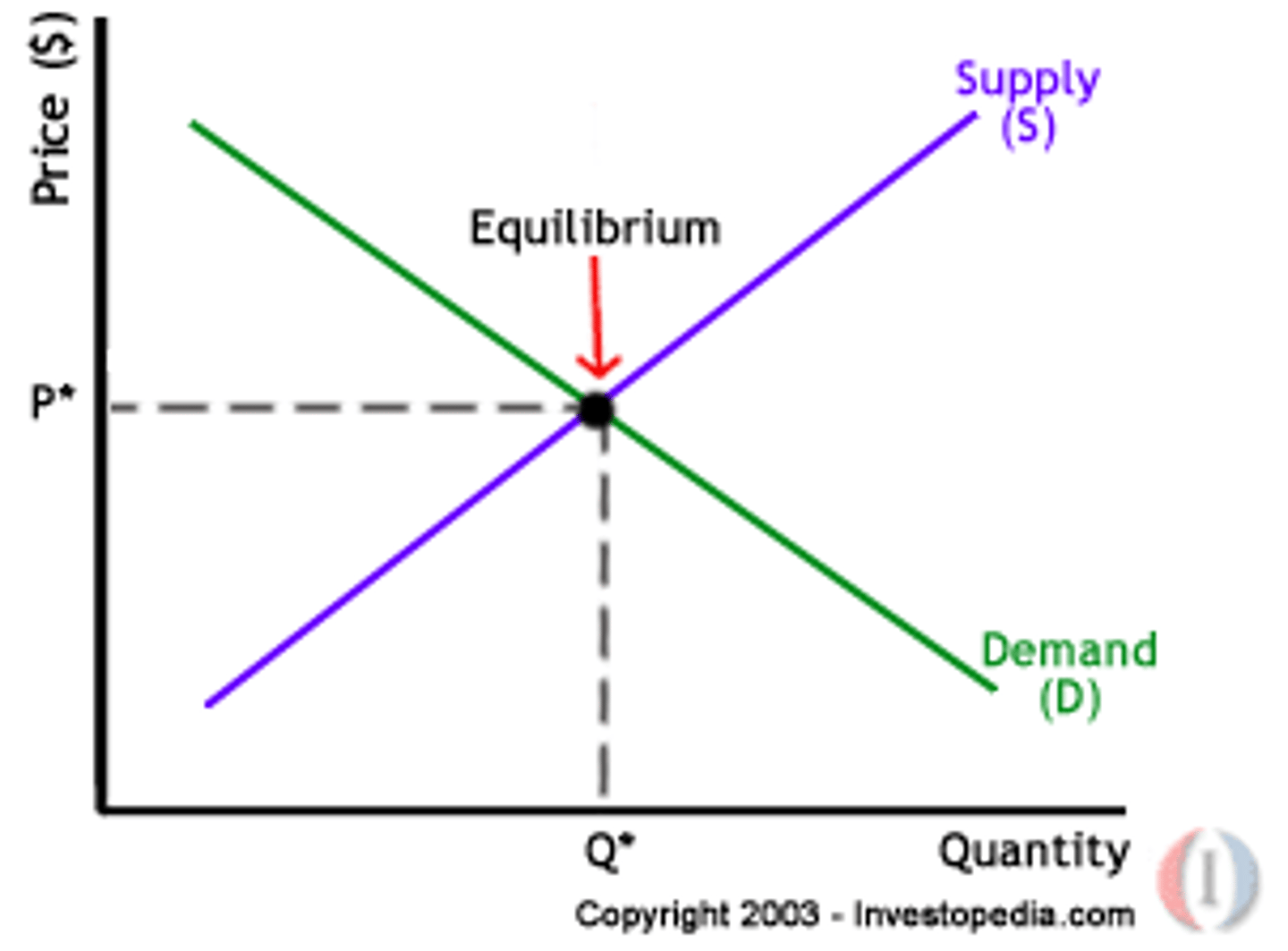

Equilibrium

where supply and demand intersect and the market is said to be working "efficiently" (in the absence of external influences); i.e., when quantity supplied equals quantity demanded meaning both are balanced.

Excess Demand

market demand is greater than its market supply causing its market price to rise; occurs when the Price of a good is lower than the Equilibrium Price, meaning more consumers will want to buy the good than suppliers are willing to sell, which can lead to a shortage.

Excess Supply

Quantity supplied is greater than the quantity demanded; some producers won't be able to sell all their goods this will induce them to lower their price to make the product/service more appealing, i.e., when quantity supplied is more than quantity demanded

Excludability

the possibility to prevent people (consumers) who have not paid for it from having access to it e.g. private goods

Nonexcludability

non-paying consumers cannot be prevented from accessing it. e.g. some public goods, public roads, etc.

External Benefit

(positive externality); occurs when producing or consuming a good causes a benefit to a third party; social benefit will be greater than private benefit (e.g. education)

External Cost

(negative externality); a cost that a transaction or activity imposes on a party that is not part of the transaction or activity, e.g. when people buy fuel for a car, they pay for the production of that fuel (an internal cost), but not for the costs of burning that fuel, such as air pollution.

Externalties

benefits or costs of an economic activity that affects a third party other than the buyer or seller, can be pos. or neg.

Fixed Costs

Costs that do not vary with the quantity of output produced, i.e., costs that do not change for a firm (e.g., no matter how many shirts a shirt firm produces, its electricity bill and rent will be the same)

Free Riding

e.g. of a market failure; situation where individuals consume more than their fair share or pay less than their fair share of the cost of a shared resource. It is a market failure when people take advantage of a collective good without paying for it. e.g. public parks, fireworks

General Equilibrium

analyzes the economy as a whole, rather than analyzing single markets like with partial equilibrium analysis. Shows how supply and demand interact and tend toward a balance in an economy of multiple markets working at once. This analysis further helps in predicting the consequences of an autonomous economic event. Suppose the demand for commodity A rises which may lead to a rise in its price. This, in turn, reduces the prices of its substitutes and raises the prices of complements.

Government Failure

an inefficient allocation of resources caused by government intervention in the economy

Incentives

a positive or negative environmental stimulus that motivates behavior, i.e., perceived consequences of actions or decisions; that may be positive or negative, monetary or nonmonetary

Indifference Maps/Curves

Curves: It refers to a set of indifference curves corresponding to different income levels of the consumer. In an indifference map, indifference curves are parallel and a higher indifference curve represents a higher level of satisfaction, i.e. using my indifference curve, how much of cats and dogs can i get within my budget

Industry Concentration

The extent to which a small number of corporations control most of the sales in an industry/market

Information Asymmetry

situation in which one party (either the producer or consumer) is more informed than another because of the possession of private information

Innovation (MBN2)

the changing of that process to serve different needs or achieve different outcomes. i.e., upon an existing idea

Intermediary Firms

companies that provide services that enable buyers and sellers to engage in trade (e.g. Amazon)

Internalities

Nonmarket environments create private goals and internal regulations as substitutes for the price system which motivate action and performance. Types of behaviors that impose costs on a person in the long-run that are not taken into account when making decisions in the present e.g.smoking, you may not consider the latter health effects (economics discourages gov from creating legislation that targets this bc it is assumed that the consumer takes these personal costs into account when paying for the good that causes the internality)

Invention (MBN2)

creating a completely new idea/concept.

Kaldor-Hicks Efficiency

efficiency which results in that there is more total benefit than total cost. Notice how this is different from a Pareto improvement. For a Pareto improvement, NOBODY must be hurt, and at least one person has to benefit. For this efficiency, any number of people can get hurt, as long as the total benefit exceeds the total cost. For example, if I lose $5 and you gain $10, that is a Kaldor-Hicks efficient change, but not a Pareto improvement. Question: Is every Pareto optimal allocation also Kaldor-Hicks efficient? Answer: no. Question: Is every Kaldor-Hicks efficient allocation Pareto optimal? Yes. Also, any Kaldor-Hicks efficient action can be "converted" into a Pareto optimal action by having the Kaldor-Hicks "winners" compensate the losers