T7 International Financial Reporting Standards for Compensation Professionals

1/98

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced |

|---|

No study sessions yet.

99 Terms

IASC

International Accounting Standards Committee

SAC

Standards Advisory Council

IASB

International Accounting Standards Board

IFRIC

International Financial Reporting Interpretations Committee

IFRS

International Financial Reporting Standards

1973

IASC founded by 10 national accountancy organizations

1981

All members of the Int'l Federation of Accountants (IFAC) became members of IASC

1999

100+ countries. Structure reviewed

2001

IASB began operations

2005

Europe, Australia, 90+ countries adopting the IFRS

2007

More than 110 jurisdictions have adopted the IAS in some form

2012

Canada adopted IFRS

2014/5

USA adopted IFRS

2019

IFRS Standards are required in more than 140 jurisdictions and are permitted in many more.

IASB Mission Statement

Develop International Financial Reporting

Standards (IFRS) that bring transparency, accountability,

and efficiency to financial markets around the world.

Our work serves the public interest by fostering trust, growth

and long-term stability in the global economy.

IASB Objectives (3)

1) To develop, in the public interest, a single set of high quality, understandable and enforceable global accounting standards

2) To promote the use and rigorous application of those standards

3) To work actively to bring about convergence of national accounting standards and IFRS

Benefits of IFRS (4)

1) Bring transparency by enhancing the international comparability and quality of financial information, enabling investors and other market participants to make informed economic decisions.

2) IFRS Standards strengthen accountability by reducing the information gap between the providers of capital and the people to whom they have entrusted their money.

3) Provide information needed to hold management to

account. As a source of globally comparable information, IFRS

Standards are also of vital importance to regulators around the world.

4) Contribute to economic efficiency by helping investors to

identify opportunities and risks around the world, thus improving capital allocation. Use of a single, trusted accounting language lowers the cost of capital and reduces international reporting costs for businesses.

Benefits of One Set of Standards (6)

1) Inter-firm comparability equals lower cost to investors

2) Lower listing costs with multiple listings

3) Greater competition amongst exchanges

4) More efficient resource allocation

5) Lower cost of capital

6) Higher global economic growth rate

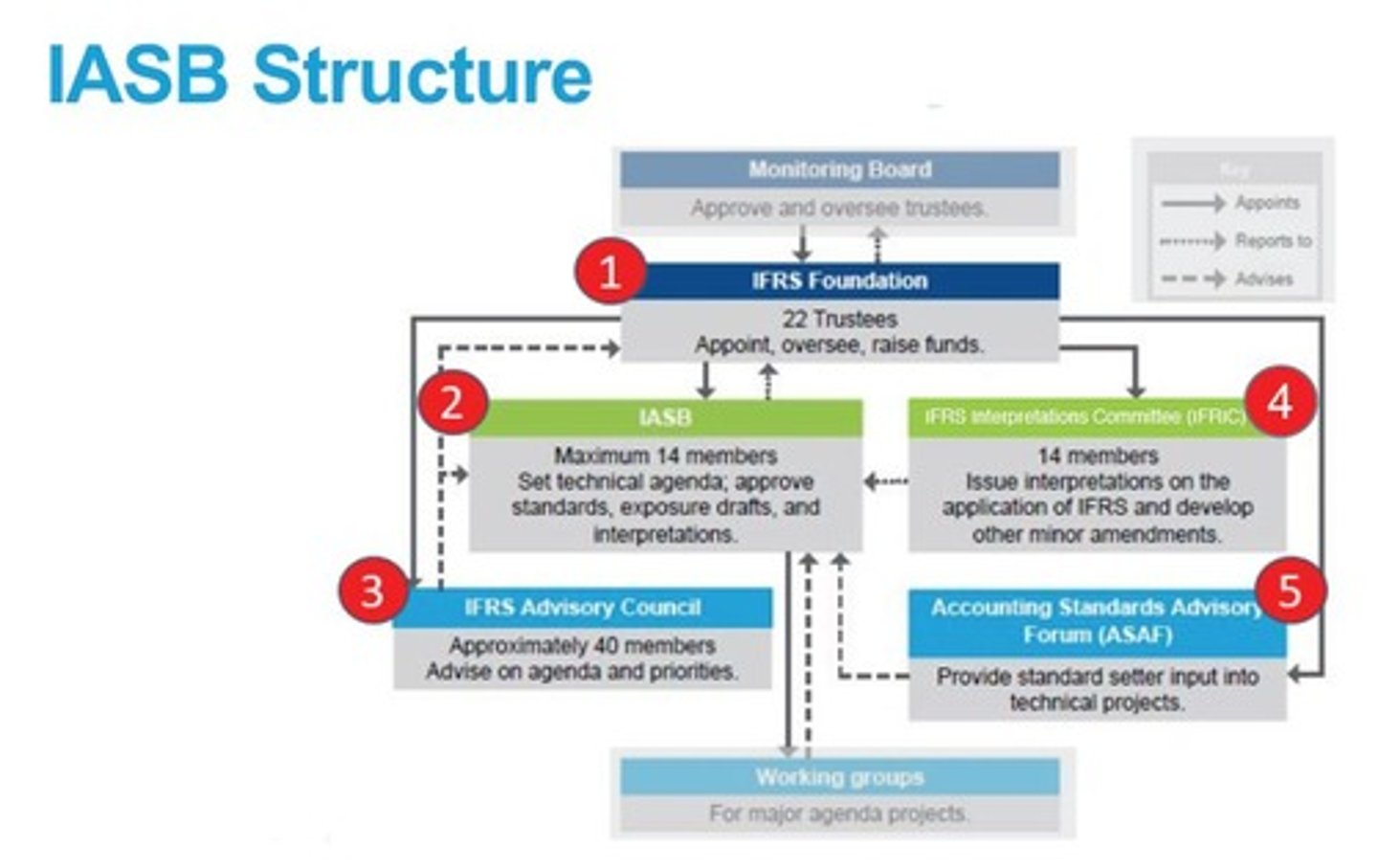

IASB Structure - Picture

IFRS Foundation (3)

1) 22 Trustees - 1 from South America, 6 from North America, 6 from Europe, 6 from Asia / Oceania, 2 from any area, 1 from Africa

2) Appoint IASB members, Advisory Council and IFRIC

3) Monitor IASB's effectiveness, secure funding, approve

budget, responsible for constitution

IASB (6)

1) Headquartered in London, the IASB has the sole

responsibility for setting all IFRS standards

2) Prepares and issues all IFRS standards

3) Approves principles-based IFRS standards, does not

issue detailed application guidelines

4) Initially was concerned only with the private sector. It

now addresses both the not for profit and the public

sector as well

5) 16 people - 4 from Asia and Oceania, 4 from Europe, 4 from North America, 1 from Africa, 1 from other areas

6) These 16 people carry out a number of duties, including

auditor, preparer, user/analyst, academic, as well as

other functions.

IFRS Advisory Council (5)

1) 40 members from throughout the world

2) Meets three times each year

3) Provides a forum for participation by organizations and

individuals

4) Informs IASB about the views of participants on major

standard-setting projects

5) Provides advice to IASB on priorities

International Financial Reporting Interpretations Committee (IFRIC) (2)

1) 14 voting members plus non-voting observers

2) Provide guidance on reporting issues not specifically

addressed in IASB's standards, or where unsatisfactory

or conflicting interpretations have developed

Accounting Standards Advisory Forum (ASAF) (4)

1) Formalize and streamline IASB's collective engagement with

the global community of National Accounting Standard-setters

and regional bodies

2) Ensures that a broad range of national and regional input on

major technical issues related to IASB's standard-setting

activities are discussed and considered

3) Comprised of representatives at a high level of professional

capability and with a deep knowledge of their jurisdictions and

regions.

4) Meets in London 4 times a year for two days

IASC Foundation (3)

- 19 Trustees (6 from N.A.)

- Appoint IASB members, SAC and IFRIC

- Monitor IASB's effectiveness, raise funds, approve budget, responsible for constitution

Standards Advisory Council (4)

- About 50 members from throughout the world

- Meets three times each year

- Provides advice to IASB on priorities

- Informs IASB of implications of proposed standards

International Accounting Standards Board (3)

- Has sole responsibility for setting standards

- Approves principles-based standards, does not issue detailed application guidelines

- Initially was concerned only with the private sector. It now addresses both the not for profit and the public sector as well

Module 1 Objectives

■Discuss the objectives of the International Accounting Standards Board (IASB).

■Explain the benefits of moving towards one set of international standards.

■Discuss the roles and responsibilities of the IASB and its advisory groups.

Definition of Accounting

A service activity. Its function is to provide quantitative information, primarily financial in nature, about economic entities that is intended to be useful in making economic decisions - in making reasoned choices among alternative courses of action.

Objective of Financial Reporting

To provide information useful for decision making.

Two Major Classifications of Stakeholders

Internal & External Users

Internal users of accounting information

Make decisions direction affecting the internal operations of the enterprise

external users of accounting information

Make decisions concerning their relationship to the enterprise.

Conceptual Framework

establishes the concepts that underlie financial reporting

The Need for a Conceptual Framework (3)

- Rule-making should build on and relate to an established body of concepts.

- Enables IASB to issue more useful and consistent pronouncements over time particularly as Board members change

- Provides benchmark for judgments

Agreed concepts that underlie financial reporting

Objective, qualitative characteristics, element definitions and other factors

Conceptual Framework sets standards (3)

- Enhances consistency across standards

- Enhances consistency over time as Board members change

- Provides benchmark for judgments

Development of a Conceptual Framework

IASB and FASB initially worked on a joint project, designed to build on the existing IASB and FASB frameworks. More recently the IASB has produced a new conceptual framework by itself.

Conceptual Framework Basic Objective - Level 1

To provide financial information about the reporting entity that is useful to present and potential equity investors, lenders, and other creditors in making decisions in their capacity as capital providers.

Fundamental Qualitative Characteristics

Relevance and Faithful representation

Fundamental Characteristics of Relevance

- Predictive value

- Confirmatory value

- Prediction & Confirmatory

Fundamental Characteristics of Faithful Representation

- Complete

- Neutral

- Free from Error

Elements of Financial Statements

Assets, Liabilities, Equity, Income, Expenses

Asset

A resource controlled by the entity as a result of past events and from which future economic benefits are expected to flow to the entity.

Liability

A present obligation of the entity arising from past events, the settlement of which is expected to result in an outflow from the entity of resources embodying economic benefits.

Equity

The residual interest in the assets of the entity after deducting all its liabilities.

Income

Increases in economic benefits during the accounting period in the form of inflows or enhancements of assets or decreases fo liabilities that result in increases in equity, other than those relating to contributions from equity participants.

Expenses

Decreases in economic benefits during the accounting period in the form of outflows or depletions of assets or incurrences of liabilities that result in decrease in equity, other than those relating to distributions to equity participants.

Economic Entity Assumption

An assumption that every economic entity can be separately identified and accounted for.

Going Concern Assumption

The assumption that the company will continue in operation for the foreseeable future.

Monetary Unit Assumption

An assumption that requires that only those things that can be expressed in money are included in the accounting records.

Periodicity Assumption

An assumption that the economic life of a business can be divided into artificial time periods.

accrual basis accounting assumption

a key assumption in financial reporting: transactions that change a company's financial statements are recorded in the periods in which the events occur

Measurement Principle

the most commonly used measurements are based on historical cost and fair value

Revenue Recognition Principle

The principle that companies recognize revenue in the accounting period in which the performance obligation is satisfied.

Expense Recognition Principle

Expenses are decreases in economic benefits during the accounting period in the form of outflows or depletions of assets or incurrences of liabilities that result in decreases in equity, other than to equity participants.

Full Disclosure Principle

Requires that companies provide information that is of sufficient importance to influence the judgment and decisions of an informed user.

Cost Constraint

Constraint that weighs the cost that companies will incur to provide the information against the benefit that financial statement users will gain from having the information available.

Materiality Constraint

Prescribes that information whose omission or misstatement could influence the economic decisions of users taken on the basis of the financial statements but be included.

Accrual Accounting

the recognition of revenue when earned and the matching of expenses when incurred

Guiding Principles of Accrual Accounting

- Revenue recognition

- Matching

Four Main Financial Statements

Statement of Financial Position

Statement of Income and Statement of Comprehensive Income

Statement of Changes in Shareholders' Equity

Statement of Cash Flows

Historical Cost

Objective, Verifiable, Not Subject to Bias, BUT not particularly relevant.

Revaluation Model

An alternative to the cost model and allows for long lived assets to be reported at fair value as long as there is an active market for the asset.

Assets (reporting order)

In order of liquidity

Liabilities (reporting order)

In order of maturity

Current Liabilities

Obligations that a company expects to pay within the next year or operating cycle, whichever is longer.

Noncurrent Liabilities

obligations that a company does not expect to pay within one year

Net Working Capital

current assets less current liabilities

Operating expenses

Usual and customary costs that a company incurs to support its main business activities.

non-operating expenses

relate to the company's financing and investing activities

Main equity categories

Retained earnings

Treasury stock

Statement of Cash Flows

the financial statement that identifies a firm's sources and uses of cash in a given accounting period

Statement of Shareholders' Equity

statement disclosing the source of changes in the shareholders' equity accounts.

Statement of Financial Position

another name for the balance sheet

Statement of Retained Earnings

Reports the way that net income and the distribution of dividends affected the financial position of the company during the accounting period.

Number of IAS standards

41

Number of IFRS standards

13

Objective of IAS 19

Prescribe the accounting and disclosure for employee benefits

Employee benefit liability

when employee has provided service in exchange for employee benefits to be paid in the future

employee benefit expense

when the entity consumes the economic benefit arising from service provided by an employee in exchange for employee benefits

IAS 19 2011 Amendments

- Operative Jan 1 2014

- require surplus or deficit of a pension fund to be detailed

- too many options leading to different accounting results

- corridor approach is no longer allowed

IFRS 2

reporting standard for share-based payments

IAS 26

Accounting and Reporting by Retirement Benefit Plans

Main categories of employee benefits

short-term benefits

post-employment benefits

long-term benefits

termination benefits

Short-term employee benefits

expected to be settled wholly before twelve months after the end of the annual reporting period in which the employees render the related service.

Post-employment benefits

benefits, other than termination benefits and short-term employee benefits) that are payable after the completion of employment

Long-term benefits

all employee benefits other than short-term employee benefits, post-employment benefits, and termination benefits.

Termination benefits

Benefits provided to employees as a result of the voluntary or involuntary termination of employment.

TVM

time value of money

Short-term benefits debit

Expenses for employee benefits (profit or loss) or cost of another asset (statement of financial position)

Short-term benefits credit

Liability or accrued expenses or cash paid

Constructive Obligation

When a change in the undertaking's informal practices would cause unacceptable damage to its relationship with staff.

Accounting Steps for DB plans

1. Determine deficit or surplus

2. Determine amount in the statement of financial position

3. Determine amount in the statement of comprehensive income

4. Determine re-measurements in other comprehensive income

Projected unit credit method

Required method for estimating the ultimate cost of a benefit

NPV

net present value

asset ceiling

present value of any economic benefits available in the form of refunds from the plan or reductions in the future contributions to the plan

current service cost

the increase in the present value of the defined benefit obligation resulting from employee service in the current period

past service cost

the change in the present value of the defined benefit obligation for employee service in prior periods, resulting from a plan amendment or a curtailment.