C1: INTRODUCTION TO MICROECONOMICS

1/12

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced |

|---|

No study sessions yet.

13 Terms

DEFINITION OF ECONOMICS

Economics is a science which studies human behaviors as a relationship between ends and scarce means, which have alternative uses.

OR

Economics is a study of how people use their limited resources to try to fulfil unlimited wants and involves alternatives or choices.

RESOURCES/ FACTORS OF PRODUCTION

Land

Labour

Capital

Enterprise

ECONOMICS

Limited > Production > Purchased by consumer > satisfy needs and wants (unlimited)

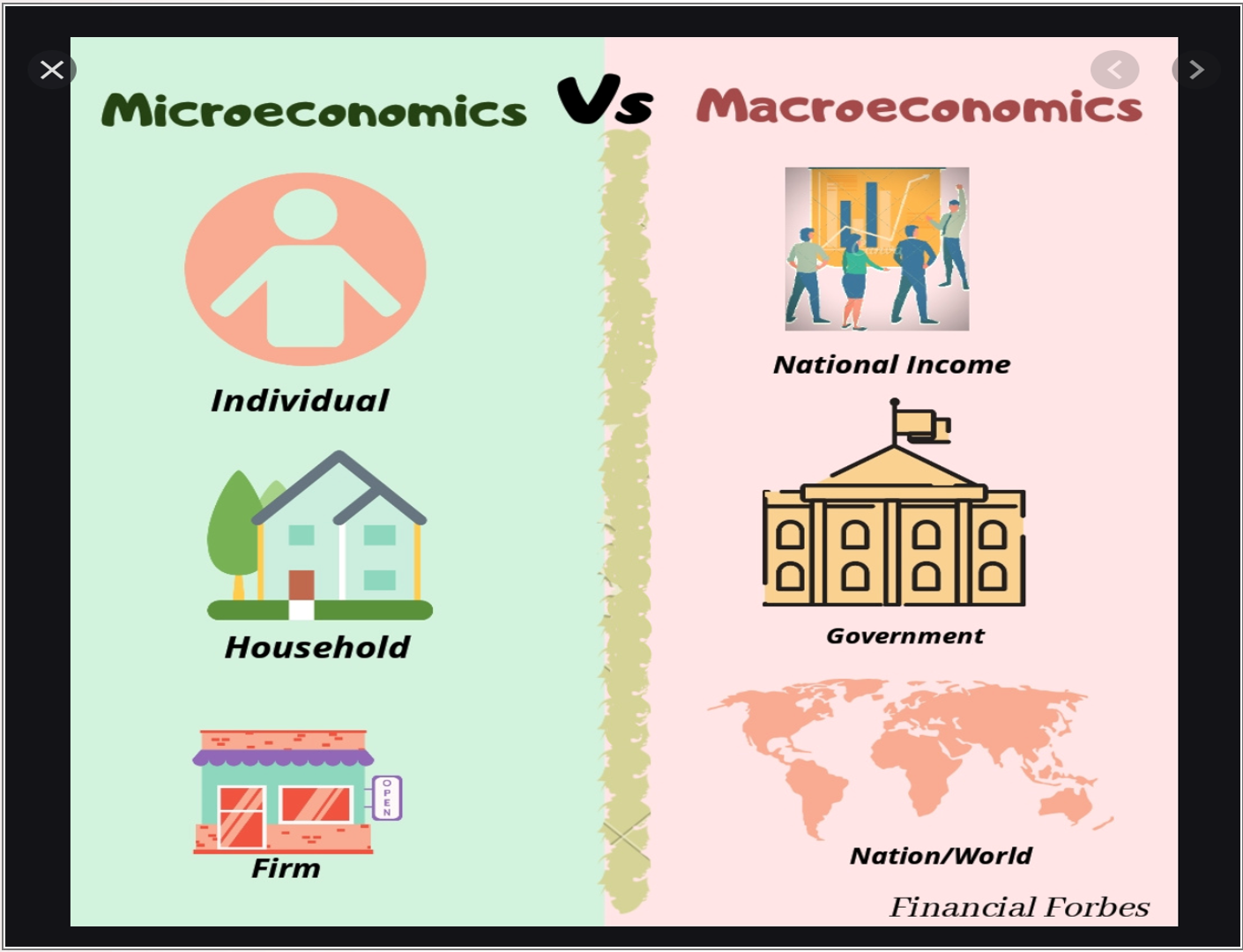

MICROECONOMICS VS MACROECONOMICS

MICROECONOMICS

The study of individual parts of the economy such as public choices, business choices and personal choices

MACROECONOMICS

The study of the economic system as a whole such as national income, trade cycle, unemployment rate, inflation and general price level.

POSITIVE VS. NORMATIVE ANALYSIS

A positive analysis is to deal with the question of “what is” and no indication of approval or disapproval. It focuses on facts and cause-and-effect relationships.

A normative analysis is to deal with the question of “what ought to be”. It incorporates value judgements about what the economy should be or what policy should be used to achieve economic goals.

BASIC ECONOMIC CONCEPTS

1. SCARCITY

One of the important concepts in economics is scarcity

Scarcity is defined as wants always exceed limited resources to satisfy them.

Limited resources vs unlimited funds

Scarcity is a universal problem faced by poor as well as rich nations in order to fulfil their needs.

CHOICE

When Scarcity exists, choices are to be made

OPPURTUNITY COSTS

Opportunity cost is defined as the second best alternative that has to be forgone for another choice which gives more satisfaction.

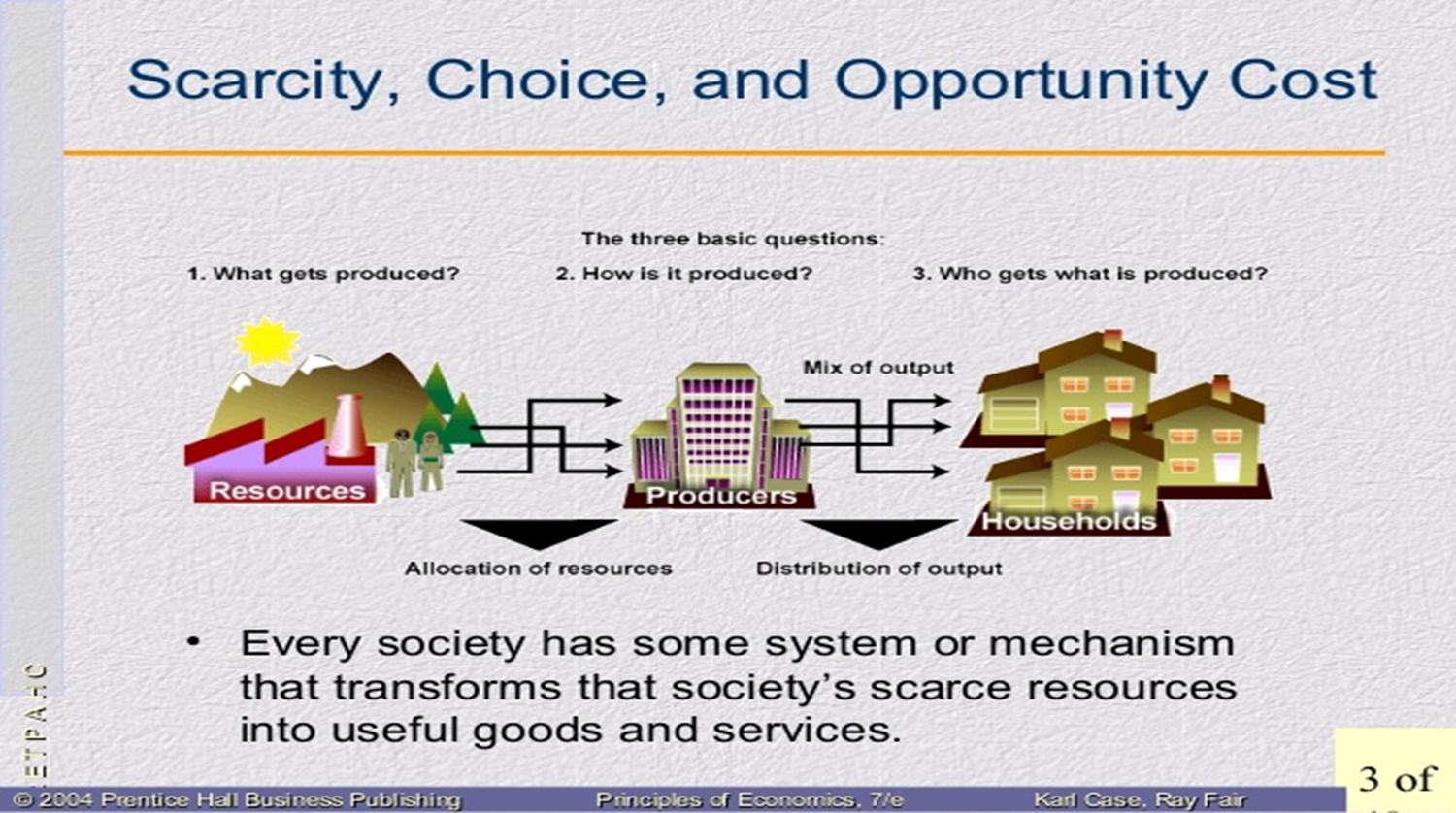

BASIC ECONOMIC PROBLEMS

WHAT TO PRODUCE?

Refers to the type of goods and services to be produced

HOW TO PRODUCE?

Refers to the cheapest method of production

FOR WHOM TO PRODUCE

Refers to the distribution of income

PRODUCTION POSSIBILITIES CURVE (PPC) /REFER SLIDE/

Used to explain the basic economic concepts: Scarcity, Choices and Opportunity cost

DEFINITION

The PPC shows the various possible combinations of goods and services produced within a specified time period with all its resources fully and efficiently employed.

ASSUMPTIONS

The economy is operating in full employment and full production capacity (full efficiency).

The amount of resources available are fixed

The state of technology does not change throughout the production

FACTORS THAT SHIFT THE PPC (REFER SLIDE)

Economic Growth

Improvements in Technology

Population

TYPES OF ECONOMIC SYSTEM

Capitalism

Socialism

Mixed

CAPITALISM /

Free market economy

An economic system where individuals and sellers make economic decisions using a price system

CHARACTERISTICS

Private ownership of resources

Freedom of enterprise and choice

Consumers’ sovereignty

Competition

Government intervention

Price System

Strength

Production according to customer needs

Economic freedom

Efficient utilization of resources

Variety of consumer goods

Enhance trade, business and R&D

Automatic Incentives

Flexibilities

Weaknesses

Inequality of distribution of wealth and income

Inflation and high unemployment rate

Lack of social welfare

Wasteful competition

Misallocation of resources

Social cost

SOCIALISM/ Planned Economy

An economic system where all the economic decisions are made by the government or a central authority

Characteristics

Public ownership of resources

Central planning authority

Price mechanism of lesser importance

Central control and ownership

Strength

Production according to basic need

Equal distribution of income and wealth

Better allocation of resources

No serious unemployment or inflation

Rapid economic development

Social welfare

Weaknesses

Lack of incentives and initiative by individuals

Loss of economic freedom and consumer sovereignty

Absence of competition

Waste of economic resources

MIXED ECONOMY

An economic system which combines both capitalism and socialism

Characteristics

Public and private ownership of resources

Price mechanism and economic plans in making decisions

Government helps to control income disparity

Government intervention in the economy

Co-operation between the government, public and business sectors

Government control of monopolies