Purdue 1st Year Microeconomics Exam 1 Study Guide

1/69

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

70 Terms

Economics

A social science that studies the choices we make as we cope with scarcity and the incentives that influence and reconcile our choices

Ceteris paribus

all else equal

Microeconomics

Individual choices in the market

Macroeconimics

Large scale, bigger picture look at the economy

Normative analysis

Judgement/opinion

Positive analysis

Factual statement

Scarcity

available resources are insufficient to satisfy wants

Examples of things that are not scarce

Air, pollution, etc.

Types of Economics Resources (scarce)

-Land (natural resources)

- Labor (People)

- Capital (Manmade resources ex: Machinery, Buildings, etc)

- Entrepreneurship (Coming up with ways products are produced)

Incentives

Rewards or penalties that encourage or discourage an action

Opportunity cost

Value of the best alternative

Explicit costs

Monetary expenses

Implicit cost

value of forgone alternatives

Free goods

Free goods can still have economic cost

Sunk Cost

Irreversable cost

- Your decision doesn't allow you to take that cost away

Ex: Time lost, you cant undo time you've spent

Car value: As soon as your car has left the dealership the value has depreciated, and if you try to sell it back it's used

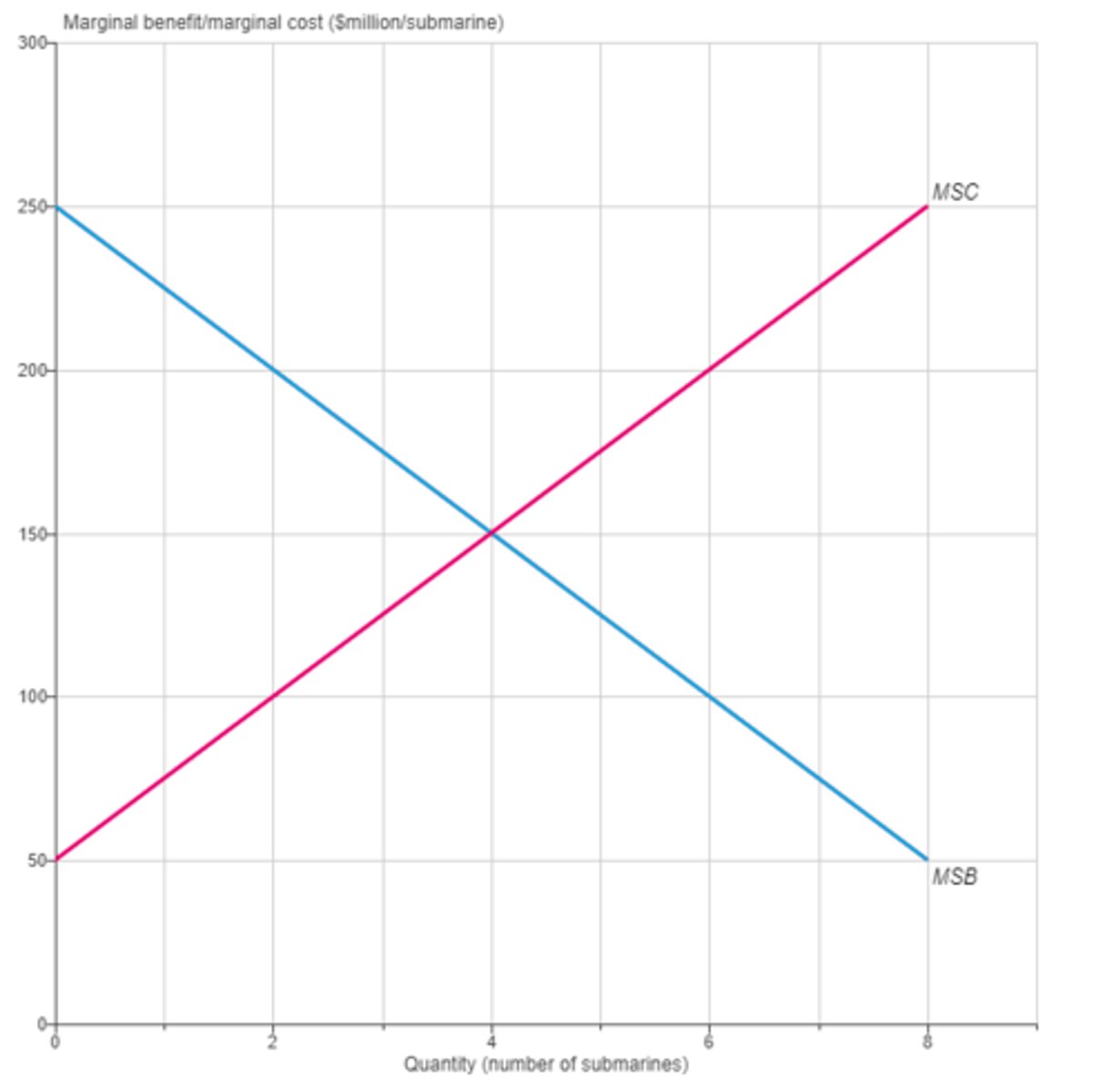

Marginal benefit

Benefit of one additional unit of a good or activity

General rule about marginal benefit and cost

- Marginal benefit goes down as quantity goes up

- Marginal cost goes up as quantity goes up

Graph of Marginal cost and Marginal benefit

Marginal cost has a positive slope

Marginal benefit has a negative slope

Absolute Advantage

Can make more than the other person in a certain amount of time

Comparative Advantage

Producing a good with a lower cost than the other person

Production Possibility Frontier (PPF)

Graph of the maximum output that can be produced by an individual or an economy

Comparing PPF slopes

Whoever has a flatter slope has the comparative advantage in the good on the X axis

Steps to Create an Economy wide PPF

1. Find the extremes on the X and Y (what they would do if they both spent their entire time on one task)

2. Work your way down the X axis, assigning the other task to the person who has the comparative advantage

3. Once you have reached the point of specialisation, the slope changes to what the person who doesn't have comparative advantage would contribute

Point of Specialization

The point at which both parties are only producing the task which they have comparative advantage at

Productive efficiency

Producing at the lowest coast

- Every point on the PPF satisfies production efficiency

Allocative efficiency

Using resources where they have the highest value

- Dependent on demand and supply

Ways that PPF shifts

- Natural resource discovery --> More of good X and Y

- Population growth --> More labor = more X and Y

- Labor Productivity --> More education, etc = More X+Y

- Technological change --> Not necessarily changing both. Could change X but not Y

- Capital accumulation --> More buildings, tools, etc = Shift out

- Natural disasters or other bad events --> Shift inward

Demand

The maximum quantity a consumer is willing and able to purchase at various prices

Law of demand

Price and quantity demanded are inversely related

- Higher prices reduce quantity demanded

- Lower prices increase quantity demanded

How to graph demand

- Price goes on the y-axis

- Quantity demanded goes on the x-axis

Changes (shifts) in Demand

1. Income - Ex: Normal goods, inferior goods both change in different ways

2. Prices of related goods Ex: Substitutes, complements

3. Changes in expectations - Change in price, Change in income

4. Tastes and Preferences - Whats trendy & Populars

5. Number of Buyers - More buyers = More demand

Normal goods

Goods where demand rises when income rises and falls when income falls

Inferior goods

Goods where demand rises when income falls and demand falls when income rises

ex: instant ramen noodles

Substitutes

Goods that are used in place of one another Ex: Oreos & thin mints

As oreos price goes up, you would buy more thin mints

Complements

Goods that are used together. Ex: Milk and Thin mints. As the price of milk goes up, the demand for both milk and thin mints go down because they are used together

Change in expectation of price

If price is expected to rise in the future, the current demand is up

If the price is expected to fall in the future, the current demand is lowered

Change in expectation of income

If income is expected to rise:

Demand for normal goods rises

Demand for inferior goods falls

Supply

The maximum quantity a seller is willing and able to sell at various prices

Law of supply

As price increases, quantity supplied increases

Factors that change supply

1. Input prices (natural resources, labor, etc.)

- Wages paid to labor = Less supply

2. Prices of related goods in production (substitutes and compliments in production)

3. Price - If prices are expected to rise, you sell less currently so that you can sell more when its higher. If you think the price is going to fall, you would sell more currently so that you can get the most out of it

4. Number of suppliers - More sellers = More supply because more people are selling the same thing

5. Technology: Changes in technology usually mean less cost to produce, increasing supply

Change in Supply/Demand VS Change in Quantity Supplied/demanded

Change in Demand/Supply - Shifts the entire line

Change in quantity demanded/supplied - shift along the line

When you are changing both Demand and Supply:

If either price or quantity shifts in opposite directions, it is indeterminate

Ex: Decrease in supply and an increase in demand:

Price rises for both but quantity decreases for supply and increases for demand. Therefore: The quantity is indeterminate

Price elasticity of demand

Responsiveness of consumers to a change in price

In a graph: the steeper the demand curve, the more inelastic

3 Ranges of Elasticity

If Elasticity > 1, demand is elastic

if elasticity > 1, demand is inelastic

If elasticity = 1, demand is unit elastic

Determinants of Elasticity of Demand

(Note: The more broadly the market is defined, the less elastic demand is)

1. Availability of Substitutes

- Lots of substitutes = more elastic demand

- Few substitutes = Less elastic demand

2. Proportion of budget spend on the good

- More budget spent = more elastic

- Small budget spent = Less elastic

This is because if you are investing more money into something, you are more likely to actually change how much you want it

3. Time

- More time to make a decision = Demand is more elastic

- Less time = less elastic

This is because if you have more time to think about your decision, you are more likely to change

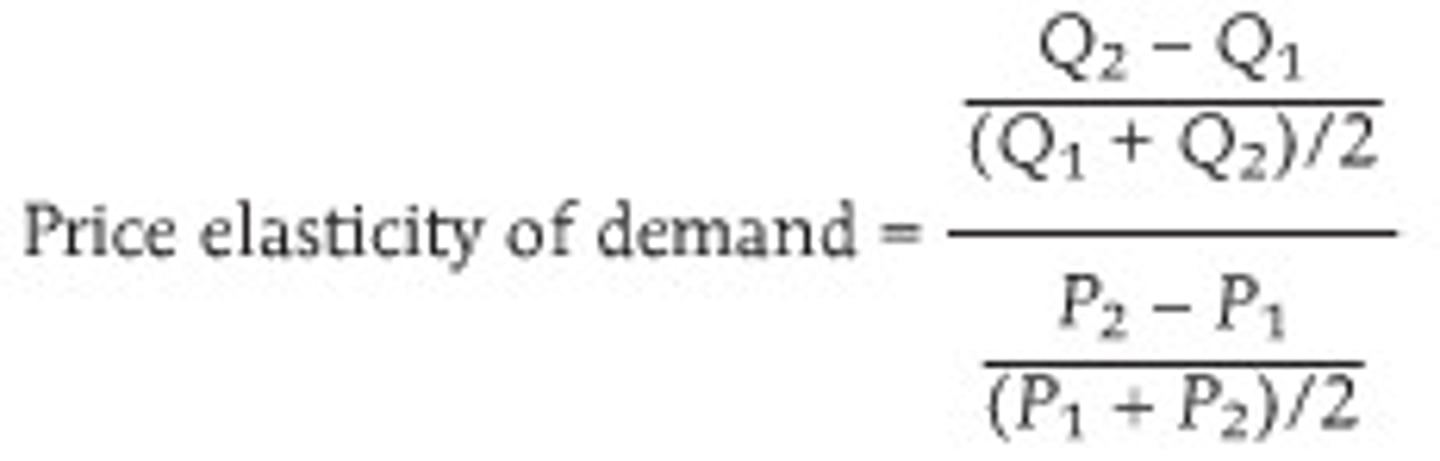

Calculating Price Elasticity of Demand

Absolute Value(Change in Quantitiy/Change in Price * Average Price/average quantitity)

Where in the graph is it elastic, inelastic, and unit elastic

At the midpoint, the graph is unit elastic. At loser prices (Left of the graph) demand is more elastic. At higher prices (right of the graph) demand is less elastic

Perfectly Inelastic Demand

Vertical Line (Does not really exist)

Perfectly Elastic Demand

Demand is Horizontal (If the price was risen at all, everybody would not buy it)

Revenue

Price times quantity demanded

It is effected depending on elasticity

When it is inelastic - Increase in price is more revenue, decrease is less revenue

When it is elastic - Increase in price is less revenue, decrease is more revenue

If it is unit elastic - Revenue is maximized

Cross-price elasticity

It is the same formula as Elasticity, except you are comparing 2 different products. (for example you would compare the change in price of one item vs the change in quantity of a second item) (NO ABSOLUTE VALUE)

Positive number = Substitute

Negative number = complement

Income elasticity

Measures how income affects demand/spending

Positive: Normal Good

Negative: Inferior good

Percent change in quantity/Percent change in income

Price Elasticity of Supply

How sellers react to a change in supply

Greater than 1 is elastic,

less than 1 is inelastic,

1 is unit elastic

Formula is the same as elasticity of demand

Determinants of Elasticity of Supply

1. Availability of substitute inputs

- Fewer substitutes = Less elastic

- more substitutes = More elastic

2. Time

- More time = More elastic

- Less time = Less elastic

Extremes of Elasticity of Supply

Identical to demand,

Vertical = Perfectly Inelastic (happens in the real world where no matter how much you change the price, you can't increase supply, in the short term)

Horizontal = Perfectly Elastic (Probably wouldn't happen in real life, but if any small change in price happened, you would completely stop producing, or produce infinitely)

Consumer Surplus

Extra value received by a consumer from a product above the listed price

Producer Surplus

The difference between the price they are selling a product for and what the lowest price they would ever sell the product for.

Total Surplus

Consumer and producer surplus together

Maximized at equilibrium

Deadweight loss

The decrease in consumer and producer surplus from an inefficient level of production

Obstacles to efficiency

Price controls & Quotas

Taxes

Lack of competition

Public goods

Externalities

High transactions cost

Symmetry Principle

people in similar situations should be treated similarly

Utilitarianism

Achieve the greatest happiness for the greatest number

Maximin Principle

Make the poorest person as well off as possible

Tax the rich and redistribute to the poor until nobody is the poorest

Price Ceiling

The maximum legal price

Ex: Rent controls, salaray caps, utilities

Price Floors

Minimum legal price

Ex: Minimum wage, agricultural price supports

Allocating a Shortage

1. Lines (waiting) --> Increases cost because your paying in time

2. Circumvent the rule - "Black market price" (offer more money under the table)

3. Lottery

4. Rationing

5. Competitions

6. Discrimination

7. Violence

Black Market Price

Plug in the quantity supplied number into the Demand equation to find the price somebody would be willing to pay in the black market

Excise Tax

Per unit tax

Tax Incidence

The division of burden of the tax between buyers and sellers

Whoever is less elastic tends to bear less of the burden

Quota

Maximum quantity that can legally be sold.