markets

arrangements between buyers and sellers of a good or service to make an exchange

Demand

An individual consumer’s willingness and ability to buy goods or services at different prices during a specific period of time (all else being equal)

Law of Demand

A negative causal relationship between a goods price and its quantity demand in a particular period of time (all else being equal)

the law of diminishing marginal utility

consumers derive utility from goods and services, the more we consume the less marginal utility (satisfaction goes lower)

substitution effect

when the price of a good decreases, consumers opt for the cheaper substitute good

income effect

the higher the consumer’s income, the more they will want and can buy of the preferred good

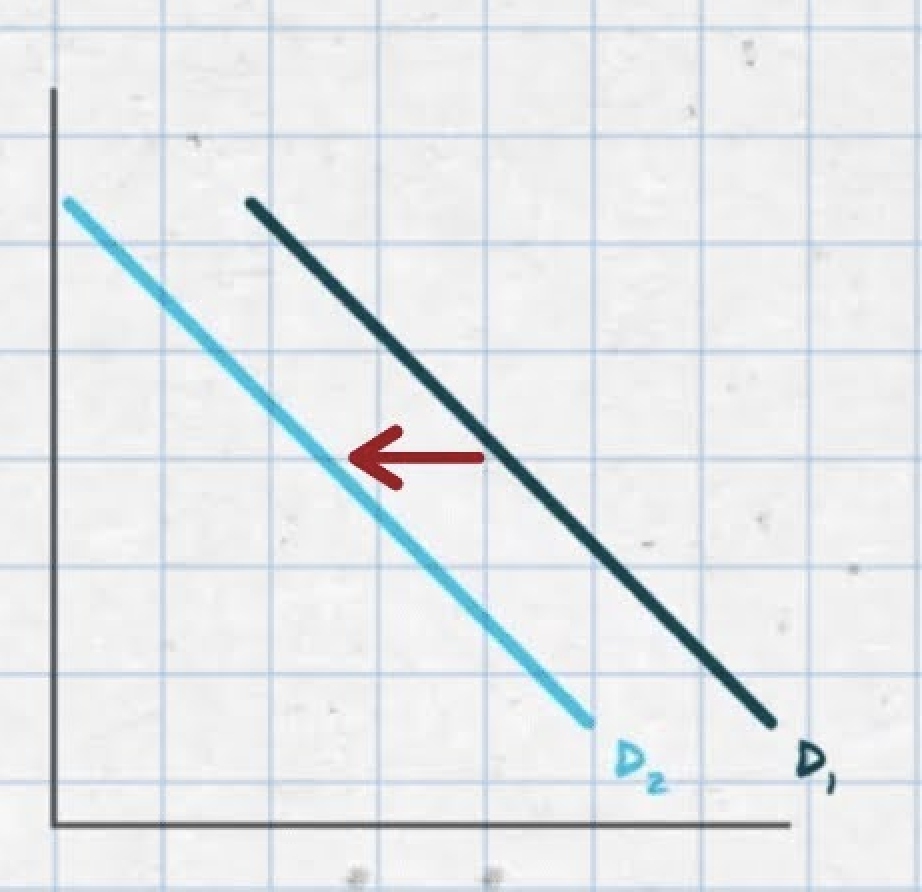

Non price determinants of Demand (CTFPS)

changes in income

tastes and preferences

future price expectations

price of related goods

size of market

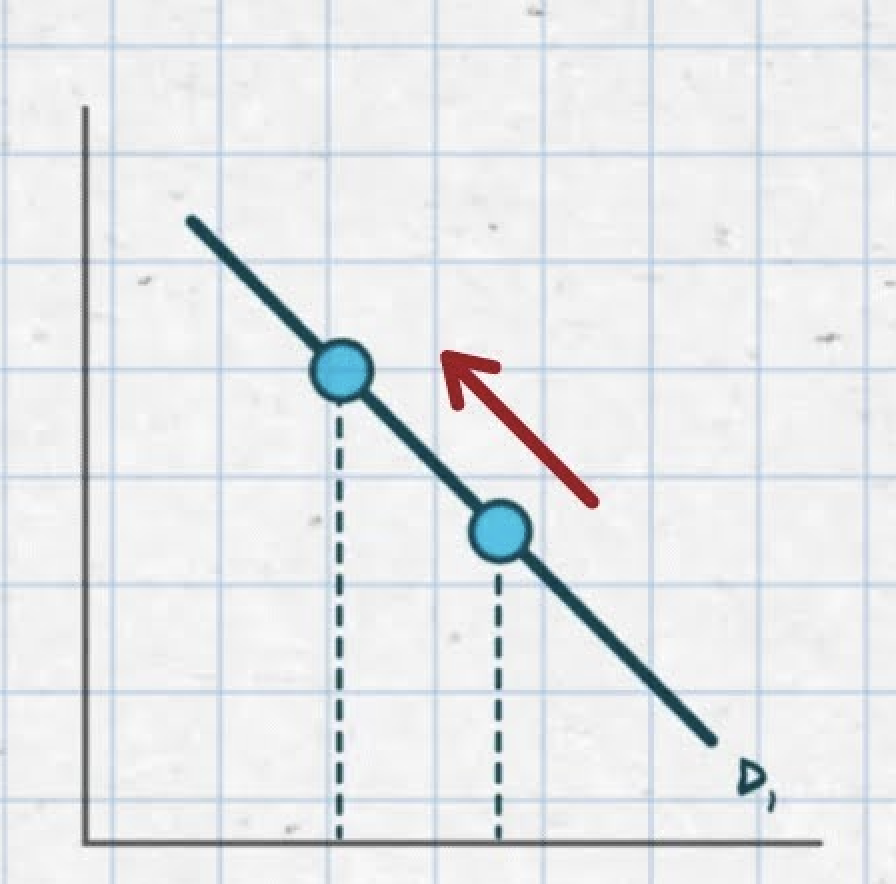

Quantity Demand vs. Demand

change in demand means that the change in Quantity Demand will change at every price.

Quantity Demand

the total amount of goods and services that consumers need or want and are willing to pay for over a given time

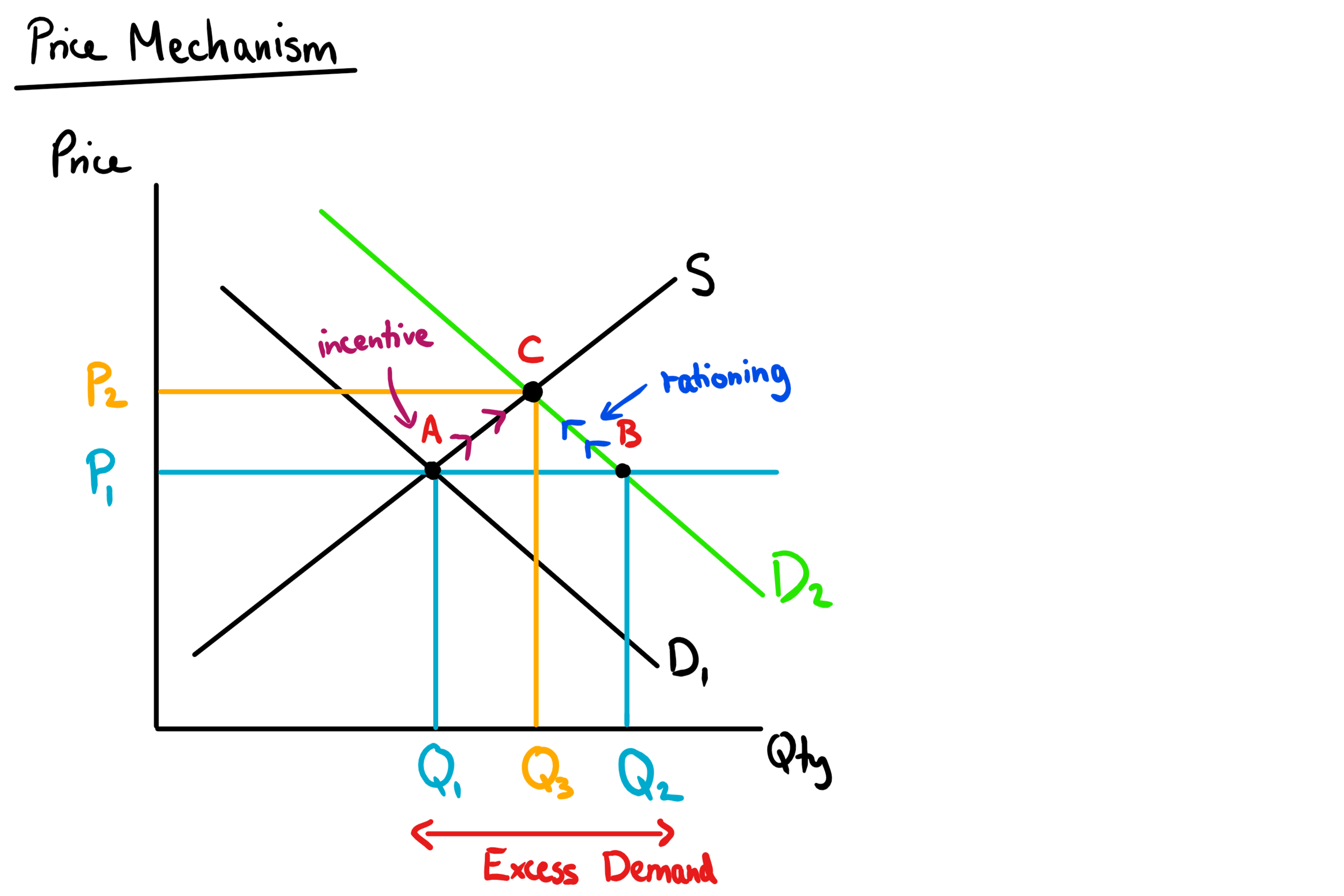

draw a diagram showing the functions of price mechanism

Supply

individual firms’ willingness and ability to produce various quantities of goods and services at different prices during a specific period of time (all else being equal)

Law of Supply

Positive causal relationship between a goods price and its quantity supplied in a particular time period (all else being equal)

Short run supply

at least one factor of production is fixed

Long run supply

All factors of production can be changed

Total Product

Total amount of output produced by a firm

Marginal Product

additional output produced by a firm if one additional unit of variable input is added.

Average Product

Total quantity of output per unit of variable input

how does MP and TP relate, illustrate with diagrams

Law of Diminishing marginal returns

as more units of variable inputs (labor) are added to fixed inputs (capital), the marginal product of the variable input will increase, but at some point will decrease, because efficiency goes down.

Marginal Cost

Cost of Producing additional input

consumer expenditure calculation

P x Qd

Marginal Product calculation

change in TP / change in units of labour

Average product calculation

TP / units of labour

marginal cost calculation

change in TC / change in Q

Non Price Determinants of Supply (STORES)

subsidies and taxes

tech advancements

other related goods prices

resource costs

expectations of future prices

size of market

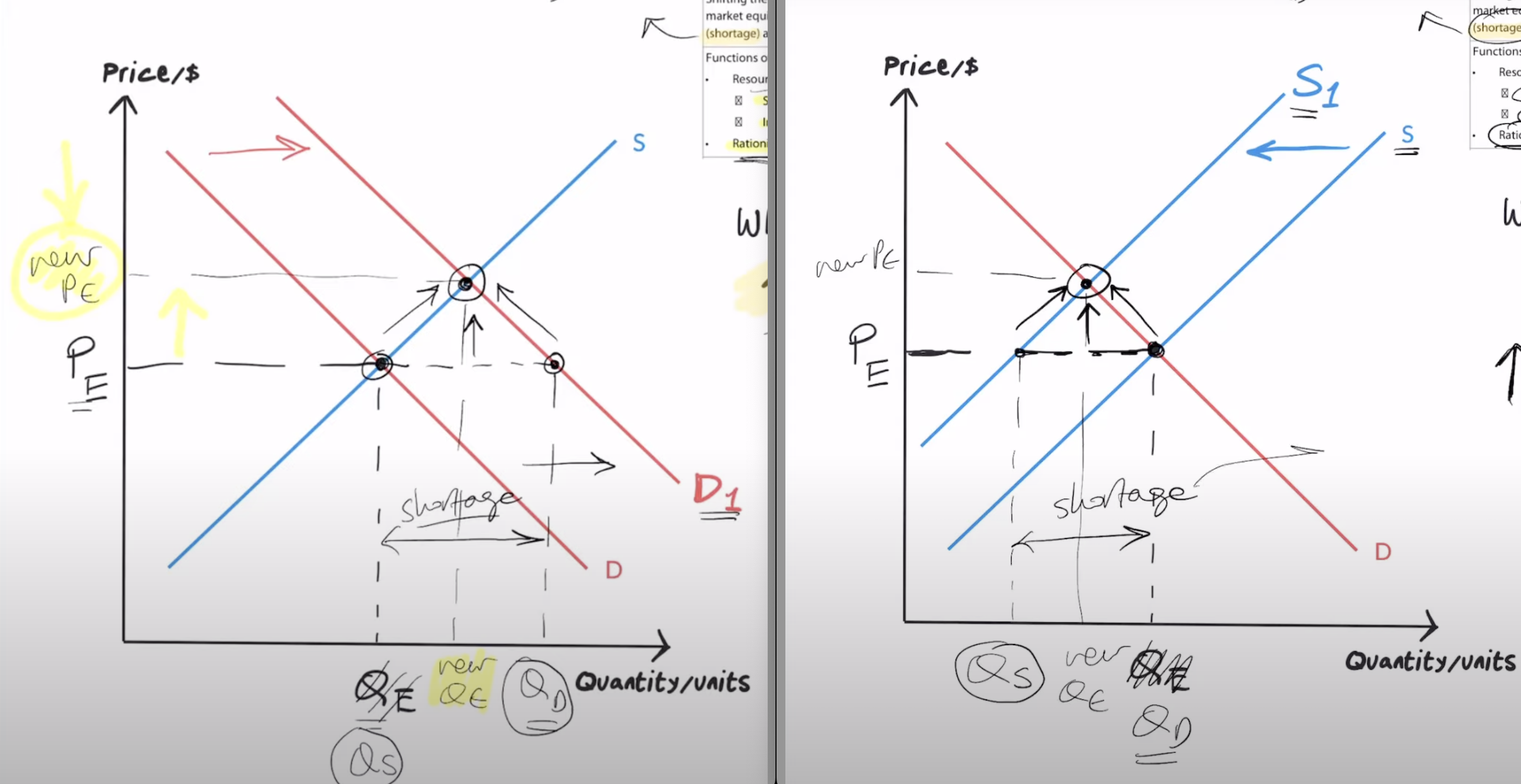

Equilibrium

market quantity supplies meets market quantity demanded and there is no tendency for the price to change (they are equal to one another)

Disequilibrium

at any price other than equilibrium price - quantity demand is not equal to quantity supplied = shortage or surplus.

when does equilibrium change

when one of the non price determinants are considered.

Marginal Social Benefit

equal to demand, benefit derived from consuming a good or service.

Marginal Social Cost

equal to supply, cost to society for producing a good or service

allocative efficency

producing combination of goods most wanted by society.

productive efficency

using the fewest possible resources

consumer surplus

the benefit consumers get from paying a price lower than the highest price they are willing to pay.

producer surplus

benefit that producers get from receiving a price higher than the lowest price they are willing to sell at

PS/ CS Calculations

base x height /2

Social surplus

CS + PS

rational economic decision making

society acts on their own best interest;

consumers maximise satisfaction

producers maximise profits

Consumer rationality

consumers buy goods based on tastes and preferences

Consumer rationality assumptions

completeness assumption (a or b)

transitivity assumption (a-b, b-c, a-c)

non satiation assumption (2a or 3b)

perfect information

knowing everything about a good or service and its alternatives

utility maximisation

maximizing utility when purchasing goods based on budget or income

rule of thumb (cognitive bias)

simplifying complex decisions based on common sense

anchoring (cognitive bias)

making a decision based on first piece of info one heard (disregarding relevance)

framing (cognitive bias)

how much information the consumer is given

availability (cognitive bias)

consumer relies on more recently available info, no matter reliability.

bounded rationality

consumers are rational but with limits to amount of info

bounded self control

consumers don’t have self control in decision making

bounded selfishness

people are selfish when making decisions

imperfect information

consumer rarely has perfect information = unable to maximise utility

nudge theory

method to influence consumer choices in a predictable way

choice architecture

design of how people make decisions;

default choice

restricted choice

mandated choice

rational producer behaviour

firms are guided by goal to maximise profits

profit calculation

total revenue - total costs

corporate social responsibility

firms engaging in socially beneficial activities

market share

firms engaging in activities to maximise percentage of sales in a particular market

growth maximisation

aiming to achieve growth rather than profit

satisficing

trying to achieve satisfactory level of profits and satisfactory level of objectives

shortage

Qd > Qs

surplus

Qs > Qd

surplus calculation

Qs - Qd

shortage calculation

Qd - Qs

What to shade when asked how total revenue changes?

Gain and Loss

Total revenue calculation

P x Q

Dead Weight Loss

(Pnew- Pold) x (Qold - Qnew)/2

Change in Qd

Change in Demand

What is the Price Mechanism

provides incentives to producers and consumers by rewarding those who respond to changes in the market