Economics

1/31

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

32 Terms

Role of Government

Maintaining law and order, ensuring the needs of the people, and fostering positive growth for the future.

Fiscal Policy

The use of government spending and taxation to influence the economy.

Monetary Policy

Rules followed by central banks to monitor the money supply for sustainable economic growth.

Social Safety Nets

Programs like welfare, unemployment benefits, and social security to support the poor, elderly, and disabled.

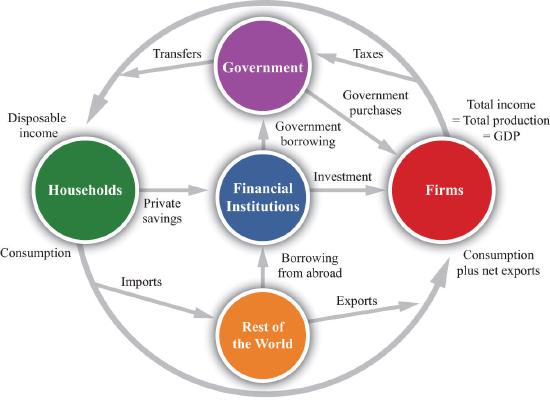

Circular Economy

Leakages

Money that exits the economy through savings, taxes, and imports.

Injections

Money that enters the economy through government spending, investments, and exports.

Resource Market

The market where households provide labor, land, capital, and enterprise to businesses.

Product Market

The market where businesses sell goods and services to households.

GDP (Gross Domestic Product)

The market value of all finished goods and services produced within a country in a year.

Intermediate Goods

Goods used to produce other goods that will be sold again.

Finished Goods

Goods that will not be sold again as part of another product.

Capital Goods

Goods used to create more goods, such as machinery or equipment.

National Spending Approach

A method of calculating GDP by summing consumption, investments, government purchases, and net exports.

GDI (Gross Domestic Income)

The factor income approach that includes income, capital interest, rent, and profit.

Economic Growth

The increase in the market value of goods and services produced by an economy over time, typically measured in real GDP.

Open Economy

An economy that engages in trade and has leakages such as financial markets and imports.

Closed Economy

An economy where households only spend money on firms, with no leakages.

Consumer Spending

Money spent by households on goods and services.

GDP Formula

Consumption + Investment + Government Spending + Net Exports

Economics

a social science that studies how human beings use their limited resources to satisfy their infinite needs and wants and how they improve their economic well-being. People cannot have everything they desire, and that is where economics comes in

Opportunity cost

the value of the next-highest-valued alternative use of that resource. If, for example, you spend time and money going to a movie, you cannot spend that time at home reading a book, and you cannot spend the money on something else. If your next-best alternative to seeing the movie is reading the book, then the opportunity cost of seeing the movie is the money spent plus the pleasure you forgo by not reading the book

Scarcity

People's needs and wants are unlimited, but it is not possible to produce all the goods and services to fulfil them, because the resources available are limited. Therefore, societies are forced to choose what it is they need or desire most

Production

The process of combining various inputs, both material (such as metal, wood, glass, or plastics) and immaterial (such as plans, or knowledge) in order to create output. Ideally this output will be a good or service which has value and contributes to the utility of individual

Consumption

the use of goods and services by households. Different from consumption expenditure which includes services and goods that have multiple uses like a car.

Sustainability

the ability of the present generation to meet its needs without compromising the ability of future generations to meet their own needs.

Equity

does not mean equal, but instead implies fairness. Everyone gets what they need

Equality

This means everyone uses the same resources and the same chances

Planned economy

Communism, where everyone gets everything from the government

(Bonus! What are the pros and cons of this variation)

Mixed economy

When a country where it is partly run by government and partly by businesses

(Bonus! What are the pros and cons of this variation)

Pure market economy

Everything is sold by businesses and there is no government intervention

(Bonus! What are the pros and cons of this variation)

How can an economy grow?

increase in household spending, employment rate, wages and exports