Economics: Production Functions, Costs, and Profit Analysis

1/27

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

28 Terms

Production Function

relationship between quantity produced and how many inputs (Q and L)

Firm

Organization that produces goods and services for sale

Product Curve

The change in output that results from employing an added unit of labor. MPL (∆Q/∆L). An illustration of the production function.

When does MPL reach max production?

When MPL = 0

When does a graph experience "increasing returns"

when slope is increasing

When slope is negative

graph experience "inflation" ,negative returns

slope is decreasing, but still positive. (inflection point)

graph experience "diminishing returns"

Explicit cost

Costs a business or individual receive when they directly pay for somth (visible)

Implicit cost

Costs an individual incurs when they choose one alternative over the other. (doesn't always relate to money)eg: if u open a bakery, costs of being able to win a salary from a standard 9-5

fixed input

an input whose quantity is fixed for a period of time and cannot be changed (in the short run at least one is fixed)

varied input

input whose quantity is can change at any time. (In the long run all inputs are varied)

short run

at least one input is fixed.

long run

all inputs can be changed (varied)

Fixed Cost

Independent of output (expenses that remain constant no matter the lvl of production)

Variable cost

dependent on output (eg output goes down cost goes down vice versa)

Opportunity Cost

Explicit + Implicit

Accounting Profit

total revenue - explicit costs

Total Revenue

Profit x Quantity

Economic Profit

Total Revenue - Opportunity cost

Normal Profit

Economic Profit = 0

EP>0

Good choice

EP<0

pick another alternative

Total Cost

fixed cost + variable cost

Marginal Cost

∆TC/∆Q

Fixed cost = Total cost

When quantity = 0

Average Fixed Cost

FC/Q

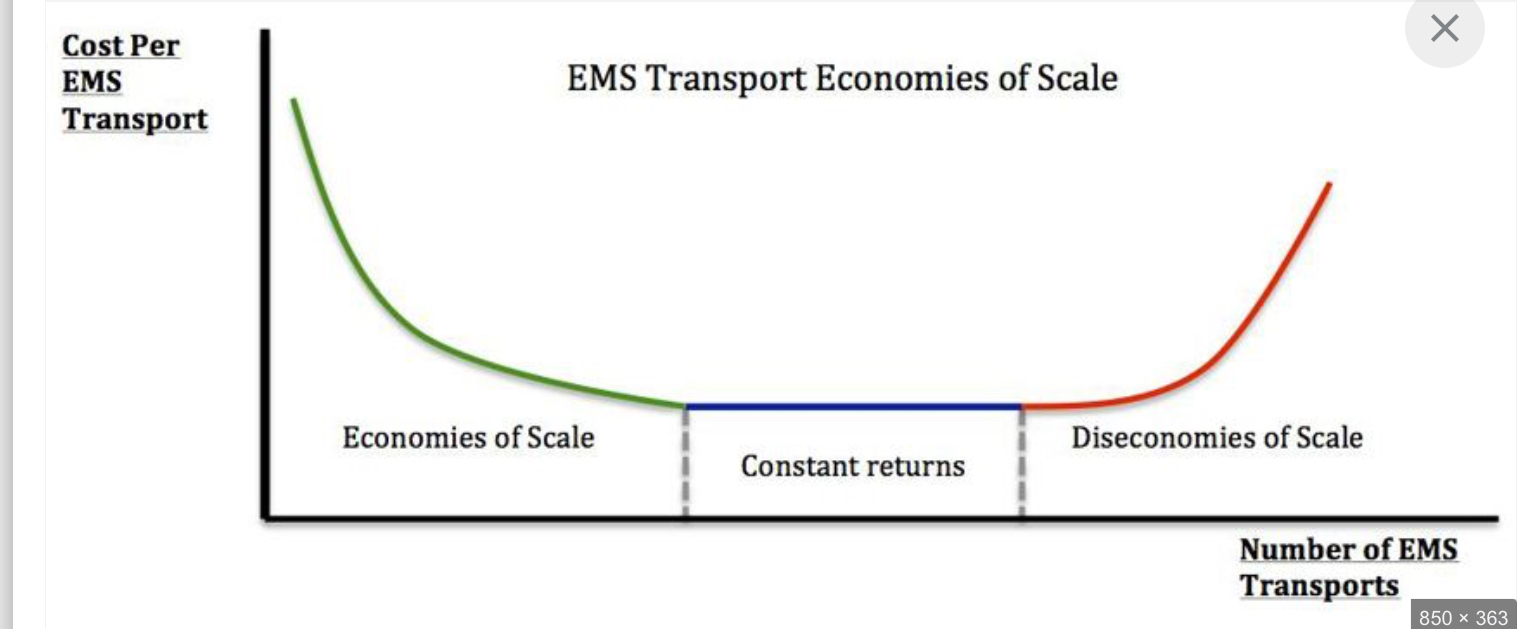

Economies of scale

Diminishing returns

benefit from adding one more unit of input eventually decreases