microeconomics graphs

1/25

Earn XP

Description and Tags

all the graphs i need to know

Name | Mastery | Learn | Test | Matching | Spaced |

|---|

No study sessions yet.

26 Terms

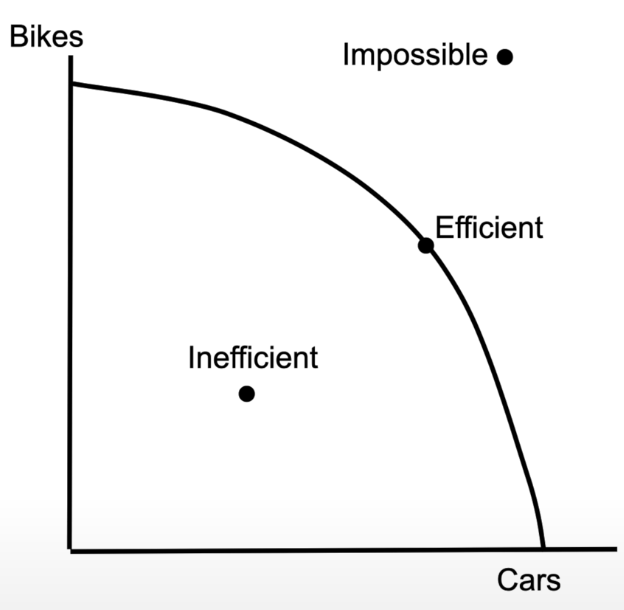

production possibilities curve

shows you can produce two different goods

any point outside the curve is impossible

any point inside the curve is inefficient

any point on the curve is efficient, as you are using all resources to the fullest

find the point on the curve that is most efficient for the socially optimal quantity (the quantity that society actually wants)

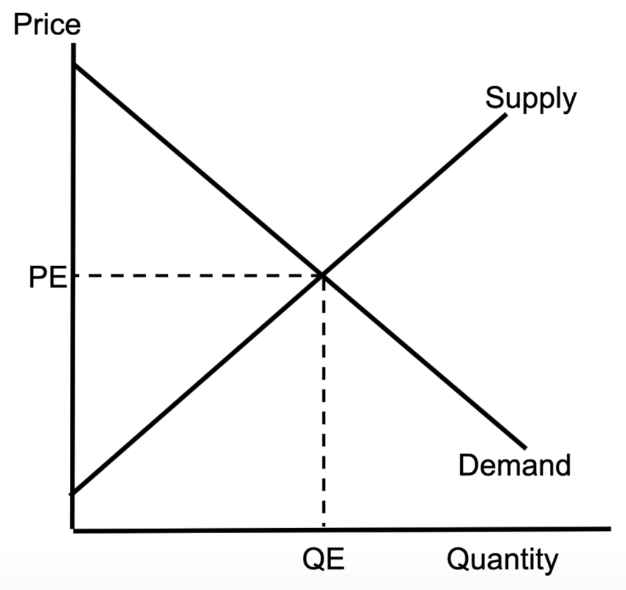

supply and demand

supply and demand showing a competitive market

shows equilibrium

curve shifting

consumer vs producer surplus

consumer surplus: what people are willing to pay for a good - what they actually pay

producer surplus: what people actually pay vs what suppliers wanted to sell it for

total surplus = sum of both

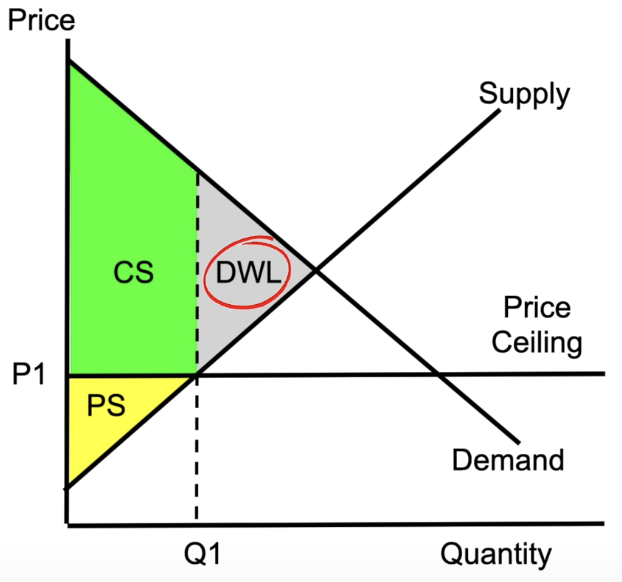

supply and demand with a price ceiling

eg. government limits the maximum price

causes a smaller producer surplus and larger consumer surplus

creates dead weightloss: the idea that we aren’t producing the socially optimal quantity (producing less than they want)

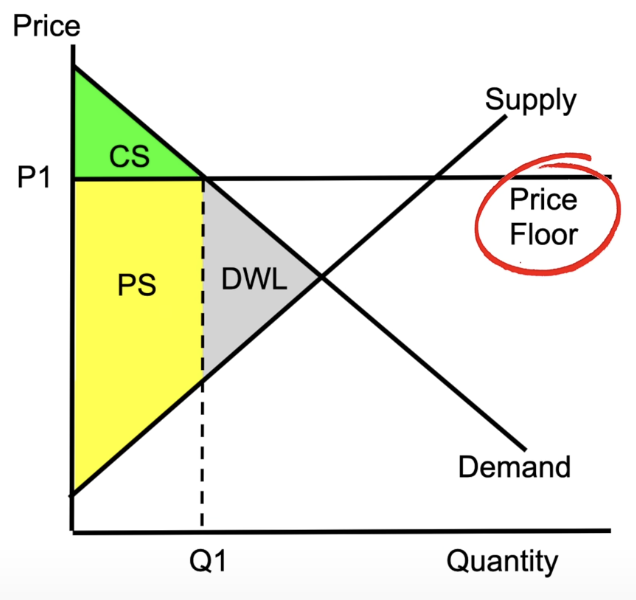

supply and demand with a price floor

eg. the price can’t fall below a certain point

causes smaller consumer surplus and larger producer surplus

creates dead weight loss: producing more than they want

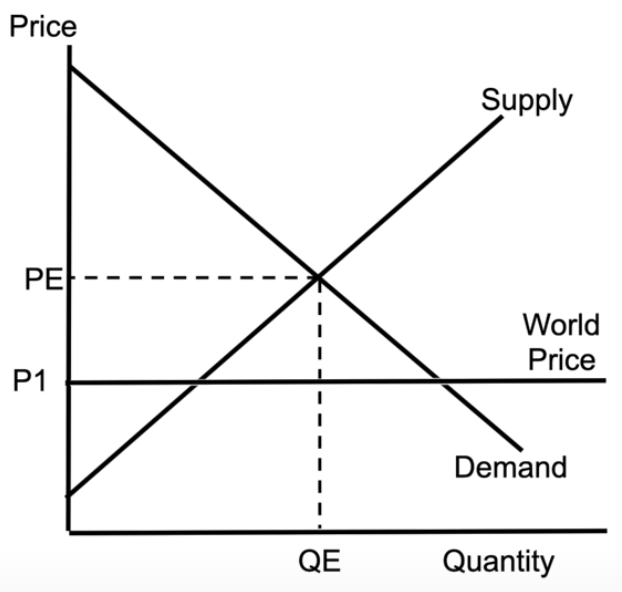

supply and demand showing result of trade

shows result of international trade

PE = domestic price of the product

P1 = the price we can get it for, if we buy it from other countries

no dead weight loss, which explains why economists like international trade

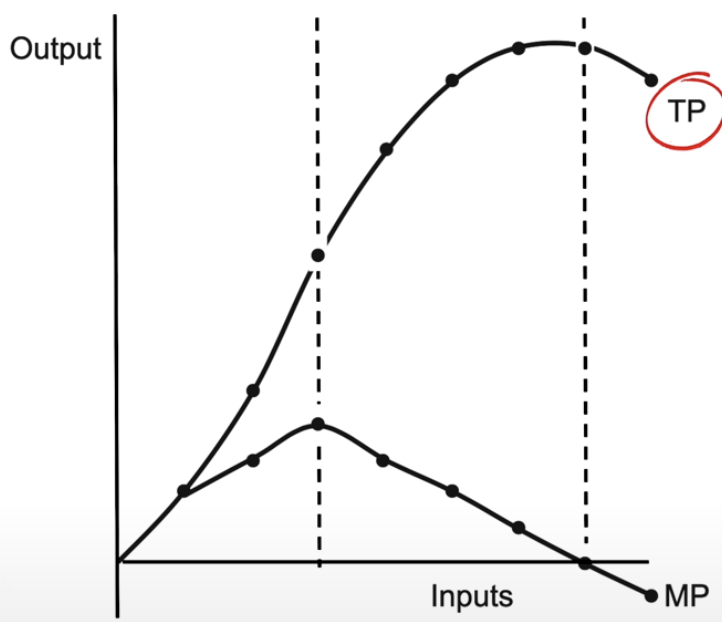

short-run production function

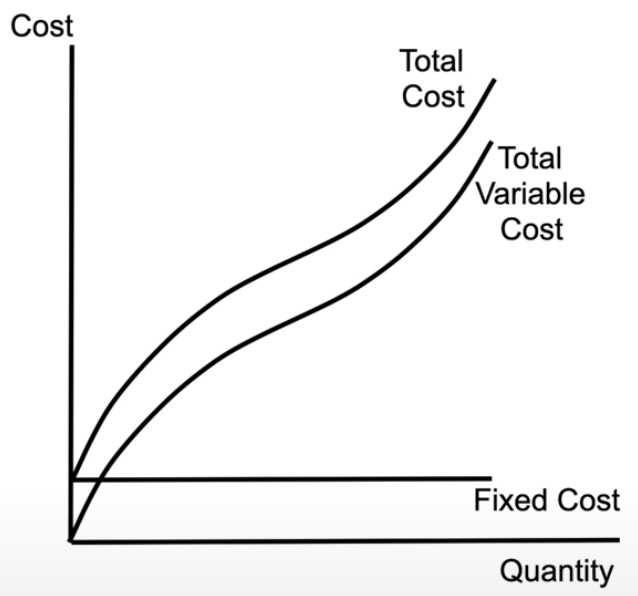

TP = total product = total amount produced

as you hire more workers TP increases at an increasing rate, then increases at a decreasing rate, then eventually starts decreasing

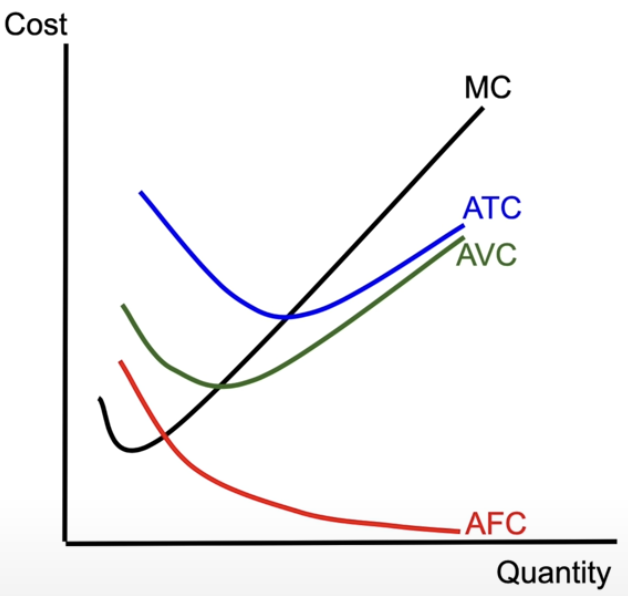

short-run per unit cost curves

MC = marginal cost → decreases then increases

tells you how much to produce

ATC = average total cost - decreases, hits a minimum, then increases

tells you how much profit or loss you’re making per unit

AVC = average variable cost → nears ATC

AFC = average fixed cost → asymptote heading toward y = 0

short-run total cost curves

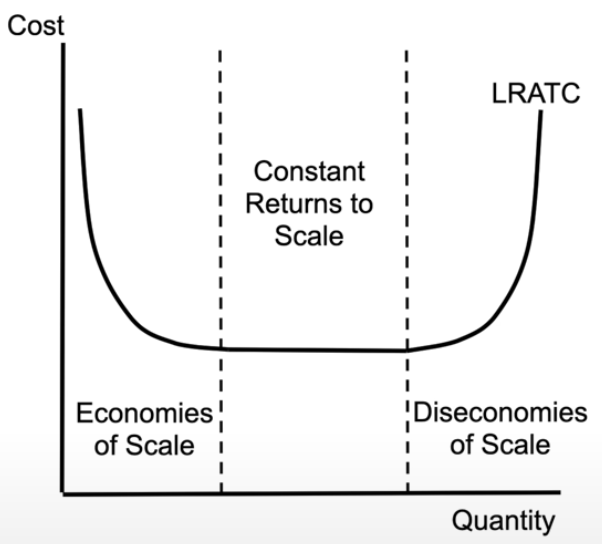

long-run average total cost curves

in the long run, if all of our resources are variable, we end up with this

shows all the sum of all short run curves

economies of scale = as a company produces more goods or services, the average cost per unit decreases

constant returns to scale: when you increase inputs to a production process by a certain proportion, the output will increase by the same proportion

diseconomies of scale = average cost per unit of production increases as its output increases

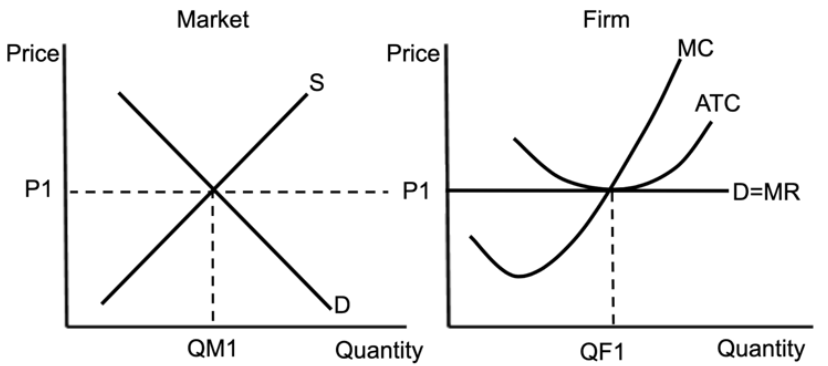

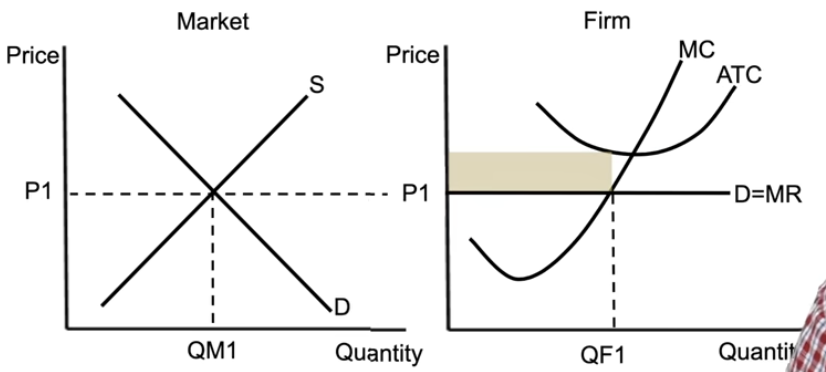

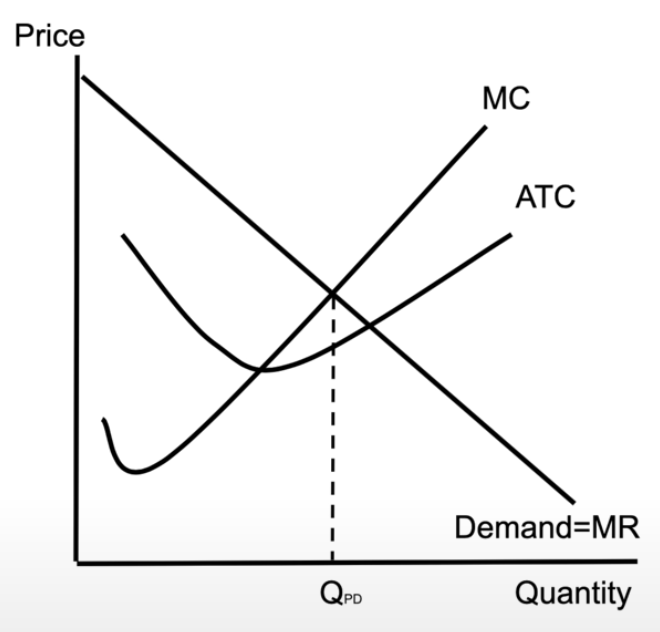

perfect competition (long run)

P1: the price is set by the market (price takers) → horizontal demand = marginal revenue curve

add in MC and ATC from short-run per unit cost curves

shows perfectly competitive firm in long-run equilibrium

you always produce where MR = MC → represents the profit maximising quantity

producing where price = marginal cost → producing amount society wants

producing at the lowest possible cost → producing productively efficient quantity

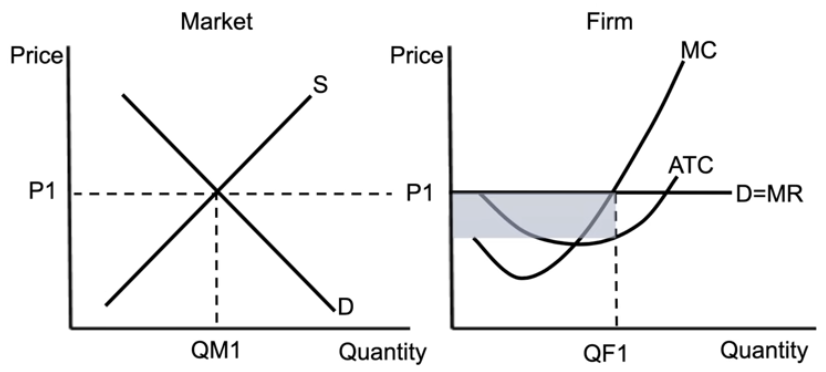

perfect competition short-run profit

the blue part

perfect competition short-run loss

the yellow part

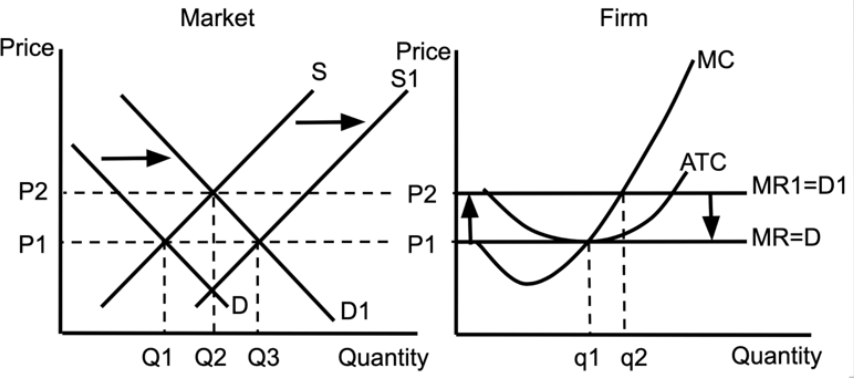

perfect competition from long run to short run back to long run

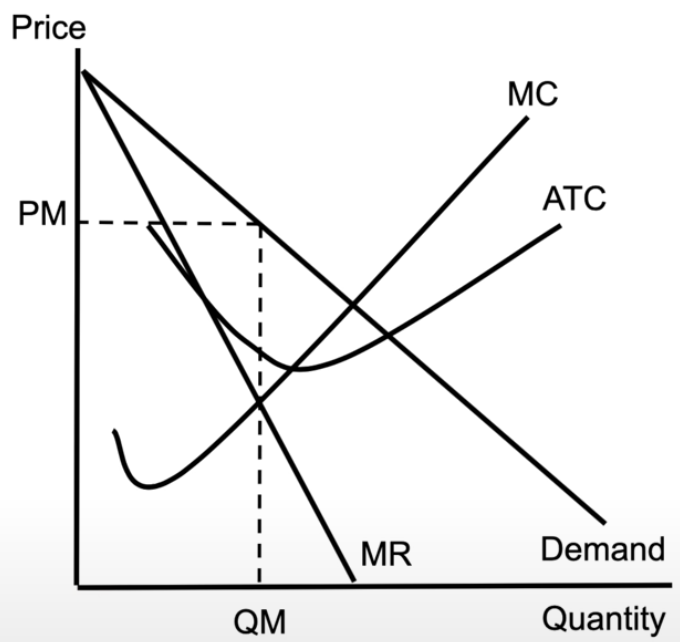

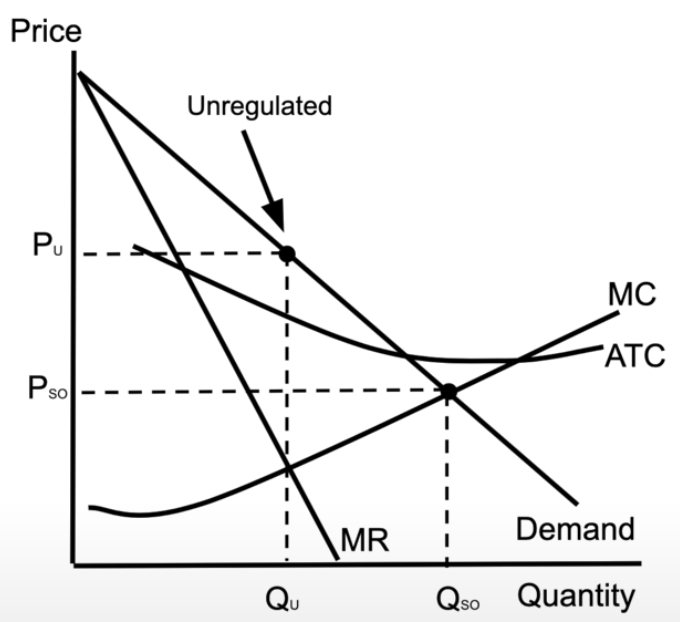

non-price discriminating monopoly

downward sloping demand curve

downward sloping marginal revenue curve

MC and ATC stay the same shape

still produce where MR = MC

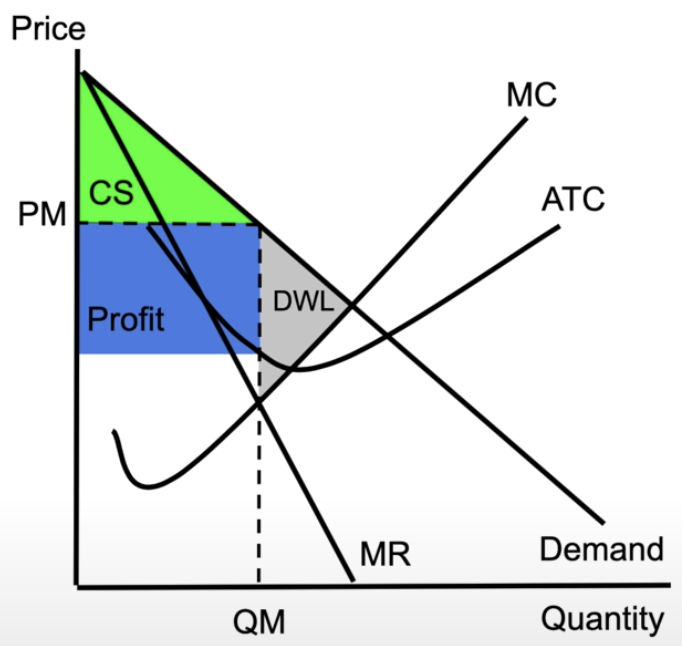

monopoly making profit

a monopoly is not allocatively efficient

not producing what society wants

it holds back production to maximise profits

monopoly making loss

monopolistic competition in the long run

ATC is tangent to the demand curve, showing no economic profit in the long run

natural monopoly

where the MC hits the demand curve (= the socially optimal quantity), the ATC is still falling

this means that the firm can produce the product at the lowest possible cost

price discriminating monopoly

the monopoly is charging each consumer exactly how much they are willing to pay

demand curve = marginal revenue curve, and there is no consumer surplus → all of it becomes profit

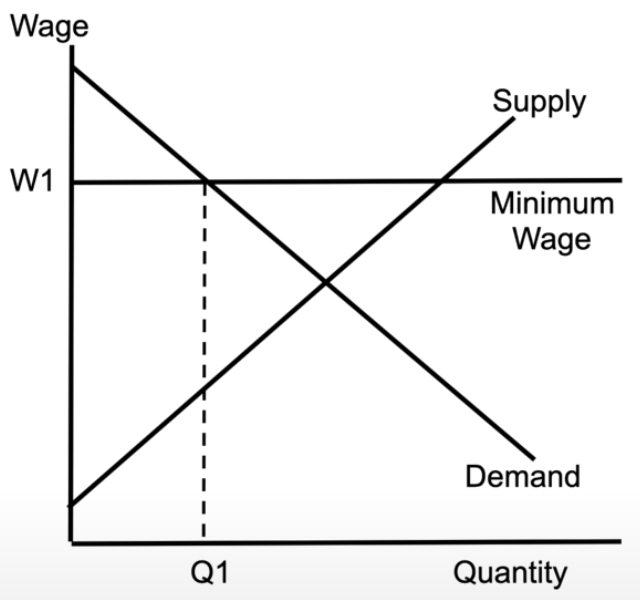

labour market (minimum wage)

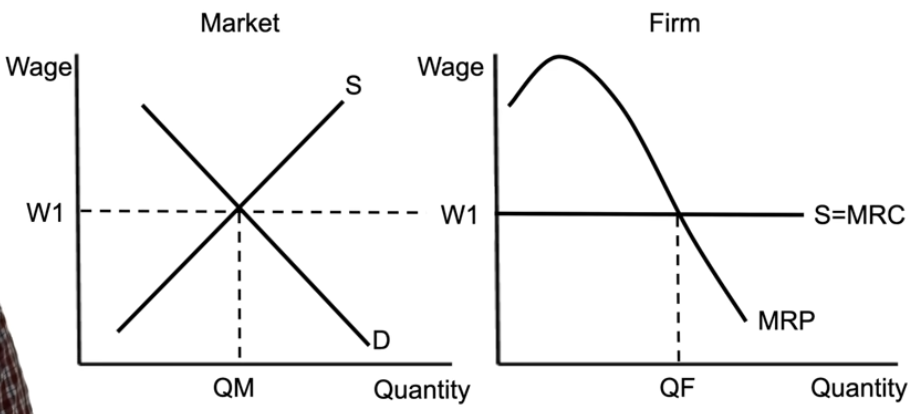

perfectly competitive resource market and firm

perfectly competitive firm in the resource market = a firm hiring workers

the wage for the firm is set by the market, gives you a horizontal supply curve, which = marginal resource cost

marginal revenue product = how much each worker generates → downward sloping, tells you exactly how many workers to hire (where MRP = MRC)

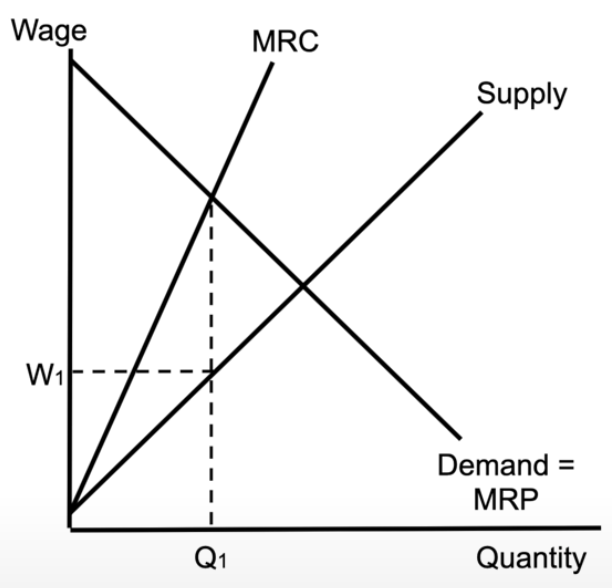

monopsony

there is only 1 firm hiring, so the supply of labour is upward sloping

there is an upward sloping marginal resource cost

you hire where MRC = MRP

the wage is below the equilibrium wage that would exist at perfect competition

firms that hire workers at a lower wage, because they are the only firm hiring

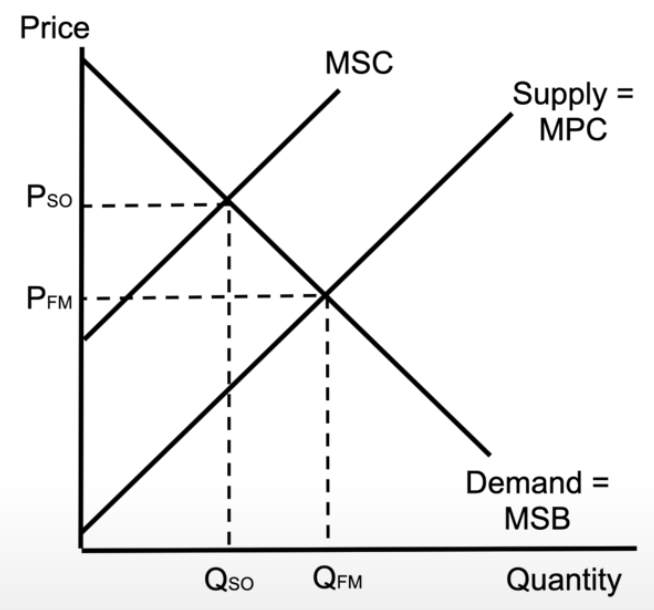

negative externality

supply and demand show you the quantity produced in the free market → the free market quantity is wrong

if this product creates a negative externality and there is additional costs on society, we end up with a marginal social cost (MSC)

MSC hits marginal social benefit, which shows the socially optimal quantity, which is less than the free market is making

result: dead weight loss (overproducing, because we didn’t take into account the additional costs on society)

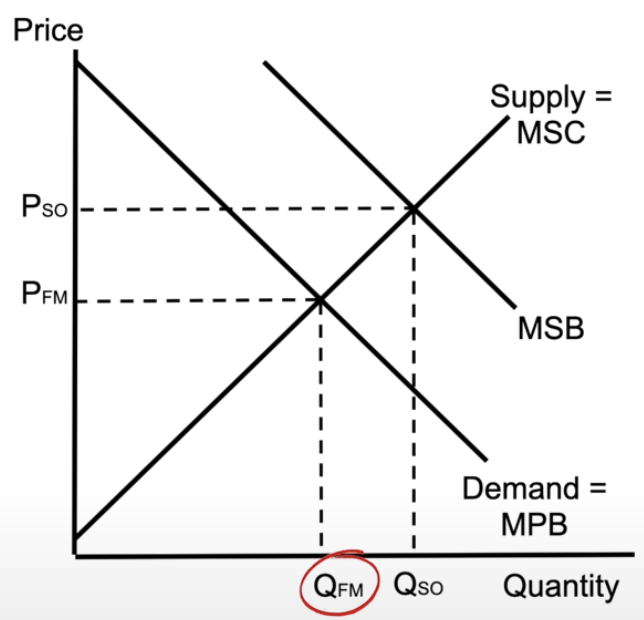

positive externality

quantity of the free market is less than the socially optimal quantity

not factoring in all the additional benefits that society gets from the product

dead weight loss → the free market is underproducing something that society wants more of

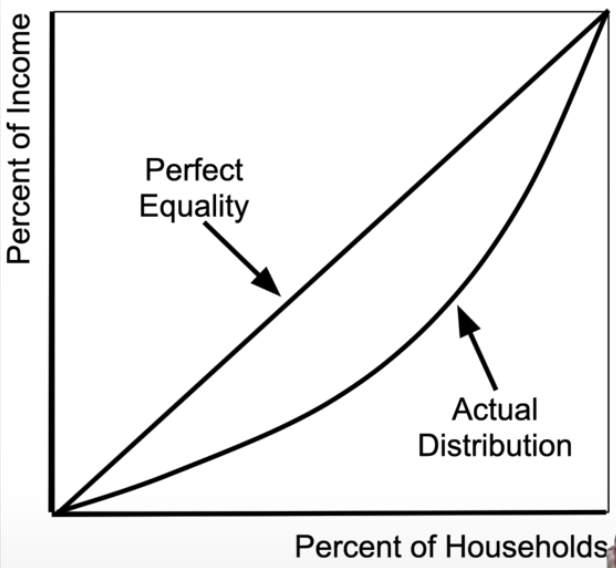

lorenz curve