Market Equilibrium

1/19

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced |

|---|

No study sessions yet.

20 Terms

Market

A market is where goods and services as well as factors of production are exchanged between two parties; buyers and sellers

There are two types of markets

Goods and services market: the market that exchanges goods and services

Factor market: the market that exchanges factors of production such as land, Labour, and capital

Functions of a market

In a market, goods and services are demanded by consumers and supplied by producers

Households demand goods & services while firms demand factors of production. On the other hand, firms supply goods and services for consumption, while households supply factors of production.

Demand for factors of production exists due to the demand for goods and services.Therefore, goods and services have a direct demand while production factors have an indirect demand/derived demand.

Demand for goods and services for consumption depends on their marginal utility while the demand for factors of production depends on their marginal productivity.

Goods and services market and factor services market

Goods and services market | Factor services market |

Exchange of consumer goods and services | Firms demand factors of production |

Firms supply goods and services | Households supply factors or production |

Goods and services have a direct demand | Factor services have an indirect demand |

Market equilibrium

Market equilibrium is the situation where the expectations of purchasers and suppliers at a competitive market equal each other

At that situation, there’s no excess demand or excess supply as quantity demanded equals to quantity supplied,

there’s no excess demand price or excess supply price as purchasers expected price equals to suppliers expected price

Conditions of market equilibrium

Expected demand price should be equal to expected supply price

Expected quantity demanded should be equal to expected quantity supplied

Excess demand and excess supply must be zero

Expected demand price and expected supply price should be zero

Consumer expenditure and producer revenue should be equal to each other

Two outcomes or the product market equilibrium

The equilibrium price (Pd= Ps)

This is called the equilibrium price because the demand price of the product is equal to the supply price of the product.

Demand Price = Supply price

Pd = P

The equilibrium quantity

This is called the equilibrium guantity because the quantity demanded of the product is equal to the quantity supplied.

Quantity demanded = Quantity supplied

Qd = Qs

Excess demand

The amount of quantity demanded which exceeds the amount of quantity supplied at a certain price is called as excess demand

Excess demand = (Quantity demanded-quantity supplied)

ED= Qd-Qs

Excess supply

The amount of quantity supplied which exceeds the amount of quantity demanded at a certain price is called as excess supply

Excess supply= ( Quantity supplied- Quantity demanded)

ES= Qs-Qd

Excess demand price

Excess demand is the amount by which the demand price exceeds supply price at a certain quantity

Excess demand price = demand price- supply price

EDP = Pd-Ps

Excess supply price

Excess supply price is the amount by which supply price exceeds demand price at a certain quantity

Excess supply price= supply price- demand price

ESP= Ps-Pd

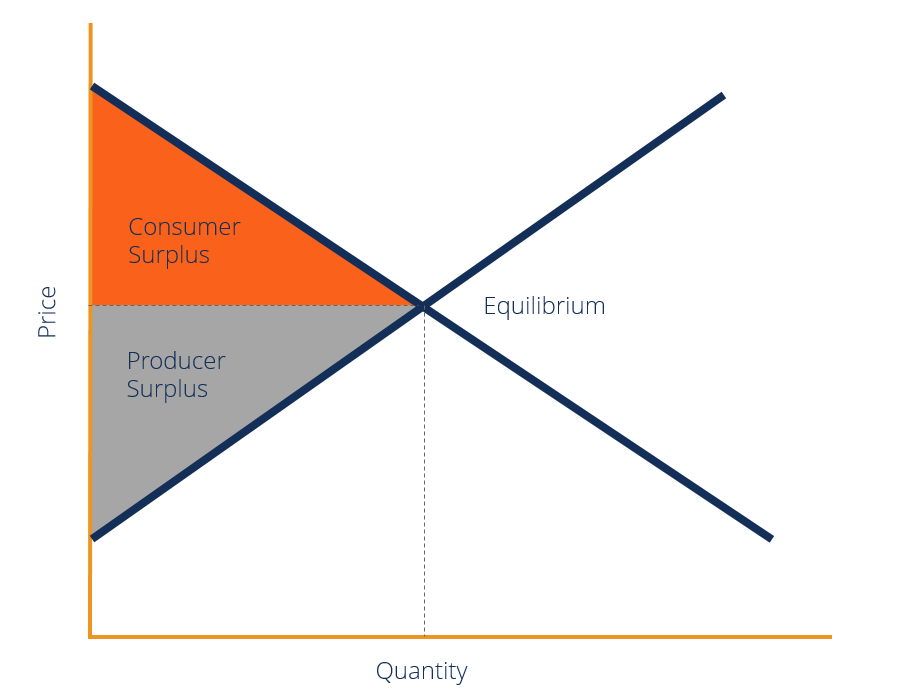

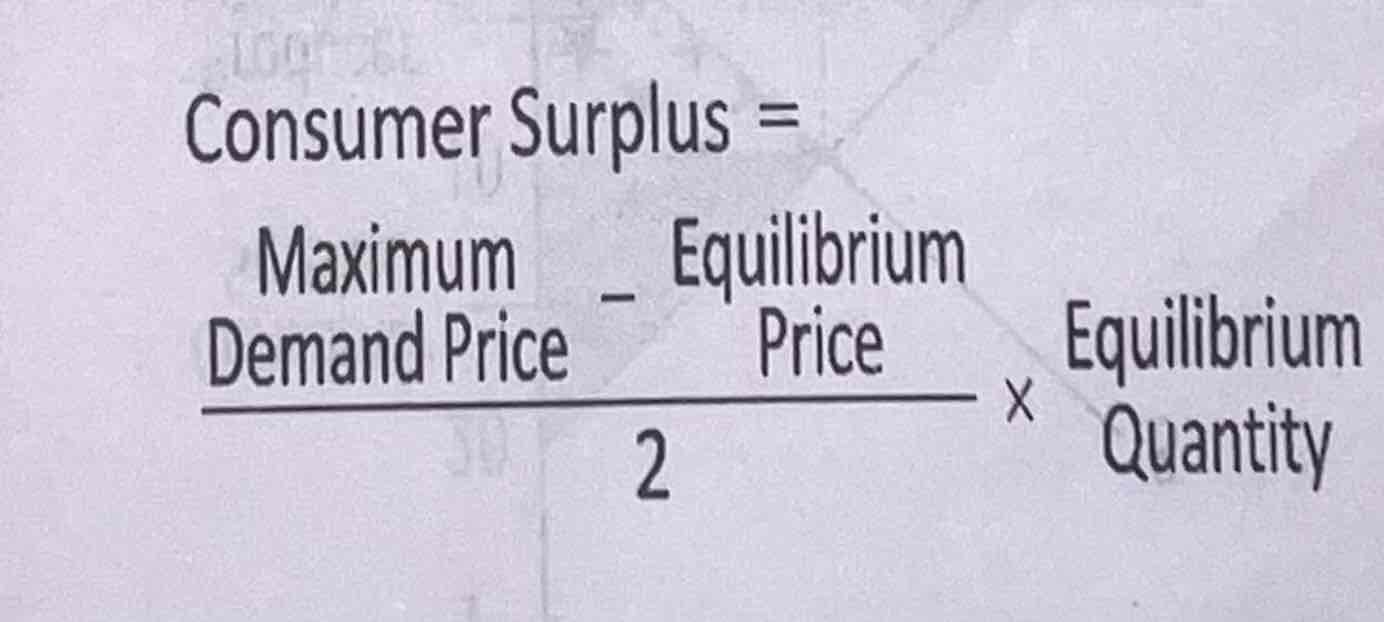

consumer surplus

The difference between the price that the consumer is willing to pay and the price that the consumer actually pays for the quantity of the goods exchanged at the market

Market equilibrium price is the price which consumer pays for goods and not the price consumer is willing to pay. The price that the consumer is wiling to pay may be higher than that price.

When consumers expect to pay a higher price, the demand and supply determines a suitable price which remains as an equilibrium price. This creates a beneficial situation for consumers as Consumers get a surplus for what they don’t actually pay

Consumer surplus

Consumer surplus equilibrium

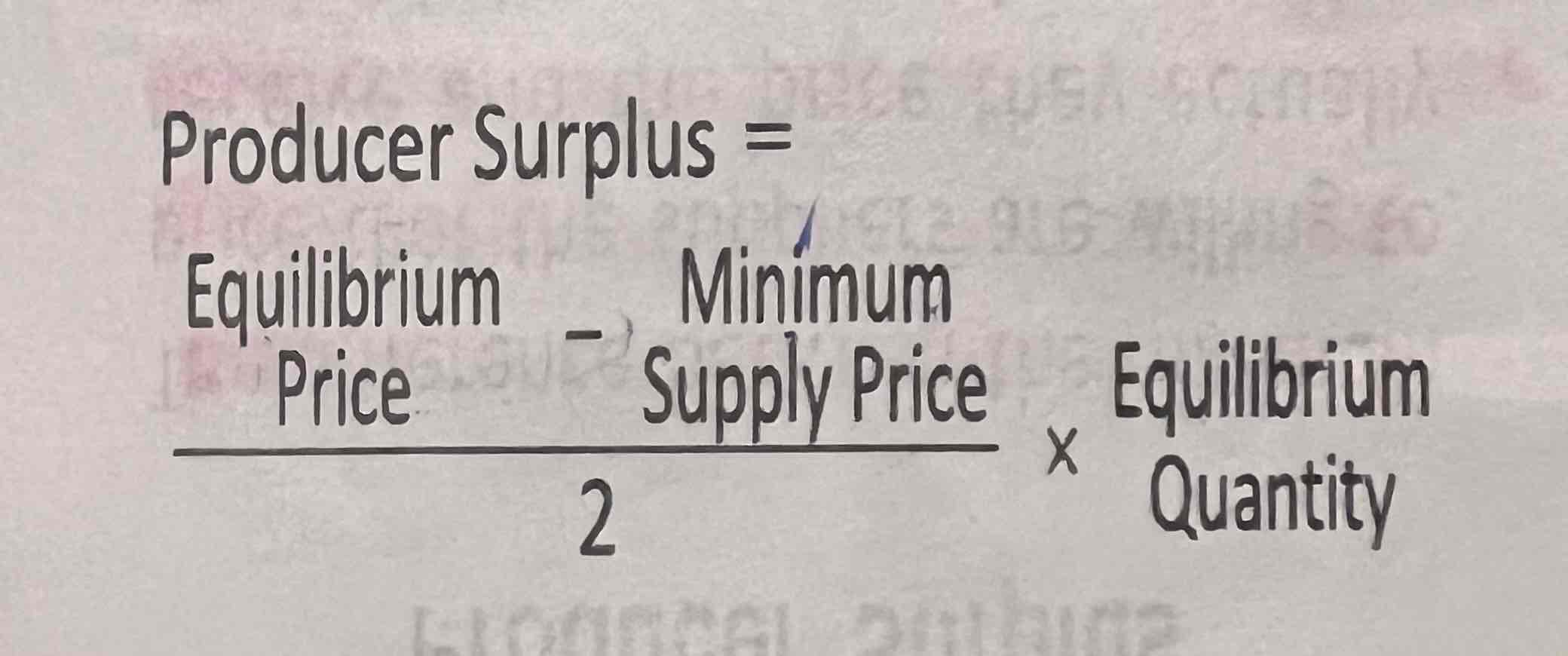

Producer surplus

The difference between minimum price that the suppliers are willing to receive and the price they actually receive

The balance obtained by reducing total variable cost from total revenue is the producer surplus

Producer surplus calculation

Economic surplus

Buyers and sellers gain profits through the equilibrium exchange, the gain achieved by both parties is called economic surplus.

Economic surplus = consumer surplus + producer surplus

Increase in demand and increase in supply

The impact on equilibrium price is uncertain

The equilibrium quantity definitely increases

Increase in demand and decrease in supply

The equilibrium price increases

Equilibrium quantity is uncertain

Decrease in demand increase in supply

The equilibrium price falls

Equilibrium quantity is uncertain