Ch.5 Supply Decisions and Factors of Production

1/23

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced |

|---|

No study sessions yet.

24 Terms

Supply

The ability and willingness to sell (produce) specific quantities of a good at alternative prices in a given time period.

Factors of Production

Resource inputs used to produce goods and services (Land, labor, capital, and entrepreneurship).

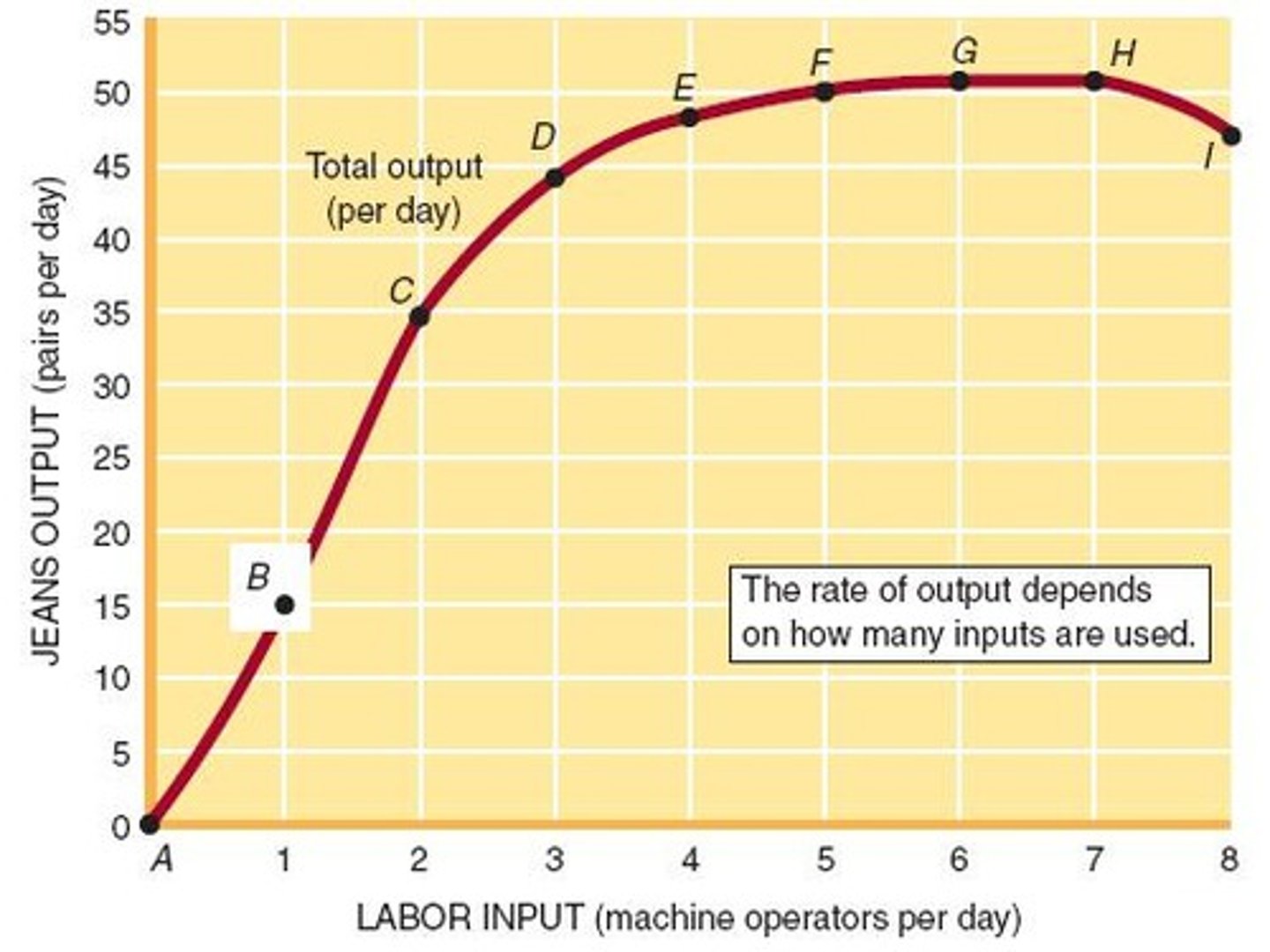

Production Function

Technological relationship expressing the maximum quantity of a good attainable from different combinations of factor inputs.

Efficiency

Achieving the maximum output attainable from given inputs.

Marginal Physical Product (MPP)

Change in total output associated with one additional unit of input.

Law of Diminishing Returns

Diminishing MPP; additional units of resources (inputs) are less valuable to the firm.

Negative MPP

MPP may become negative if too much labor is added to a fixed level of capital and land.

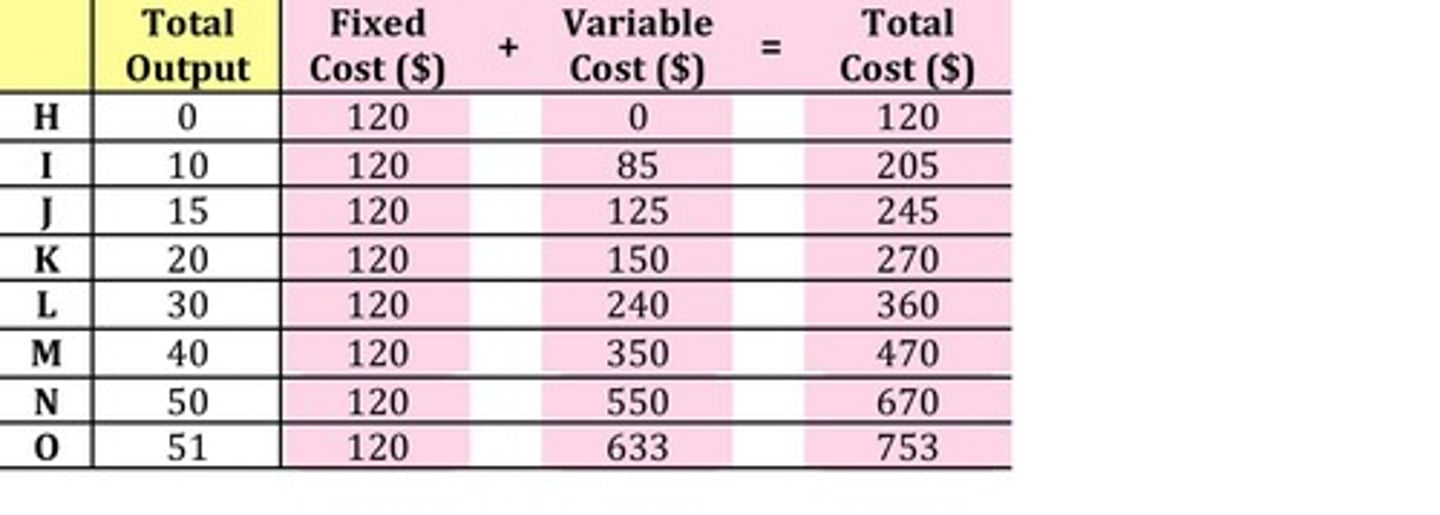

Cost of Production

Production function tells us how much a firm could produce but not how much it will want to produce.

Total Profit

Total profit = total revenue - total cost.

Total Revenue

Total revenue = price x quantity; price of a product multiplied by the quantity sold in a given time period.

Total Cost

Total cost = market value of all resources used to produce a good or service.

Fixed Costs

Costs of production that do NOT change with the rate of output.

Variable Costs

Costs of production that change when the rate of output is altered.

Average Total Cost (ATC)

Total cost divided by the quantity produced in a given time period.

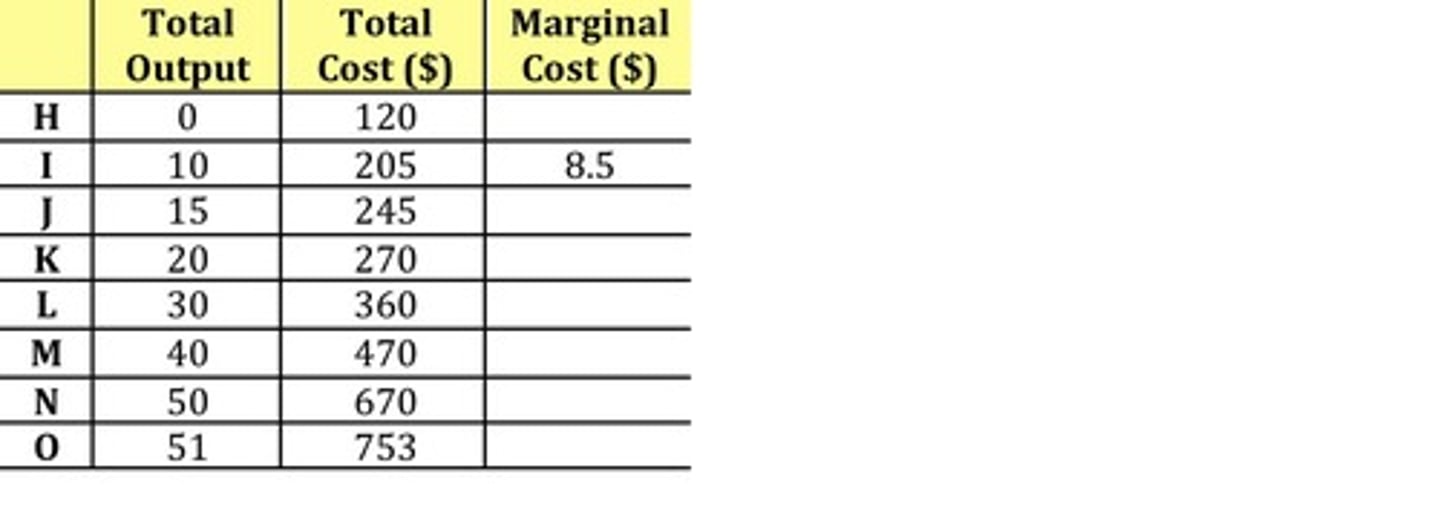

Marginal Cost (MC)

The change in total cost when one more unit of output is produced.

Economic Profit

In economic terms, profit is the difference between total revenue and total economic costs.

Total Cost Formula

Total Cost = Fixed Cost + Variable Cost.

Average Total Cost Formula

Average Total Cost = Total Cost / Total Output.

Marginal Cost Formula

Marginal Cost (MC) = change in total cost / change in total output.

Example of Total Profit Calculation

Total profit = $100 - $30 = $70.

Impact of Fixed Costs

Fixed costs cannot be avoided in the short-run.

Impact of Variable Costs

Any short-run change in total costs is a result of change in variable costs.

Production Inefficiency

Producing any less than the maximum output means production is inefficient.

Decline of MPP

As more labor is hired, each unit of labor has less capital and land to work with, causing MPP to decline.