Financial Markets - (4) Bonds

1/20

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced |

|---|

No study sessions yet.

21 Terms

What are Bonds? Types 1

ობლიგაცია არის დოკუმენტი, ანუ ხელშეკრულება, სადაც:

🔹 ერთ მხარეს არის კომპანია ან მთავრობა → გამომშვები (issuer)

🔹 მეორე მხარეს ხარ შენ ან ინვესტორი → მესაკუთრე (bondholder)

👉 კომპანია გპირდება:

რომ დაგიბრუნებს სესხის თანხას (principal) განსაზღვრულ დღეს

და ამავე დროს გიხდის პერიოდულ პროცენტს (coupon)

ესე იგი ობლიგაცია ≈ სესხი, რომელსაც შენ აძლევ კომპანიას ან სახელმწიფოს 💰

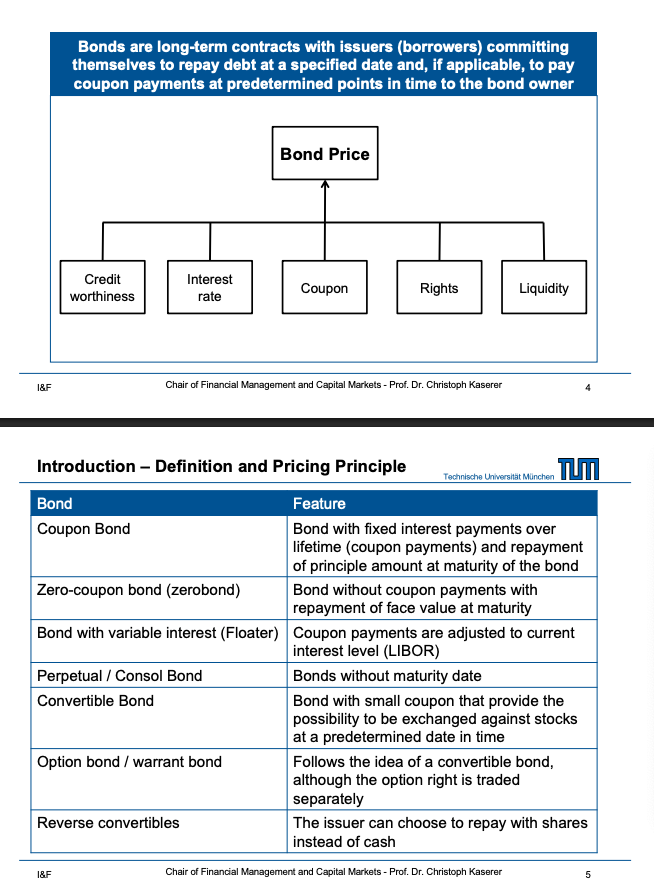

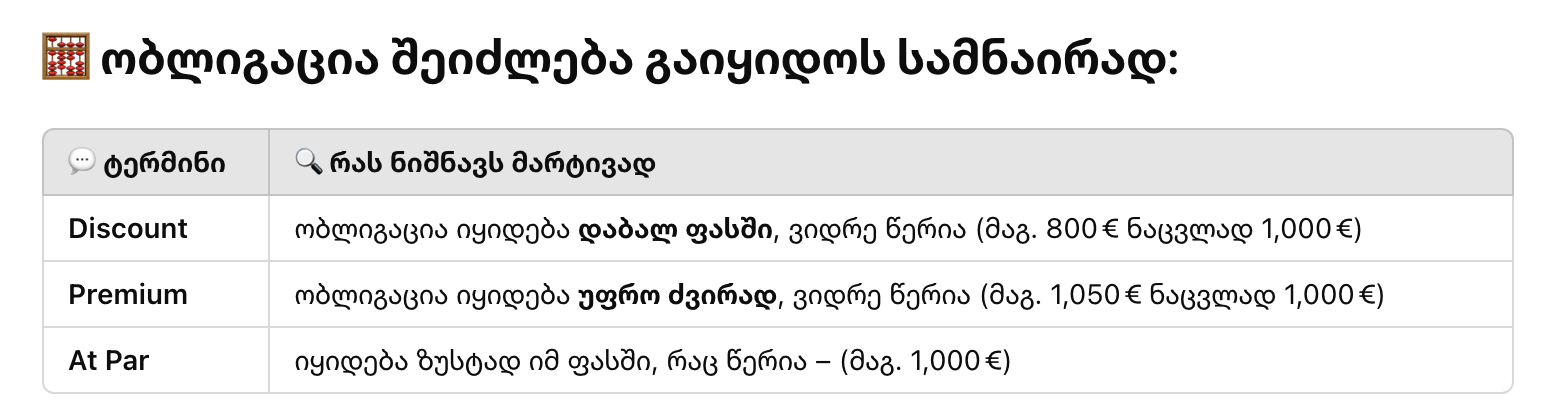

Bond Price დამოკიდებულია შემდეგზე:

ფაქტორი | რას ნიშნავს მარტივად |

|---|---|

✅ Credit worthiness | ვისგან არის? რამდენად სანდოა? (ნდობის დონე) |

✅ Interest rate | ბაზარზე არსებული პროცენტის დონე |

✅ Coupon | წელიწადში რამდენს იხდის ეს ობლიგაცია? (მაგ. 5%) |

✅ Rights | იძლევა რაიმე უფლებებს? (მაგ. შესყიდვა აქციებად) |

✅ Liquidity | რამდენად მარტივად შეგიძლია გაყიდო (მოთხოვნა) |

What is a Bond and its types 2

Zero-Coupon Bonds: These bonds don't make coupon payments. Investors buy them at a discount and receive the face value at maturity, compensating for the time value of money. 👉 არცერთ წელს არაფერი იღებ — ფული მოდის მხოლოდ ბოლოს.

Coupon Bonds: These bonds pay fixed interest (coupon payments) over their lifetime and return the principal amount at maturity. 👉 ყოველ წელს იღებ ფულს პროცენტის სახით და ბოლოს თანხას

Floater Bonds: The interest payments on these bonds are regularly adjusted to current interest rates, like LIBOR.

Perpetual Bonds: These bonds have no maturity date, meaning the coupon payments continue indefinitely.

Convertible Bonds: These bonds offer a low coupon rate and can be exchanged for stocks at a predetermined date.

Option/Warrant Bonds: Similar to convertible bonds, but the option to convert is traded separately.

Reverse Convertibles: In these bonds, the issuer can repay with shares instead of cash at maturity.

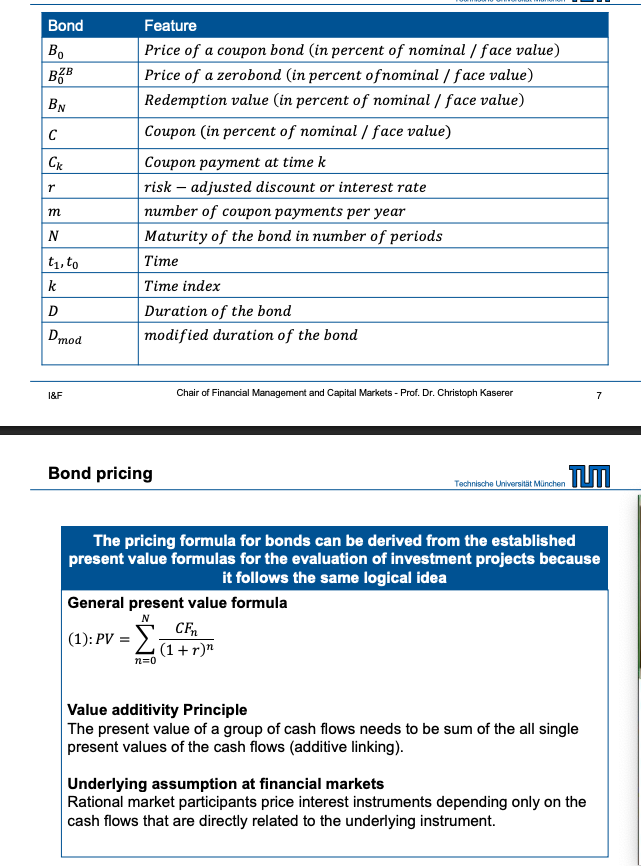

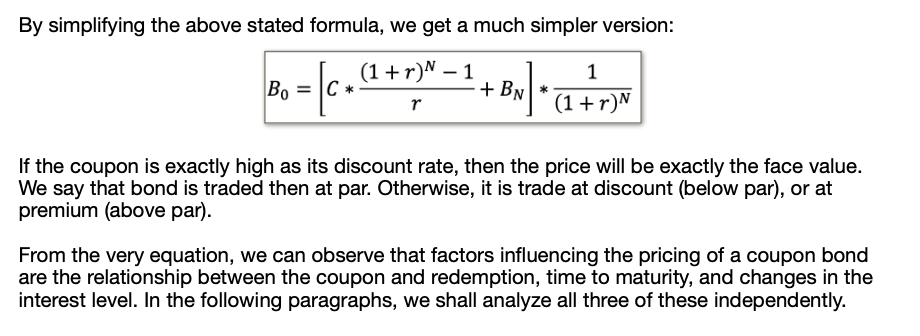

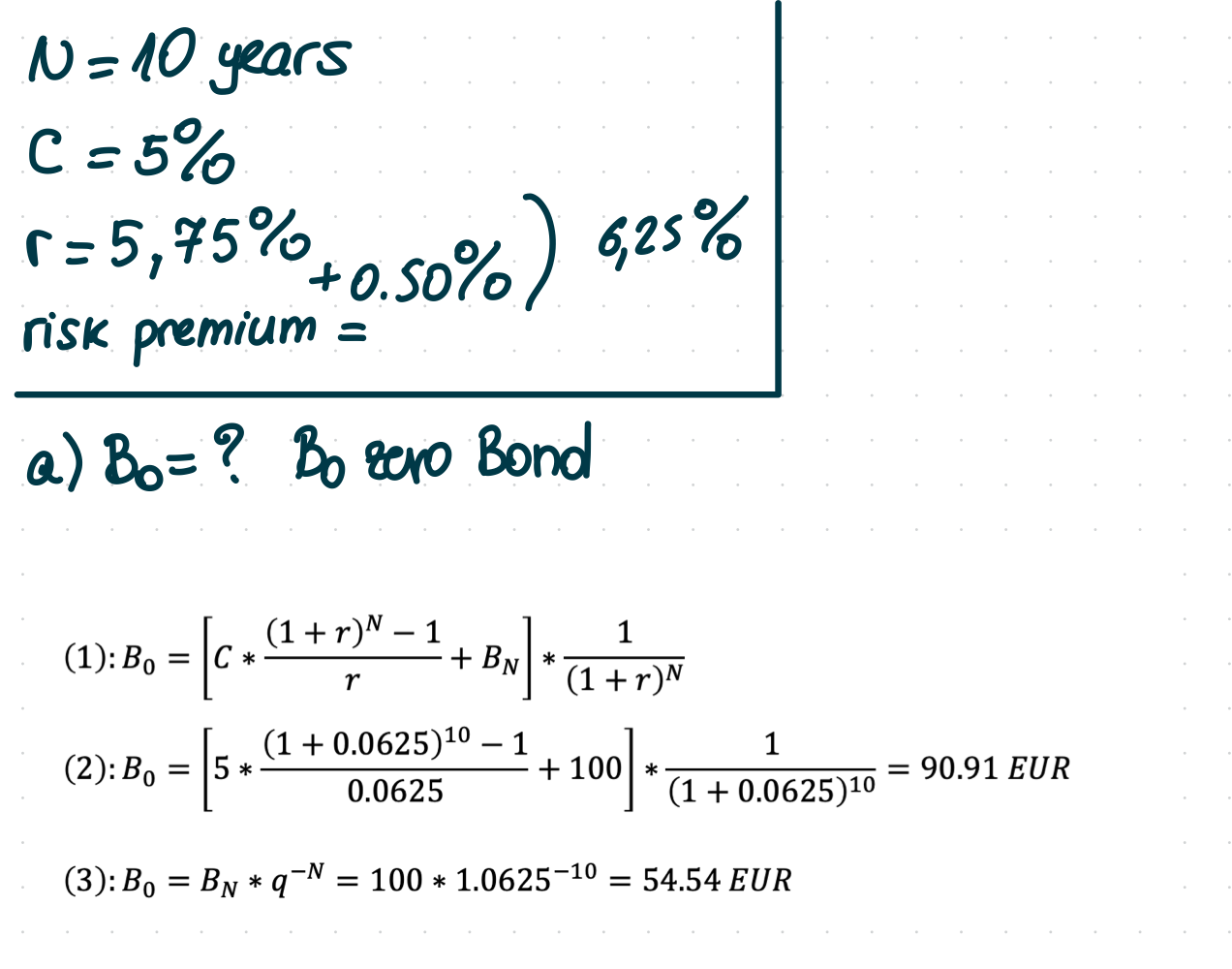

Terms and Bond pricing formula

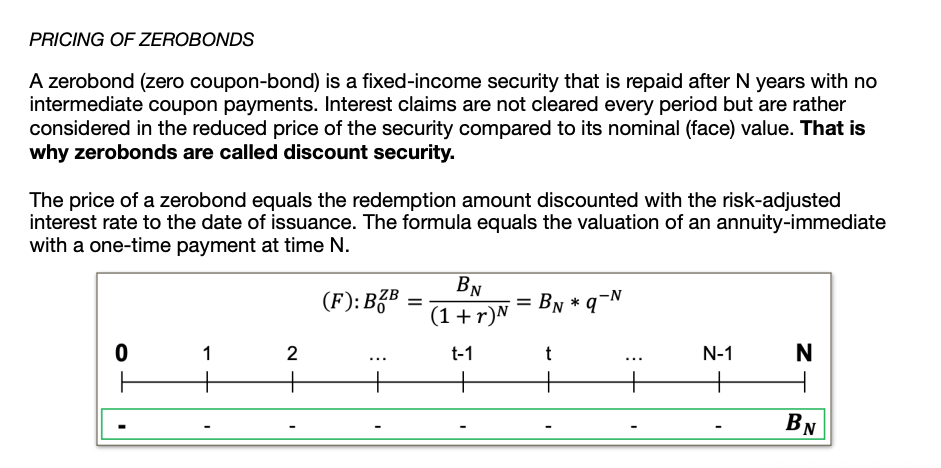

Zero-coupon bonds sell for less than their face value before the maturity date. This means they are traded at a discount.

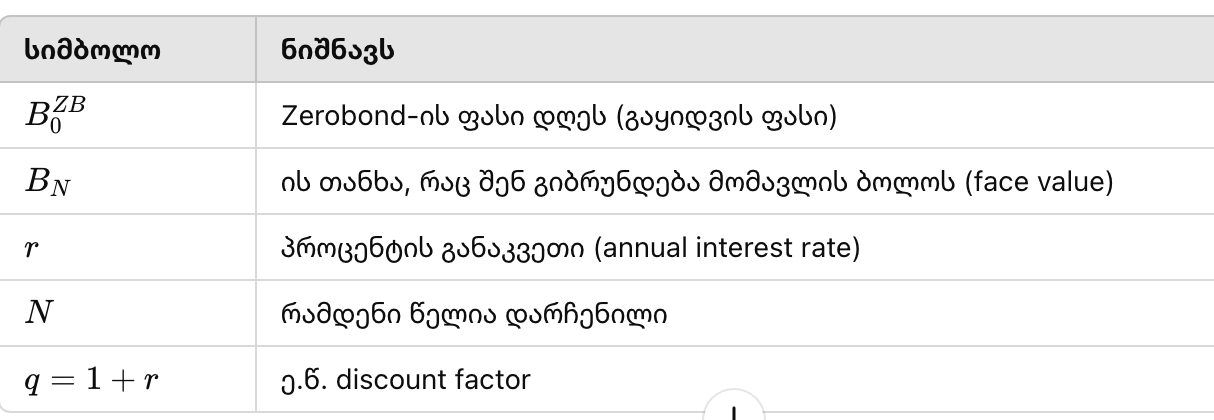

Pricing of Zerobonds

Zerobond (ანუ Zero-Coupon Bond) არის ისეთი ობლიგაცია, რომელიც:

❌ არ იხდის ყოველწლიურ პროცენტს (coupon-ს)

✅ მხოლოდ ბოლოს, ბოლო წელს გიბრუნებს მთლიან თანხას (face value-ს)

📍 მაგ: შენ ყიდულობ Zerobond-ს 800 €-ად

📍 და N წელში გიბრუნებენ 1,000 €

👉 ამიტომ ეძახიან discount security – ფასდაკლებული ფასიანი ქაღალდი, იმიტომ რომ იაფად ყიდულობ და მეტს იღებ უკან

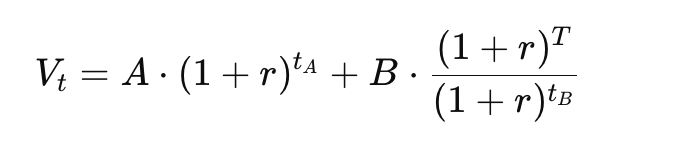

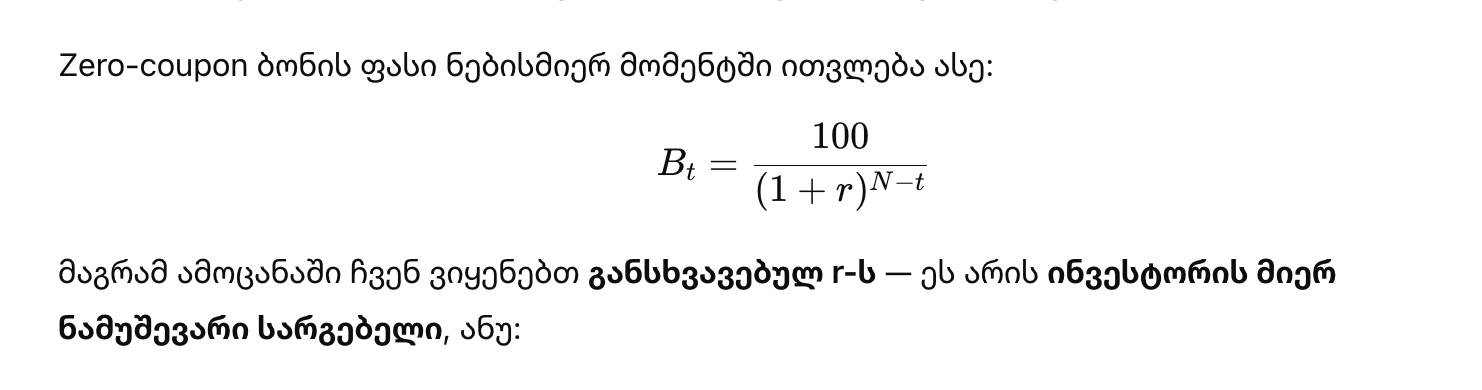

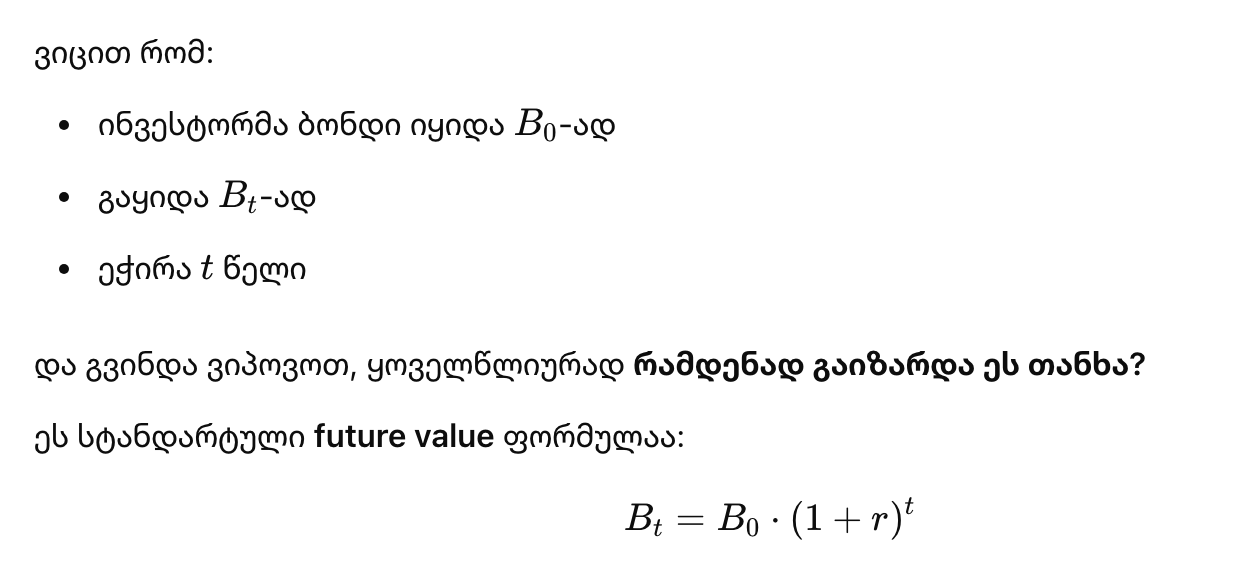

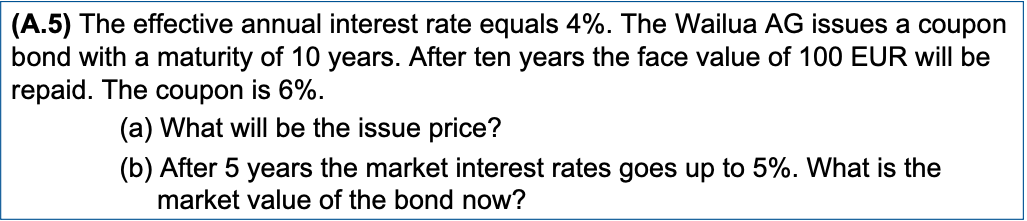

ფორმულაში ვსვამთ დარჩენილი წლებს როცა market value, ანუ დღევანდელი ფასი 10 წლის შემდეგ.

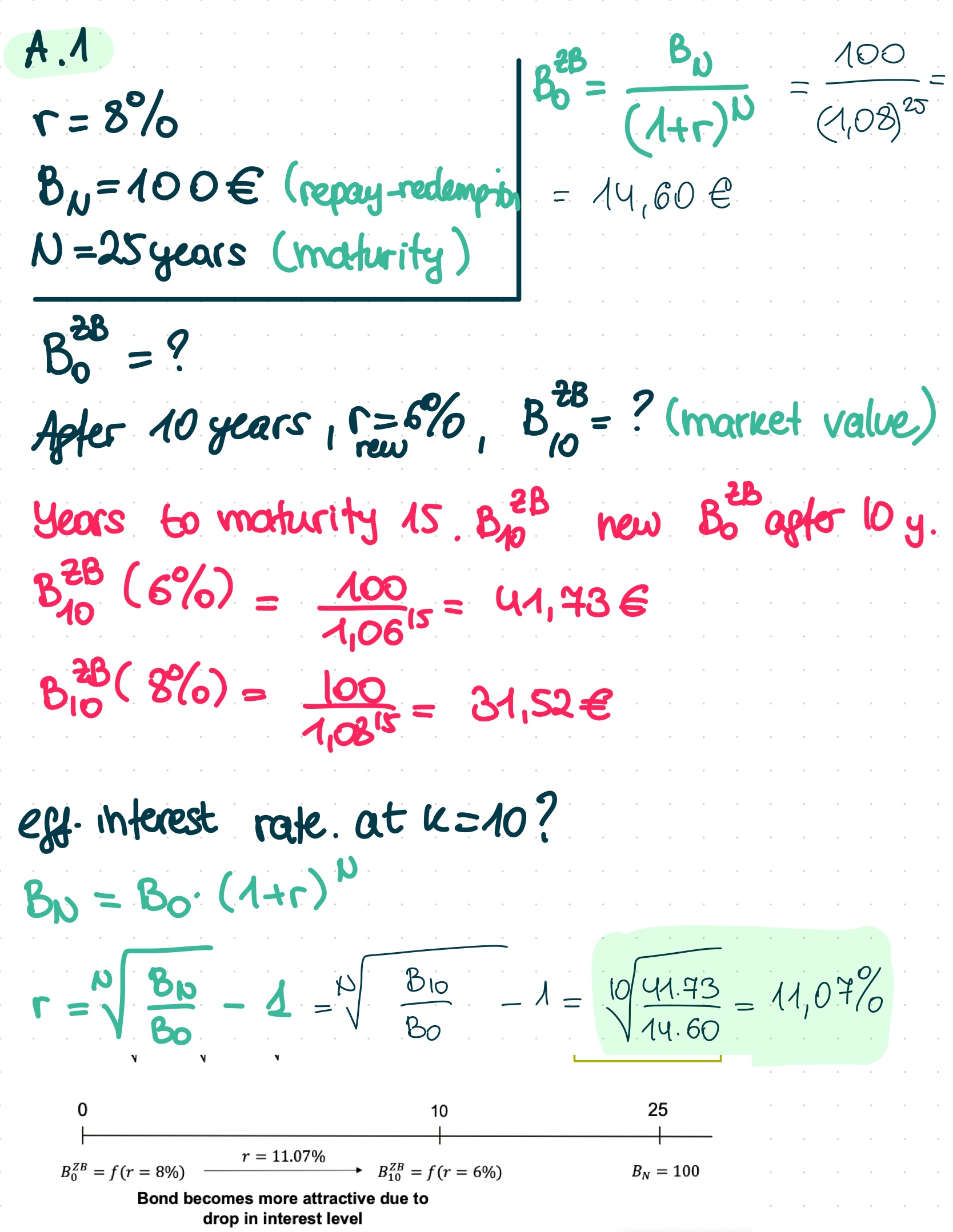

🟨 A.1c:

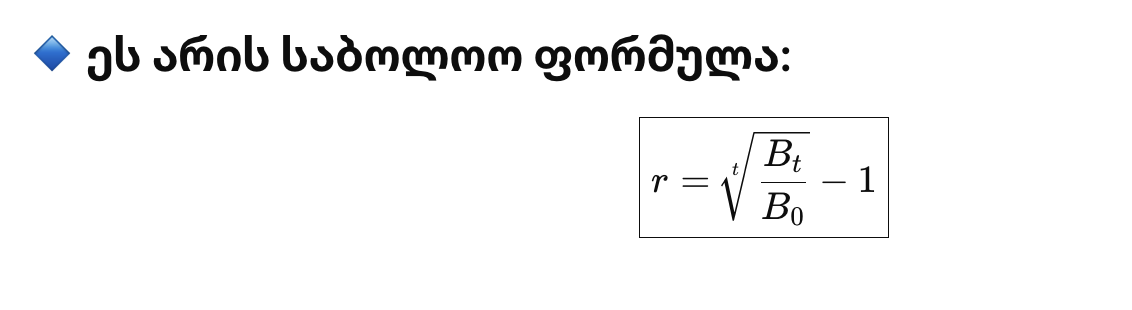

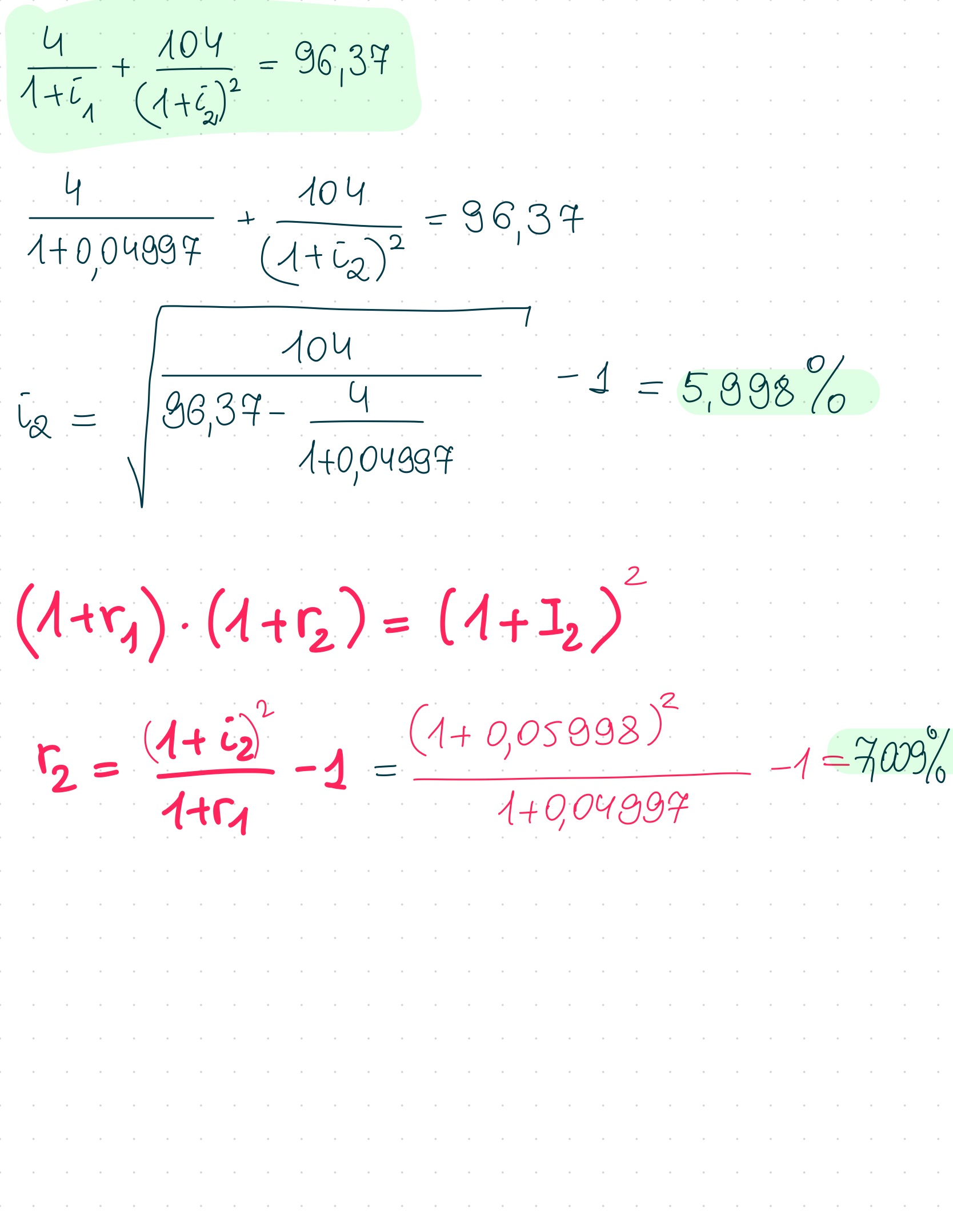

გვაინტერესებს: თუ ვიღაცამ იყიდა ბონდი 14.60 ევროდ და 10 წელიწადში გაყიდა 41.73 ევროდ, რამდენი პროცენტი მიიღო წელიწადში?

ამ ფორმულაში r არის issue discount interest rate, ბაზრის ან თეორიული საპროცენტო განაკვეთი → ფასი დაითვალო

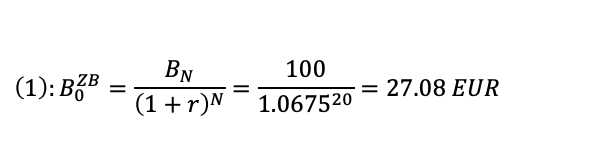

ეს არის ბონდის ფასი, როცა მასზე დარჩენილია 12 წელი (20 – 8 = 12). (ფასი 8 წლის წინ) და ახლანდელი ფასი როცა 8 წელი გასულია არის 48.31.

ეს არის r, სადაც ინვესტორის მოგების გამოთვლა შეიძლება. უკვე მოხდა ყიდვა/გაყიდვა და სარგებელი უნდა იპოვო

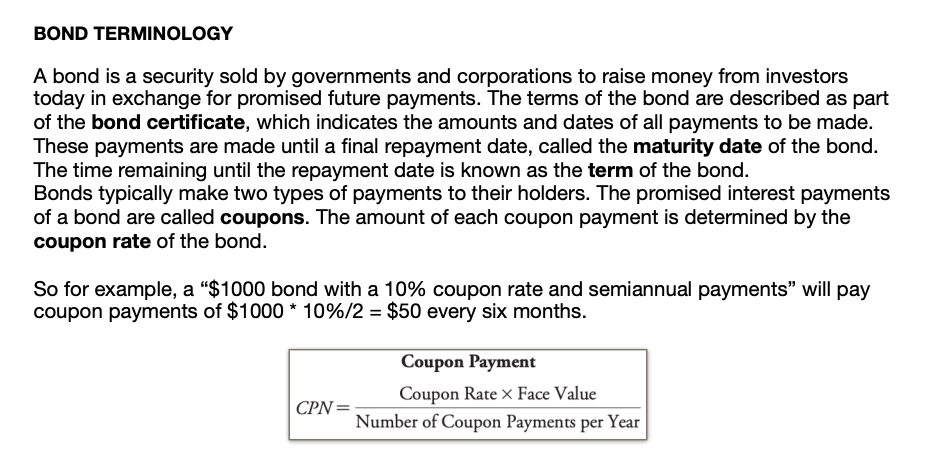

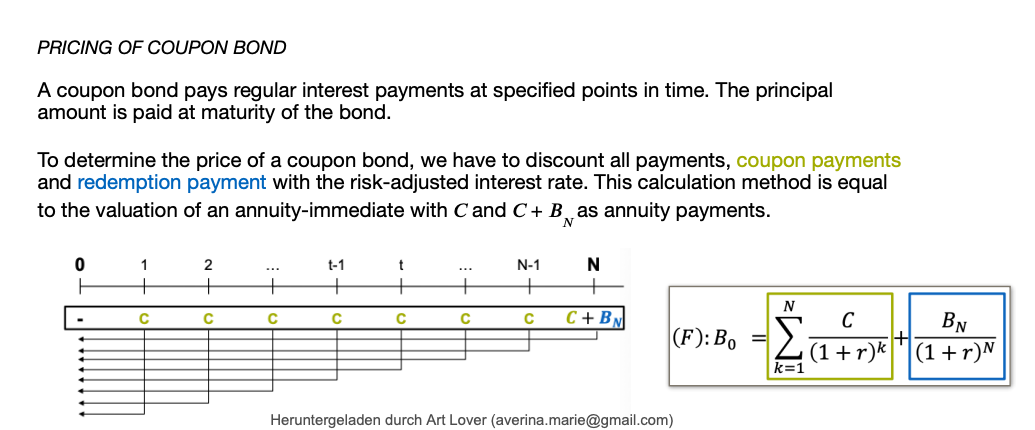

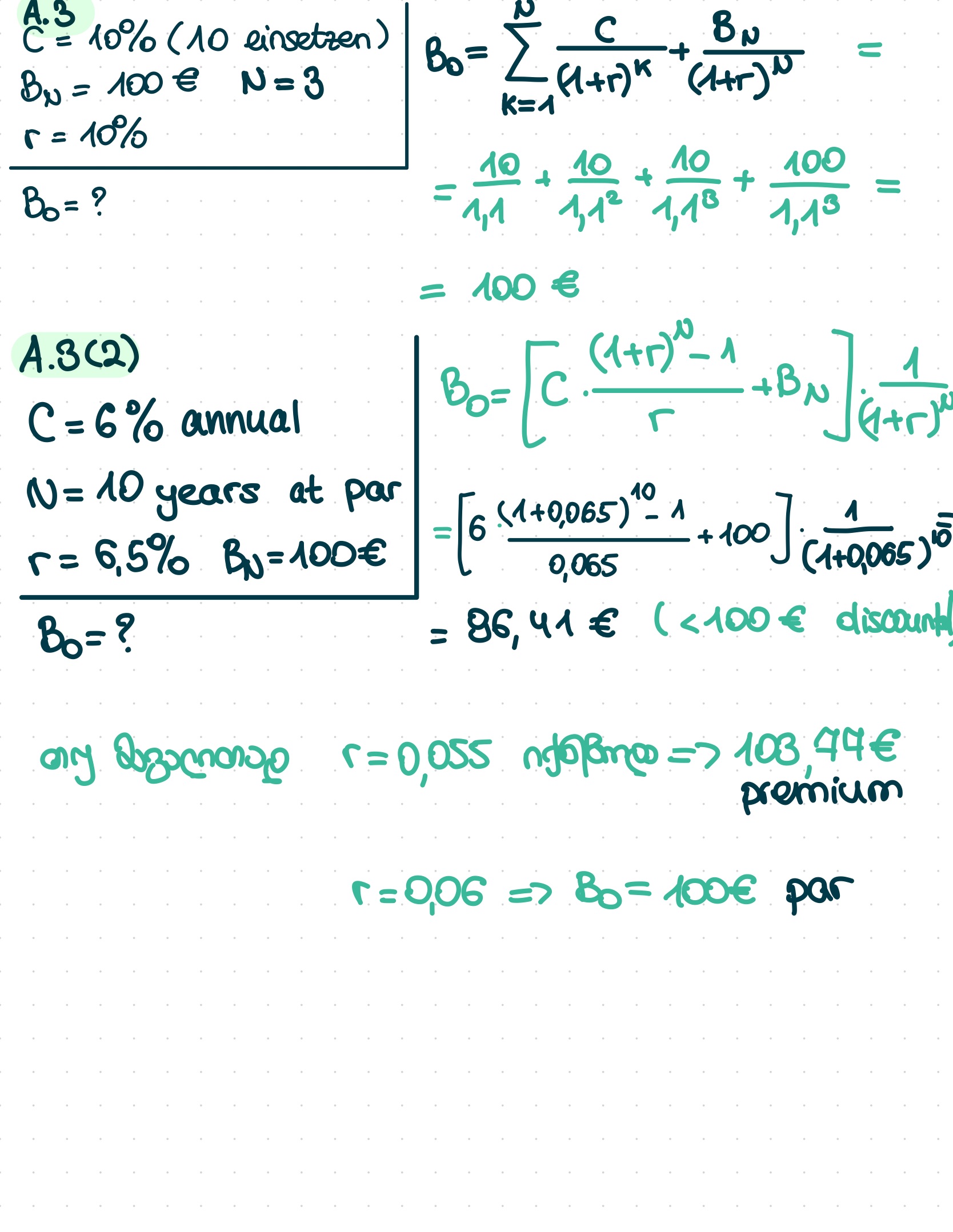

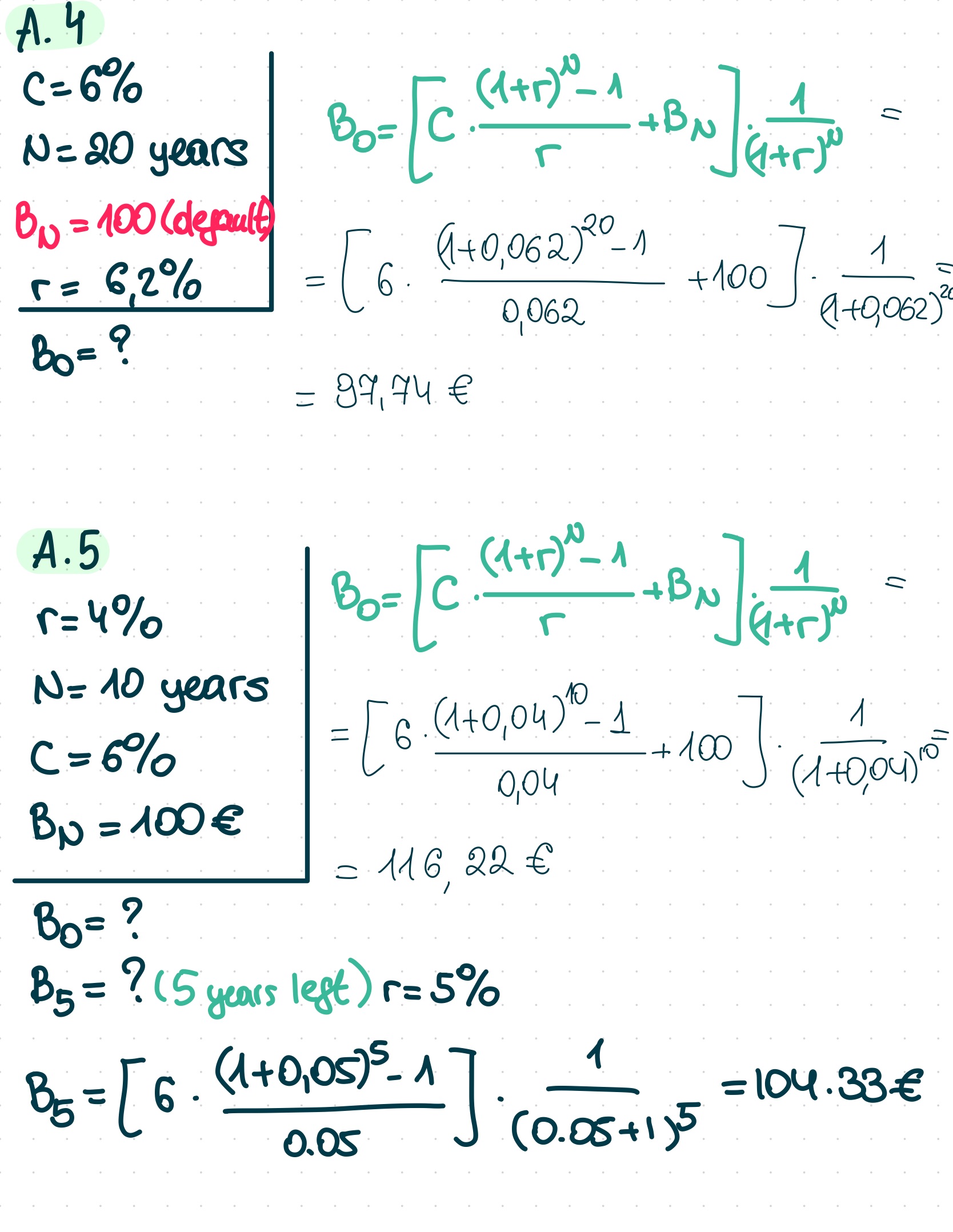

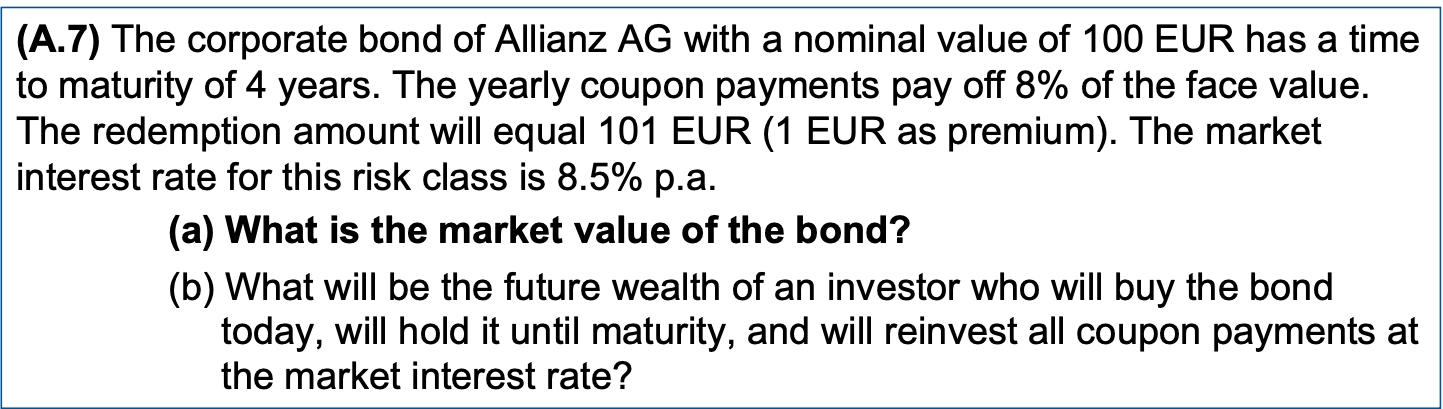

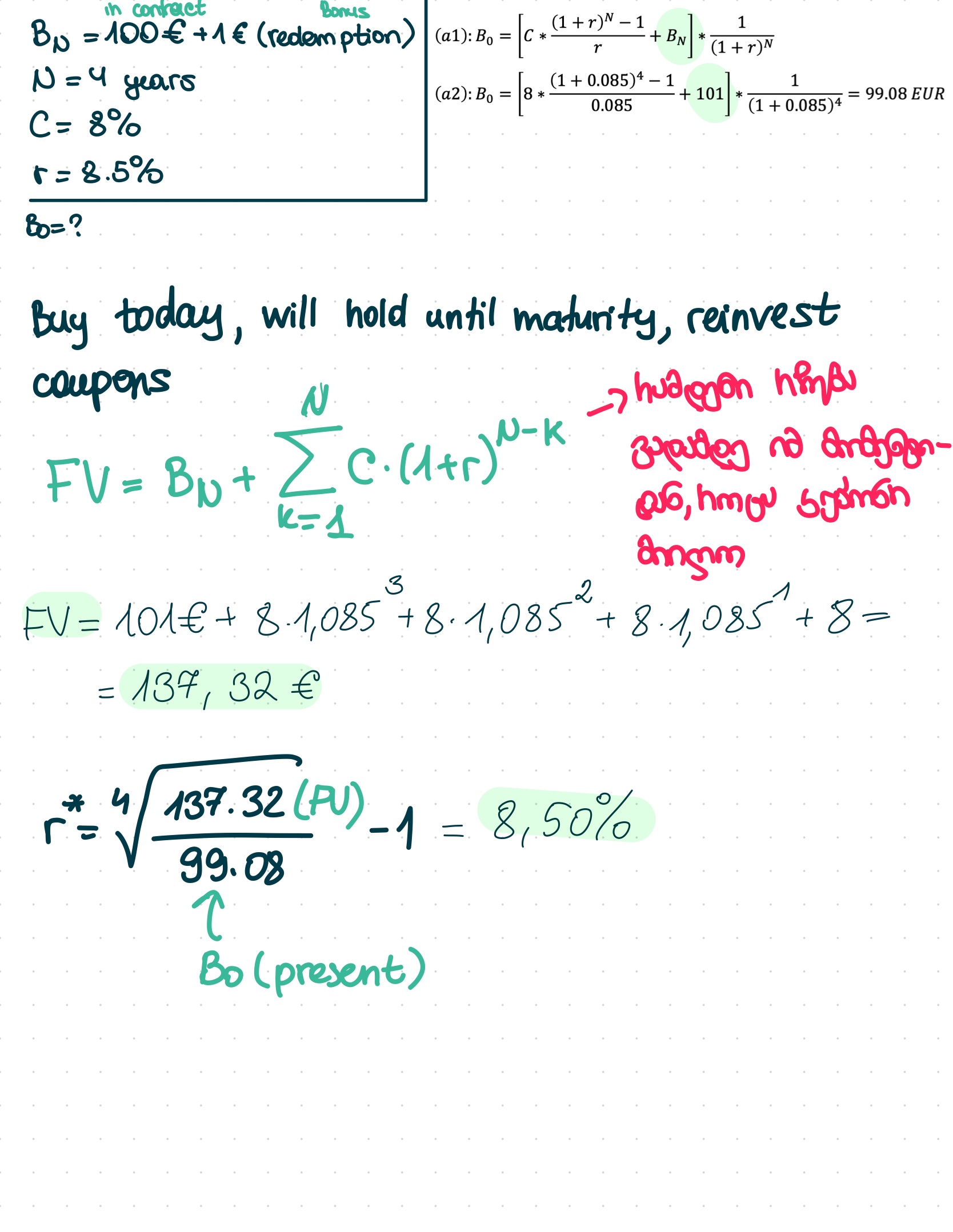

Coupon Bond (კუპონური ობლიგაცია) არის ობლიგაცია, რომელიც:

ყოველწლიურად გიხდის ფიქსირებულ თანხას (რომელსაც ვუწოდებთ კუპონს, C)

და ბოლოს გიბრუნებს მთელ თანხას (ე.წ. face value, ან BN), მაგალითად, 100 ევროს

➡ ყველა კუპონის დისკაუნტირებული ჯამი

➕

➡ ძირითადი თანხის redemption დისკაუნტირებული ღირებულება (risk adjusted)

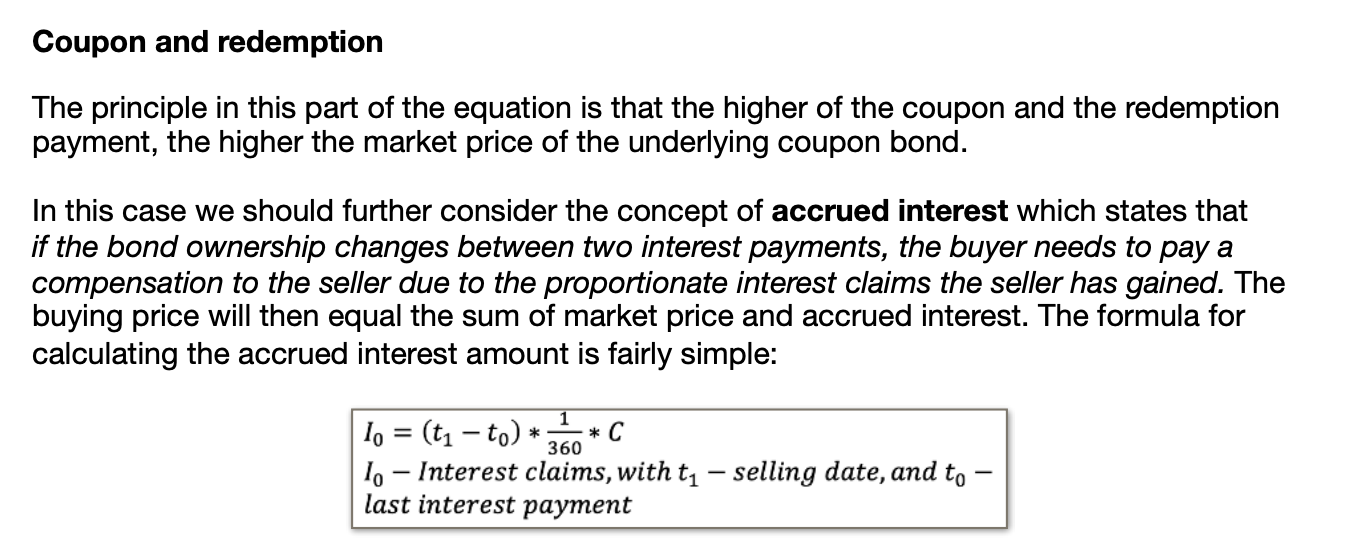

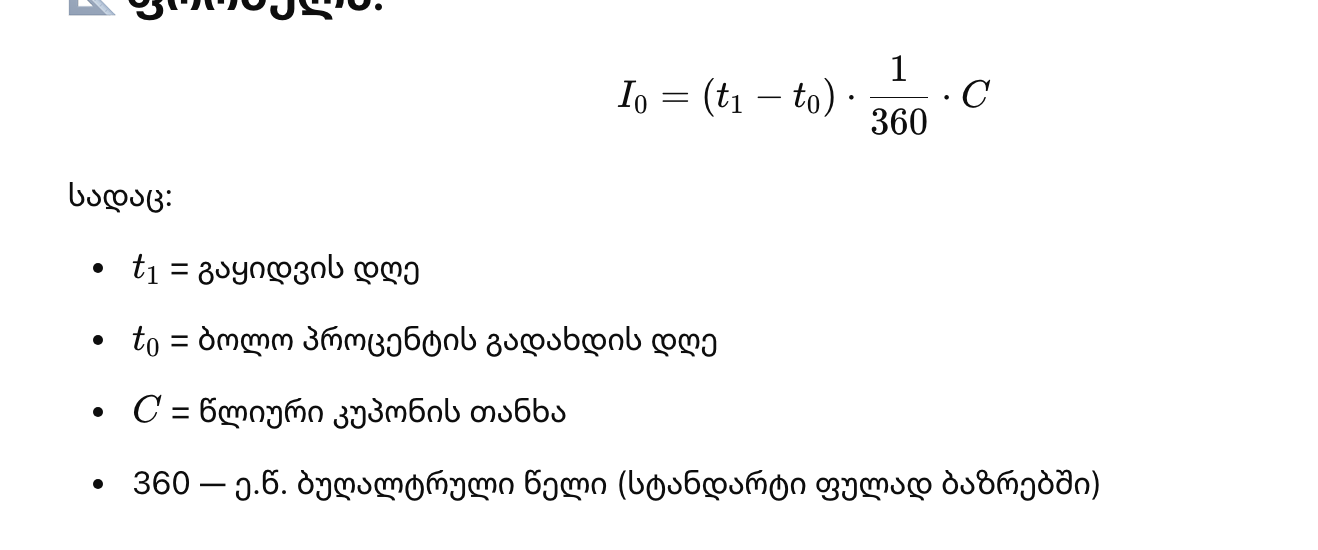

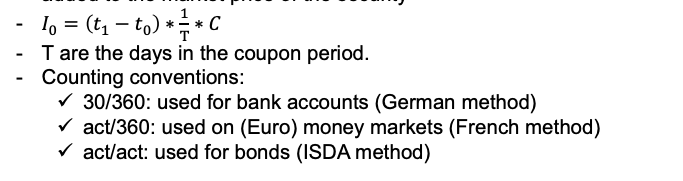

Coupon and Redemption, clean price, dirty price

რა ხდება როცა ობლიგაციას (bond-ს) ყიდი ან ყიდულობ ისეთი მომენტში, როცა პროცენტი (კუპონი) ჯერ არ მიგიღია — ანუ ე.წ. accrued interest-ზეა საუბარი.

🔹სუფთა ფასი (Clean Price)

— ეს არის ობლიგაციის საბაზრო ფასი (ex-coupon price),

რომელიც გამოჩნდება ბირჟაზე.

🔹საბოლოო ფასი (Dirty Price)

— ეს არის ის ფასი, რასაც მყიდველი რეალურად იხდის:

სუფთა ფასი + დარიცხული პროცენტი

🎯 მთავარი აზრი:

ობლიგაციის ფასი ბირჟაზე არ შეიცავს დარიცხულ პროცენტს, მაგრამ რეალურად რომ იყიდო, შენ უნდა გადაიხადო ორივე — ფასი + დარიცხული კუპონი.

Time to Maturity factor on bond price (market price)

when the interest rate is the same as the bond's coupon rate, the time until the bond matures does not affect its market price. (no effect wehn r = C)

if the interest rate is higher than the coupon rate, the time to maturity will lower the bond's market price more as time goes on. (r > C → market price lowers withttime)

if the interest rate is lower than the coupon rate, the market price of the bond will increase more as time passes. (r < C → market price increases with time)

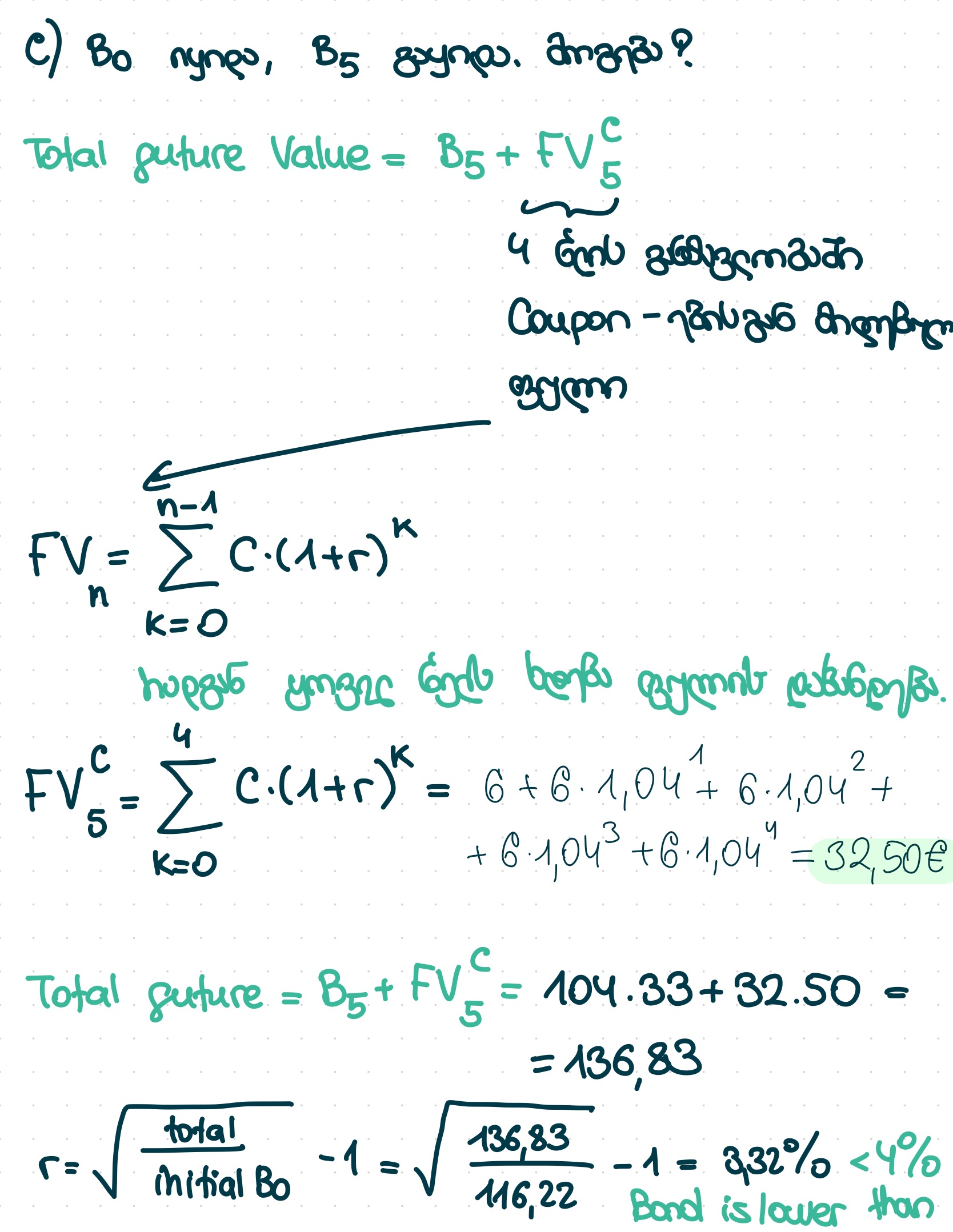

Yield to Maturity (YTM) is the return a bondholder earns if they keep the bond until it matures and if the market interest rate stays the same (this is called the re-investment hypothesis). YTM is expressed per year (p.a.).

Bond prices change when interest rates change. Bond prices are sensitive to interest rate changes.

When market interest rates drop, bond prices go up because the present value of the bond's payments increases. (r lowers → bond price up)

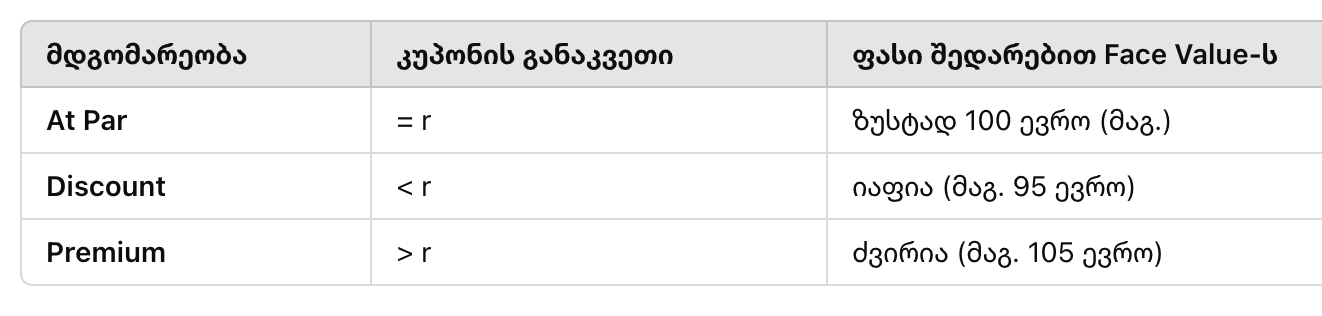

If the market interest rate falls below the coupon rate, the bond price goes above its face value (called “par”). (r < C → bond price more than face value)

If the market interest rate rises above the coupon rate, the bond price falls below par. (r > C → bond price lowers below par)

📘 Yield Curve – რას ნიშნავს?

👉 Yield curve show how interest rates change depending on the maturity period.

📘 Yield Curve-ის ტიპები

ტიპი | ახსნა |

|---|---|

Normal | რაც უფრო გრძელვადიანია ინვესტიცია, მით მაღალია პროცენტი |

Flat | ყველა ვადაზე პროცენტი ერთნაირია |

Inverse | რაც უფრო გრძელვადიანია ინვესტიცია, მით დაბალია პროცენტი (იშვიათი და რეცესიასთან კავშირშია) |

📘 Yield Curve-ის 3 ახსნა

Pure Expectation Hypothesis

→ ბაზარი ელოდება მომავლის განაკვეთებს

→ The curve reflects market expectations about future interest ratesLiquidity Preference Theory

→ გრძელვადიანი ინვესტიცია მოითხოვს პრემიუმს

→ Investors want extra return (premium) for long-term riskMarket Segmentation Theory

→ სხვადასხვა სეგმენტი მოქმედებს სხვადასხვა ვადაში

→ Different investors operate in different maturity segments

📘 Yield Curve და რეცესიები

🔻 When the yield curve becomes inverted, it often predicts an economic recession.

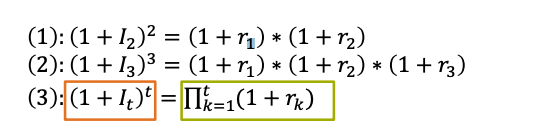

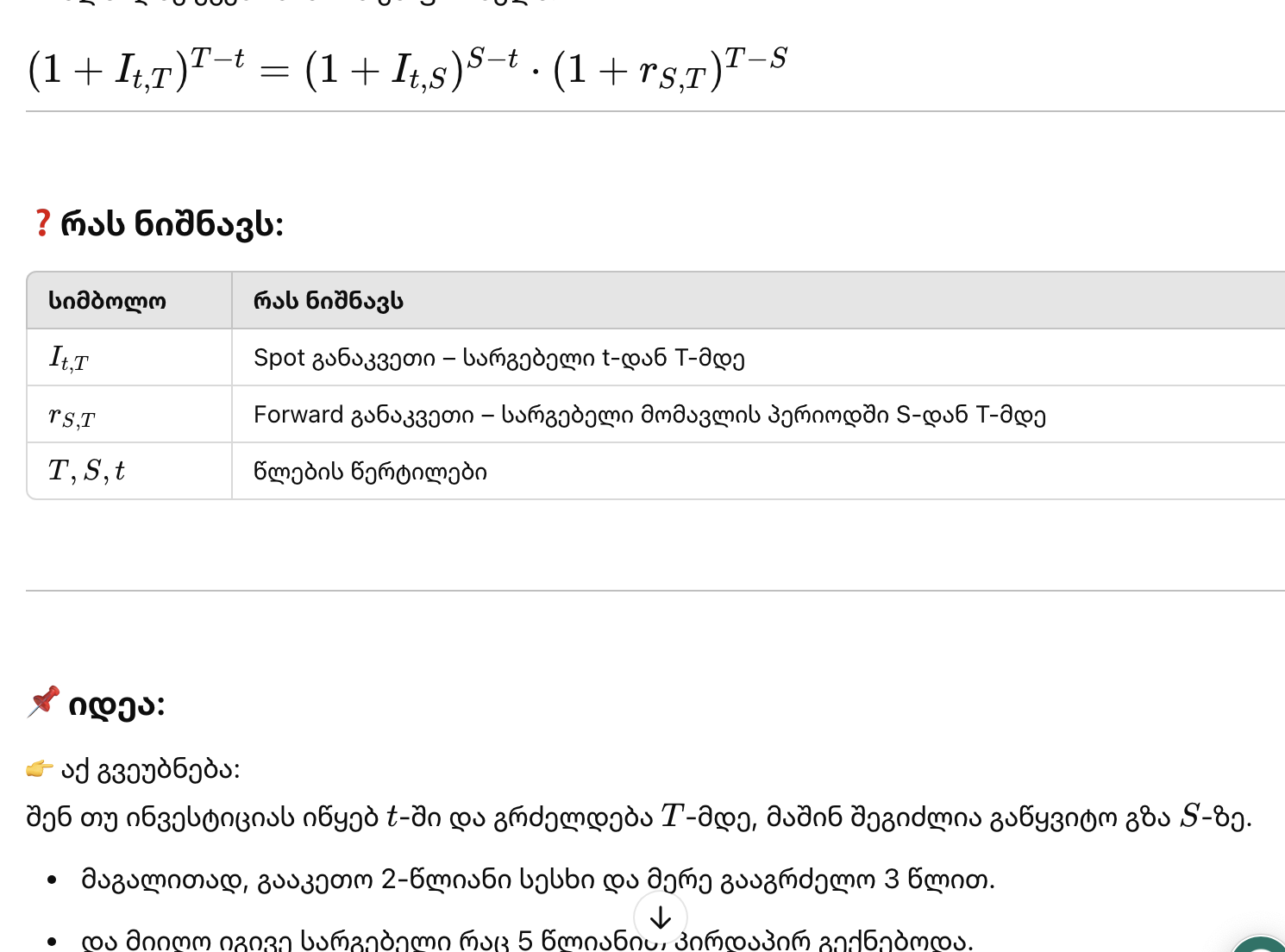

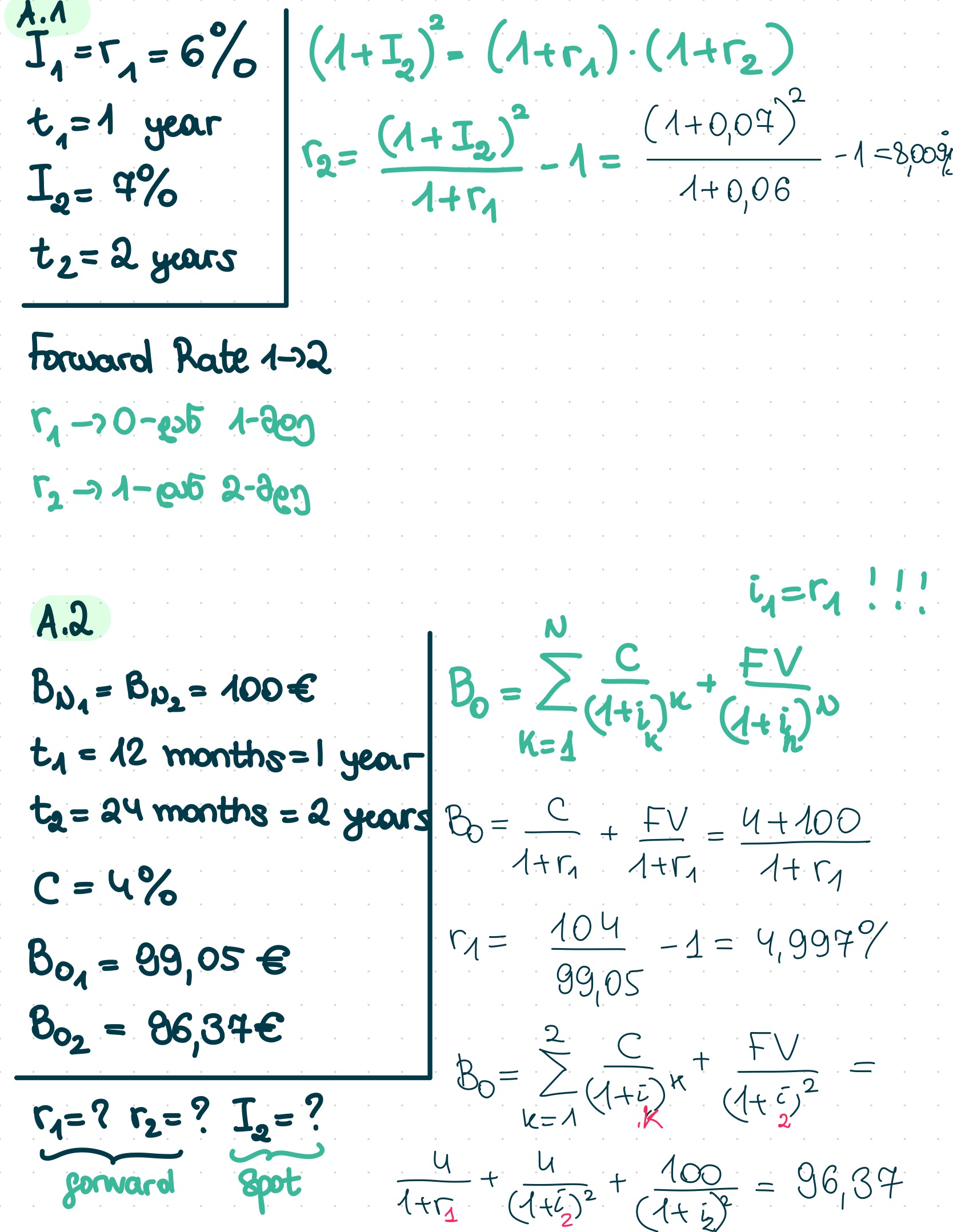

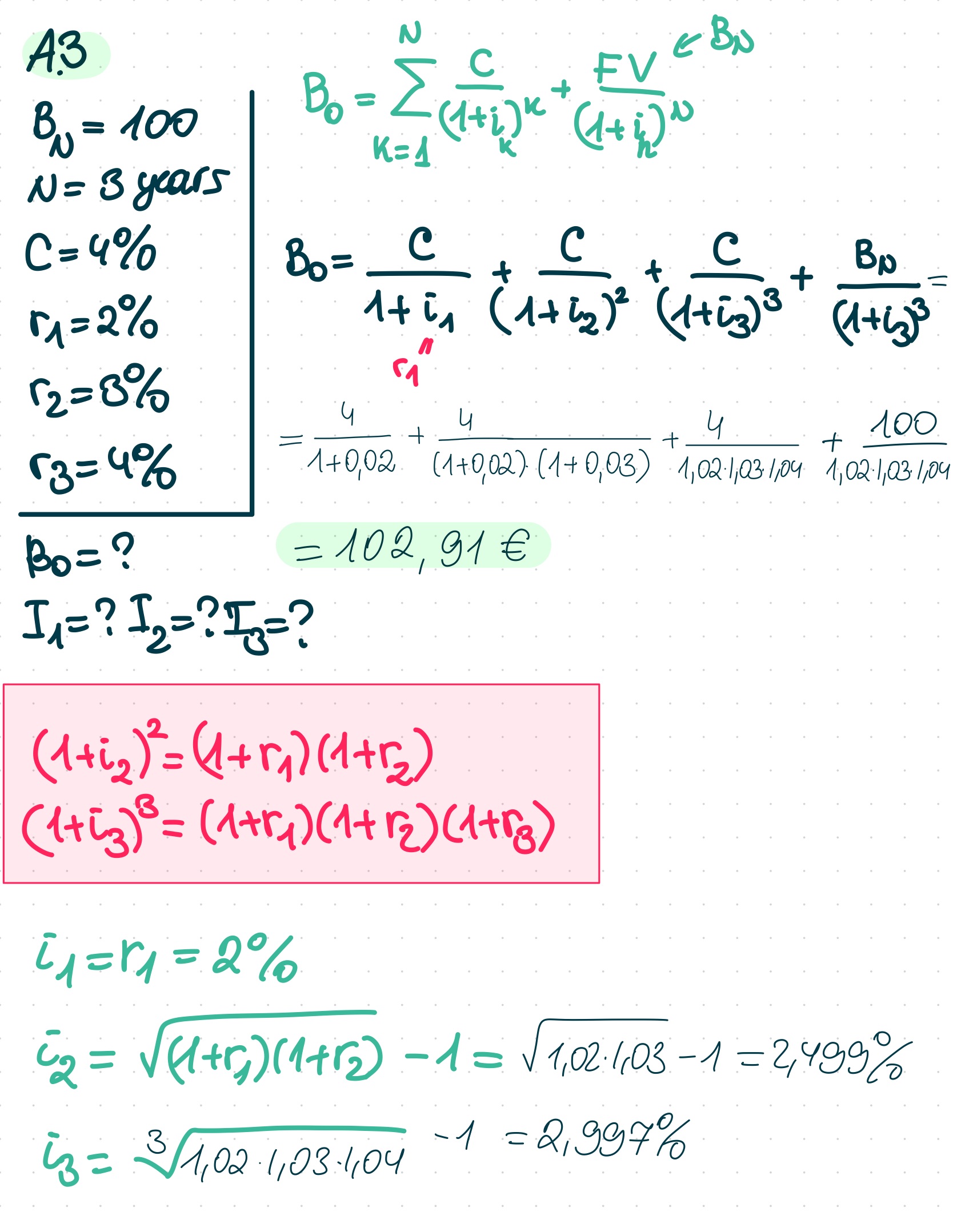

📘 Spot და Forward განაკვეთი

Spot Rate (I) → პროცენტი წერტილიდან t=0 დან t=N მდე

Interest rate from today to a future time. ჩვეულებრივი პროცენტია, რომელიც მოქმედებს თუ შენ დღეს აბანდებ ფულს და იღებ შემოსავალს მომავალში.

Forward Rate (r) → პროცენტი მომავალი პერიოდისთვის, წინასწარ განისაზღვრება. ეს არის მოსალოდნელი პროცენტი მომავალში. ანუ რას ელოდება ბაზარი რომ იქნება პროცენტი მომავალ პერიოდში.

Interest rate agreed today for a future period

📌 If no forward market exists, forward rates are calculated from spot rates.

Formulas.

Risk of Bonds. Three Categories

The risk of bonds can be divided into three risk components:

- Credit risk

- Price risk due to changes in the interest rate level

- Risk of reinvestment (of coupons)

Credit risk

არის თუ არა შანსი, რომ ბონდის გამცემი (კომპანია/სახელმწიფო) ვერ გადაგიხდის?

Credit risk refers to the chance that a bond issuer will fail to make coupon or redemption payments. It can affect:

- The interest payments when the bond is issued (risk premium)

- The interest rate used to price the bond (discount rate)

In general, higher credit risk leads to a lower market value for the bond. As credit risk rises, investors expect a higher return (risk premium) to compensate for the default risk, making them less willing to pay for the bond, which decreases its market price. Bond yields can fluctuate based on changes in market interest rates and the issuer's credit risk.

Price risk due to changes in the market interest rate

If the market interest rate changes, it affects the bond price.

When the market interest rate rises, the bond price goes down. The longer the bond’s maturity date, the bigger the impact of the interest rate change.

როცა ბაზრის პროცენტები იცვლება, ბონდის ფასი იცვლება.

თუ ბაზრის პროცენტი აიწევს, ბონდების ფასი ეცემა

თუ ბაზრის პროცენტი იკლებს, ბონდების ფასი ზრდება

📌 და რაც უფრო გრძელვადიანია ბონდი,

მით უფრო ძლიერ რეაგირებს ამ ცვლილებაზე.

Reinvestment risk

future cash flows may have to be reinvested at lower market interest rates, which is not good for the investor. For example, if you invest in bonds with a yield to maturity (YTM) of 5%, and when you cash out, you find the best yield available is now only 2%, you’ll earn less money. In this case, you might wish you had kept that first bond. Generally, long-term bonds carry more price risk but have less reinvestment risk. In contrast, short-term bonds have less price risk but higher reinvestment risk because their face value must be reinvested at lower rates until the long-term bond matures.

თუ ბონდი გიხდის კუპონებს ყოველ წელს, სად გადაინვესტებ ამ ფულს მომავალში?

მაგალითად:

დღეს იღებ კუპონს და აბანდებ 5%-იან ბონდში

მომავალში ბაზარზე ყველაზე კარგი ბონდი მხოლოდ 2%-იანია 😞

👉 ანუ შენი ფული ახლა ნაკლებად მოგაბრუნებს

📌 ამიტომ:

გრძელვადიან ბონდს აქვს დაბალი რეინვესტირების რისკი, მაგრამ მაღალი ფასის რისკი

მოკლევადიან ბონდს აქვს მაღალი რეინვესტირების რისკი, მაგრამ დაბალი ფასის რისკი

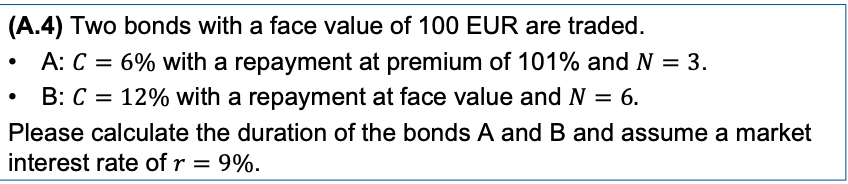

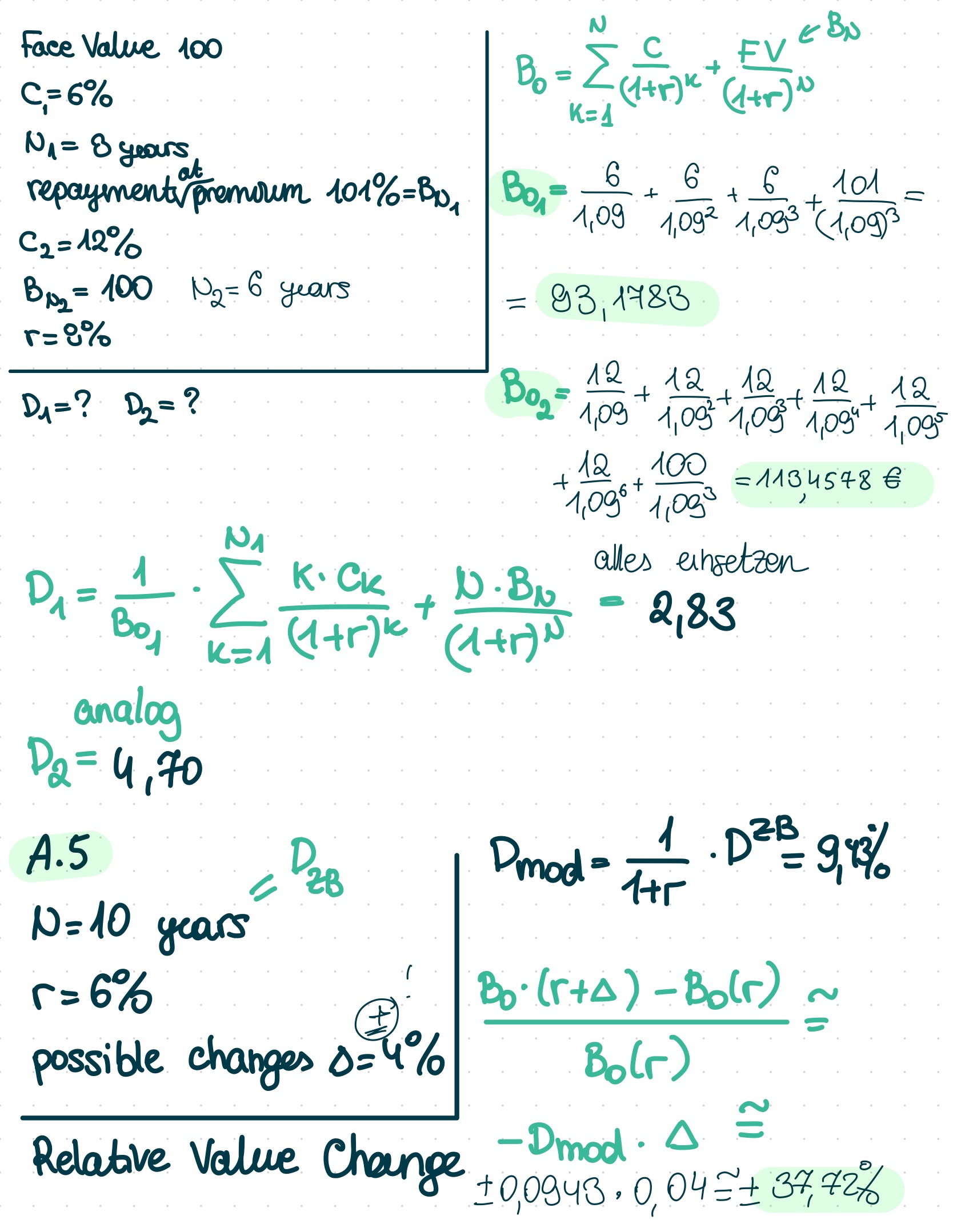

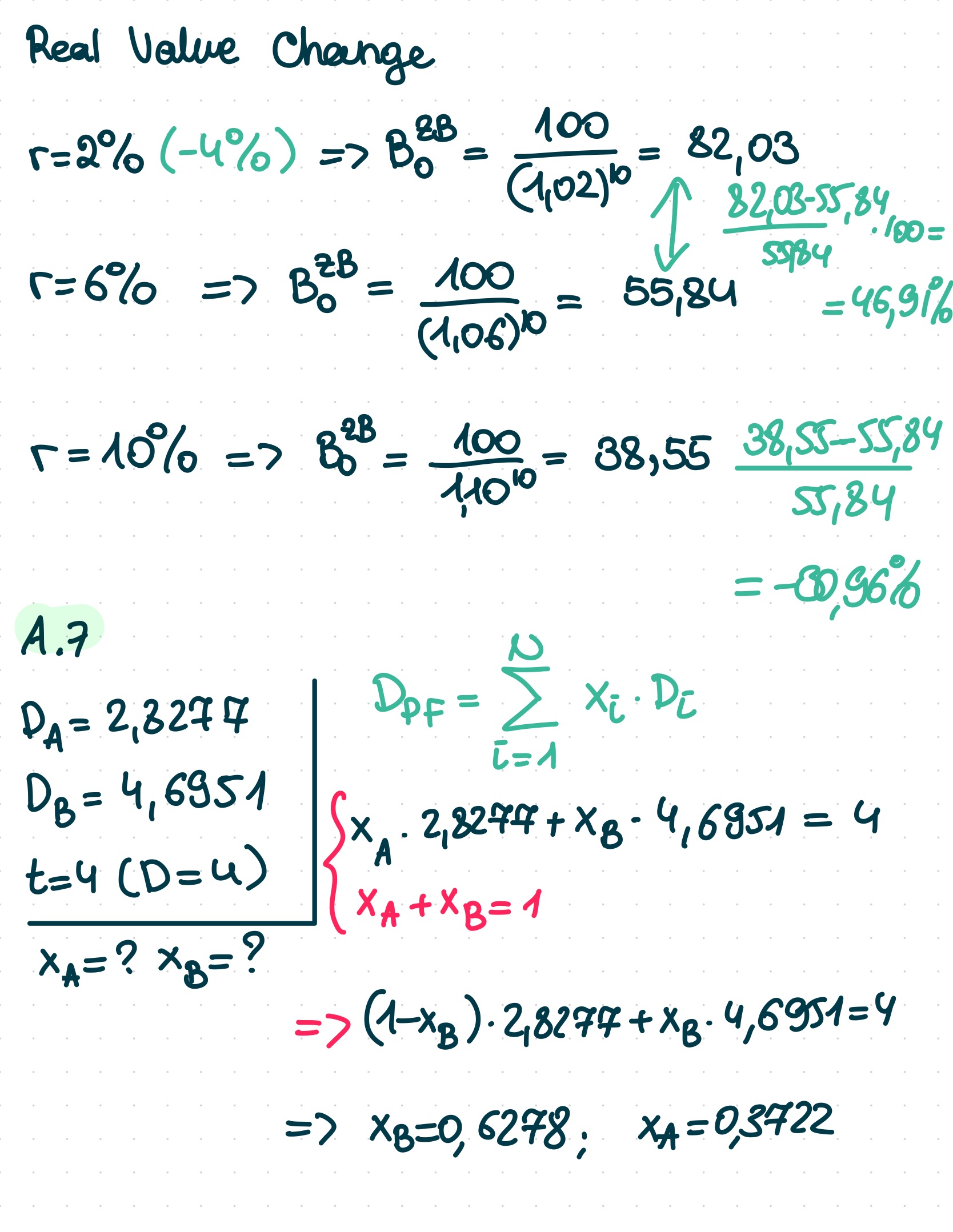

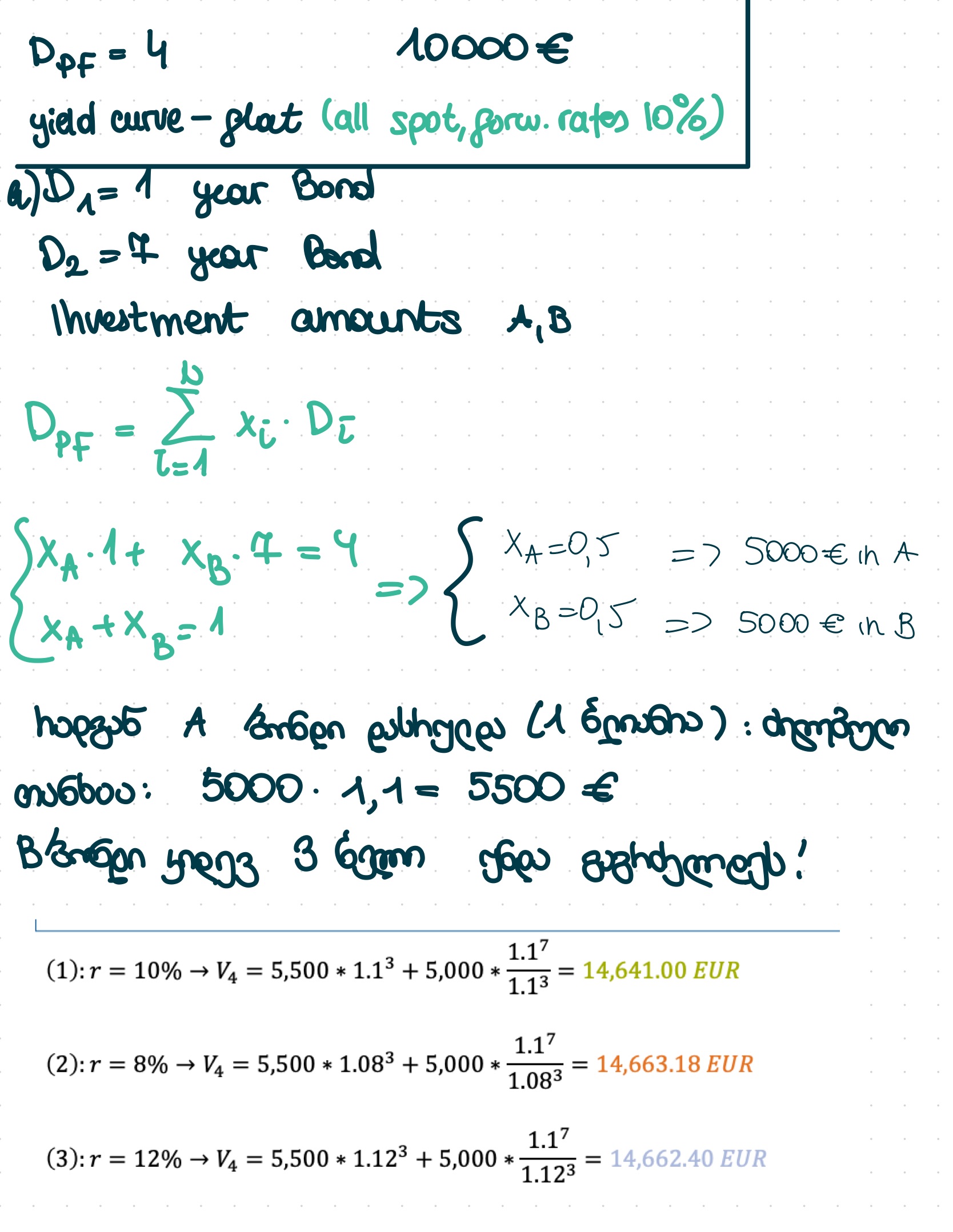

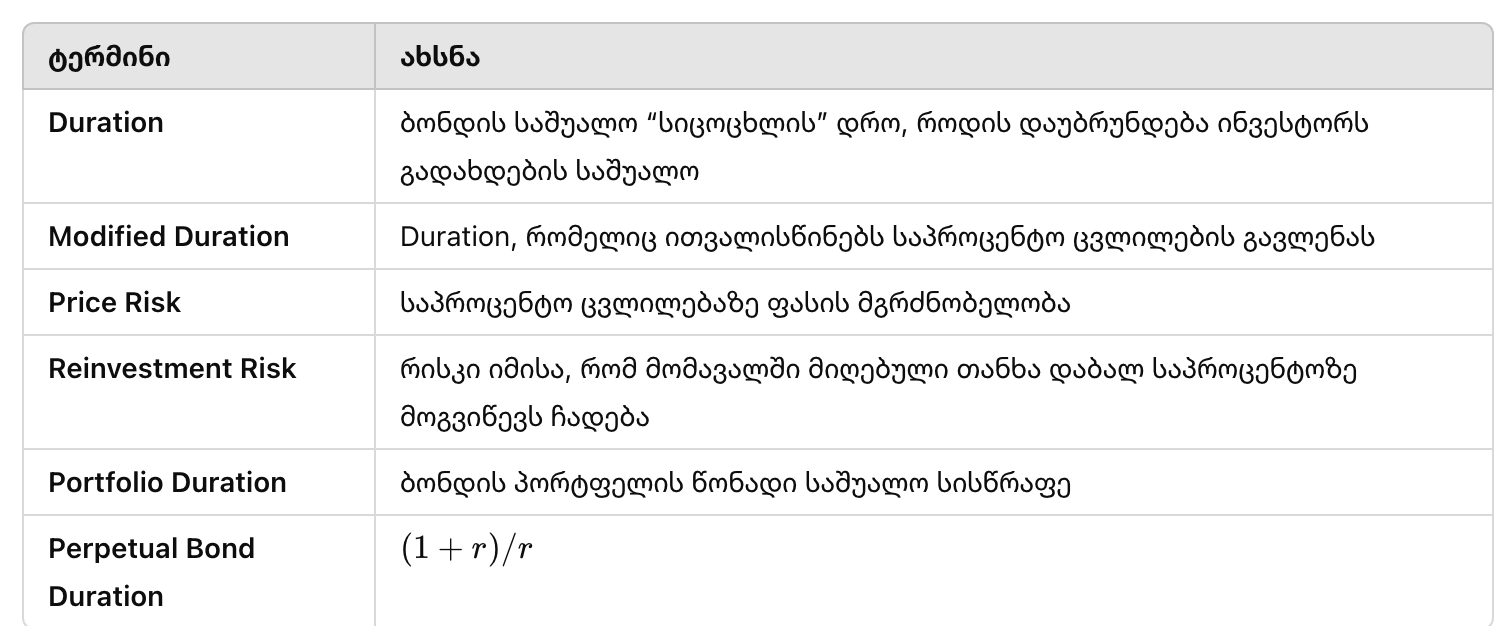

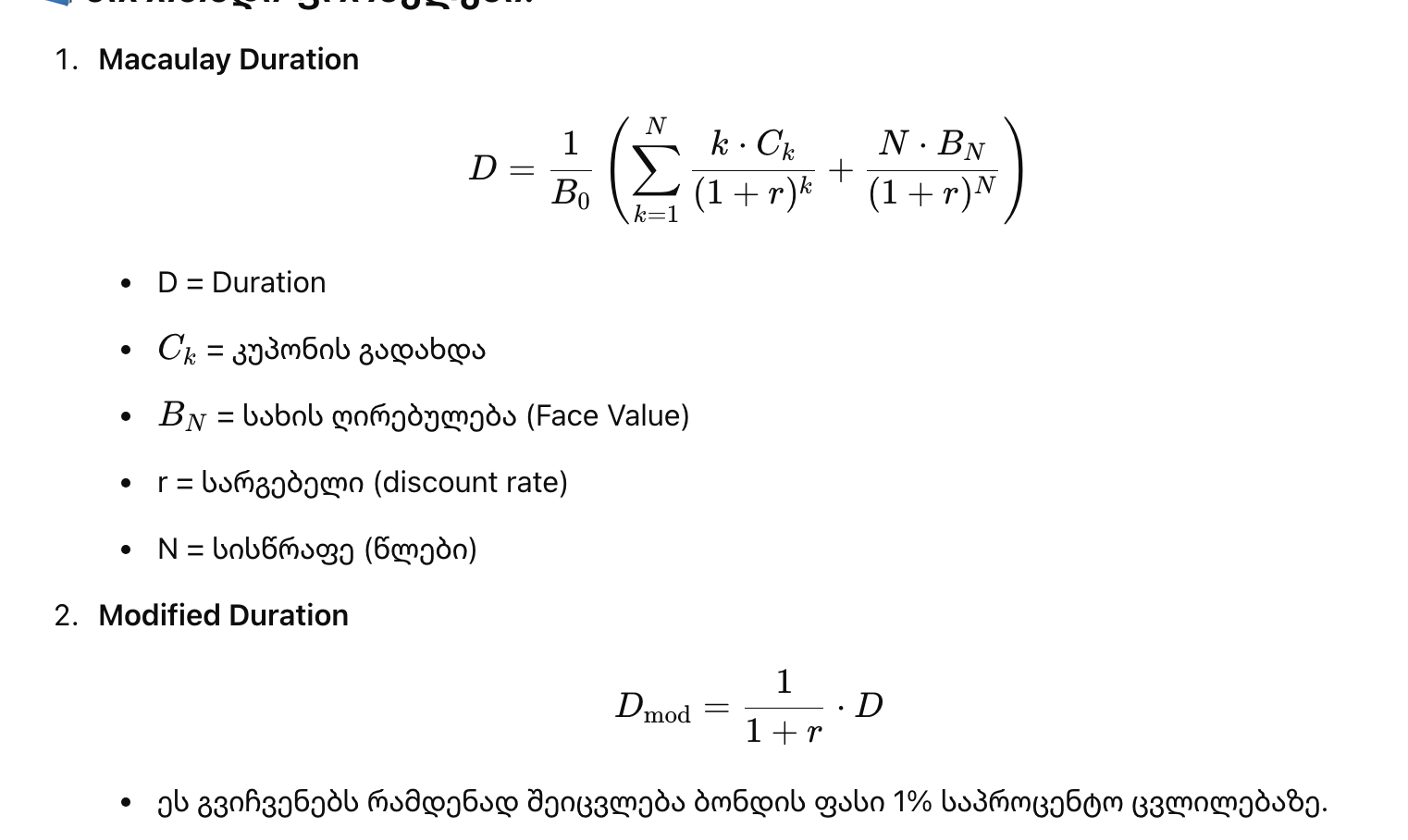

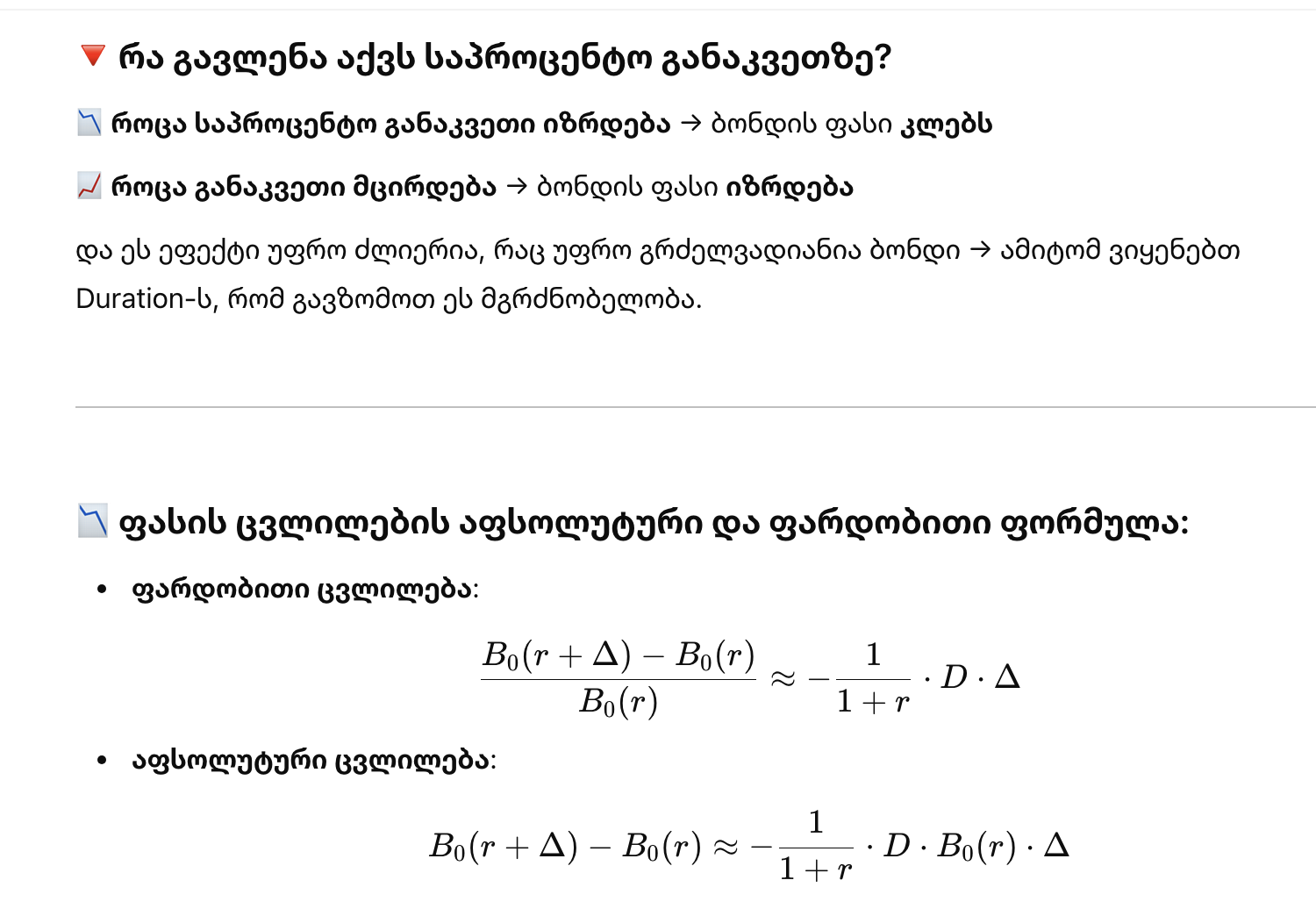

Concept of Duration

Interest rate risk arises from changes in market interest rates, affecting bond prices and reinvestment conditions. When interest rates rise, bond prices fall, but reinvestments become more attractive. Investors can mitigate this risk by holding a bond until a specific point where the effects of interest rate changes offset each other. At this point, they are not exposed to interest rate risk, as cash flows are not influenced by market rates. The sensitivity of a bond to interest rate changes can be measured using duration: the higher the duration, the greater the sensitivity. Understanding the mathematical relationship between bond value and interest rate changes helps in estimating duration.

Formulas

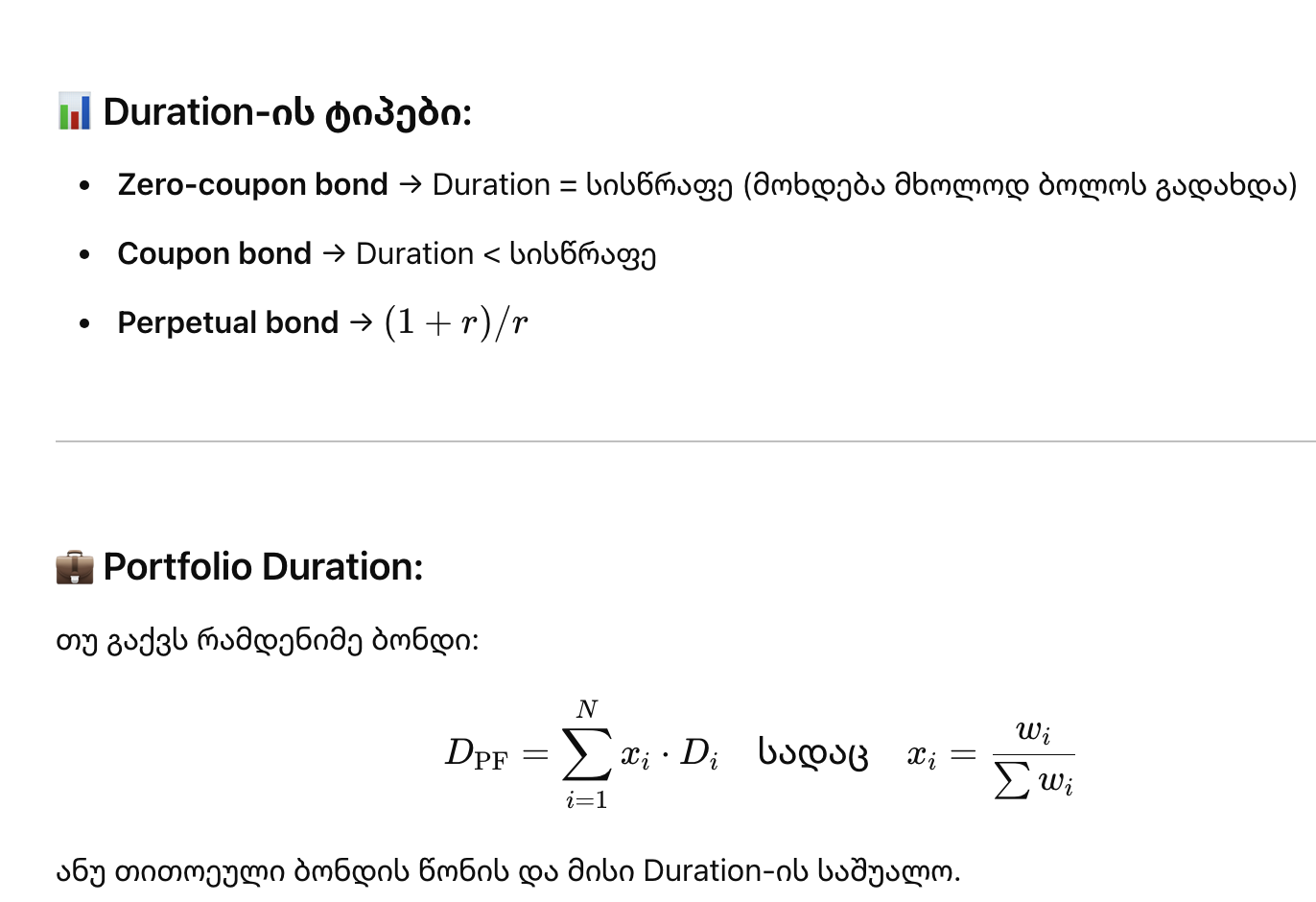

Duration of specific instruments

- Duration of a zero-bond equals the maturity of the bond since there are no coupon payments.

- Duration of coupon bonds is such that the larger the duration the larger the time to maturity, lower the market interest rate and lower the coupon

- Duration of perpetual is calculated specially as (1+r)/r