Chapter 11 - Dividends, Stock Repurchases, and Payout Policy

1/19

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced |

|---|

No study sessions yet.

20 Terms

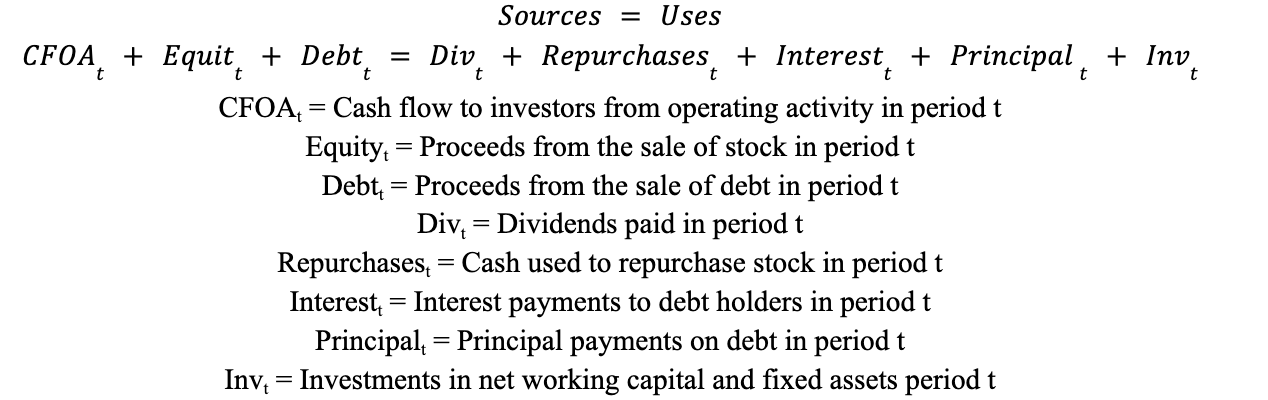

Dividends

Reduces the stockholders’ investment in a firm by distributing some of that investment to them

The value that the stockholders receive through a dividend was already theirs and the dividend simply takes this value out of the firm and returns it to them

Regular Cash Dividend

Cash dividend that is paid on a regular basis (generally quarterly) for the firm to return some of their profits to stockholders

Extra Dividend

Often paid at the time of regular cash dividends and used to ensure a minimum portion of earnings is distributed to shareholders

Management can afford to set the regular cash lower because it always has the option of paying extra dividend if earnings are too high

Special Dividend

One-time payment to stockholders that are used to distribute unusually large amounts of cash

Liquidating Dividend

Paid to stockholders when a firm is liquidated (its assets are sold)

Assets are used to first pay all wages owed to employees and the company’s obligations to suppliers, lenders, and taxing authorities

After all those obligations are satisfied, the company pays liquidating dividend to stockholders

Dividend Payment Process - Public Company

Board Vote: The board of directors, as stockholder representatives, vote to pay a dividend

Public Announcement/Declaration Date: The company announces to the public that it will pay the dividend, as well as the value received for each share and the dates

Can affect the firm’s stock price

Ex-Dividend Date: The first date on which the stock will trade without rights to the dividend

Investors who buy shares before this date will receive the dividend and investors who buy the stock after this date will not

The price of the stock drops on the ex-dividend date to reflect the difference in the value

Ex. A company currently trading for $10 per share announces $1 per share dividend, however, stock price drop on the ex-dividend date is less than $1 because the dividend will be taxed

Record Date: The date on which an investor must be a stockholder of record to receive the dividend (2 days after ex-dividend date)

Payable Date: Stockholders of record receive the dividend

Dividend Payment Process - Private Company

There is no public announcement, and there is no need for an ex-dividend date

The record date and payable date can be any day on or after the day that the board approves the dividend

Stock Repurchase vs Dividend

Stockholders can decide whether to participate in stock repurchases (not on a pro-rata basis) whereas all stockholders receive dividend distribution

Stock repurchases reduces the number of share held by investors

In stock repurchases, the stockholder is taxed only on the profit from the sale whereas in dividends, the total value of the dividend is taxed

Both cash dividends and stock repurchases decrease cash on the asset side, however, while cash dividends reduces retained earnings, stock repurchases increases treasury stock (making L&SE more negative)

Open Market Repurchases

Purchase shares in the market similar to an individual

Convenient way of repurchasing shares

However, the government limits the number of shares that can be repurchased each day to restrict the ability of firms to influence their stock price through trading activity

** Most common

Tender Offer

Open offer by a company to purchase shares and used when a company wants to distribute large amounts of cash at one time

Fixed-Price: Management announces the price that will be paid for shares, as well as the maximum number of shares that will repurchase and interested stockholders tender their shares by telling management how many they are willing to sell

Dutch Auction: The firm announces the number of shares it would like to repurchase and asks the stockholders how many shares they would sell at a series of prices

Targeted Stock Purchases

Direct negotiation with a specific stockholder to buy blocks of shares from large stockholders

Often allows companies to purchase shares below current market price since the shareholder would prefer it in exchange for certainly and speed of sale

Average stock price reaction to this is negative

A large stockholder's willingness to sell his or her shares may signal this investor's pessimism about the firm's prospect

Benefits of Dividends

Signal of Financial Strength:

Paying regular dividends shows that the company is financially healthy, which can attract investors and boost stock prices

External Monitoring:

If dividends exceed available cash, the company needs to raise funds by selling new shares

Raising capital triggers audits and scrutiny by external parties, encouraging managers to act efficiently and transparently

Capital Structure Management:

Dividends help the company return excess cash to stockholders, preventing it from becoming too equity-heavy

This supports maintaining an optimal mix of debt and equity, maximizing the firm’s value

Cost of Dividends

Dividends are taxable and stockholders have no choice but to receive the dividends and pay the associated taxes if they want to own the stock

Stockholders who want to reinvest their dividends often pay transaction costs like brokerage fees

Paying dividends reduces the total value of a company's assets which increases the risk for debt holders and may result in higher interest rates on the company’s debt

Stock Price Reactions to Dividend Announcements

In General:

When a company announces that it will begin paying a regular cash dividend, its stock price increases by an average of about 3.5 percent

Announcements of increases in regular cash dividends are associated with an average stock price increase of 1 to 2 percent

The announcement that a company will reduce its regular cash dividend is associated with a 3.5 percent decrease in its stock price

An announcement that a company will pay a special dividend is associated with an average stock price increase of about 2 percent

** This is not evidence that changes in dividends cause changes in stock prices, rather, changes in dividends are a result of fundamental changes

Advantage of Stock Repurchases

Flexibility for Stockholders: Stockholders can choose when to sell shares and time their taxes accordingly

Taxes on stock repurchases are often lower

Flexibility for Management: Stock repurchases can be adjusted or ended quietly without the negative market reaction associated with cutting dividends

No long-term dividend commitment

Disadvantages of Stock Repurchases

Weaker Signalling: Dividends send a stronger, more visible signal to investors about a company’s confidence in its future cash flows

Potential for Managerial Misuse: Managers who have best understanding of the company may repurchase shares when they believe the stock is undervalued, disadvantaging those who sell their shares

Management should act in the best interest of all shareholders, not just those who remain invested

Stock Dividends

Involves a company issuing additional shares to existing shareholders, rather than distributing cash

10% stock dividend means a shareholder with 100 shares will receive 10 additional shares

No value is distributed through stock dividends and it is simply an accounting change (the total value of the company is spread over more shares and the price per share decreases proportionally)

** Smaller, often regularly scheduled increases in shares, similar to cash dividends

Stock Splits

Division of each share into more than one share

Stockholders frequently receive one additional share for each share they already own (two-for-one stock split)

Three-for-one stock split means each stockholder receives 2 additional shares for each share they own

The value of each share decreases so the shareholder’s investment does not change

** Typically one-time events and involve larger increases in the number of shares

Reasons for Stock Dividends & Splits

Sends a positive signal to investors about management's outlook for the future and result in higher stock prices

Management is unlikely to want to split the stock of a company two-for-one or three-for-one if it expects the stock price to decline

Companies occasionally do reverse stock splits to satisfy exchange requirements

Ex. The NYSE generally requires listed shares to trade for more than $5, and the NASDAQ requires shares to trade for at least $1