microeconomics 2.1, 2.2, 2.3 demand, supply, equilibrium

1/44

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

45 Terms

Define a market

A place where willing + able people exchange to purchase a good/service/resource with others willing/able to provide it

*Does not need to be a physical place

What are 4 types of markets?

Product: selling goods and services

Factor: where resources are sold

Labour: people offer their services for a salary

Financial: where foreign currencies, company shares, other financial assets are traded

What is competition?

Occurs when there is many buyers and sellers that act independently

Markets are free + competitive when…..

private individuals can decide for themselves what is bought/sold at what price

What is the opposite of competition?

Market/monopoly power

What is individual demand? What is market demand?

Demand of one person for a product

Sum of all individual demands for a product at every price

Define demand

The quantity of a good or service that consumers are willing/able to purchase at various prices during a specific time period, ceteris paribus

What influences demand?

Price + non price determinants

For demand curve:

_____ lead to movement along the demand curve

______ will shift the entire demand curve because _________

Price changes —> movement on demand curve

Non price determinants —> shifts entire demand curve, since it changes the entire relationship between price and quantity

Examples of non price determinants that affect demand

Changes in income

Normal goods: goods whose demand increases when people’s income rises → in this case, demand curve shifts right

Applies for most items

Inferior goods: goods whose demand decreases as people’s income increases → in this case, demand curve shifts left

Ex. lower quality, cheaper goods that are used as substitutes for higher-quality goods

Substitutes

Definition: goods that have similar characteristics and uses for consumers

When price of the original good declines, quantity demanded of it increases → consumers have no need for the substitute → demand curve for substitute shift left

Close and remote substitutes

Close: almost identical goods but different brands (Coca cola + pepsi)

Remote: less similar goods, like coffee and orange juice

*Close substitutes will shift demand curve more drastically than remote substitutes → consumers more likely to change their preferences if they are similar

Complements

Definition: goods that are consumed together

The decrease in the price of one good = increase in quantity demanded → therefore, the second good is impacted as demand will also increase (even if price doesn’t change)

Close and remote complements

Close complements: one cannot function without another (Ex. printer + ink)

Remote complements: not so close but still related

*Like before: close complements will shift the demand curve more than remote complements

Other examples

Taste + preferences

Future expectations

1. Expectations about future prices → if they predict something will increase in value later, they will buy more of it now

2. Expectations about economy

Demographic changes

Number of consumers (due to government policy, etc)

Seasonal changes

What are normal and inferior goods?

Normal goods: goods whose demand increases when people’s income rises → in this case, demand curve shifts right

Applies for most items

Inferior goods: goods whose demand decreases as people’s income increases → in this case, demand curve shifts left

Ex. lower quality, cheaper goods that are used as substitutes for higher-quality goods

What are close and remote subsitutes?

Close: almost identical goods but different brands (Coca cola + pepsi)

Remote: less similar goods, like coffee and orange juice

Define substitute

Definition: goods that have similar characteristics and uses for consumers

What are complements?

Definition: goods that are consumed together

What are close and remote complements?

Close complements: one cannot function without another (Ex. printer + ink)

Remote complements: not so close but still related

Define ceteris paribus

Ceteris paribus: “all other things equal” → everything EXCEPT price of goods remains the same

What does the law of demand state?

Definition: as the price of the good/service decreases, the quantity demanded of it increases (ceteris paribus)

Why: since price decreased, this good has become relatively less expensive (compared to other similar goods). People have more real income to spend on this good so they will likely consume more of it

essentially, there’s an inverse relationship between price of good/service and the quantity demanded of it

It explains why the demand curve has a DOWNWARD slope

What assumptions/explanations were made for the law of demand?

Substitution effect → when customers substitute cheaper goods when those prices decline and consume more of them

Income effect → we assume that as real income increases, people have more money to spend to buy goods

Law of diminishing marginal utility (pizza)

How this impacts law of demand: a lower marginal utility leads to less willingness to pay a price for goods

Ex. after the 5th slice of pizza, people wouldn’t be willing to pay a lot to eat the 6th slice → this shows inverse relationship between price and quantity

*note: this is not always the case. For example, with more consumption of social media, marginal utility may increase

What is marginal utility?

the benefit (happiness) gained from consuming one extra unit of a product/service

*Total utility is all the utility added together, it declines when marginal utility becomes negative

What is the law of diminishing marginal utility?

Definition: as people consume additional units of a good/service, the marginal utility declines

*people usually get less satisfaction → ex. Eating pizza

What are producers?

Definition: people/companies/countries that make, grow, or supply goods + services + resources in a market

What is supply?

Definition: the quantity of a good/service that producers are willing/able to offer at various prices in a time period (CP)

What is effective supply? Individual supply? Market supply?

Effective —> demonstrated by the supply curve, it shows what producers can produce (not just willing)

Individual —> Supply of one product from one firm at every price

Market —→ Sum of all individual supplies of a product at every price

What is the law of supply?

Definition: as the price of a product increases, the quantity supplied will usually increase, CP → since they can cover their increasing marginal costs of production

But why? Due to profit. Firms want to make maximum profit, so higher prices tell them they should produce more goods.

Explains the UPWARD slope of supply curve (positive relationship between price and quantity)

What factors explain the law of supply?

Law of diminishing marginal return

If the marginal returns decrease = leads to more inputs needed to increase output → makes costs of production greater

Increasing marginal costs of production

A producer only wants to increase quantity supplied if they will receive a higher price in the market → therefore, assume that marginal costs increase as output increase and marginal returns decrease

What is marginal return? What’s the law of diminishing marginal return?

Marginal return: the additional output gained from adding an extra unit of input to a production process

The law: adding more of one factor of production (while other factors are constant) will at SOME point yield lower marginal returns

What is marginal cost?

Definition: cost of producing one extra unit of a good

For a supply curve

____ causes a movement

______ causes a shift

Price change causes movement

Non price determinants cause a shift

Give examples of non price determinants that effect supply curve

Changes in cost of factors of production (FOP)

Increase in cost of FOP → supply decrease (shifts inwards)

Technological change

More advanced technology → increased supply by more efficiency

Future expectations

Number of firms in market

If there are more firms offering this good → supply overall increases

Prices of related goods

Joint supply: occurs when 2+ goods are derived from the same product

*you cannot produce more of one good without producing more of another

*the second good is called a byproduct

Competitive supply: when production of 2 goods use similar resources and processes

*producing one of a good means prod ucing less of another

Government interventions

Indirect tax: tax imposed on a good/service → adds to selling price

When this is implemented → costs of production for firms increase, causing supply to decrease

Subsidies: money granted to a firm by the government

Opposite effect of tax

Reduces cost of production → supply increases

Regulations: a rule that requires certain behaviour

Usually increase cost of production → decrease supply

What is joint and competitive supply?

Joint supply: occurs when 2+ goods are derived from the same product

*you cannot produce more of one good without producing more of another

*the second good is called a byproduct

Competitive supply: when production of 2 goods use similar resources and processes

*producing one of a good means producing less of another

What is indirect tax?

Tax imposed on a good/service → adds to selling price

What are subsidies?

Money granted to a firm by the government

What are regulations?

A rule that requires certain behaviour

What is market equilibrium?

Market equilibrium: the point where the supply curve of a good or service crosses the demand curve

a state of balance, where the price/quantity of a good doesn’t change

Markets spend most of their time in _____ since ______

Disequilibrium, quantity demand doesn’t equal quantity supplied

Excess supply is also called _____ occurring when…..

Surplus

Qd < Qs

Increase in supply or decrease in demand

When the price in market is above equilibrium price

Excess demand is also called _____ it occurs when….

Shortage

Qd > Qs

Increase demand or lack of supply

When the price in market is below below equilibrium price

What is a feedback loop?

interdependency between 2+ components of a system → change in state of one component affects t

What is a negative feedback loop? Give 2 types

helps stabilise systems after disturbance →

Created by price changes

1. Signals

Rising prices give consumers signals that they should consume less of the product → they tell producers they should make more

Similarly, decreasing prices tell consumers they should consume more → tell producers to make less

Therefore: the signalling function of prices gives negative feedback by telling consumers/producers WHAT to do → brings market back into equilibrium

2. Incentives

Assuming that consumers want to maximise utility and producers want to maximise profits

Price of product rises → consumers buy less of it, reallocate resources into other products

Introduces negative feedback loop by providing financial MOTIVATION to react to bring market back in equilibrium

What are 2 types of efficiency? Describe.

1. Allocative efficiency

Producing optimal combination of goods (lowest opportunity cost) → reaching this situation is called pareto optimality

Requires productive efficiency + maximising social/community surplus

*in society’s POV

2. Productive efficiency

Producing goods using fewest resources (lower cost)

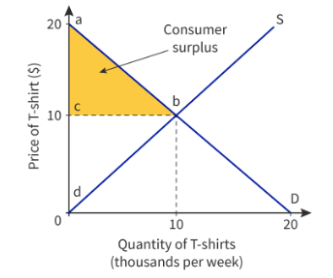

Consumer surplus is….

Difference between highest price consumers willing to pay and actual price paid

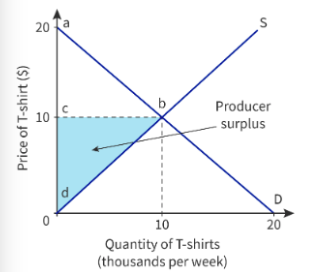

Producer surplus is….

Difference between lowest price producers willing to offer and actual price they receive

Social/community surplus is….

Sum of consumer surplus + producer surplus → total benefit gained by society

give 3 assumptions made about human behaviour

Human beings are assumed to have clear preferences that are stable over time, ceteris paribus.

Human beings are assumed to have highly developed analytical skills and perfect knowledge to make rational choices.

Rational behaviour for human beings means maximising personal satisfaction (utility) at all times.

what is the difference between the quantity demanded of bananas and the demand of bananas?

quantity demanded of bananas: a movement along the demand curve

the demand of bananas: a shift of the entire demand curve