Portfolio management

1/39

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai | Chat |

|---|

No analytics yet

Send a link to your students to track their progress

40 Terms

A portfolio manager is evaluating whether to add Stock X to a well-diversified equity portfolio. Stock X has relatively high firm-specific risk but a correlation of only 0.15 with the existing portfolio.

The manager’s primary reason for adding Stock X is that it will most likely:

A. Reduce the portfolio’s overall volatility through diversification.

B. Eliminate the portfolio’s market risk.

C. Increase expected return without affecting risk.

Answer:

A

Topic: Portfolio Risk and Return

Key Testable Point: Diversification benefits depend on correlation, not simply individual asset risk.

Explanation:

A low correlation allows firm-specific risk to offset risk from other holdings, potentially lowering overall portfolio volatility. Diversification cannot eliminate systematic (market) risk, and adding an asset generally changes both expected return and risk.

Difficulty: Medium

An analyst estimates the following for a stock:

Risk-free rate: 3%

Expected market return: 9%

Beta: 1.4

The stock’s expected return is 13%.

Based on CAPM, the stock is most likely:

A. Overvalued because its expected return exceeds its required return.

B. Undervalued because its expected return exceeds its required return.

C. Fairly valued because its beta is above one.

Answer:

B

Topic: CAPM

Key Testable Point: Compare expected return with CAPM required return.

Explanation:

Required return = 3% + 1.4(9% − 3%) = 11.4%. Since the stock is expected to earn 13%, it offers more return than required for its level of systematic risk, suggesting it is undervalued. Beta alone does not determine valuation.

Difficulty: Medium

A client owns 35 individual stocks selected from different industries. Despite the large number of holdings, the portfolio remains heavily invested in companies that are highly sensitive to economic cycles.

The portfolio is still exposed primarily to:

A. Unsystematic risk.

B. Firm-specific operational risk.

C. Systematic risk.

Answer:

C

Topic: Diversification

Key Testable Point: Diversification removes mainly unsystematic risk.

Explanation:

Holding many securities substantially reduces firm-specific risk. However, exposure to broad economic conditions cannot be diversified away and remains as systematic risk.

Difficulty: Easy

A portfolio has a Sharpe ratio of 0.95. Another portfolio has a Sharpe ratio of 0.70.

Assuming both portfolios are evaluated over the same period, the first portfolio most likely:

A. Generated a higher absolute return.

B. Earned more excess return per unit of total risk.

C. Had a lower beta.

Answer:

B

Topic: Risk Measures

Key Testable Point: Interpretation of the Sharpe ratio.

Explanation:

The Sharpe ratio measures excess return relative to total volatility. A higher ratio indicates better risk-adjusted performance but does not necessarily imply higher absolute returns or lower beta.

Difficulty: Easy

An investor currently holds two stocks with a correlation of 0.85. She replaces one stock with another that has similar expected return and volatility but a correlation of 0.20 with the remaining stock.

The portfolio’s standard deviation will most likely:

A. Increase.

B. Remain unchanged.

C. Decrease.

Answer:

C

Topic: Correlation

Key Testable Point: Lower correlation increases diversification benefits.

Explanation:

Reducing correlation improves diversification, lowering overall portfolio volatility while expected return may remain similar. Correlation—not individual volatility alone—drives diversification benefits.

Difficulty: Medium

A pension fund is choosing between two efficient portfolios.

Portfolio A offers a higher expected return but substantially higher volatility.

Portfolio B offers a lower expected return with much lower volatility.

Which additional information is most important before selecting one portfolio?

A. The fund’s risk tolerance.

B. The portfolio managers’ years of experience.

C. The average dividend yield.

Answer:

A

Topic: Portfolio Theory

Key Testable Point: Investor preferences determine the optimal portfolio on the efficient frontier.

Explanation:

Every efficient portfolio is optimal for some investor depending on risk tolerance. Manager experience and dividend yield are secondary compared with matching the portfolio to the investor’s objectives.

Difficulty: Medium

A security has a beta of 0.6. The market declines by 10%.

Ignoring firm-specific events, the security would be expected to:

A. Decline by approximately 16%.

B. Decline by approximately 6%.

C. Experience no predictable change.

Answer:

B

Topic: Beta

Key Testable Point: Beta measures sensitivity to market movements.

Explanation:

A beta of 0.6 implies the security tends to move about 60% as much as the market. A 10% market decline therefore implies an expected decline of roughly 6%.

Difficulty: Easy

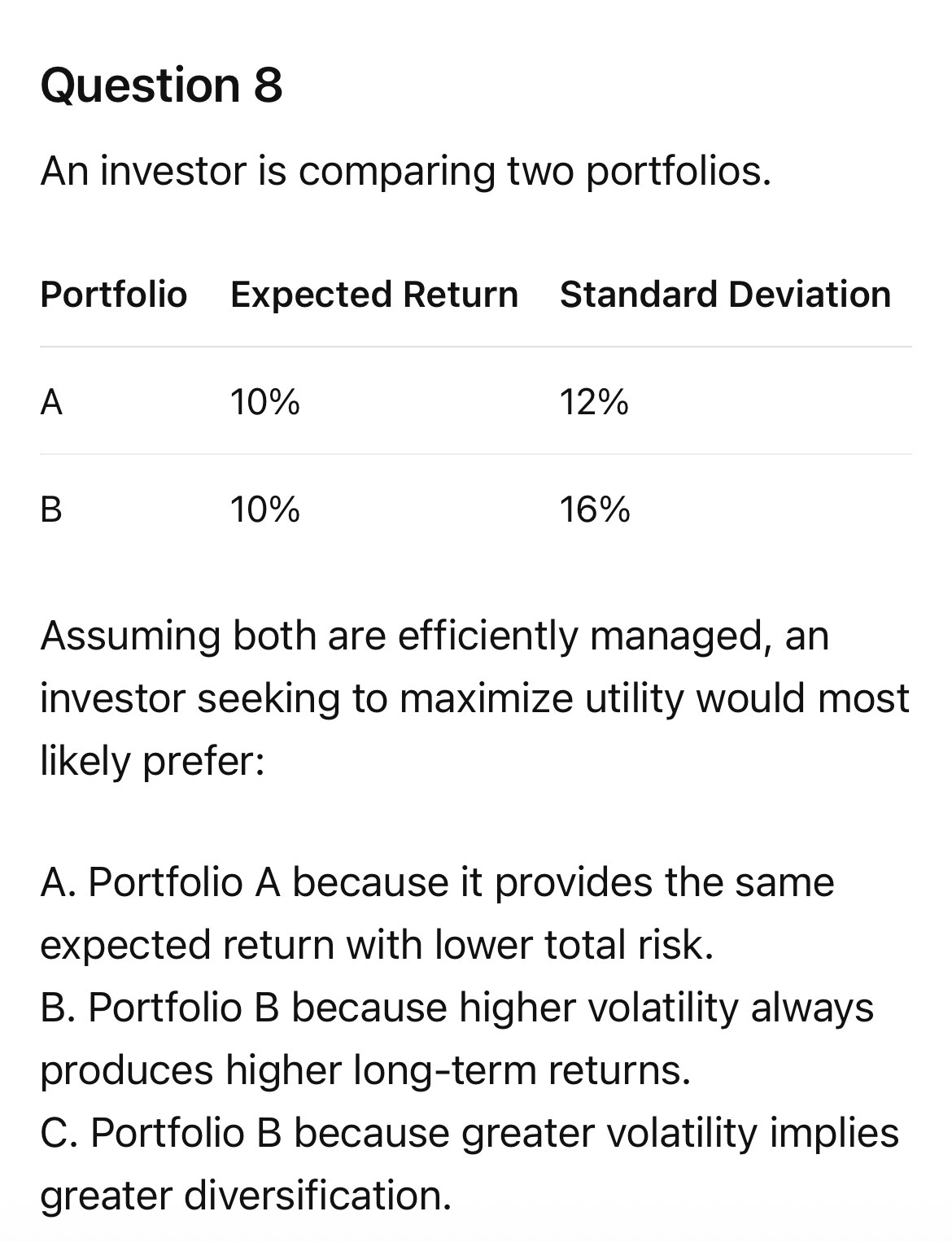

Answer:

A

Topic: Mean-Variance Optimization

Key Testable Point: Portfolio dominance.

Explanation:

Portfolio A dominates Portfolio B because it offers the same expected return with less risk. Rational investors prefer dominant portfolios when all other characteristics are equal.

Difficulty: Easy

A retired investor expects substantial medical expenses over the next year and wants to avoid selling long-term investments during unfavorable market conditions.

The IPS should most strongly emphasize:

A. A higher return objective.

B. Greater tolerance for market risk.

C. Increased liquidity needs.

Answer:

C

Topic: Investment Policy Statement (IPS)

Key Testable Point: Liquidity constraints.

Explanation:

Expected near-term cash requirements increase liquidity needs. The portfolio should contain assets that can be readily converted to cash without forcing sales of long-term investments.

Difficulty: Medium

Following a strong bull market, an investor refuses to reduce exposure to speculative technology stocks because she believes her previous investment success proves she can consistently identify winning stocks.

This behavior most likely reflects:

A. Loss aversion.

B. Overconfidence bias.

C. Mental accounting.

Answer:

B

Topic: Behavioral Finance

Key Testable Point: Recognizing overconfidence.

Explanation:

Overconfidence causes investors to overestimate their forecasting ability and investment skill. Loss aversion relates to avoiding realized losses, while mental accounting involves treating money differently depending on its source or intended use.

A portfolio manager is evaluating two securities with identical expected returns and standard deviations. The securities have a correlation of –0.40.

Combining the two securities in a portfolio will most likely:

A. Increase portfolio volatility because one asset has to offset the other.

B. Reduce portfolio volatility due to their negative correlation.

C. Leave portfolio volatility unchanged because expected returns are identical.

Answer:

B

Topic: Portfolio Risk and Return

Key Testable Point: Effect of negative correlation on diversification.

Explanation:

Negative correlation causes the assets’ returns to offset one another, reducing overall portfolio risk. Identical expected returns do not determine portfolio volatility, and diversification benefits arise from correlation, not return.

Difficulty: Medium

Question 12

An investor calculates a stock’s required return using CAPM at 10%. The analyst’s forecasted return is 8%.

The stock is most likely:

An investor calculates a stock’s required return using CAPM at 10%. The analyst’s forecasted return is 8%.

The stock is most likely:

A. Overvalued.

B. Undervalued.

C. Correctly priced.

Answer:

A

Topic: CAPM

Key Testable Point: Comparing expected and required return.

Explanation:

If the expected return is below the required return, investors are not being adequately compensated for risk. The stock’s price is therefore too high, making it overvalued.

Difficulty: Medium

A client wants the lowest possible portfolio risk without considering expected return.

The most appropriate portfolio on the efficient frontier is the:

A. Tangency portfolio.

B. Maximum return portfolio.

C. Minimum variance portfolio.

Answer:

C

Topic: Portfolio Theory

Key Testable Point: Characteristics of the minimum variance portfolio.

Explanation:

The minimum variance portfolio has the lowest possible volatility among all feasible portfolios. It may not provide the highest expected return but is appropriate for extremely risk-averse investors.

Difficulty: Easy

A stock has a beta of 1.8. The market risk premium unexpectedly increases while the risk-free rate remains unchanged.

According to CAPM, the stock’s required return will:

A. Increase more than that of a stock with beta 0.8.

B. Increase by the same amount as all other stocks.

C. Remain unchanged because beta is constant.

Answer:

A

Topic: CAPM

Key Testable Point: Impact of changes in the market risk premium.

Explanation:

Required return equals the risk-free rate plus beta times the market risk premium. A higher beta amplifies the effect of an increase in the market risk premium.

Difficulty: Medium

A portfolio manager adds several additional securities to an already well-diversified portfolio.

The manager should expect the greatest reduction in:

A. Market risk.

B. Inflation risk.

C. Firm-specific risk.

Answer:

C

Topic: Diversification

Key Testable Point: Diversification primarily reduces unsystematic risk.

Explanation:

Adding securities diversifies away firm-specific risk. Market-wide risks such as recessions and inflation remain largely unavoidable.

Difficulty: Easy

Portfolio X has an expected return of 11% and a standard deviation of 13%.

Portfolio Y has an expected return of 12% and a standard deviation of 20%.

Without additional information, the better portfolio depends primarily on:

A. The investor’s risk preferences.

B. Which portfolio has more securities.

C. Which portfolio has the higher beta.

Answer:

A

Topic: Portfolio Theory

Key Testable Point: Utility depends on investor risk tolerance.

Explanation:

Neither portfolio dominates because one offers higher return while the other has lower risk. The preferred portfolio depends on the investor’s willingness to accept additional volatility.

Difficulty: Medium

Two portfolios generated identical annual returns.

Portfolio A experienced substantially lower volatility than Portfolio B.

Assuming the same risk-free rate, Portfolio A most likely has the:

A. Lower Sharpe ratio.

B. Same Sharpe ratio.

C. Higher Sharpe ratio.

Answer:

C

Topic: Risk Measures

Key Testable Point: Interpretation of Sharpe ratio.

Explanation:

With equal returns and the same risk-free rate, lower volatility produces a higher Sharpe ratio. This indicates superior risk-adjusted performance.

Difficulty: Easy

An investor refuses to sell a declining stock because she wants to “wait until it gets back to what I paid.”

This behavior is most consistent with:

A. Overconfidence.

B. Loss aversion.

C. Availability bias.

Answer:

B

Topic: Behavioral Finance

Key Testable Point: Recognizing loss aversion.

Explanation:

Loss-averse investors dislike realizing losses and often hold losing investments too long. Overconfidence involves excessive faith in one’s abilities, while availability bias relies on easily recalled information.

Difficulty: Medium

An investor refuses to sell a declining stock because she wants to “wait until it gets back to what I paid.”

This behavior is most consistent with:

A. Overconfidence.

B. Loss aversion.

C. Availability bias.

Answer:

B

Topic: Behavioral Finance

Key Testable Point: Recognizing loss aversion.

Explanation:

Loss-averse investors dislike realizing losses and often hold losing investments too long. Overconfidence involves excessive faith in one’s abilities, while availability bias relies on easily recalled information.

Difficulty: Medium

A stock plots above the Security Market Line.

The stock is most likely:

A. Offering more expected return than required for its systematic risk.

B. Carrying less systematic risk than indicated by its beta.

C. Correctly priced because it lies above the CAPM relationship.

Answer:

A

Topic: CAPM / Security Market Line

Key Testable Point: Interpretation of the Security Market Line.

Explanation:

A security above the SML offers a higher expected return than required by CAPM, indicating it is undervalued. Securities below the SML are considered overvalued because they offer insufficient expected return for their level of systematic risk.

An investor is comparing two portfolios with identical expected returns. Portfolio A has a beta of 0.9, while Portfolio B has a beta of 1.4. The investor’s existing wealth is already broadly diversified.

The investor should view Portfolio B as having:

A. Greater systematic risk.

B. Greater unsystematic risk.

C. Better diversification.

Answer:

A

Topic: CAPM / Beta

Key Testable Point: Beta measures systematic risk.

Explanation:

For a diversified investor, beta is the primary measure of relevant risk. A higher beta indicates greater sensitivity to market movements. Unsystematic risk is assumed to be largely diversified away.

A portfolio manager adds an asset with an expected return slightly below the portfolio average. However, the asset’s correlation with the existing portfolio is close to zero.

The addition is most likely to:

A. Reduce expected return without affecting risk.

B. Improve the portfolio’s risk-return tradeoff.

C. Increase total portfolio risk.

Answer:

B

Topic: Portfolio Risk and Return

Key Testable Point: Diversification can improve portfolio efficiency.

Explanation:

Even an asset with a modest expected return may improve the portfolio if it provides substantial diversification benefits. The reduction in risk may outweigh the slight decrease in expected return.

Difficulty: Hard

An analyst calculates the following:

Risk-free rate = 2%

Expected market return = 8%

Beta = 0.5

The required return under CAPM is closest to:

A. 4%

B. 5%

C. 6%

Answer:

B

Topic: CAPM

Key Testable Point: CAPM calculation.

Explanation:

Required return = 2% + 0.5 × (8% − 2%) = 5%. A common mistake is forgetting to multiply the market risk premium by beta.

Difficulty: Easy

A young professional has stable employment, minimal debt, and does not expect to use investment assets for at least 35 years.

The IPS should most likely reflect:

A. High liquidity needs.

B. A short investment horizon.

C. Above-average ability to accept investment risk.

Answer:

C

Topic: Investment Policy Statement

Key Testable Point: Time horizon influences risk objective.

Explanation:

A long investment horizon generally increases an investor’s ability to tolerate short-term market volatility. Liquidity needs are relatively low, allowing greater allocation to growth assets.

Difficulty: Easy

Portfolio A has a Sharpe ratio of 0.80.

Portfolio B has a Sharpe ratio of 1.10.

Portfolio C has a Sharpe ratio of 0.95.

Based solely on risk-adjusted performance, the preferred portfolio is:

A. Portfolio B.

B. Portfolio C.

C. Portfolio A.

Answer:

A

Topic: Risk Measures

Key Testable Point: Comparing Sharpe ratios.

Explanation:

The highest Sharpe ratio indicates the greatest excess return per unit of total risk. Absolute return alone is insufficient for comparing risk-adjusted performance.

Difficulty: Easy

An investor insists on evaluating every investment account independently instead of considering total household wealth.

This behavior is most consistent with:

A. Confirmation bias.

B. Mental accounting.

C. Overconfidence.

Answer:

B

Topic: Behavioral Finance

Key Testable Point: Recognizing mental accounting.

Explanation:

Mental accounting occurs when investors separate assets into distinct “mental buckets” instead of viewing wealth as one portfolio. This can result in suboptimal asset allocation decisions.

Difficulty: Medium

A portfolio currently consists of 40 securities from many industries. The manager is considering adding another stock that has a correlation of 0.95 with the existing portfolio.

The additional diversification benefit will most likely be:

A. Significant because another security is being added.

B. Moderate because the portfolio already contains many holdings.

C. Minimal because the new security is highly correlated with the portfolio.

Answer:

C

Topic: Diversification

Key Testable Point: Marginal diversification depends on correlation.

Explanation:

Adding another highly correlated asset provides little additional diversification. The number of holdings alone does not determine the benefit; correlation is the critical factor.

Difficulty: Medium

A stock has a beta of 1.3. The risk-free rate decreases while the expected market return remains unchanged.

According to CAPM, the stock’s required return will most likely:

A. Decrease.

B. Increase.

C. Remain unchanged.

Answer:

A

Topic: CAPM

Key Testable Point: Effect of changes in the risk-free rate.

Explanation:

Required return = Risk-free rate + Beta × Market Risk Premium. A lower risk-free rate reduces both the base rate and the market risk premium (if the expected market return is unchanged), leading to a lower required return.

Difficulty: Hard

An investor selects a portfolio on the efficient frontier that maximizes expected utility based on personal risk preferences.

This portfolio is known as the investor’s:

A. Minimum variance portfolio.

B. Optimal portfolio.

C. Market portfolio.

Answer:

B

Topic: Portfolio Theory

Key Testable Point: Optimal portfolio selection.

Explanation:

The optimal portfolio is the point on the efficient frontier that best matches the investor’s risk-return preferences. It differs among investors because utility functions vary.

Difficulty: Medium

During a quarterly performance review, a portfolio manager explains that the portfolio underperformed primarily because the allocation to defensive sectors lagged a strong rally in cyclical stocks.

This explanation is an example of:

A. Security selection attribution.

B. Risk budgeting.

C. Asset allocation attribution

Answer:

C

Topic: Return Attribution

Key Testable Point: Distinguishing allocation effects from security selection effects.

Explanation:

Asset allocation attribution evaluates the impact of overweighting or underweighting sectors or asset classes relative to a benchmark. Security selection attribution instead focuses on the choice of individual securities within those sectors.

A portfolio manager is considering replacing one holding with another that has the same expected return but higher standard deviation and a much lower correlation with the rest of the portfolio.

The replacement is most likely to:

A. Increase portfolio risk because the individual security is more volatile.

B. Reduce portfolio risk if the diversification benefit outweighs the higher individual volatility.

C. Have no effect because expected return is unchanged.

Answer:

B

Topic: Portfolio Risk and Return

Key Testable Point: Portfolio risk depends on both individual volatility and correlation.

Explanation:

A security with higher individual volatility can still lower overall portfolio risk if it has sufficiently low correlation with the existing portfolio. Portfolio risk is determined by covariance among assets, not simply the volatility of each holding.

Difficulty: Hard

Two portfolios have identical expected returns and standard deviations. Portfolio A has a beta of 0.8, while Portfolio B has a beta of 1.3.

For a well-diversified investor, Portfolio B is most likely to:

A. Have greater relevant risk.

B. Have greater firm-specific risk.

C. Provide superior diversification.

Answer:

A

Topic: CAPM / Beta

Key Testable Point: Beta is the relevant risk measure for diversified investors.

Explanation:

Diversified investors are primarily concerned with systematic risk, which beta measures. Firm-specific risk is assumed to have been diversified away.

Difficulty: Medium

A portfolio manager observes that adding international equities has reduced the portfolio’s overall volatility even though the international market has higher individual volatility than the domestic market.

The most likely explanation is:

A. International equities have lower expected returns.

B. International equities have low correlation with domestic equities.

C. International equities eliminate systematic risk.

Answer:

B

Topic: Diversification

Key Testable Point: International diversification benefits arise from imperfect correlation.

Explanation:

Assets with low correlation reduce total portfolio volatility, even if they are individually volatile. Systematic risk cannot be completely eliminated through diversification.

Difficulty: Medium

A stock’s expected return is 11%, while its CAPM required return is 13%.

Relative to the Security Market Line, the stock plots:

A. Above the SML.

B. On the SML.

C. Below the SML.

Answer:

C

Topic: CAPM / Security Market Line

Key Testable Point: Relationship between expected and required return.

Explanation:

A stock earning less than its required return lies below the Security Market Line and is considered overvalued. Investors are receiving insufficient compensation for its systematic risk.

Difficulty: Medium

An investor becomes increasingly risk-averse after suffering significant investment losses, even though her long-term financial objectives have not changed.

This behavioral response is most consistent with:

A. Loss aversion.

B. Anchoring.

C. Representativeness.

Answer:

A

Topic: Behavioral Finance

Key Testable Point: Emotional biases affecting investment decisions.

Explanation:

Loss aversion causes investors to weigh losses more heavily than gains, often resulting in excessive conservatism after market declines. Anchoring and representativeness involve different cognitive errors.

Difficulty: Medium