Unit 1: Basic Economic Concepts

1/53

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

54 Terms

Economics

The study of how people seek to satisfy their needs and wants by making choices

scarcity

Limited quantities of resources to meet unlimited wants

Microeconomics

the study of how households and firms make decisions and how they interact in markets

macroeconomics

the study of the economy as a whole, including topics such as inflation, unemployment, and economic growth

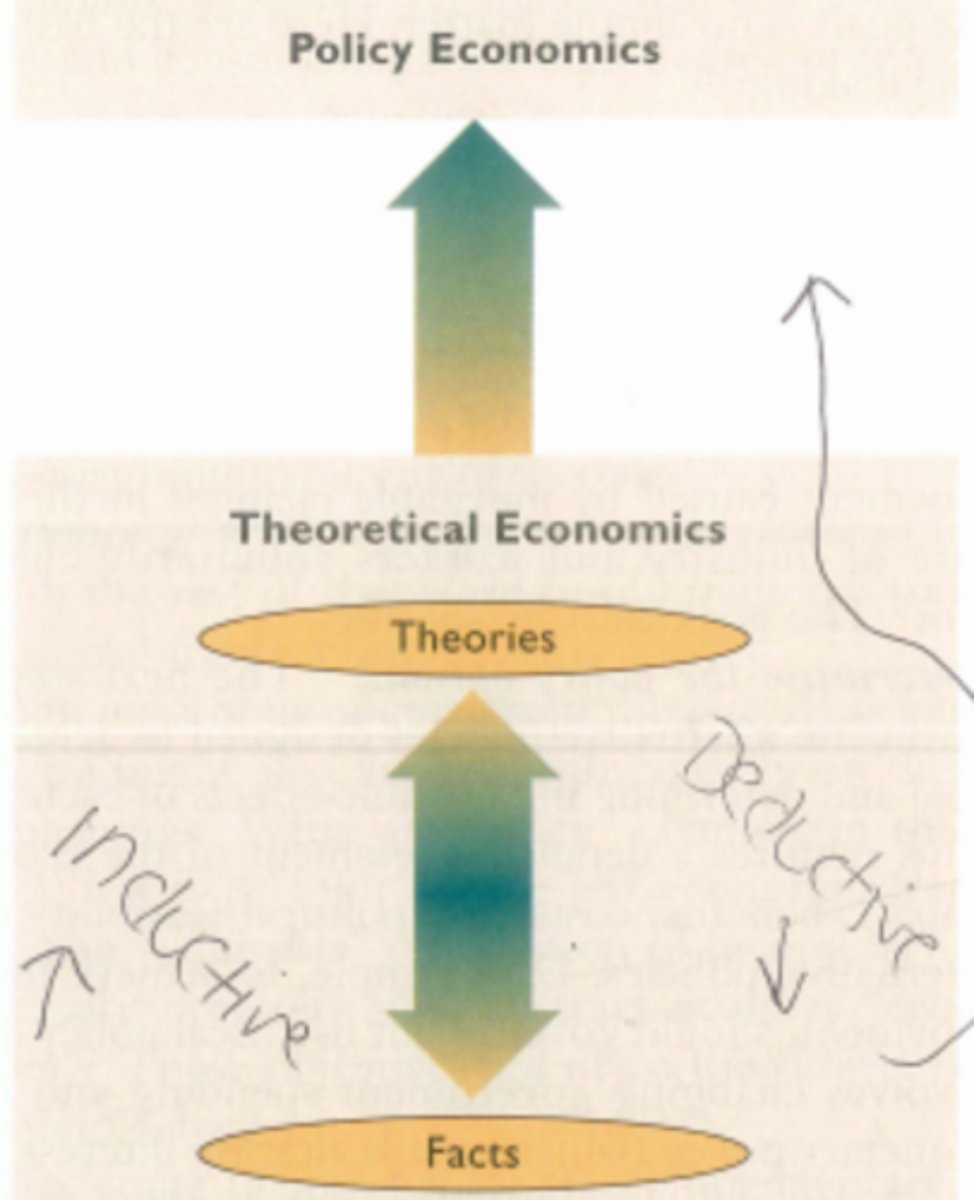

theoretical economics

economists use the scientific method to make generalizations and abstractions to develop theories

policy economics

Theories are applied to fix problems or meet economic goals

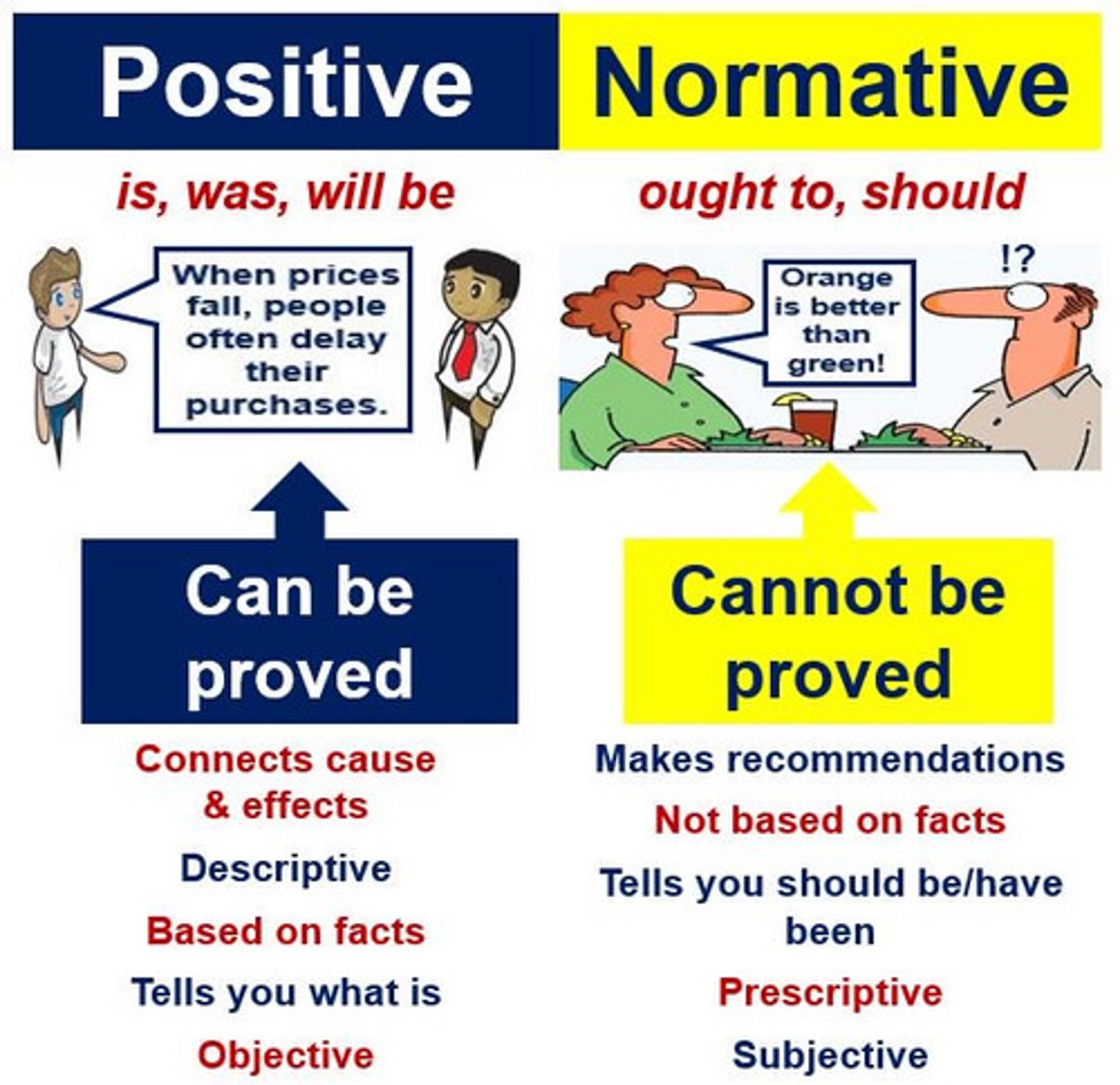

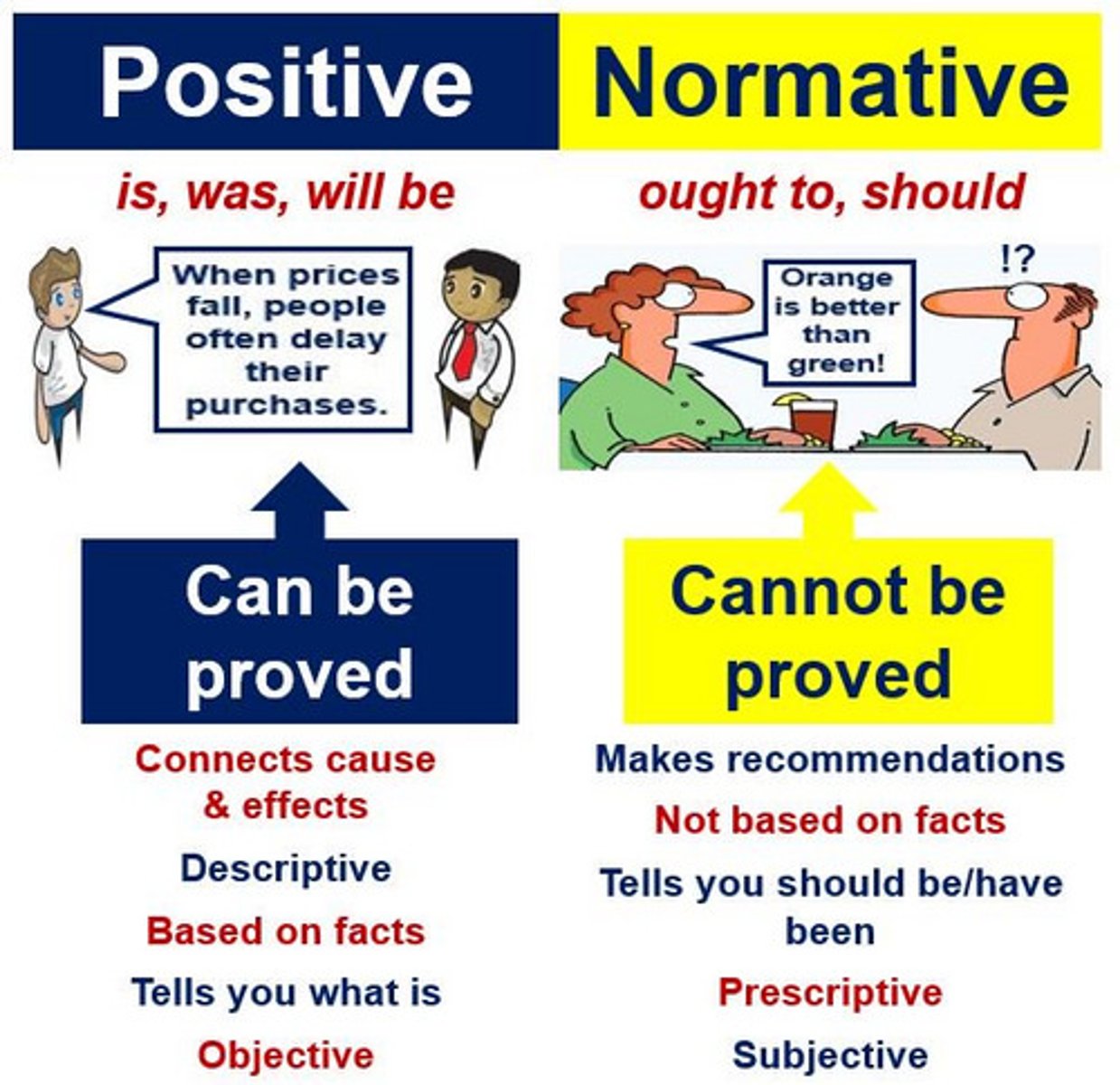

positive economics

the branch of economic analysis that describes the way the economy actually works; based on Facts

normative economics

The part of economics involving value judgments about what the economy should be like; focused on which economic goals and policies should be implemented; policy economics; What ought to be.

trade-off

all the alternatives that we sacrifice when we make a decision

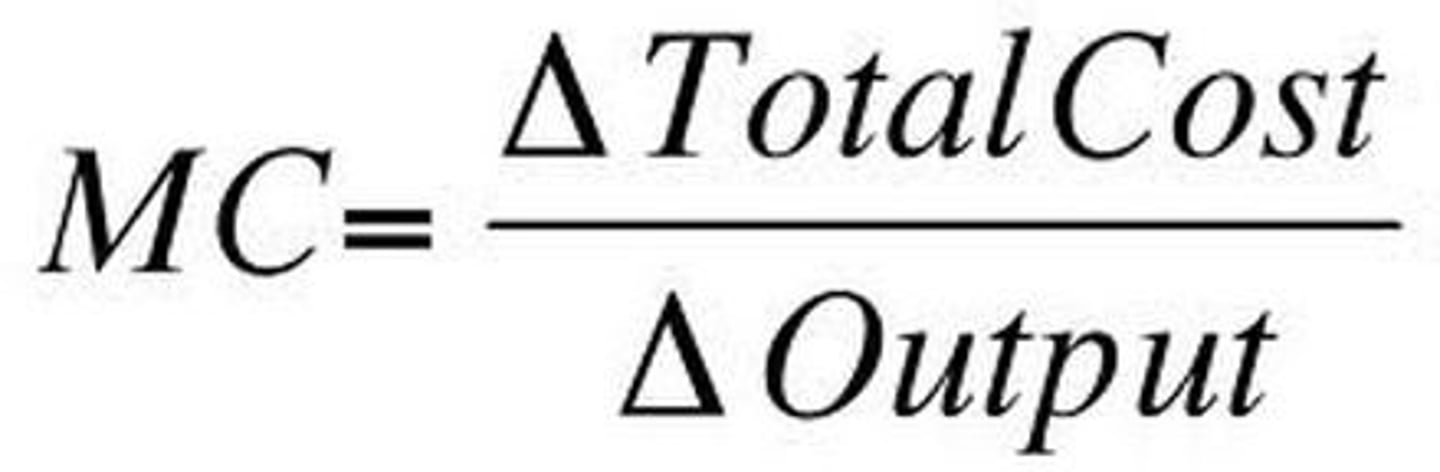

marginal costs (MC)

the cost of producing one more unit of a good

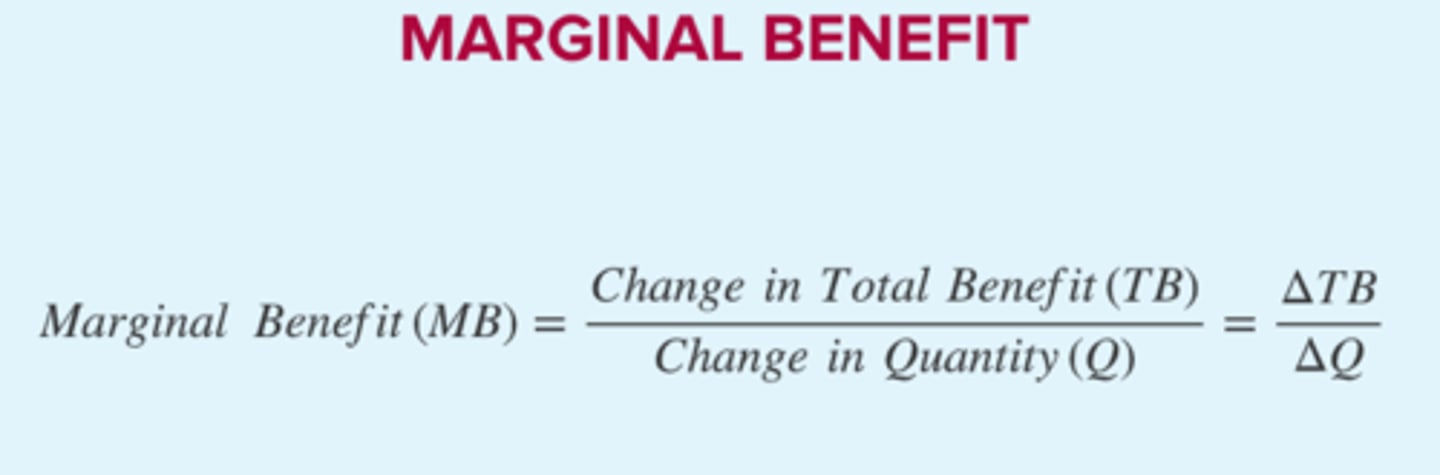

marginal benefit (MB)

The additional benefit received from the consumption of the next unit of a good or service

marginal analysis

analysis that involves comparing marginal benefits and marginal costs (Marginal = Additional)

opportunity cost

the most desirable alternative given up as the result of a decision

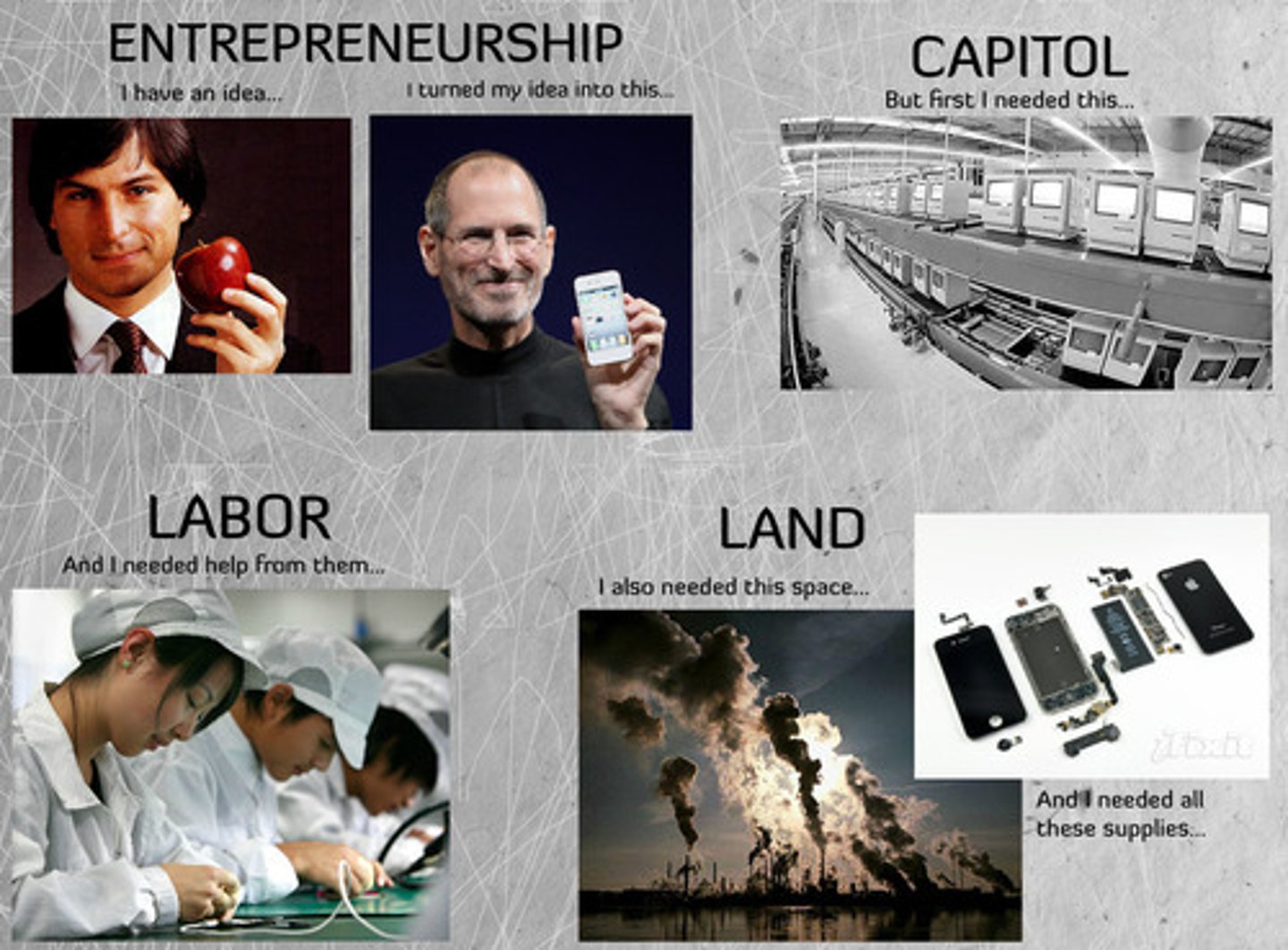

four factors of production

land, labor, capital, entrepreneurship

land

all natural resources used to produce goods and services (water, sun, plants, animals, etc)

labor

Human effort directed toward producing goods and services

physical capital

the human-made objects used to create other goods and services

human capital

the skills and knowledge gained by a worker through education and experience

Entrepreneurship

the process of starting, organizing, managing, and assuming the responsibility for a business

investment

the money spend by businesses to improve their production usually by increasing their capital

consumer goods

products and services that satisfy human wants directly

capital goods

Buildings, machines, technology, and tools needed to produce goods and services.

Productivity

The value of a particular product compared to the amount of labor needed to make it.

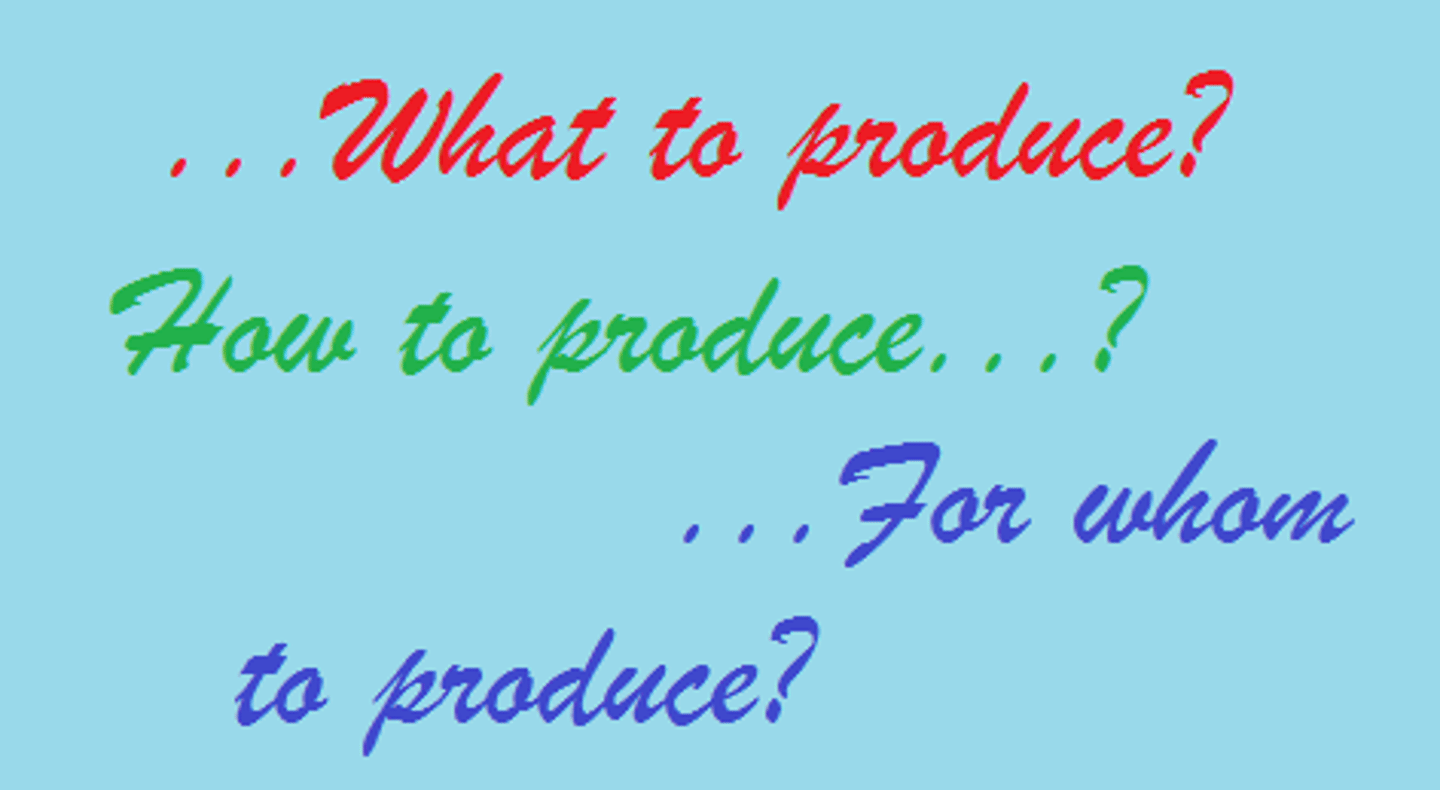

Three Economics Questions

What to produce? How to produce? For whom to produce?

economic system

the method used by a society to produce and distribute goods and services

command economy

An economic system in which the government controls a country's economy. aka: communism

free market economy

an economic system in which decisions on the three key economic questions are based on voluntary exchange in markets

mixed economy

An economy in which private enterprise exists in combination with a considerable amount of government regulation and promotion.

Laissez-faire economics

Theory that opposes government interference in economic affairs beyond what is necessary to protect life and property.

invisible hand

A phrase coined by Adam Smith to describe the process that turns self-directed gain into social and economic benefits for all

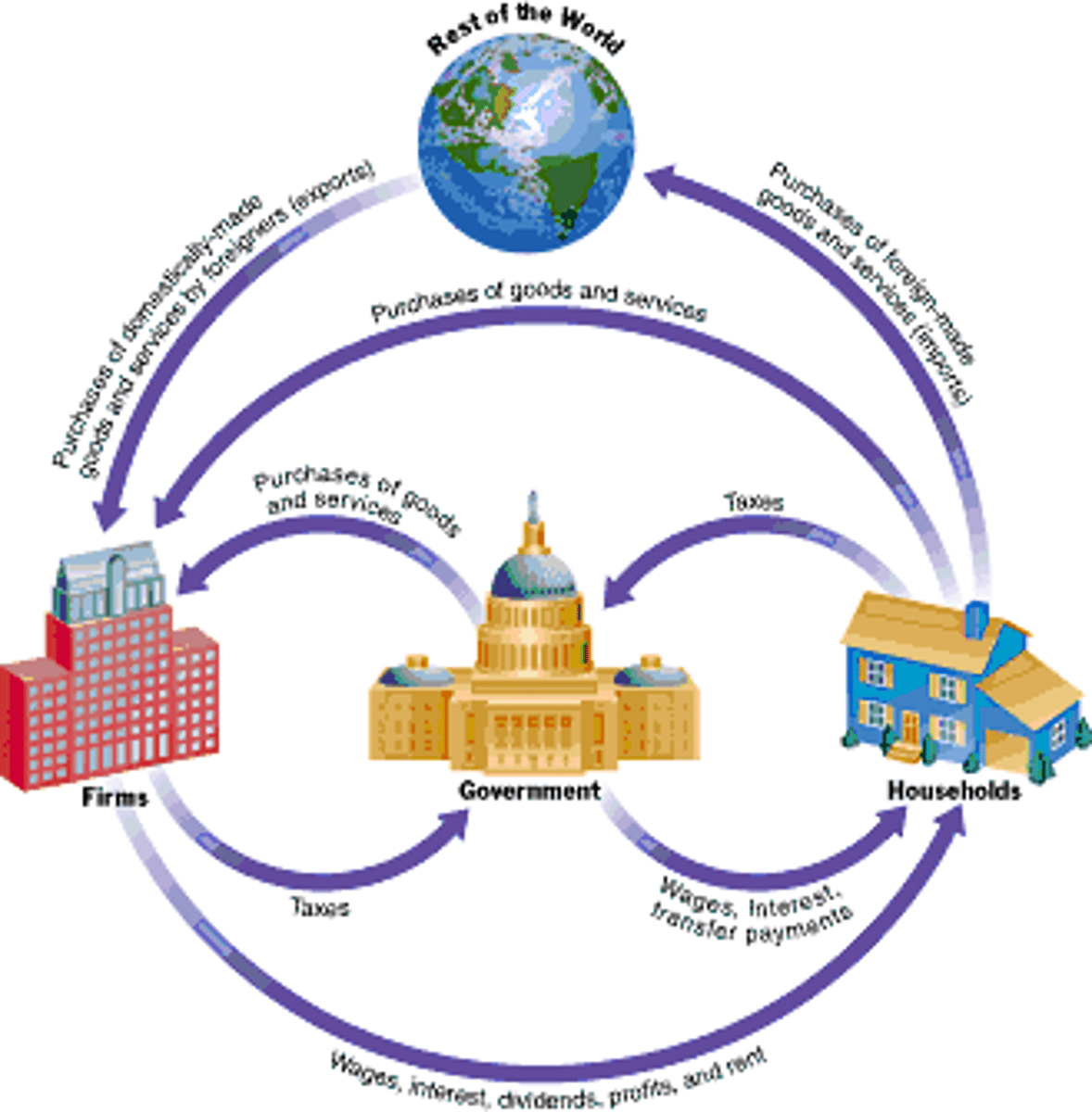

circular flow matrix

relationship between households, businesses, and the government

businesses supply products but demand resources

consumers supply resources but demand products

product market

the market in which households purchase the goods and services that firms produce

resource market

a market in which households sell and firms buy resources or the services of resources

private sector

the part of the national economy that is not under direct government control.

public sector

the part of an economy that is controlled by the government.

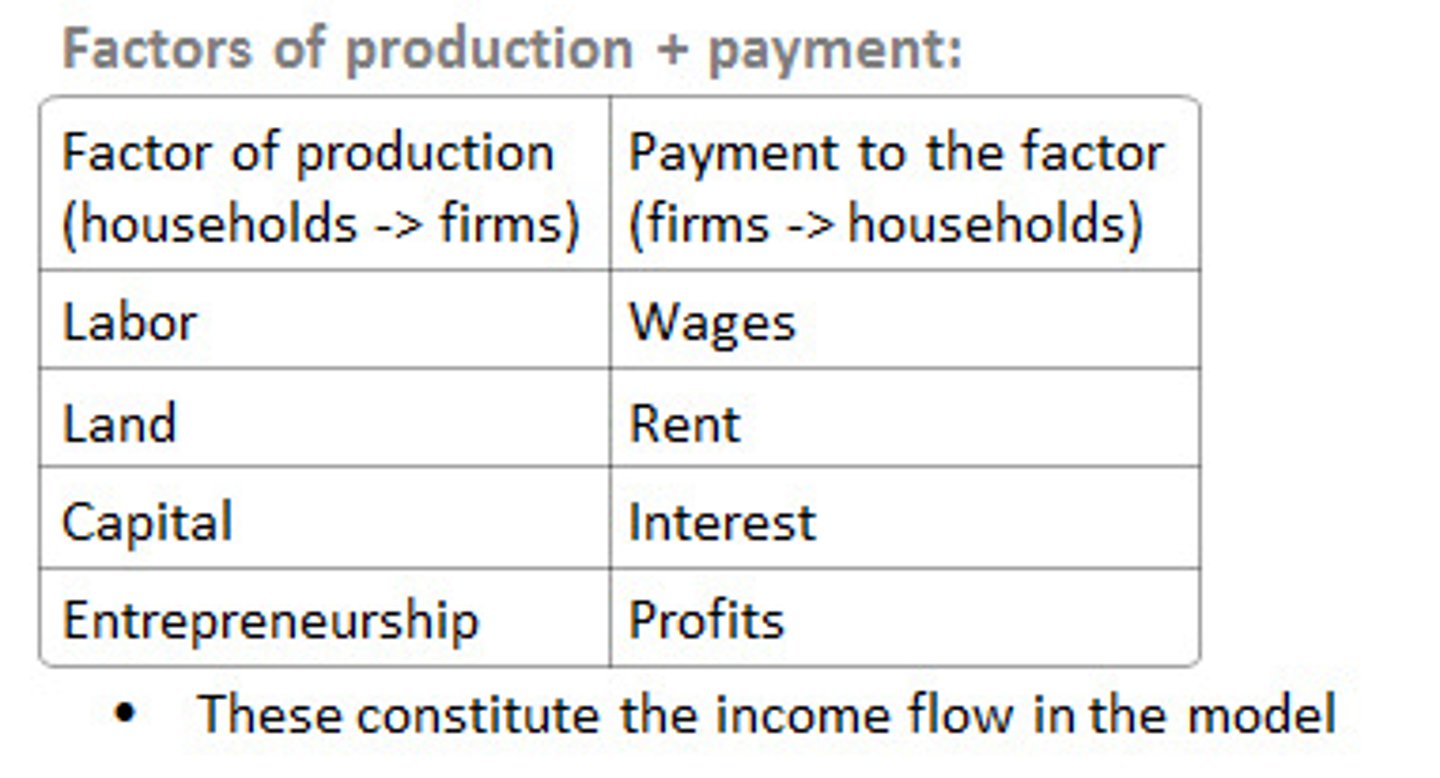

factor payments

payment for the factors of production, namely rent for land, wages for labor, interest for capital, and profit for entrepreneurship

transfer payments

Benefits given by the government directly to individuals. Transfer payments may be either cash transfers, such as Social Security payments and retirement payments to former government employees, or in-kind transfers, such as food stamps and low-interest loans for college education.

Subsidies

a sum of money granted by the government or a public body to assist an industry or business so that the price of a commodity or service may remain low or competitive.

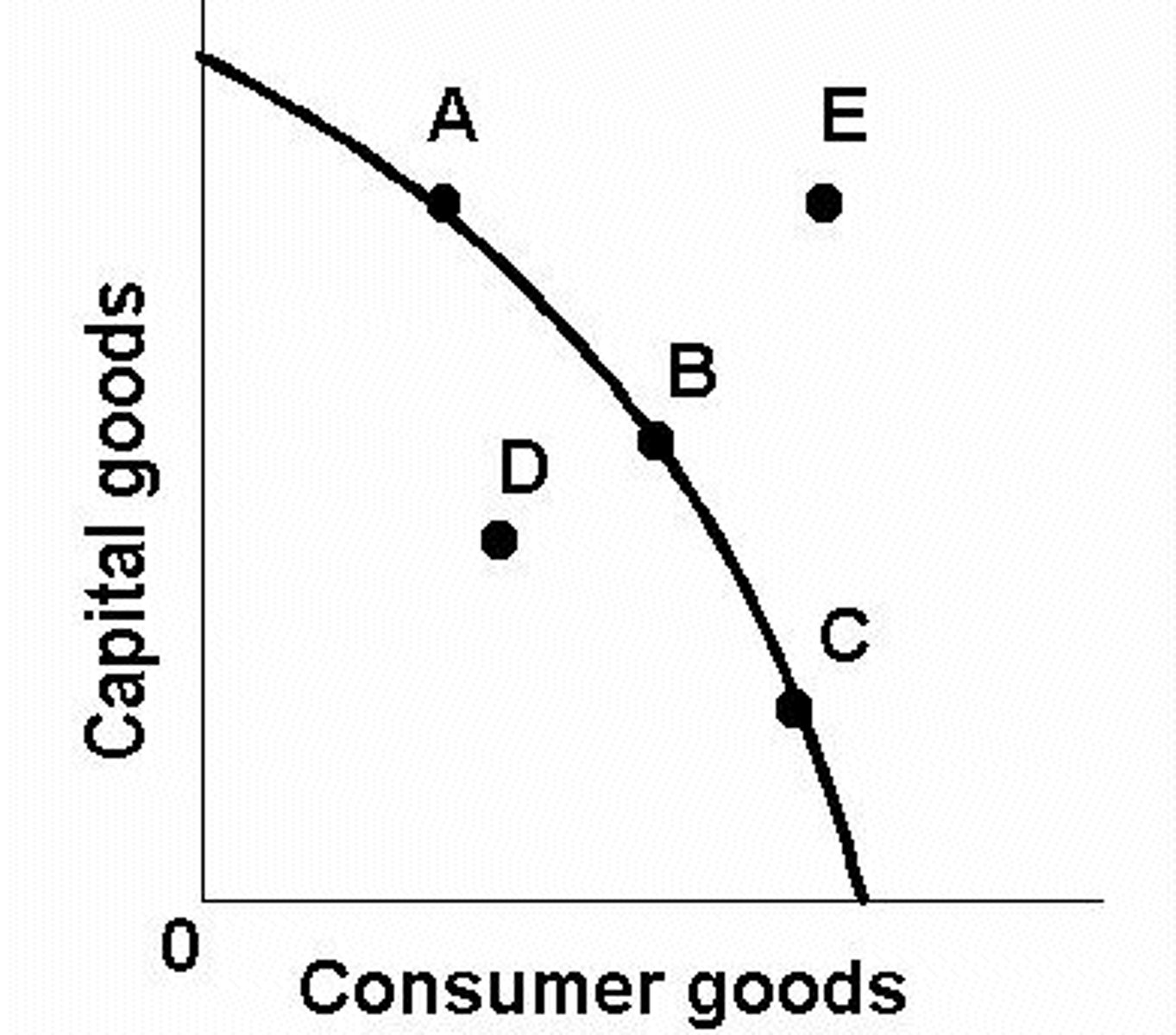

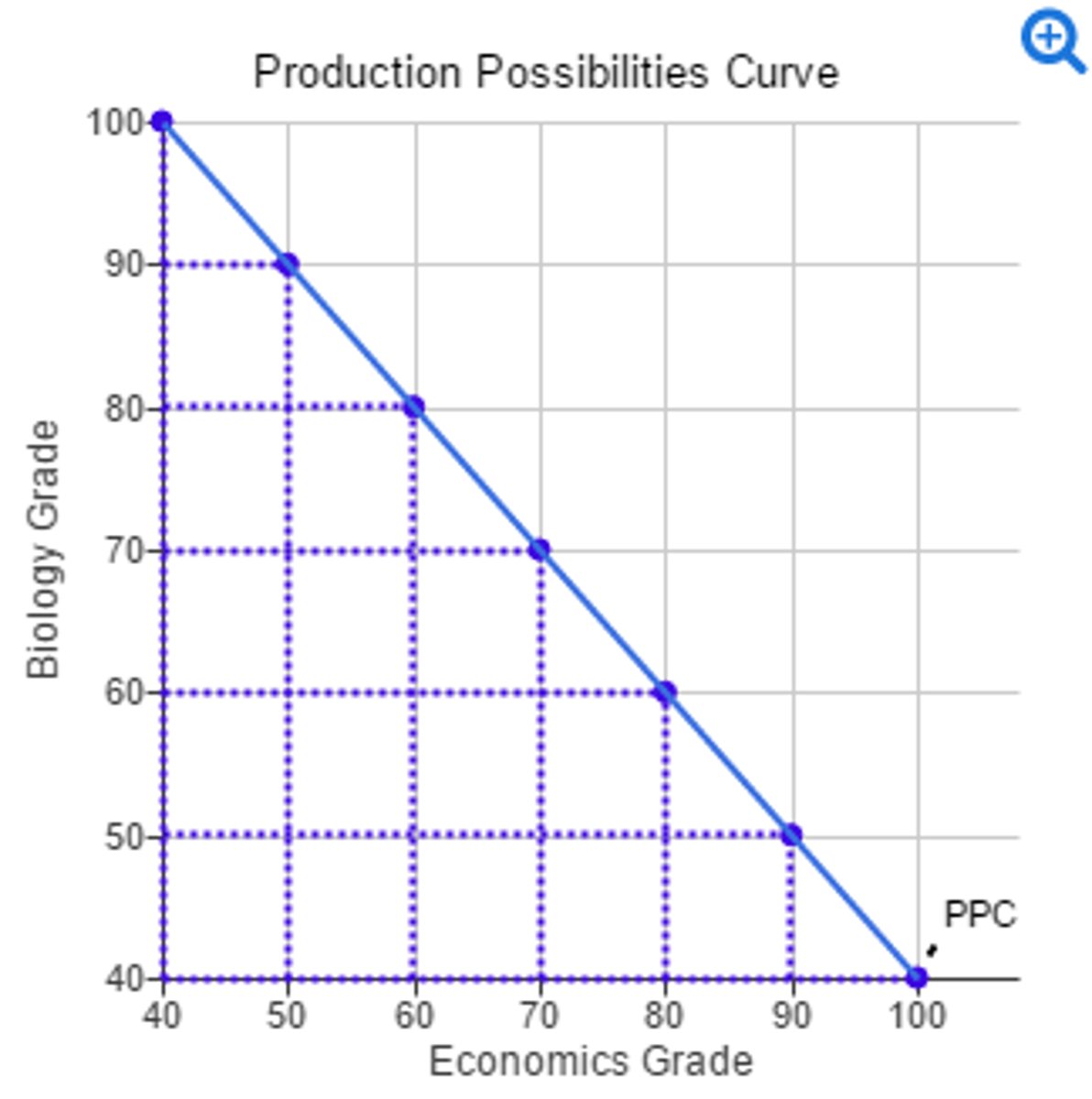

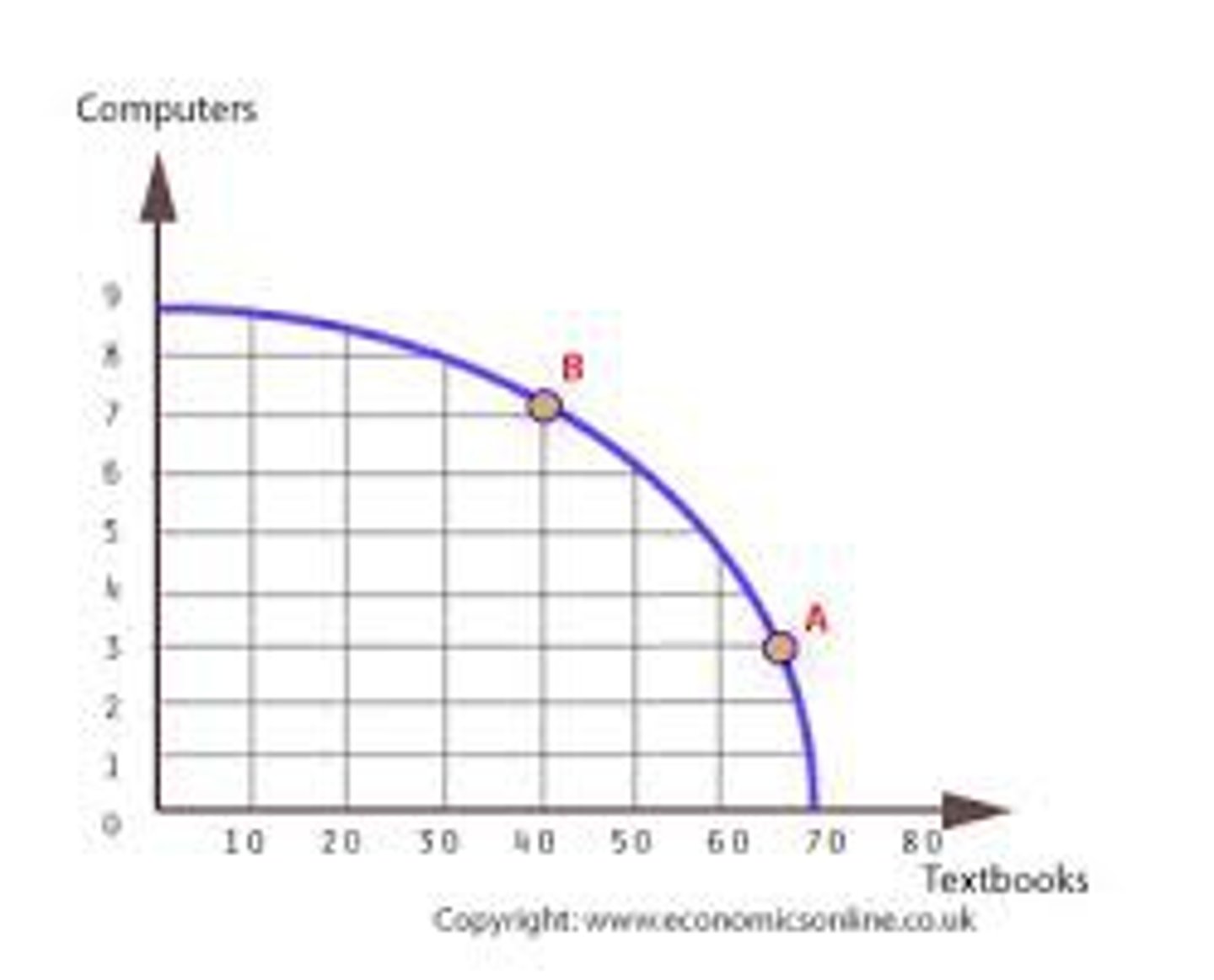

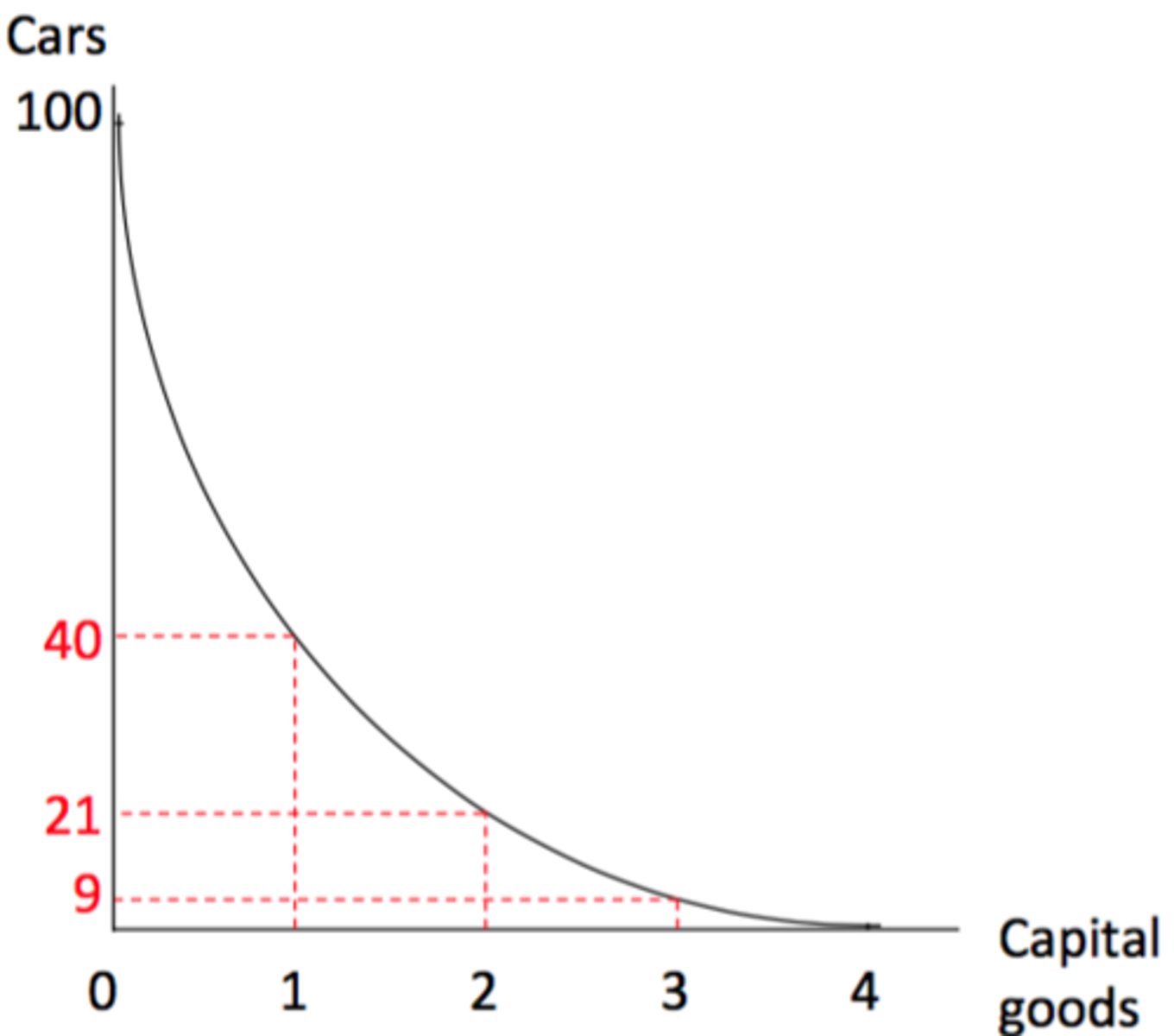

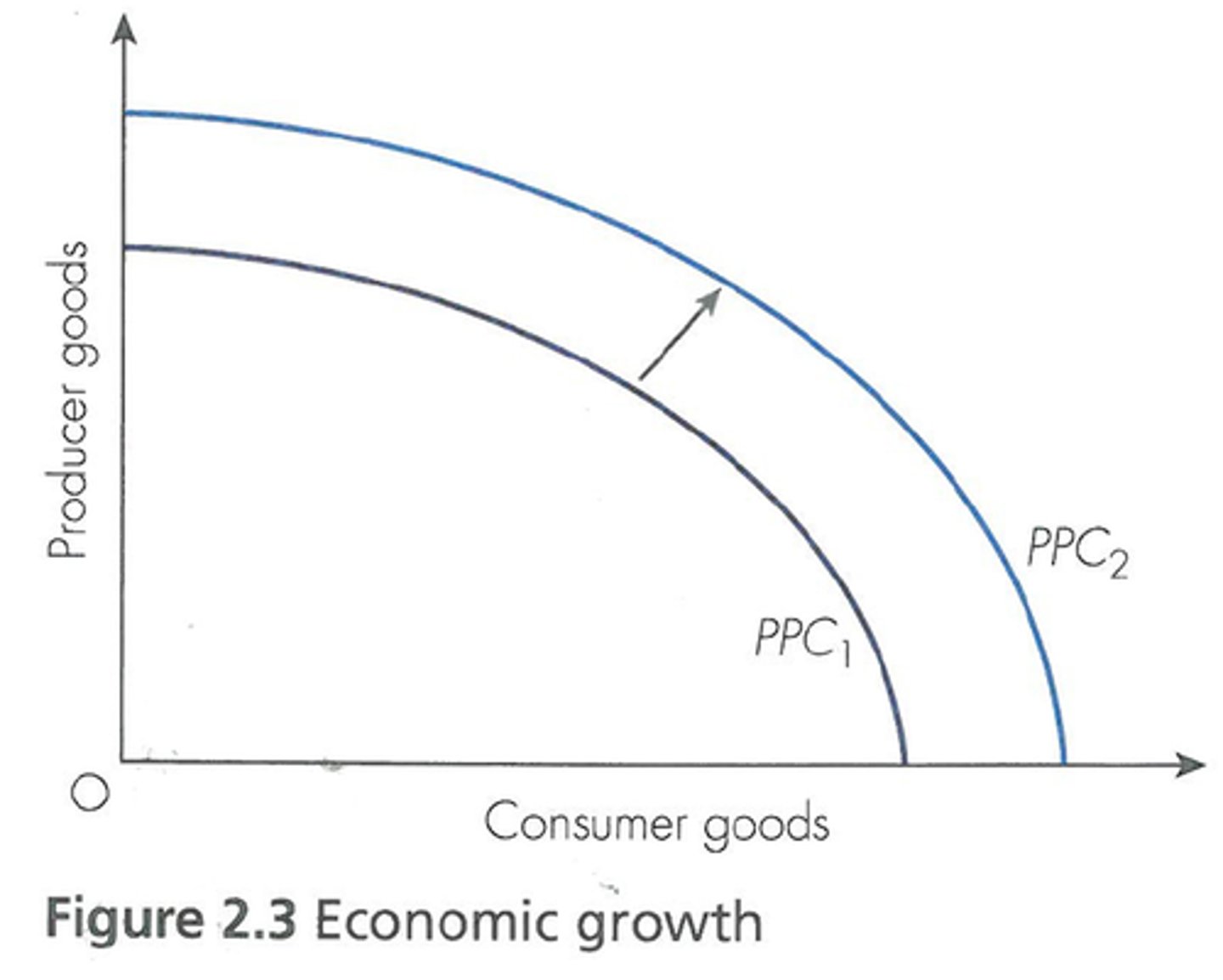

production possibilities curve

a graph that shows alternative ways to use an economy's productive resources

constant opportunity cost

Resources are easily adaptable for producing either good

increasing opportunity cost

the opportunity cost of producing additional units of a good rises as society produces more of that good

decreasing opportunity cost

having to give up an ever decreasing amount of one good to get additional units of another

Three shifters of the PPC

1. change in resource quantity or quality

2. change in technology

3. change in trade

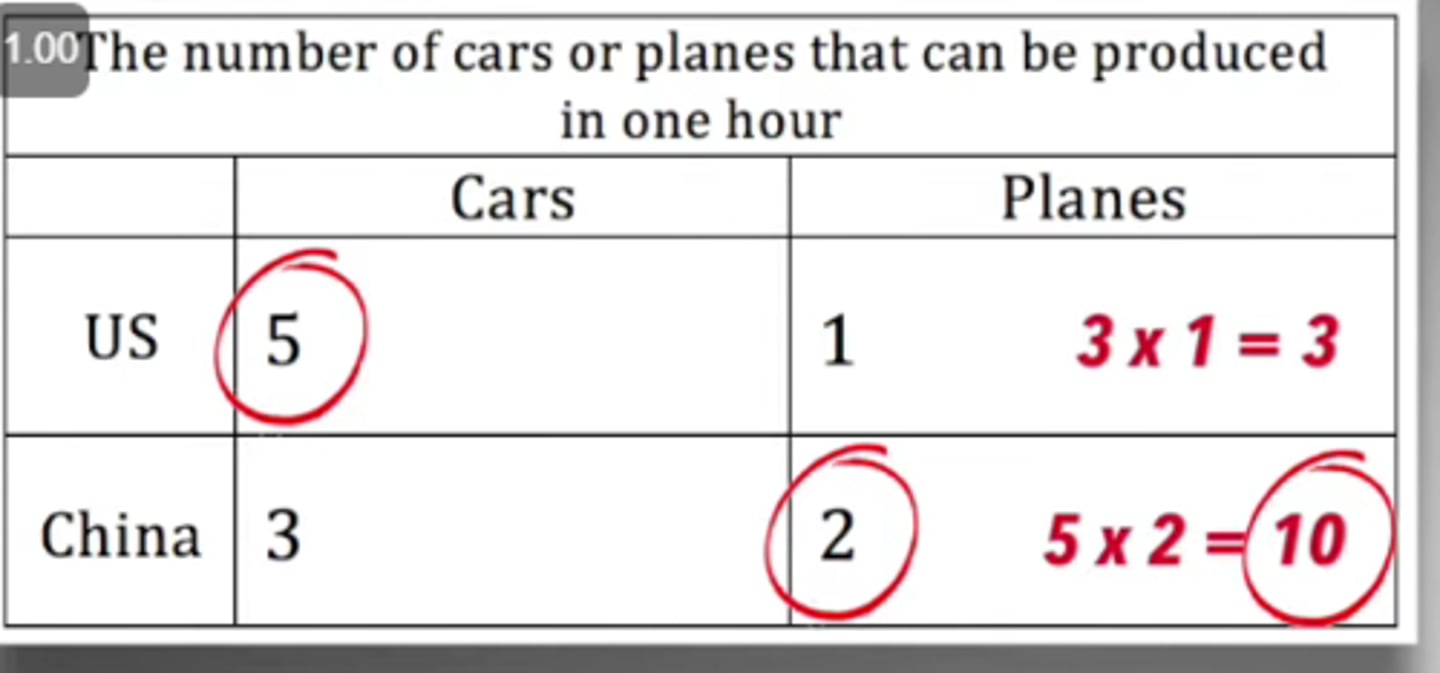

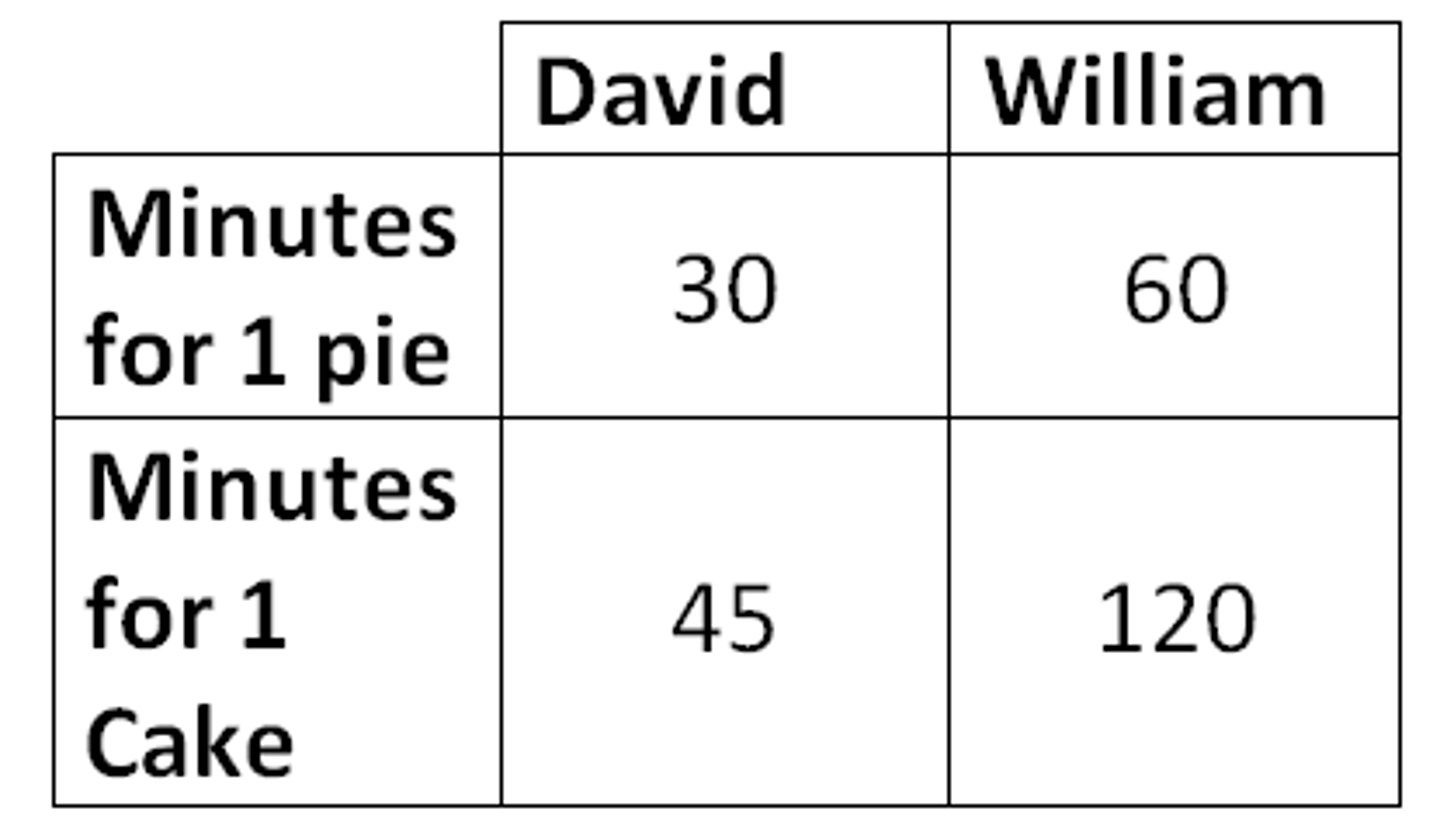

absolute advantage

the ability to produce a good using fewer inputs than another producer

comparative advantage

the ability to produce a good at a lower opportunity cost than another producer

terms of trade

the ratio at which a country can trade its exports for imports from other countries

output questions

OOO - Output: Other goes Over

input questions

IOU - Input: Other goes Under

explicit costs

The actual payments a firm makes to its factors of production and other suppliers.

implicit costs

Indirect, non-purchased, or opportunity costs of resources provided by the entrepreneur

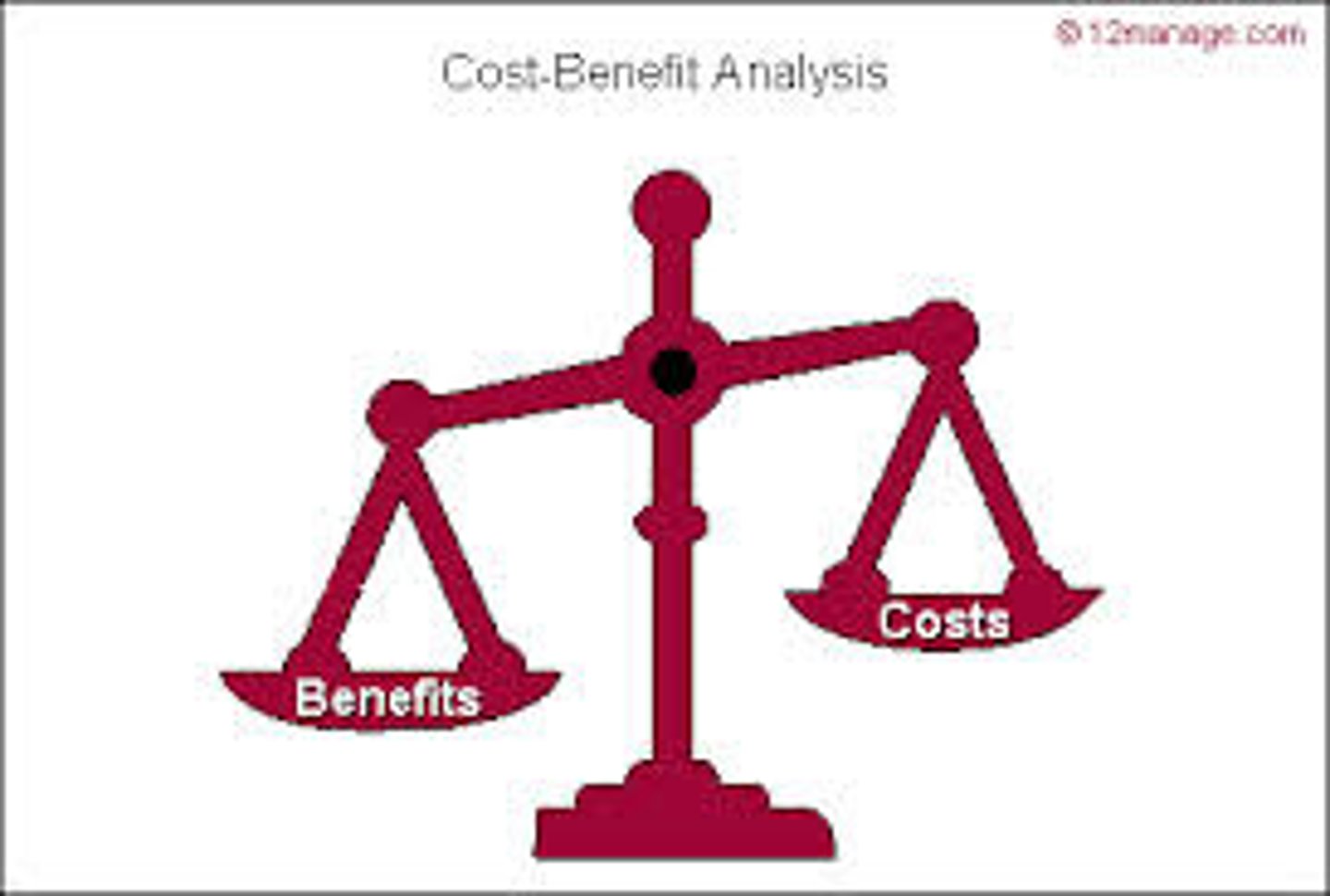

cost benefit analysis

a study that compares the costs and benefits to society of providing a public good

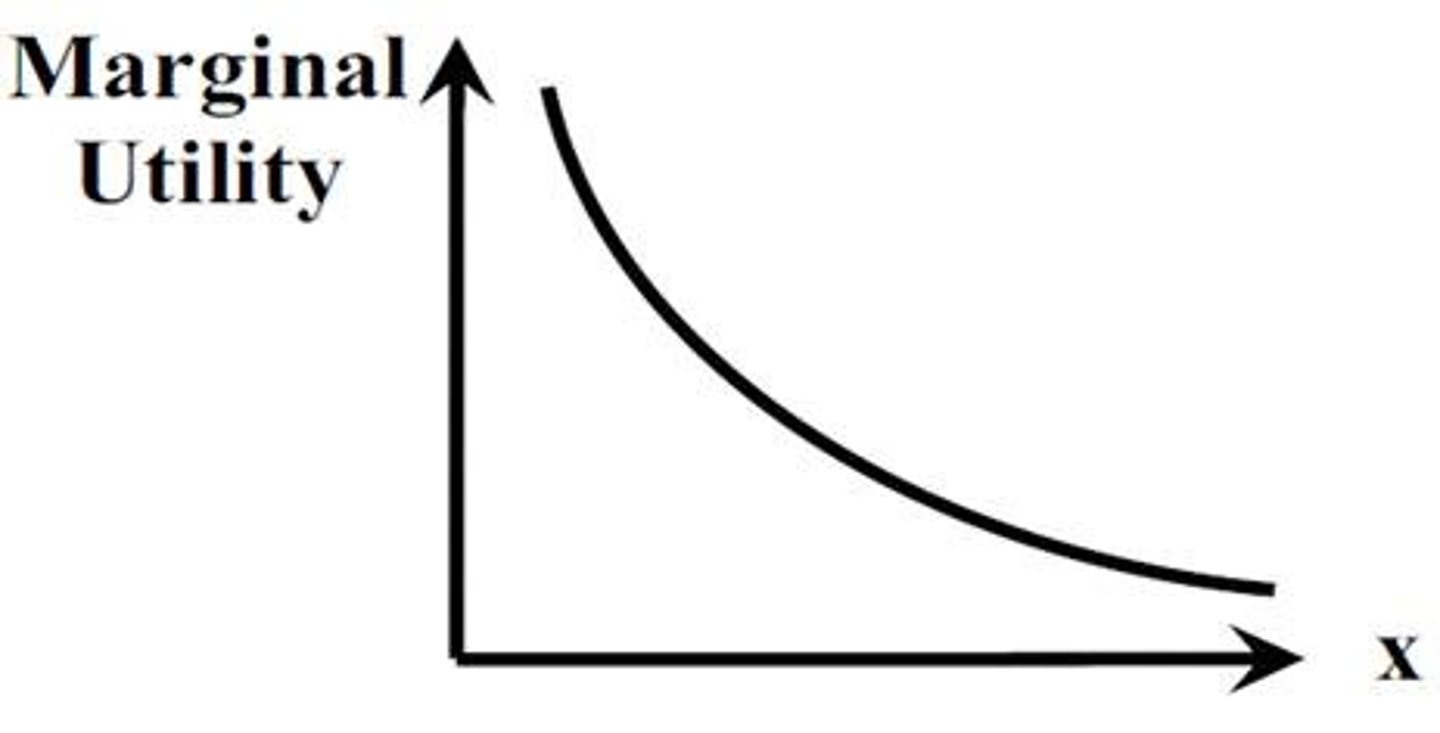

law of diminishing marginal utility

the principle that consumers experience diminishing additional satisfaction as they consume more of a good or service during a given period of time

marginal utility

an additional amount of satisfaction (Utility = Satisfaction)

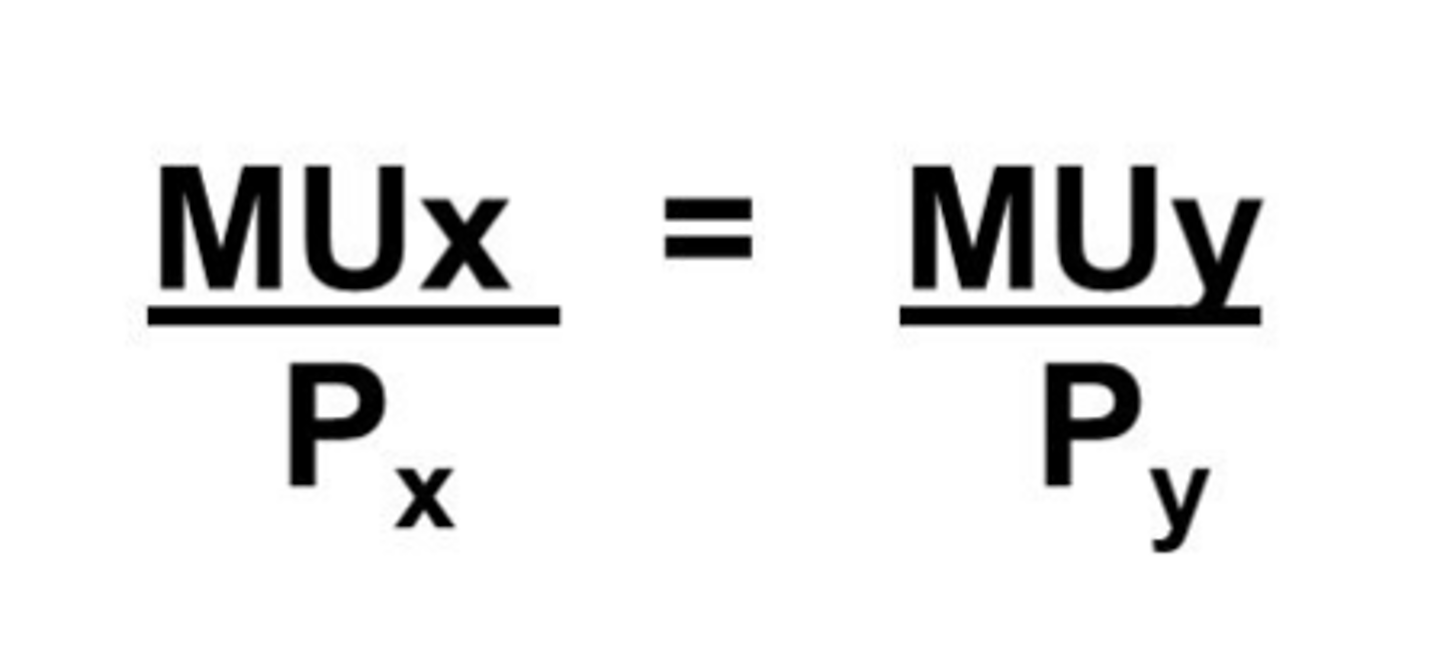

utility maximizing rule

The principle that to obtain the greatest utility, the consumer should allocate money income so that the last dollar spent on each good or service yields the same marginal utility.