chapter 5 - checking accounts, credit cores, and credit cards

1/37

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced |

|---|

No study sessions yet.

38 Terms

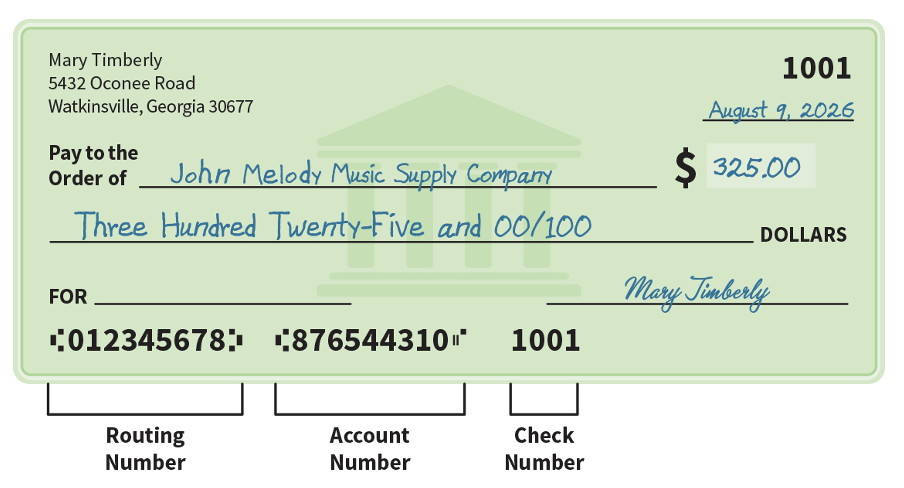

overview of checks (def, three elements)

A check is simply a written order to a bank to pay a third party (payee).

Three elements are required when you write a check:

The name of the person or company that gets the money (the payee).

The date.

The amount to be paid. The amount needs to be recorded both in numerical and written form.

It is possible to make a check payable to “Cash” instead of a person or company, but be aware that once you do this, anyone who comes into possession of the check can cash it.

form of checks

To link your checking account with online or other electronic payment tools, you’ll need to know your bank routing number and bank account number.

check alternatives

Check alternatives are rapidly being replaced by electronic payments, which are more secure.

Money order: A prepaid check purchased with cash from a bank, credit union, or convenience/grocery store.

Certified check: A personal check issued by a bank that guarantees the amount will be paid; the bank charges a fee for this type of check.

Cashier’s check: A check of a bank or other financial institution that can be purchased by paying the amount of the check plus a service fee.

Traveler’s check: A prepaid check purchased from a credit card company, bank, or credit union that must be signed before it can be cashed.

opening and using a checking account

Advantages of a Checking Account

Liquidity: Quick and easy way to access cash.

Direct deposit of paychecks: A way for an employer to transfer your earnings directly to your bank or credit union account.

FDIC insurance: Protection of all deposits up to at least $250,000 in case the bank or credit union fails.

Debit cards: Usually comes with a checking account

transaction methods used

Traditional methods

Cash, coins, and checks

Electronic payments

Debit cards and prepaid cards

Hybrid methods

Peer-to-peer payment (P2P)(Venmo, Cashapp), Cryptocurrency, and Automated Clearing House (A C H)

electronic payment methods

Debit Cards

Payment made directly from cardholder’s checking account using either a PIN or the cardholder’s signature to verify the transaction.

Prepaid Cards

Money loaded on a card in advance to be used to make payments in the future. Does not require a bank or checking account.

hybrid payment methods

Peer-to-peer payment (P2P)

Mobile apps such as: Apple Pay, Cash App, Venmo, and Zelle which allow you to transfer money electronically to people in your network.

Cryptocurrency

Digital money, meaning there is no physical coin or bill. Transactions between parties are recorded on a decentralized online ledger called a blockchain.

automated clearing house (ACH)

The Automated Clearing House (A C H) is a nationwide network of banks, credit unions, and other depository institutions that send each other credit and debit transfers electronically.

Make up a high percentage of payments made in the United States.

Credit transfers include wages, salaries, Social Security benefits, and tax refunds.

Debit transfers typically are payments for mortgages, utility bills, and credit card payments.

cryptocurrency

According to the IRS, cryptocurrency is a type of digital or virtual currency.

All currency is recorded and stored digitally.

Not issued by a government, therefore it can fluctuate dramatically in value.

Not insured by the FDIC.

Be very cautious and be aware of your risk tolerance when considering whether to purchase and type of cryptocurrency.

choosing the best payment method

Debit cards have insurance, fraud protection, and generally low or no fees.

Prepaid cards have limited loss liability (if financial institution goes out of business), unlimited loss liability (for fraud), and generally higher fees.

ACH is generally preferred by employers to pay wages and by lenders to schedule loan payments

when to borrow

There may be times when you won’t have enough money in your checking and savings accounts to make important purchases or pay for unexpected expenses.

The best protection against borrowing is to have an emergency fund — money set aside for expenses that have not been budgeted.

Without an emergency fund, you may need to borrow money by obtaining a loan if large expenses occur, such as paying for unexpected car repairs or college tuition.

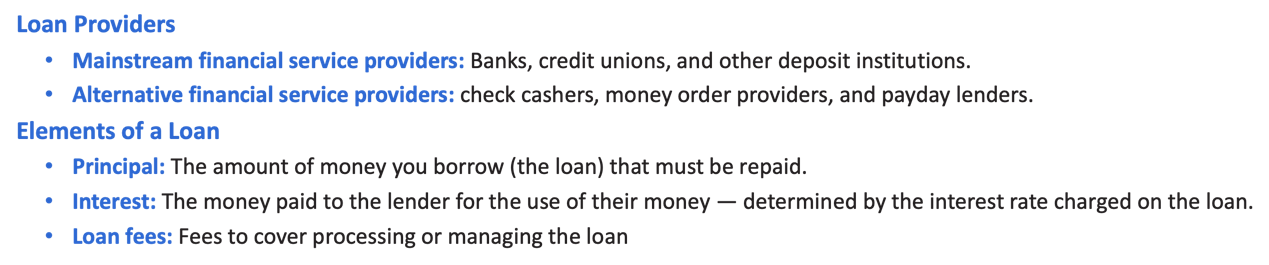

overview of loans (loan providers, elements of a loan)

Loan Providers

Mainstream financial service providers: Banks, credit unions, and other deposit institutions.

Alternative financial service providers: check cashers, money order providers, and payday lenders.

Elements of a Loan

Principal: The amount of money you borrow (the loan) that must be repaid.

Interest: The money paid to the lender for the use of their money — determined by the interest rate charged on the loan.

Loan fees: Fees to cover processing or managing the loan

collateral and finance charges

Collateral

Something of value that can be sold in the event that the loan payments are not made by the borrower. For example, a car or a house.

Finance Charges

The total amount of fees and interest charged by the lender for a loan.

choosing the right loan: fixed installment loans

Fixed Installment Loans

Lending contracts where the borrower agrees to repay the money through fixed monthly payments that will not change during the life of the loan.

The borrower gets all the money at once and repays over time.

The loan balance always decreases when payments are made until the loan is paid in full.

Common fixed installment loans include auto loans, education loans, and mortgages

choosing the right loan: variable installment loans

Variable Installment Loans

Structured so that the loan will be paid off within a certain time period; however, payments may fluctuate during the repayment period due to changes in the interest rate.

If the interest rate changes, then the payments due and interest charged will change each month.

The change in interest charged may increase or decrease the loan payments or length of the loan.

Example, Adjustable Rate Mortgages (A R M s)

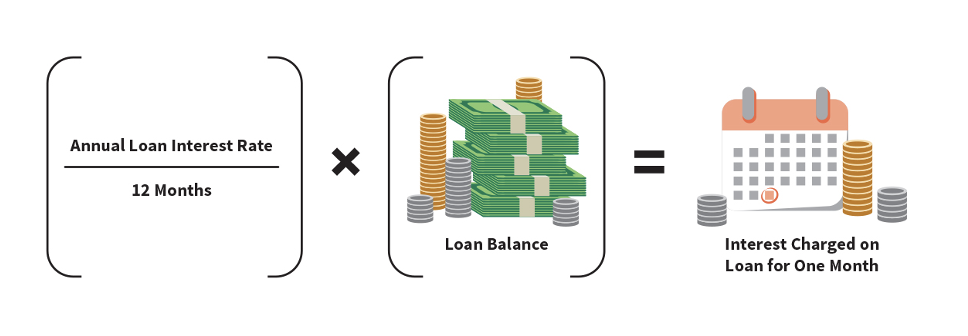

calculating interest

annual percentage rate (APR)

Finance charges can be difficult to compare across loans.

The annual percentage rate (APR) is a way to simplify comparison shopping for consumers (disclosure is required by the federal government).

A broad measure of the cost of borrowing — includes both the interest rate charged and any required fees for the loan.

dealing with debt collectors (FDCPA)

The Fair Debt Collection Practices Act (FDCPA) regulates the behavior of debt collectors.

Prohibits lenders and debt collectors from abusive, deceptive, and unfair debt collection practices

Debts owed to the government are generally excluded from protection under FDCPA

what is a credit report?

A credit report is a summarized accounting of your credit history.

How Credit Reports Are Used

A lender will request your credit report to determine creditworthiness when you apply for credit.

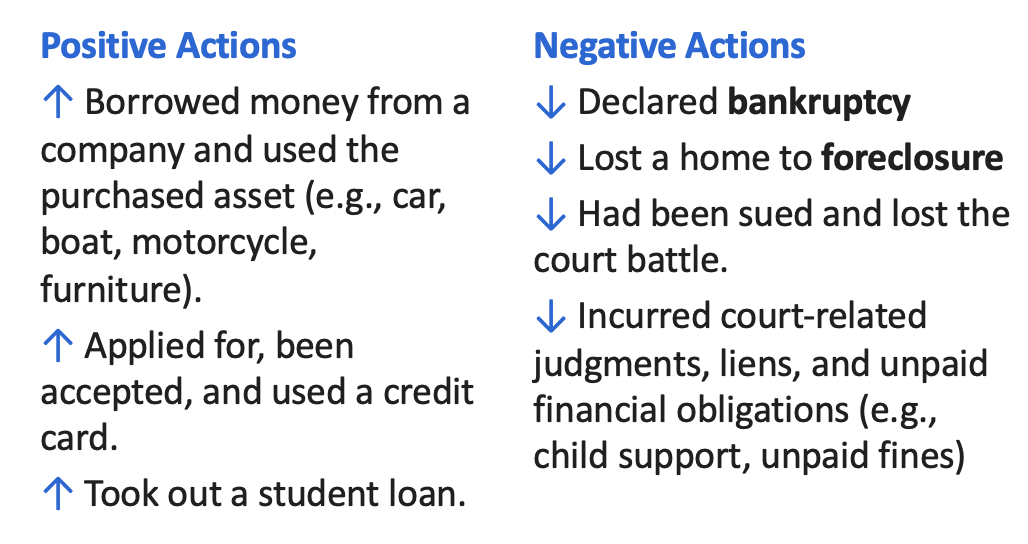

Credit Report Actions

A credit bureau is a company that maintains housing and credit files on consumers. There are three primary national credit bureaus: Equifax, TransUnion, and Experian.

Fair Isaac Corporation (FICO), the nation’s leading credit-scoring company.

credit report actions (positive and negative)

how credit reports are used

When a lender requests your credit report to determine creditworthiness, it is referred to as an inquiry.

The lender uses the report to determine the probability that you will make timely payments in the future.

Every 30 days or so, the lender will report information to the credit bureaus about your outstanding balance and payment timeliness.

contents and accessibility of a credit report

The information that goes into your credit report comes primarily from current creditors, which are firms that you have borrowed money from.

Additional information comes from credit applications that you submit and that contain employment information and addresses.

Other information comes from public legal records such as bankruptcy filings, court ordered liens, or court judgments

analyzing your credit report (FCRA)

The Fair Credit Reporting Act (F C R A) requires Equifax, Experian, and TransUnion to provide you with a free copy of your report once every 12 months.

You should request a copy just to make sure that everything in your report is accurate. Credit reports can have errors.

If you find an error on your credit report, you should contact the credit bureau to have the information corrected.

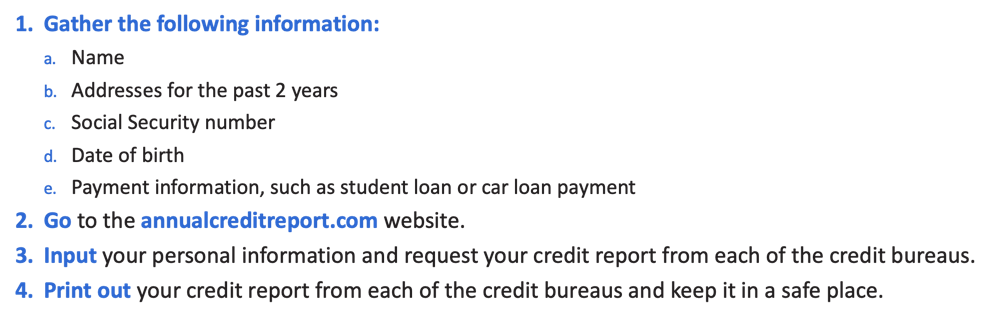

accessing your credit report

Gather the following information:

name

Addresses for the past 2 years

social Security number

date of birth

Payment information, such as student loan or car loan payment

Go to the annualcreditreport.com website.

Input your personal information and request your credit report from each of the credit bureaus.

Print out your credit report from each of the credit bureaus and keep it in a safe place.

identity theft

Identity theft occurs when someone else uses your personal information, such as your name and Social Security number, to obtain credit.

If you are the victim of identity theft or a credit scam:

Write to each of the credit bureaus directly, telling them that the information is inaccurate.

Write to the merchant(s) and dispute any items purchased that you did not buy.

If these actions do not work, contact the Federal Trade Commission and your state Attorney General’s office.

You can also report the crime to local law enforcement

the purpose of credit scores

The information within a credit report is analyzed and then reduced into a number - known as a credit score.

A credit score is merely a tally that summarizes a person’s credit risk.

A bad credit risk is someone who has a history of not paying bills on time or not repaying their loans.

developing credit scores

Within the financial world, credit scores are used to predict which people are likely to manage their debt wisely in the future.

The most widely used credit score was created by Fair Isaac Corporation, referred to as a FICO® score.

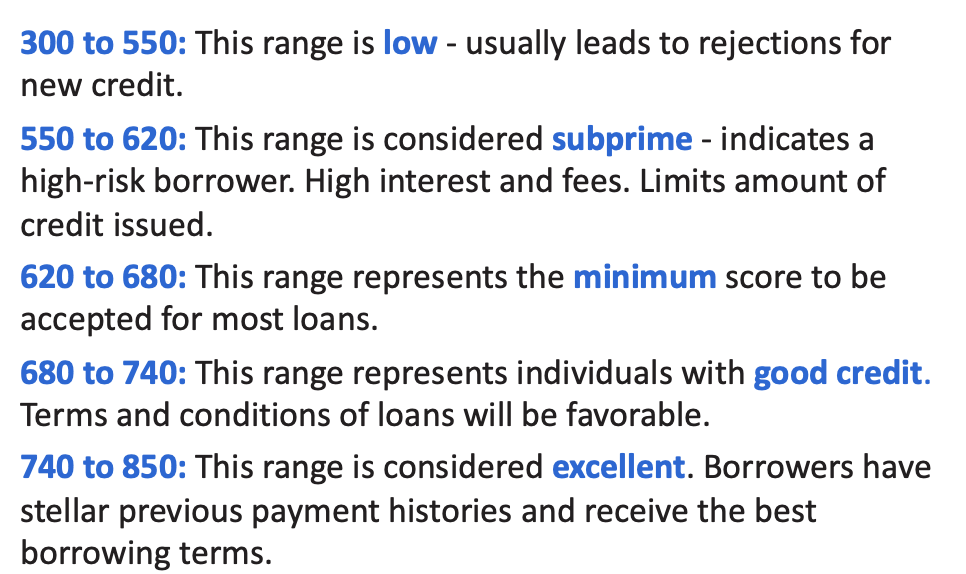

FICO scores can range from a low of 300 to a high of 850.

Higher credit score = lower credit risk

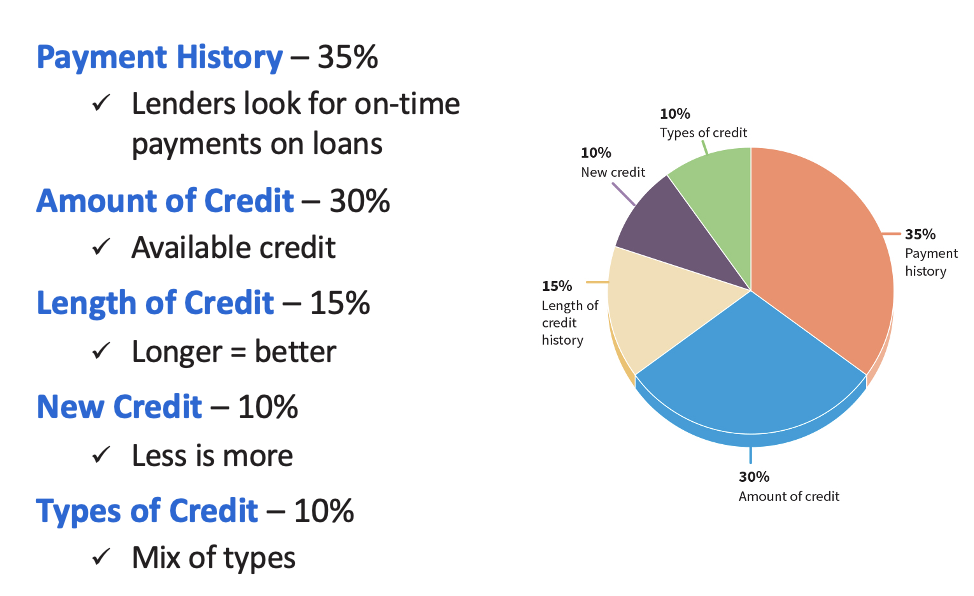

how FICO scores are calculated

credit score ranges

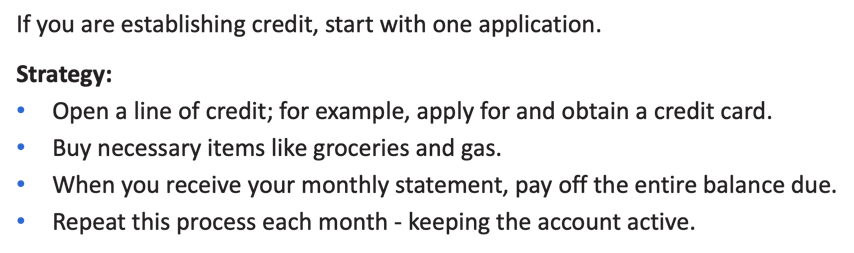

building a favorable credit score

If you are establishing credit, start with one application.

Strategy:

Open a line of credit; for example, apply for and obtain a credit card.

Buy necessary items like groceries and gas.

When you receive your monthly statement, pay off the entire balance due.

Repeat this process each month - keeping the account active.

how credit scores are used and updated

Your credit score is regularly updated based on your most recent credit report. A change in any of these items will result in an update to your report.

Personal information: Name, date of birth, social security number, and address)

Summary of accounts: All open credit

Inquiries: List of all lenders who have looked at your credit over the past 2 years

Negative Items: Summary of missed payments, overdue notices, and any public record information

optimizing your credit score

Try never to miss a payment. If you do miss one, get and stay current as quickly as possible.

Basic rules to optimize your credit score:

Keep revolving debt balances low

Apply the ratio rule

Credit Usage Ratio

Avoid applying for lots of new credit cards at one time

Vary your credit mix

bankruptcy

Bankruptcy is the legal process that allows a person who owes money to others to either repay the money over time or have the entire debt discharged.

Effectively freezes the ability of creditors to harass a debtor or seek payment outside of the bankruptcy process

Chapter 7 bankruptcy allows a debtor’s liabilities to be fully discharged

Chapter 13 bankruptcy places the debtor on a debt repayment plan

characteristics of credit cards

A credit card is a loan that can be used at the borrower’s discretion and convenience and has flexible repayment options.

Generally essential when renting cars, reserving hotel rooms, or booking airline and other travel tickets.

Responsible use of credit cards can also help build your credit score making it easier to qualify for other loans, such as auto loans and mortgages.

qualifying for a credit card

For many individuals, a credit card is the easiest way to establish or re-establish credit history.

Ironically, many individuals are not able to qualify for a credit card because they lack sufficient credit histories and therefore do not have a credit score.

Some credit card issuers have special student credit cards that are easier to obtain. Otherwise, adding a co-signer or obtaining a secured credit card are options

adding a co-signer

A co-signer is an individual, in addition to the borrower, who will be held responsible for repayment of the debt.

obtaining a secured credit card

There is another way to obtain a credit card. Banks and credit unions offer secured credit cards:

Provides a way to establish credit without a co-signer.

Requires the borrower to deposit the full amount of the line of credit at the bank as collateral before the credit card is issued.

know your rights

The Credit Card Accountability Responsibility and Disclosure Act was passed by Congress in 2009

Protects consumers from unfair and deceptive practices in the credit card industry

Leveled the field between credit card companies and credit card account holders