North Carolina Life Insurance Exam

1/142

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

143 Terms

Adverse Selection

the insuring of risks that are more prone to losses than the average risk

Agent/Producer

a legal representative of an insurance company; the classification of producer usually includes agents and brokers; agents are the agents of the insurer

Applicant or proposed insured

a person applying for insurance

Attained Age

the insured’s age at the time the policy is issued or renewed

Beneficiary

a person who receives the benefits of an insurance policy

Cash Value

a policy’s savings element or living benefit

Death Benefit

the amount paid upon the death of the insured in a life insurance policy

Lump-Sum distribution to beneficiary and Principal are TAX FREE

Interest is taxable if paid in installments (not lump-sum)

Deferred

withheld or postponed until a specified time or event in the future

Endow

to have cash value of a whole life policy reach the contractual face amount (ex. whole life insurance endows at age 100, so the cash value of all premium payments will sum to equal the face amount at that age)

Face Amount

the amount of benefit stated in the life insurance policy

Insured

person covered by the insurance policy; may or may not be the policyowner

Insurer(Principal)

the company that issues an insurance policy

Lapse

Policy termination due to nonpayment of premium

Level Premium

the premium that does not change through the life of a policy

Nonforfeiture Values

benefits in a life insurance policy that the policyowner cannot lose even if the policy is surrendered or lapses

Policyowner

the person entitled to exercise the rights and privileges in the policy

Policy Maturity

in life policies, the time when the face value is paid out

Premium

the money paid to the insurance company for the insurance policy

NOT TAX DEDUCTIBLE

Securities

financial instruments that may trade for value (ex. stocks, bonds)

Permanent Life Insurance

refers to various forms of life insurance policies that build cash value and remain in effect for the entire life of the insured (or until age 100) as long as the premium is paid.

Whole Life Insurance

Key Characteristics:

Level Premium based on issue age

Death Benefit is guaranteed & remains level

Cash value (AKA nonforfeiture value) = face value at 100 y/o, and are credited to the policy regularly with guaranteed interest rate. Does not usually accumulate until the third policy year and grows tax deferred

Living Benefits allow policy owner to borrow against the cash value (aka nonforfeiture value) while policy is in effect or can receive cash value if policy is surrendered

3 Main types: Straight, limited pay, single premium

provides lifetime protection, and includes a savings element (or cash value). Endow at age 100. Policy premium calculated assuming that the policy owner will be paying until age 100 and are usually higher than term insurance.

Straight (Ordinary/Continuous Premium) Whole Life Insurance

The basic whole life policy. Policyowner pays premium from the time the policy is issued until the insured’s death or age 100. Has the lowest annual premium of the whole life policies. Cash Value increases overtime, premium stays constant

Limited-Pay Whole life

Designed so that premiums are all paid before age 100. Short premium-paying period, so higher annual premium than straight life. Cash Value builds up faster than straight life. Ideal for individuals who do not want to pay premiums after a certain point in time

Types: 20-pay life (all premiums paid within 20 years), life paid-up at 65(all premiums paid by age 65)

Single Premium Whole Life

provide a level death benefit to insured’s age 100 with a one-time, lump-sum premium payment. Cash Value is immediately generated and grows over time

Indexed (AKA Equity Index) Whole Life

Cash Value dependent on performance of an equity index (ex. S&P 500). Guaranteed minimum interest rate. Face amount increases annually to adjust for inflation w/o requiring evidence of insurability.

If policyowner assumes the risk, premium increase with increasing face amount. If Insurer assumes the risk, premium stays constant.

Modified Whole Life

Charges a lower premium (similar to term rates) in the first few years, then premium increases for remainder of insured’s life. Higher premium usually higher than straight life for equal age and coverage. Intend to help people with limited finances short-term

Graded-Premium Whole Life

Premiums start low then increase to a level point in the future. Starts with premium 50% lower than that of straight life. Then, premium gradually increases each year for ~5-10 years, then levels off.

Indeterminate Premium Whole Life

premium varies yearly, two rates; guaranteed level premium (maximum premium) or nonguaranteed lower premium. Premiums paid for set period and then new rates are established based on expected company mortality, expenses, and investments. Can never exceed the maximum

Interest-sensitive (Current Assumption) Whole Life

Guaranteed death benefit to age 100. Premium based on current assumptions abt risk, interest, and expense. If actual values are different, company will change premium. Credit Cash value with the current interest rate that can be higher than guaranteed levels. Guaranteed minimum interest rate.

Same benefits as other traditional whole life policies with added benefit of current interest rates, which can increase cash value accumulation or decrease premium-paying period

Endowment Whole Life

Same features of regular whole life policies just with earlier maturity date. Permanent, level death protection if insured dies prematurely, accumulates cash values, premiums can be paid up to endowment date or in lump-sum. Intended to be used while the insurer is alive. Premiums considerably higher than straight life. the shorter the premium period, the higher the premium

Flexible Premium Policies

Allows policyowner to pay more or less than the planned premium

Adjustable (Term/Whole) Life

Intended to combine term and permanent coverage. Insured determines how much coverage is needed and affordable premium. Insurer determines appropriate type of insurance. As insured’s needs change, policyowner can make adjustments (increase/decrease premium, increase/decrease premium-paying period, increase/decrease face amount, or change period of protection) to the policy.

Can be converted from term to whole life or vice versa. Increasing death benefit or decreasing premium usually requires proof of insurability. Cash value only develops when premiums paid > cost of the policy

Universal Life (Flexible Premium Adjustable Life)

policyowner can increase premium, later decrease, or skip premium. Cash value must cover monthly cost of insurance to skip premium payments, otherwise policy will lapse.

Policyowner may have minimum and target premiums. Minimum keeps policy in force for current year and behaves like an annually renewable term product. Target is recommended to cover cost of insurance protection and keep policy in force throughout its lifetime

interest-sensitive, guaranteed contract interest rate or nonguaranteed current market interest rate (whichever is higher)

Two components: Annually renewable term insurance and cash account.

Partial withdrawal(Surrender) of cash value is allowed. There may be associated withdrawal limits, charges, and frequency. Interest earned on the withdrawn cash value may be subject to taxation. Death benefit reduces by the withdrawn amount. NOT A POLICY LOAN

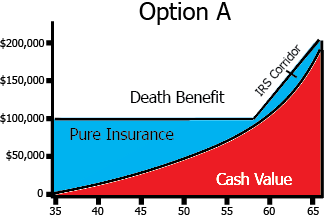

Universal Life Option A

Level death benefit

Cash Value gradually increases, lowering pure insurance in later years

Required corridor between cash value and death benefit to be considered life insurance

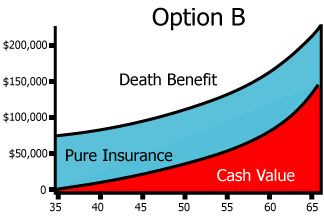

Universal Life Option B

Increasing Death Benefit

Cash Value increases annually and is included in the death benefit, meaning the death benefit increases annually. Total death benefit always = face amount + current amount of cash value

Pure insurance remains level for life, expenses are much higher than the other option.

Cash value lowers in the older years (all else equal)

Fixed Life Insurance or Annuities

contracts that offer guaranteed minimum or fixed benefits that are stated in the contract

Variable Life Insurance or Annuities

Contacts where cash values accumulate based on a portfolio of stocks WITHOUT guarantees of performance.

Keep pace with inflation and are determined by securities backing it

Variable Whole Life Insurance

investment-based

level, fixed premium with guaranteed minimum death benefit.

Cash value is NOT guaranteed & fluctuates with portfolio

Premiums are invested by the INSURER

Policyowner specifies where cash value should be invested and bears investment risk

Assets in a separate account (NOT in insurance general account) that acts as a mutual fund(unit trust)

Variable Universal Whole Life

Flexible premium

increasing/decreasing amount of insurance

Cash withdrawals & Policy Loans

Return not guaranteed compared to Universal Life

Regulation of Variable Products

SEC, FINRA, State & Federal Governments

Agents must be registered with FINRA; be licensed by the state to sell life insurance; and have received a securities license

Family Protection Policy

Combination of Whole Life and Term insurance to cover family members in one policy

Breadwinner covered under whole life

Spouse and dependents under convertible term insurance which can be converted to permanent coverage between 21 and max dependent age or before 65 years old for the spouse WITHOUT evidence of insurability

Family Income Policy

Combination of decreasing term insurance and whole life insurance on family breadwinner

Income period funded with decreasing term; term covers surviving family with income payments for the remaining period should breadwinner die during income period.

At the end of income period, face amount of the whole life coverage has been paid to the beneficiary

If insured dies after income period, only whole life portion will be paid to the beneficiary

Joint Whole Life

Insures two or more lives; can be spouses or business partners

can be in the form of term or permanent insurance

premium for joint life is less than separate premiums for each person

premium is based on joint average age

death benefit paid upon first death only

Survivorship Whole Life (Second to Die)

Insures two or more lives

premium based on average age

pays on the last death

lower premium than Joint Whole Life

Often used to offset the liability of estate tax

Jumping Juvenile Life

life insurance written on the life of a minor

Face amount increases at a predetermined age (often 21)

Face amount “jumps” premium remains constant

Double or Triple (Multiple) Protection

Combine permanent and level term insurance

pay double or triple the face amount if insured dies during specified period

If insured dies after the period, policy only pays face amount

Term Riders

allow for an additional amount of temporary insurance without needing to issue another policy

Typically attached to whole life to provide more protection at reduced cost

Limited Benefit

cover certain expenses from specifically namd illnesses, injuries, or circumstances

IRS

Internal Revenue Service: a US government agency responsible for collecting taxes and enforcing Internal Revenue Code

Life Contingency

dependent upon whether or not the insured is alive

Liquidation of an estate

converting a person’s net worth into a cash flow

Natural Person

a human being

Qualified Plan

a retirement plan that meets the IRS guidelines for receiving favorable tax treatment

Suitability

a requirement to determine if an insurance product or an investment is appropriate for a particular customer

Annuity

contract that provides income for a specified period of years, or for life

protects individuals against outliving their money main use is for retirement income or education expenses

NOT life insurance

Vehicle for the accumulation of money and liquidation of an estate

Do not pay face amount upon death of annuitant; payments stop upon death

Uses mortality tables with longer life expectancy than life insurance

Mortality Table

inddicates the number of individuals within a specified group starting at a certain age, who are expected to be alive at a succeeding age (e.g. males, females, smokers, nonsmokers, etc)

Annuity Owner

purchaser of the annuity contract but not necessarily the one who receives the benefits

has all of the rights to name beneficiary and to surrender the annuity

May be a corporation, trust, or other legal entity

Annuitant

the NATURAL PERSON who receives benefits from an annuity

life expectancy taken into consideration

annuity is written for this person

Beneficiary

the person who receives annuity assets (amount paid in or cash value; whichever is greater) if the annuitant dies during the accumulation period

Accumulation Period AKA Pay-in period

period of time over which the owner makes payments (premiums) into an annuity. Payments earn interest on a tax-deferred basis

Annuity Period AKA Annuitization Period, Liquidation Period, or Pay-Out Period

time when the accumulated sum is converted into income payments to the annuitant. Can last for the lifetime of the annuitant or for a specified period

Annuity Income

based on cash value accumulated, frequency of payment, interest rate, and annuitants age & gender

shorter life expectancy = higher benefit

longer life expectancy = lower benefit

Beneficiary receives cash value or total premiums paid (whichever is greater) if annuitant dies during accumulation period

Premium Payment Annuity Options

Single Premium: one, lump-sum payment

Periodic Premium: premium paid in installments over a period of time

Can be level premium or flexible premium

Immediate vs Deferred Annuities

Immediate: purchased with single, lump-sum payment and provides income payments within one year from purchase date. Can be as early as one month

Deferred: income payments begin after one year, can be lump-sum or periodic payments.

The longer it is deferred, more flexible payment premiums

Nonforfeiture

Deferred Annuity must have a guaranteed surrender value that is available. 10% penalty applied to withdrawals before 59.5 y/o

Surrender Charges

Compensates company for loss of investment value due to early surrender; typically decreases over time

Fixed Annuity

-Guaranteed minimum rate of interest or the current interest rate (whichever is higher)

-Income payments that do not vary from one payment to the next (Level benefit payment amount)

-Guaranteed specified dollar amount for each payment and length of period of payments

-Do not adjust for inflation

-Premiums are placed in company’s general account

-Insurer bears the investment risk

(Equity) Indexed Annuities

Fixed annuity that is tied to an index like the S&P 500

Company keeps some of interest earned but excess interest is credited to account

Less risky than variable annuity or mutual fund and typically higher interest rate than fixed annuity

Variable Annuity

Considered a security; regulated by SEC and State Insurance Regulations

No guaranteed minimum interest rate

payments are invested into insurer’s separate account NOT general account

Agent/Company must be registered with FINRA and have securities license

Pure Life (Life-only or Straight Life) Annuity

Payment stops at annuitants death

highest monthly benefits

no guarantee that entire principal will be paid out

Life with Guaranteed Minimum (Refund Life) Settlement

Principal will be refunded to beneficiary if annuitant dies before principal amount has been paid out. Guarantees entire principal will be paid out. Benefits subject to taxation when paid to beneficiary

Cash Refund: lump-sum payment of principal-benefit payments made to annuitant. Does not guarantee interest

Installment Refund: beneficiary receives guaranteed installments until principal has been paid

Life with period (term) certain

Annuity payments guaranteed for lifetime of annuitant and for a specified period for beneficiary.

Joint Life Annuity

two or more annuitants receive payments until the first death among the annuitants

Joint and Survivor

guarantees an income for two recipients that neither can outlive. Typically survivor receives reduced payment.

No guarantee that all proceeds will be paid out if both beneficiaries die

Lump-Sum Annuity

Paid at annuitization; all interest accumulated is taxable; 10% penalty for withdrawal before 59.5 y/o

Annuities Certain

Payment guaranteed for fixed period or until certain fixed amount paid. NO life option

Activities of Daily Living

a person’s essential activities that include bathing, dressing, eating, transferring, toileting, continence

Contingent Beneficiary

beneficiary who has second claim to the policy proceeds after the death of the insured (usually after the death of primary beneficiary)

Principal Amount

face value of the policy; original amount invested before earnings

Entire Contract

Policy + Copy of application + any riders or amendments

Insuring Clause (Insuring Agreement)

agreement between the insurer and the insured promising to pay the death benefit upon the insured’s death. Defines who the parties are, how long coverage lasts, and type of loss insured against

Free Look

policyowner has 10 days from receiving the policy from the agent to look over policy and return it for a full premium refund

Owners rights

Only policyowner has rights under the policy and are responsible for paying the premiums and must have an insurable interest in the insured. They can name/change the beneficiary, receive living benefits, select benefit payment options, and assign the policy

Absolute Assignment

transferring all rights of ownership to another person or entity. Permanent and total transfer of all the policy rights. New policyowner does not need to have an insurable interest in the insured

Collateral Assignment

transfer of partial rights to another person. Usually done in order to secure a loan or some other transaction. temporary assignment of some policy rights until debt is repaid

No named beneficiary

policy proceeds go to the insured’s estate

Revocable vs Irrevocable Beneficiaries

Revocable can be removed by policyowner at any time

Irrevocable can only be changed with the consent of the beneficiary. Owner cannot borrow against the policy’s cash value or assign policy to another person without beneficiary’s consent

Changing the Beneficiary: recording or filing method

policyowner completes a form with the change and submits it to the insurance company

Changing the Beneficiary: Endorsement Method

policy owner is required to send the request for change with the contract to the home office of the insurer. Home office will have to approve and make the change

Uniform Simultaneous Death Law

if policy owner and beneficiary die at the same time with no indication of who died first, the policy will be distributed as if the beneficiary died first and will go to the contingent beneficiary

Common Disaster Clause

Protects Contingent Beneficiary

If insured and primary beneficiary died in a common disaster, the policy will be distributed as if the beneficiary died first and will go to the contingent beneficiary or estate. Primary beneficiary must die within 14-30 days from the insured for this to be utilized

Net Premium

Mortality-Interest

Gross Premium

Net Premium (AKA Mortality-Interest) + Expense(AKA loading)

Grace Period

period of time after the premium due date that the policyowner has to pay the premium before the policy lapses (usually a month)

Misstatement of age or Gender on Application

results in adjustment of premiums or benefits

Reinstatement Provision

a lapsed policy can be put back in force if all premiums, interest, and outstanding loans and reinstated within a specified maximum time limit with evidence of insurability. Policy will be restored to original status and the insured’s issue age. Does not apply to surrendered policies

Incontestability Clause

If policy has been in force for at least 2 years, insurer cannot deny a claim based on misstatements on application. Does not apply to nonpayment, statements relating to age, sex, or identity

Conversion and Change of Plan

changing to a higher premium plan does NOT require proof of insurability

changing to a lower premium plan REQUIRES proof of insurability

Days of written notice required to tell policyowner that policy is going to lapse

30

Policy Loans

ONLY available in policies with cash value (whole life)