Lvl2: Equity

1/53

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai | Chat |

|---|

No analytics yet

Send a link to your students to track their progress

54 Terms

rational efficient markets formulation

investors will not rationally incur the expenses of gathering information unless they expect to be rewarded by higher gross returns compared with the free alternative of accepting the market price

difference between a valuation estimate and the prevailing market price

true mispricing - true but unobservable intrinsic value V and the observed market price P

error in the estimate of the intrinsic value - valuation estimate and the true but unobservable intrinsic value

valuation process

Understanding the business. Industry and competitive analysis, FS analysis

Forecasting performance

Selecting appropriate model

converting forecasts to valuation

applying conclusions - investment recommendation

sum-of-the-parts valuation

sometimes called the breakup value or private market value

segments in different industries that have different valuation characteristics

DDM is suitable when

dividend-paying

board of directors has established a dividend policy that bears an understandable and consistent relationship to the company’s profitability

investor takes a non-control perspective

FCFE /FCFF model suitable when

not dividend-paying

dividends significantly exceed or fall short of free cash flow to equity

free cash flows align with the company’s profitability

control perspective

residual model

book value per share plus the present value of expected future residual earnings.

residual model suitable when

not paying dividends

expected free cash flows are negative

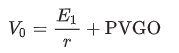

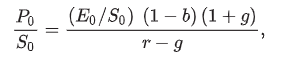

present value of growth opportunities

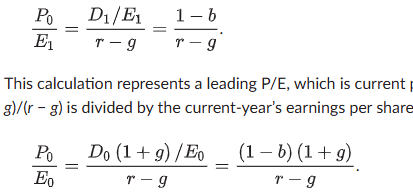

justified pe ratio

leading PE

trailing PE

H-model

growth begins at a high rate and declines linearly throughout the supernormal growth period until it reaches a normal rate at the end

H = half-life in years of the high-growth period (i.e., high-growth period = 2H years)

gS = initial short-term dividend growth rate

gL = normal long-term dividend growth rate after Year 2H

sustainable growth rate

g = b × ROE

FCFF vs FCFE

FCFF = NI + NCC + Int(1 – Tax rate) – FCInv – WCInv

FCFE = FCFF – Int(1 – Tax rate) + Net borrowing.

FCFF = CFO + Int(1 – Tax rate) – FCInv

FCFE = CFO − FCInv + Net borrowing.

FCFF = EBITDA(1 – Tax rate) + Dep(Tax rate) – FCInv – WCInv.

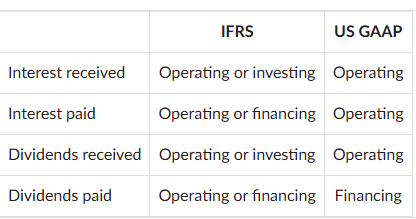

Interest and dividends (IFRS vs GAAP)

deferred taxes

should not add back deferred tax changes expected to reverse unless ot can consistently defer until a much later date

Incremental fixed capital expenditures as a proportion of sales increases

Required rate of return (real)

Country return (real)

+/– Industry adjustment

+/– Size adjustment

+/– Leverage adjustment

value of firm (FCFF)

V = Value of operating assets (FCFF) + value of non-operating assets (cash, marketable securities, land held for investment)

when to use FCFF vs FCFE

target debt/equity ratio is expected to remain consistent - FCFE

P/E ratios

Earning power is a chief driver of investment value,

widely recognized and used

EPS can be zero, negative, or insignificantly small

difficult to distinguish transient components

managers may distort EPS

normalizing EPS

estimating the level of EPS that the business could be expected to achieve under mid-cyclical conditions

historical average EPS

average return on equity, in which normalized EPS is calculated as the average return on equity (ROE) from the most recent full cycle, multiplied by current book value per share - effect on EPS of growth or shrinkage in the company’s size

inverse price ratio - earnings yield

reciprocal of the negative PE ratio

Predicted P/E Based on Cross-Sectional Regression

over a particular time period - predictive power over a different time/stock not known

relationships between P/Es and such characteristics as earnings growth, dividend payout, and beta are not stable over time

prone to the problem of multicollinearity

PEG ratio

P/E divided by the expected earnings growth rate (in %)

assumes a linear relationship between P/E and growth - in reality not linear

does not factor in differences in risk

does not account for differences in the duration of growth

justified price - historical eps

P/B

generally positive even when EPS is zero

book value per share is more stable than EPS- when EPS is abnormally high or low or is highly variable

companies composed chiefly of liquid assets, such as finance, investment, insurance, and banking institutions

not expected to continue as a going concern

human capital more important than physical capital - service companies not appropriate

levels of assets differ significantly - diff business models

Accounting effects on book value

some historical value some fair value

share repurchases or issuances can distort historical comparison

(Common shareholders’ equity)/(Number of common stock shares outstanding) = Book value per share

Adjustments to PB ratio

subtracting reported intangible assets

goodwill should be excluded

restate the book value of the company using LIFO to what it would be based on FIFO

adjusted for significant off-balance-sheet assets and liabilities

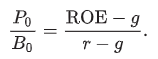

justified PB ratio

Price/Sales

Sales are generally less subject to distortion or manipulation than are other fundamentals

Sales are positive even when EPS is negative

appropriate for valuing the stocks of mature, cyclical, and zero-income companies

business may show high growth in sales even when it is not operating profitably

Share price reflects the effect of debt financing on profitability and risk but sales are before financing

does not reflect differences in cost structures

revenue recognition practices

justified PS ratio

price to CF ratio

Cash flow is less subject to manipulation

addresses the issue of differences in accounting conservatism

Operating cash flow, for example, can be enhanced by securitizing accounts receivable

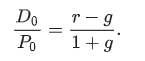

price/dividend yield

less risky component of total return than capital appreciation

but only one component of total return

may trade off future earnings growth to receive higher current dividends

annualized dividend rate divided by the current market price per share

justified price/dividend yield

Enterprise Value/EBITDA

for comparing companies with different financial leverage (debt)

EBITDA controls for differences in depreciation

EBITDA is frequently positive when EPS is negative

EBITDA will overestimate cash flow from operations if working capital is growing

FCFF better

Enterprise Value

Market value of common equity (Number of shares outstanding × Price per share)

Plus: Market value of preferred stock (if any) and any minority interest (unless included elsewhere)

Plus: Market value of debt

Less: Cash and investments (specifically, cash, cash equivalents, and short-term investments)

Equals: Enterprise value.

Return on invested capital

operating profit after tax divided by invested capital

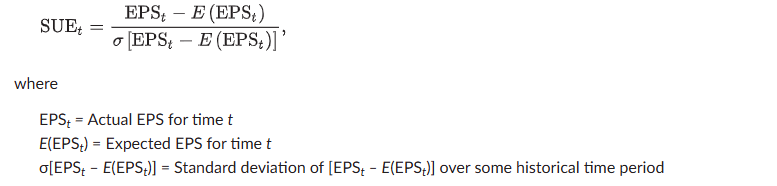

Earnings surprise

UEt = EPSt – E(EPSt),

standardized unexpected earnings (SUE)

harmonic mean - for multiples

mitigate the impact of large outliers. It may aggravate the impact of small outliers

look-ahead bias

use of information that was not contemporaneously available in computing a quantity - back testing

capital charge

total cost of capital in money terms

COE* Equity + COD*(1-t)*Debt

Residual income

NOPAT (after tax) - Capital charge or

Net income - Equity charge

ROIC

NOPAT (after tax)

Residual income can also be calculated as (ROIC – Effective capital charge) × Beginning capital.

economic value added

EVA = NOPAT – (C% × TC),

C% is the cost of capital, and TC is total capital

R&D is added back net of estimated amortization

Capital charge for strategic investments not expected to generate an immediate return - suspended until a later date

Deferred taxes eliminated- only cash taxes as expense

LIFO reserves added back to capital; increase in LIFO reserve added to NOPAT

Operating leases treated as capital - non-recurring items adjusted

market value added

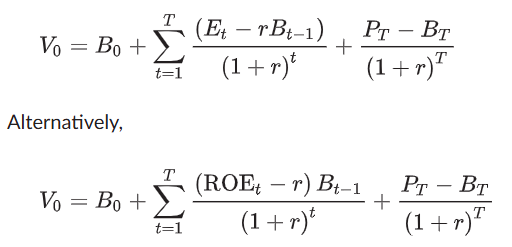

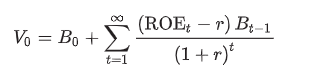

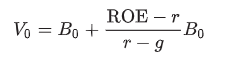

residual income model

current book value of equity + pv of expected residual income

assumes clean surplus accounting

excess earnings model

justified residual income model

Tobin’s q

ratio of the market value of debt and equity to the replacement cost of total assets

expected to be higher the greater the productivity of a company’s assets

residual income model where residual income fades over time

persistence factor, ω, which is between zero and one

1: will not fade

residual income model - Strengths & weaknesses

Terminal values do not make up a large portion of the total present value

readily available accounting data

companies that do not pay dividends or to companies that do not have positive expected near-term free cash flows

when cash flows are unpredictable

focus on economic profitability

accounting data that can be subject to manipulation

require either that the clean surplus relation hold

assumes that the cost of debt capital is reflected appropriately by interest expense

DLOC & Control premium

DLOC = 1 – [1/(1 + Control premium)]

discount for lack of marketability (DLOM)

reflect the relative absence (compared with publicly traded companies) of a liquid market for a company’s shares.

DLOM + DLOC

Total Discount = [1 – (1 – DLOC)×(1 – DLOM)]