nat 5 economics- unit 1

1/23

Earn XP

Description and Tags

Name | Mastery | Learn | Test | Matching | Spaced |

|---|

No study sessions yet.

24 Terms

the basic economic problem

also known as scarcity, arises because human wants for goods and services are unlimited due to greed, but we have limited resources. all countries are affected by scarcity, and it is not the same as a shortage

factors of production

resources which are used to produce goods/services

land- naturally occuring resources eg oil and fish

labour - the human workforce that produces goods and services. eg factory workers

capital- man made resources eg machines

enterprise- when an entrepeuner combines these to produce a good/service.

returns to the factors of production

land - rent

labour - wages

capital - interest

enterprise - profit

opportunity cost

the sacrifice of the next best alternative

mobility

the speed and ease with which a resource can change its location or use

effective demand

a want backed up by the money to buy the good/service you want

why does the demand curve slope downwards

law of diminishing marginal utility - consumers are willing to pay less for each additional unit

income effect - as price falls, consumers are able to buy more with the same amount of income

substitution effect - as a goods price decreases, substitutes appear more expensive, so demand for the cheaper good increases

willingness and ability to pay - as price falls, consumers are more willing and able to buy it

marginal utility

the extra satisfaction gained from consuming one more of a good or service

the law of diminishing marginal utility

the more of something you consume, the less marginal utility you gain from it

determinants of demand

income

price of substitute or complementary goods

tastes and fashion

advertising and publicity

population

weather and seasons

state of the economy

supply vs output

supply is the amount of good or service a firm is willing and able to send to the market at a certain price, in a certain time

output refers to the entire production of a good or service

why does the supply curve slope upwards

firms are only willing and able t increase their production as price increases, as they need to cover additional csts of production

when price therefore profit is high, new firms will start to produce the same product so overall supply increases

(assuming firms are profit maximisers)

higher costs

determinants of supply

costs of production

technology

weather and natural disasters

taxes and subsidies

competetive and joint supply

market

when buyers and sellers of a good or service come into effective contact, agree a price and then exchange the product for money

different types of market

goods eg cars

services eg transport

factors (cell) eg labour

money eg forex

fixed and variable costs

fixed costs are payments that dont change as output changes. eg rent and rates

variable costs are payments which directly changes with output. eg raw materials and wages

profit

the amount of money a firm has left over after they have paid all their costs.

TSR - TC

total sales revenue

the total amount of money/ income a firm recieves from selling their products

TSR = price x quantity sold

ASR = income per unit sold

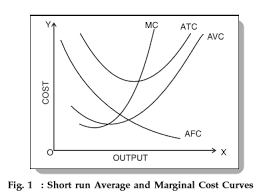

short run cost diagram

ATC - summation of AVC and AFC

AVC - law of diminishing marginal returns

AFC - spreading fixed cost over more output

short run

long run

period of time where at least one factor of producition is fixed

when al the factors of production are variable, therefore costs are variable

the law of diminishing returns

in the short run, marginal cost will decrease initially, but will always start to increase at some level of input

how to lower costs in supply

reduce wages

invest in technology

find cheaper supplies

improve training

greater specialisation

productivity

the relationship between output and input ( how much is being produced with a certain amount of resources )

methods of improving productivity

pay workers bonuses

use more division of labour

improve training of workers

invest in more efficient machinery