market failure - information failure/imperfect information

1/26

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai | Chat |

|---|

No analytics yet

Send a link to your students to track their progress

27 Terms

information failure/imperfect information

imperfect information: a case of information failure, where consumers/producers do not have correct or complete information about the costs/benefits of consuming or producing a good.

asymmetric information: a form of imperfect information, when one party has more information than the other party in an economic transaction

causes of imperfect information → myopic decision-making

MPCperceieved < MPCactual

in making decisions, consumers may only consider the costs and benefits in the immediate term, and are unaware of the costs or benefits in the long run ⇒ causes them to perceive the MPC to be

lower than what it actually ise.g.: smokers in deciding how many cigarettes to consume may only consider the private costs and benefits to themselves presently, and are unaware of the long-run detrimental health effects of smoking

when economic agents underestimate MPC, MPCperceived is less than MPCactual ⇒ the private optimal quantity Qp (where MPCperceived = MPB) is greater than the socially optimal quantity Qs (where MSC = MSB)

there is an overconsumption or overproduction of the good or service ⇒ deadweight loss of area abc because between Qs and Qp units of the good, the total social costs (area QsabQp) is greater than the total social benefits (area QsacQp), resulting in market failure

as the actual MPC is not fully taken into account, there is distortion of price signals ⇒ price mechanism fails to bring about a socially optimal allocation of resources

MPBperceieved < MPBactual

individuals may only take into account the costs and benefits to themselves at that point in time, but are unaware

of the long-run benefits → causes consumers to perceive the MPB to be lower than what it actually ise.g. health screening

when economic agents underestimate marginal private benefits, MPBperceived is less than MPBactual ⇒ the private optimal quantity Qp (where MPCPERCEIVED = MPB) is smaller than the socially optimal quantity Qs (where

MSC = MSB)there is an underconsumption or underproduction of the good or service ⇒ deadweight loss of area abc because between Qp and Qs units of the good, the total social benefits (area QpabQs) is greater than the total social costs (area QpcbQs), resulting in market failure

as the actual MPB is not fully taken into account, there is a distortion of price signals ⇒ price mechanism fails to bring about a socially optimal allocation of resources

causes of imperfect information → addiction

consumers may be addicted to consuming a good, causing the perceived MPC to be lower than what it actually is

e.g. for someone who is addicted to smoking, the smoker perceives the MPC of consuming cigarettes to be lower than the actual MPC, though he may experience a short-term high from smoking, he does not fully recognise the health risks of consuming cigarettes due to his addiction, causing him to underestimate the MPC involved

because MPCperceived is less than MPCactual, the private optimal quantity is more than the socially optimal quantity,

resulting in overconsumption of the good and hence deadweight loss of the shaded area ⇒ allocative inefficiency and market failure

causes of imperfect information → product complexity

when consumers shop for a technical product, they may not be

familiar with many of the technical terms or functions associated with it → consumers may end up overestimating the MPB and go for higher specifications or additional features even when they do not need them at alle.g. in the purchase of laptops, consumers are faced with technical terms such as “Processor Speed”, “RAM” among many others

customers may end up overestimating their MPB and go for more expensive procedures than needed

e.g. medical services which would involve a lot of technical knowledge, unethical doctors may prescribe services or medicine that may be more than what a patient actually requires

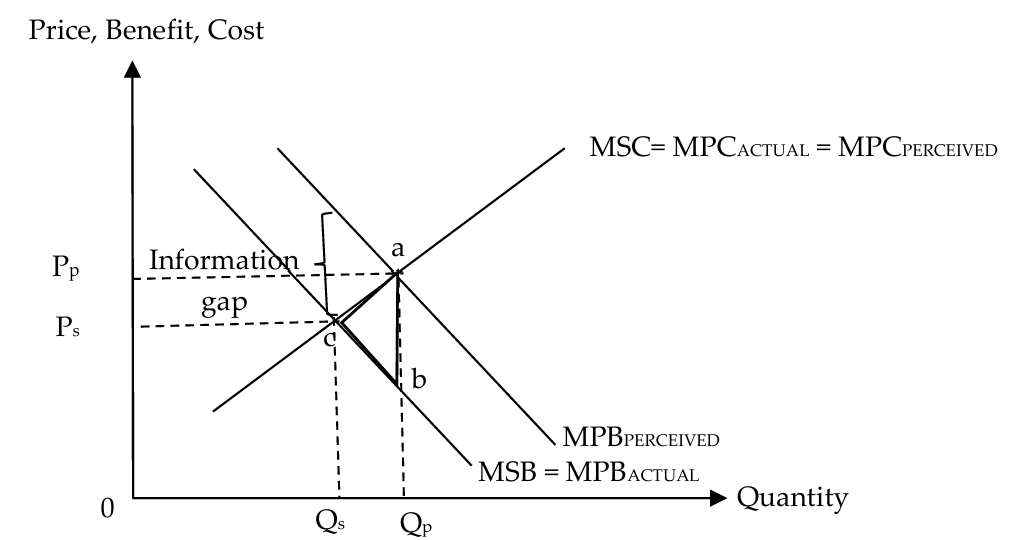

causes of imperfect information → persuasive advertising

firms may engage in advertising to influence consumers to buy their good or service⇒ perceived MPB is higher than what it actually is (an overestimation of the MPB)

e.g. laptop firms and salesmen may go all out to convince consumers that having more features and functions is better or necessary

when economic agents overestimate MPB, MPBperceived is more than MPBactual → the MPBperceived curve lies above the MPBactual curve

the private optimal quantity Qp (where MPCperceived = MPB) is greater than the socially optimal quantity Qs (where MSC = MSB)

there is an overconsumption or overproduction of the good or service ⇒ deadweight loss of area abc because between Qs and Qp units of the good, the total social costs (area QscaQp) is greater than the total social benefits (area QscbQp), resulting in market failure

as the MPB is perceived to be higher than what it actually is, there is a distortion of price signals ⇒ price mechanism fails

to bring about a socially optimal allocation of resources

government intervention for imperfect info → rules and regulations

in situations where consumers have incorrect or incomplete information regarding the private costs and/or benefits of consuming a good or service, the government can put in place measures to provide consumers with relevant information

provides consumers with more accurate information of the private costs and/or benefits of consuming a good or service ⇒ reduces the extent of over- or under- consumption, and hence the extent of allocative inefficiency

e.g. in Singapore, food companies are required to declare a significant amount of basic information (e.g. name and description of food, ingredients, possible

allergens, country of origin etc) on the labels of pre-packed foods. this enables consumers to more accurately consider the private costs and benefits of consuming a food product. if these regulations are not complied with, offenders may be subjected to a fine and/or imprisonment not exceeding 3 monthse.g. in the area of healthcare services, all medical practitioners are required to display medical charges openly and provide itemised receipts of fees charged, so that consumers have more accurate information regarding the services and reduces instances of overestimation of MPB

e.g. cigarette companies are also required by law to

display health warnings on cigarette packets so that consumers can more accurately determine the private costs of consuming cigarettes. this allows consumers to get a better sense of the actual costs of smoking and reduces instances of underestimation of MPC

limitations of rules and regulations

high administrative costs → unsustainability

there are high administrative costs involved in the enforcement of laws, which include the costs incurred in

setting up structures and deploying government officials to check whether consumers and producers are complying with the lawssuch high administrative costs could cause the implementation and enforcement of the rules and regulations to be unsustainable and hence ineffective in the long term

unintended consequences of rules and regulations

higher prices/poor quality of goods

requiring firms to provide more information to consumers may raise their cost of production

firms may pass on these additional costs to the consumers in the form of higher prices, or compromise on the quality of their good or service, thus negating the gain in consumer welfare from having more information

opportunity cost of implementation

to fund the high administrative costs, the government may have to channel public funds from other public projects, thus incurring opportunity costs in terms of the benefits that could have been gained from spending more in the other sectors

if the administrative costs of implementing, monitoring and enforcing the laws are substantial, causing it to outweigh the intended welfare gain, government failure will result

government intervention for imperfect info → public education

aims to provide more information to consumers about the actual

private costs and benefits of consuming a good to allow them to make informed choicesreflected by the shifting of the MPCperceived curve upwards to

coincide with the MPCactual curve and shifting the MPBperceived curve to coincide with the MPBactual curve so that the private optimal quantity is equal to the socially optimal quantity, thereby eliminating the deadweight losssome examples include education fairs, education on preventive healthcare, and anti smoking campaigns

the Health Promotion Board engages the community in various public campaigns to educate the public on the benefits of regular health check-ups

the Screen for Life (SFL) is a national screening programme that encourages members of the public to go for regular health screenings and follow up → educates the public of the private benefits of health screening, increasing their perceived MPB of doing so, and hence their consumption of such screening services ⇒ reduces the deadweight loss that would otherwise arise from under-consumption, achieving allocative efficiency

limitations of public education

time lag

it takes time for education to take effect, so this method does not offer immediate solutions to more pressing, urgent problems

the over- or under-consumption of the good continues, causing the market failure to persist

uncertainty of outcome

the outcomes of public education are subjected to the

receptivity of the publicthe eventual outcome is uncertain as people may not heed the advice due to stubbornness and ingrained habits that are hard to change

unintended consequences of public education

opportunity cost of implementation

education campaigns are expensive and may require substantial public funds

to fund these extra costs, the government may have to channel public funds from other public projects, thus incurring opportunity costs in terms of the benefits that could have been gained from spending more in the other sectors

other arguments for public education

education is a long-term solution to raise awareness of the actual costs and benefits of consuming certain goods and services

by reducing the extent of imperfect information, it directly targets the root cause of the market failure, hence reducing the gap between the private optimal quantity and the socially optimal quantity, as opposed to subsidies which are more expensive in the long run and only make people behave like they are well informed when they are not

public education may be a more politically favourable policy option for the government compared to rules and regulations as consumer sovereignty is preserved (consumers can still decide their level of consumption)

success of public education is also dependent on government’s knowledge of consumers’ cognitive biases such as salience bias

salience bias is our tendency to focus on things that are more apparent or obvious

e.g.: as obesity is a more visible problem compared to other health issues, the public education campaigns aimed at encouraging an active lifestyle are likely to be more successful if they were to focus on how regular exercises can help with immediate weight loss rather than the long term benefits of exercising

asymmetric information

a specific case of imperfect information and can be thought

of as a subset of itoccurs when one party has more information than the other party in an economic transaction ⇒ there is a difference in information available to buyers and sellers of a good (either the buyer or the seller can be the party withholding the information)

two main issues that can arise from asymmetric information → important to identify when information asymmetry happens (before or after)

adverse selection → happens before the transaction has been completed

moral hazard → happens after the transaction has been completed

the presence of adverse selection and moral hazard can lead to the eventual collapse of markets → no production and consumption takes place

however, with intervention from the government, and/or measures adopted by consumers and firms, asymmetric information can be mitigated, and the markets can continue to function

adverse selection

adverse selection: the process by which "undesirable" members of a population of buyers or sellers are more likely to participate in a voluntary exchange

arises from information asymmetry between the buyer and seller before the transaction has been completed ⇒ there are hidden characteristics of the good or service before the transaction takes place

adverse selection in the second-hand car market

used car dealers often have more information regarding the condition of the used cars being sold than potential buyers

e.g. dealers would probably have knowledge of the true mileage of the car, whether the car has met with any road

accidents (and if so, how many and to what extent), as well as whether the car has any defects that are unnoticeable by the naked eye

in order to profit from the sale of used cars and to fetch the highest possible selling price for their cars, used car dealers might have the incentive to hide some of the information that they have about the condition of their used cars from potential

buyerswhen used car buyers do not know whether the cars they are buying is of high or low quality, the tendency is for the market to be dominated by low quality cars that need frequent repairs, also known as the ‘lemons’

facing lack of information as to whether a car is a ‘cherry’ (high quality) or a ‘lemon’ (low quality), a buyer treats all cars to be of medium quality and will only be willing to pay the average price for a car of medium quality

hence, the sellers willing to sell the higher quality cars at higher prices will exit the market, which reduces the average quality of used cars in the market

over time, the increased presence of low-quality cars in the market will further lower the prices that consumers are willing to pay

the decrease in price will further decrease the number of high-quality cars supplied.

asymmetric information results in a market where some high-quality cars are sold, but fewer than what would be sold in a market with perfect information ⇒ welfare loss

in the most extreme case, the downward spiral in prices may continue, causing the number of high-quality cars supplied to drop to zero, resulting in no possible trade of high-quality used cars ⇒ missing market – ‘cherries’ are pushed out of the

market, leaving only ‘lemons’the market fails and is allocative inefficient as welfare

loss arises when mutually beneficial trade of high-quality used cars cannot take placethe sellers and buyers cannot overcome the information gap to trade at the prices that satisfy both their willingness to pay and sell

adverse selection occurs as the uninformed buyers end up having to choose from an undesirable or adverse selection of goods, which is not socially optimal

adverse selection in the health insurance market

buyers of health insurance have greater information over sellers (insurance companies), and consumers of health insurance

might not have the incentive to divulge sufficient and accurate information about their health conditions (e.g. how long they have been smoking, or if they have any persisting ailments) to insurance companies, as that would mean that they are likely

to have to pay higher premiums on their insuranceconsumers with higher risks are more likely to buy health insurance and choose higher levels of coverage ⇒ insurance companies risk providing insurance coverage to those with higher health risks

facing a lack of information as to whether a consumer of health insurance is healthy, the insurance company treats all consumers to be of average health and will only be willing to charge an average price for health insurance

the healthy consumers who are only willing to buy a cheaper plan will exit the market, which reduces the average health quality of consumers in the market

over time, the increased presence of less healthy consumers in the market will further increase the prices that the insurance company charges, to cover the potentially higher costs of insuring these people

the increase in price will further decrease the number

of relatively healthier consumers, as they drop out of the market

as the process continues, eventually, the remaining consumers left dominating the health insurance market will be the unhealthy ones ⇒ leads to adverse selection, where the unhealthy people are the only ones buying health insurance

private insurance companies find it unprofitable to provide insurance, as nearly all the people who want to buy insurance are unhealthy to a certain extent

could lead to a missing market where no insurance companies are willing to sell insurance

as transactions that could potentially increase society’s welfare are not realised, there is a deadweight loss, leading to market failure

moral hazard

moral hazard: a situation where economic agents take greater risks than they normally would, because the costs that would result would not be borne by the economic agents themselves

arises due to the presence of hidden actions taken by

economic agents after the transaction has been completed

moral hazard in the health insurance market

after purchasing health insurance, an individual might have the incentive to pursue an unhealthy lifestyle of excessive smoking and alcohol consumption since his medical bills will be covered by insurance payouts

there is no way for the insurance company to monitor the buyer’s behaviour after the policy is purchased

may result in excessive insurance payouts as the insured is likely to take on greater risks and engage in undesirable behaviour, which increases the probability that claims are made

as it would be too unprofitable to provide insurance in this case, no insurance companies would be willing to do so, thus leading to a missing market

results in allocative inefficiency and hence market failure, as mutually beneficial transactions between the insurance company and the potential customers do not take place,

leading to deadweight loss

government intervention for asymmetric information → rules and regulations

laws can be put in place to make it a legal requirement to facilitate the flow of information between economic agents (consumers and producers), reducing information asymmetry

laws to reduce adverse selection

the government can enact laws to regulate the quality of goods and services produced by firms

for second-hand car markets: the government may make it compulsory for used car dealers to send their cars for inspection and certification

by allowing the buyer of the car to have similar information to that possessed by the seller of the car, this helps alleviate the asymmetric information problem when buying a used car

better cars can be sold at higher prices, and ‘lemons’ can be sold at lower prices, thus allowing mutually beneficial transactions to take place in the market ⇒ eliminates the deadweight loss that would otherwise arise from a missing

market

the government can also set in place laws to protect consumers from ‘lemons’ even after the transaction is completed ⇒ effect is to increase in output of high-quality goods closer to the allocative efficient level

in Singapore, there is the Consumer Protection (Fair Trading) Act, also known as the Lemon Law → protects consumers against goods that do not conform to contract or are not of satisfactory quality or performance standards at the time of delivery

a consumer is able to make a claim for a defective product (known as a ‘lemon’) sold to him/her within 6 months of purchase

under the Lemon Law, it is compulsory for the seller of the defective good to either repair, replace, refund or reduce the price of the defective good, subject to certain conditions

if the seller does not comply, the issue can be raised to the Consumers Association of Singapore (CASE), whose aim is to protect the interest and welfare of

consumers

the penalties of the Lemon Law will incentivise the sellers of the defective products to disclose information about the products such that consumers have full information about the costs and benefits of purchasing the good at the point of transaction

as consumers can determine the quality of goods prior to the transaction, sellers of high-quality goods have the incentive to supply their goods at a higher price

laws to reduce moral hazard

the government can regulate insurance plans to ensure that moral hazard is reduced and there is no unnecessary wastage of resources

e.g. in 2019, the Singapore government passed a law that removed full riders on new insurance policies

previously, people could purchase insurance policies with full riders, which effectively allows people to pay nothing for hospital bills ⇒ present a moral hazard problem as it diluted responsibility for personal health, since the insurance would foot the full bill for medical treatment (for example, certain individuals may not be that careful with their sugar intake since they know that they can claim healthcare treatments from their insurance plans anyway).

as the demand for healthcare services is artificially increased with the presence of full riders, this could

lead to a wastage of resources as more resources are put into the healthcare sector than needed, leading to allocative inefficient outcomeswith this law in place, all insurance policies are no longer allowed to offer full riders and will require patients to pay 5% of their hospital bills (co-payment) before the insurance covers the rest

from 1 April 2026, this co-payment cap is raised from $3000

to $6000 per policy year, excluding deductibles

this would reduce moral hazard as paying part of their own hospital bills (co-payment) would incentivise people to take better care of their health + promote greater personal responsibility and reduce the strain on the healthcare system in the long run

limitations of rules and regulations

increased government expenditure → unsustainability

with a mandatory health insurance scheme, it is necessary to build up a reserve to manage the volatility of claims made by the high-risk insured

as a result, the premium rates of the low-risk individuals will increase

furthermore, with the growth in aging population in Singapore, medical insurance claims will rise ⇒ puts an upward pressure on MediShield Life premiums and increase government spending on subsidies in order to keep premiums affordable

such increase in government spending could be unsustainable, making the policy ineffective in the long term

information gap

the government may not have sufficient information to

determine the level of co-payment that is sufficiently high to incentivise the insured consumers to take responsibility of their own health, and yet not too high such that consumers end up bearing a large part of the costs

unintended consequences of rules and regulations

opportunity cost of implementation

to fund the high government expenditure, the government may have to channel public funds from other public projects, thus incurring opportunity costs in terms of the benefits that could have been gained from spending more in the other sectors

if the costs are substantial, causing it to outweigh the intended welfare gain, government failure will result

application of adverse selection and moral hazard to medishield life

MediShield Life is a basic and compulsory health insurance plan for all Singaporean Citizens and Permanent Residents, with the aim of lowering healthcare costs at both the individual and state level

with MediShield Life, the private insurance companies will help to foot a part of the bill when an individual incurs large hospital bills or have to go for selected costly outpatient treatments, such as chemotherapy for cancer

To tackle the problem of adverse selection, the government has made it mandatory for everyone to purchase MediShield Life

through the enforcement of such a mandatory insurance for the population, a win-win situation can be created where

insurers can spread the risk of insurance among both risky and less risky consumers (risk-pooling)consumers who are more susceptible to ailments have access to insurance at a cheaper price, and the government can save on expensive healthcare subsidies

to reduce the moral hazard problem, MediShield Life makes use of deductible and co-payment to incentivise people to take better care of their health

with a deductible and co-payment clause, the buyer of the insurance is required to pay a portion of any claim made

reduces moral hazard on the part of the insurance buyer, as the buyer will now bear part of the costs of his risky behaviour, and hence think twice about taking excessive risks after the insurance is bought

private solutions to reduce asymmetric information

in the presence of asymmetric information, buyers and/or sellers have the incentive to facilitate the flow of information between parties so that mutually beneficial transactions may take place

the existence of asymmetric information does not necessarily mean that the government needs to intervene directly to solve

the market failureprivate sector solutions often reduce the problems of adverse selection and moral hazard to some extent as private agents are highly incentivised to do so

private solutions to reduce adverse selection

signalling

signalling refers to the more informed party’s attempt to convey information about the product quality to the less informed party

as sellers of high-quality goods would like to charge high prices, they have the incentive to convince buyers that their quality is indeed high

sellers may signal to buyers that their products are of high quality through various ways

e.g. guarantees and warranties may be a way for sellers to signal that their product is of high quality as the sellers are liable to repair or replace a defective product

with the additional information obtained through signalling, buyers are assured that the product is of good quality and would be willing to pay a higher price for it

prevents adverse selection and enables mutually beneficial transactions to take place, achieving an allocative efficient outcome

screening

screening refers to an action taken by the less informed party to make it mandatory for the more informed party to provide him with information, before the transaction takes place

by providing the less informed party with the necessary information, screening prevents adverse selection and enables mutually beneficial transactions to take place between buyers and sellers

e.g. health insurance firms can gather information such as medical history or make it mandatory for customers to go for health check-ups, to determine the risk level of a potential customer before selling the insurance. having ascertained which customers are of high risk, the firm may then charge them a higher premium to compensate for the higher risk

private solutions to reduce moral hazard

insurance companies can make the insured bear a portion of the claims made through co-payments and deductibles in insurance plans → creates a monetary incentive for the insured to make a more responsible decision and not to engage in risky behaviour

insurers could also include terms in the insurance contracts to reduce moral hazard

e.g. a fire insurance company may insist that a firm install a sprinkler system in a warehouse to offset any increased carelessness once the insurance policy is in place