ACG2071 EXAM 1 MCQ

1/33

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai | Chat |

|---|

No analytics yet

Send a link to your students to track their progress

34 Terms

Which of the following statements is not true?

Operating income is also referred to as earnings before interest and taxes.

Gross margin equals sales revenue minus cost of goods sold.

Gross profit equals gross margin minus selling and administrative expenses.

Operating income equals gross margin minus selling and administrative expenses.

Gross profit equals gross margin minus selling and administrative expenses.

The primary reason managers classify costs as either product costs or period costs is to:

Measure operating income for an accounting period.

Predict future costs at an expected level of activity.

Assign costs to operating segments.

Choose between alternative courses of action.

Measure operating income for an accounting period.

Which of the following statements regarding product costs are true (check all the statements that are true)?

A manufacturing company treats all its operating expenses as product costs.

Advertising expenses that promote a specific product line are treated as product costs.

Product costs that are expensed are reported on the income statement as cost of goods sold.

Product costs always reduce operating income in the accounting period the cost is incurred.

Conversion costs include all product costs other than direct materials costs.

Product costs that are expensed are reported on the income statement as cost of goods sold.

Conversion costs include all product costs other than direct materials costs.

Selling and administrative expenses include:

Advertising costs (order-getting) but not shipping costs (order-filling).

Depreciation on property, plant and equipment used in administrative activities.

Executive compensation, including the salaries of manufacturing plant managers.

Manufacturing overhead costs that are fixed in nature.

Depreciation on property, plant and equipment used in administrative activities.

Within the relevant range, which costs will change as the level of activity changes?

Total fixed costs and total variable costs.

Per-unit fixed costs and total variable costs.

Per-unit variable costs and per-unit fixed costs.

Per-unit fixed costs and total fixed costs.

Per-unit fixed costs and total variable costs.

Which of the following statements regarding committed versus discretionary fixed costs is true?

Discretionary fixed costs are less difficult to change in the short run.

Employee training costs are an example of a committed fixed cost.

A capital expenditure for new equipment is an example of a discretionary fixed cost.

Research and development costs are an example of a committed fixed cost.

Discretionary fixed costs are less difficult to change in the short run.

Which of the following statements is true?

The contribution margin measures how much a company charges for its products over and above the cost of acquiring or producing the products.

The gross margin measures how much of a company’s revenue is available to cover fixed costs and generate a profit.

Managers prepare contribution margin income statements for internal planning and decision-making purposes.

GAAP requires companies to prepare income statements using the contribution margin format.

Managers prepare contribution margin income statements for internal planning and decision-making purposes.

A manufacturing company’s contribution margin equals:

Sales revenue less variable cost of goods sold.

Sales revenue less variable cost of goods sold and variable selling and administrative expenses.

Sales revenue less variable manufacturing costs.

Sales revenue less all variable and fixed operating costs.

Sales revenue less variable cost of goods sold and variable selling and administrative expenses.

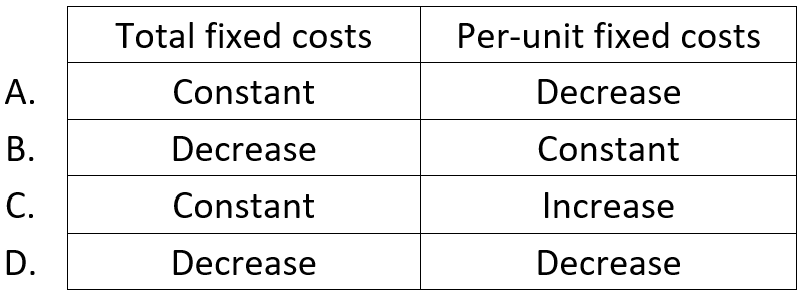

How do total fixed costs and per-unit fixed costs react to a decrease in the level of activity?

Choice C

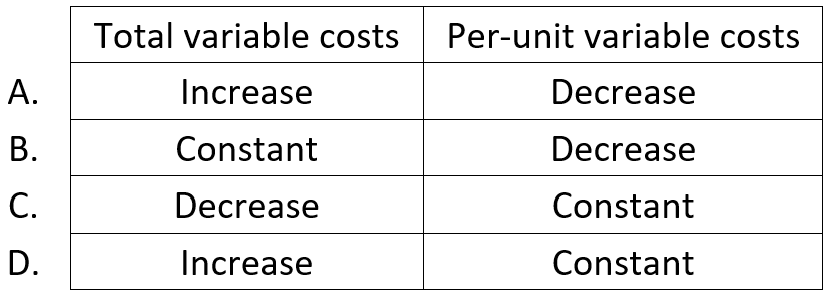

How do total variable costs and per-unit variable costs react to an increase in the level of activity?

Choice D

Which of the following statements regarding manufacturing overhead costs is not true?

Manufacturing overhead is an indirect cost that is difficult or impossible to trace to a specific job.

Manufacturing overhead includes both variable overhead costs and fixed overhead costs.

Manufacturing overhead is incurred to support only specific jobs rather than jobs in general.

Manufacturing overhead includes indirect materials, indirect labor, and other types of indirect manufacturing costs.

Manufacturing overhead is incurred to support only specific jobs rather than jobs in general.

Which of the following statements regarding manufacturing overhead costs is true?

Using a single plantwide overhead rate based on direct labor hours will ensure that overhead costs are accurately traced to jobs.

An overhead allocation base is an activity, such as rooms occupied, miles driven, or computer time, that causes direct costs to increase or decrease.

If a specific job is not completed by year end, then no overhead costs are applied to that job when computing the end-of-year balance of work in process inventory.

The amount of overhead applied to a specific job reflects an estimate of the overhead resources consumed by the job.

The amount of overhead applied to a specific job reflects an estimate of the overhead resources consumed by the job.

Which of the following is the correct formula for computing a predetermined overhead rate?

Actual total overhead costs ÷ Actual total units of the allocation base

Estimated total overhead costs ÷ Estimated total units of the allocation base

Actual total overhead costs ÷ Estimated total units of the allocation base

Estimated total overhead costs ÷ Actual total units of the allocation base

Estimated total overhead costs ÷ Estimated total units of the allocation base

In a job costing system, each of the following events triggers a journal entry which results in a debit to the Work in Process Inventory account, except:

Tracing direct material costs to a specific job.

Tracing direct labor costs to a specific job.

Completing the production of a specific job.

Applying manufacturing overhead costs to a specific job.

Completing the production of a specific job.

Which of the following statements regarding the use of multiple departmental overhead rates rather than a single plantwide overhead rate to apply manufacturing overhead costs to jobs is not true?

A job costing system that uses departmental overhead rates is more complex than a system that uses a single plantwide overhead rate.

If a company uses cost-plus pricing, the target selling price will generally be the same regardless of whether the company uses departmental overhead rates or a single plantwide overhead rate.

The benefit of using departmental overhead rates is that they more accurately reflects the actual amount of overhead resources consumed by a specific job.

One reason for using departmental overhead rates is that the activity in some departments is more labor intensive whereas the activity in other departments is more machine intensive.

If a company uses cost-plus pricing, the target selling price will generally be the same regardless of whether the company uses departmental overhead rates or a single plantwide overhead rate.

Acme Company uses the cost-plus method for establishing a target selling price for each of its products. Which of the following statements best describes the items that Acme must consider when determining the mark-up percentage?

Manufacturing costs, including direct labor, direct materials, and manufacturing overhead.

Manufacturing costs and selling and administrative expenses.

Manufacturing costs, selling and administrative expenses, interest expense, and income taxes.

Manufacturing costs, selling and administrative expenses, interest expense, income taxes, and the desired profit.

Manufacturing costs, selling and administrative expenses, interest expense, income taxes, and the desired profit.

Which of the following formulas for computing a merchandising company’s cost of goods sold and ending merchandise inventory are correct?

Choice B and D

For a manufacturing company, which of the following formulas is correct?

Cost of goods sold = Cost of goods manufactured + Ending finished goods inventory – Beginning finished goods inventory

Raw materials used = Ending raw materials inventory + Purchases – Beginning raw materials inventory

Cost of goods manufactured = Total manufacturing costs added + Beginning work in process inventory − Ending work in process inventory

Ending finished goods inventory = Cost of goods sold – Beginning finished goods inventory + Cost of goods manufactured

Cost of goods manufactured = Total manufacturing costs added + Beginning work in process inventory − Ending work in process inventory

In a job order costing system, indirect labor costs are usually recorded as a debit to:

Manufacturing overhead.

Work in process inventory.

Finished goods inventory.

Cost of goods sold.

Manufacturing overhead.

Manufacturing overhead is overapplied if:

The manufacturing overhead account has a debit balance at the end of the year.

The actual manufacturing overhead costs are greater than the estimated manufacturing overhead costs.

The manufacturing overhead account has a credit balance at the end of the year.

The estimated manufacturing overhead costs are greater than the actual manufacturing overhead costs.

The manufacturing overhead account has a credit balance at the end of the year.

If manufacturing overhead is underapplied and the amount is immaterial, the entry to close the manufacturing overhead account will:

Decrease gross margin.

Which of the following statements regarding activity-based costing is not true?

Costing is a two-stage process, whereby costs are first assigned to activity cost pools and then each cost pool is allocated using activity measures.

Potential allocation bases are limited to duration-based cost drivers; transaction-based cost drivers are not permitted.

Each major activity has its own overhead cost pool, its own activity measure, and its own allocation rate.

A cost pool is a type of “cost bucket” in which a company accumulates the costs related to a particular activity.

Potential allocation bases are limited to duration-based cost drivers; transaction-based cost drivers are not permitted.

The use of a single overhead allocation base that is based on overall production volume, such as plantwide direct labor hours, may not accurately allocate the costs of different types of overhead resources to specific product lines if these products vary significantly in terms of:

the number of units of the product that are produced and sold each year.

the cost of specialized equipment used to manufacture a specific product line.

the number of custom features that customers may request with respect to a specific product line.

All the above.

All the above.

Which of the following statements regarding the cost hierarchy is not true?

Assembling a product is an example of a unit-level activity.

Parts administration is an example of a product-level activity.

Processing a purchase order for component parts is a facility-level activity.

Setting up the equipment used in a production line is a batch-level activity.

Processing a purchase order for component parts is a facility-level activity.

Acme Company produces a wide range of products and applies manufacturing overhead to jobs using a plantwide overhead rate based on direct labor hours. Acme’s use of a single cost driver that reflects overall production volume will tend to systematically:

Over-cost high-volume products and under-cost low-volume products.

Under-cost high-volume products and over-cost low-volume products.

Over-cost both low-volume and high-volume products.

Under-cost both low-volume and high-volume products.

Over-cost high-volume products and under-cost low-volume products.

Which of the following statements regarding process costing is not true?

Production costs are transferred from one work in process inventory account to the next as products flow from one processing department to the next.

A process costing system serves the same basic purposes as a job costing system.

A process costing system is best suited for companies that mass produce a large quantity of a homogeneous product.

Separate work in process inventory accounts are maintained for each type of production cost, direct materials and conversion costs.

Separate work in process inventory accounts are maintained for each type of production cost, direct materials and conversion costs.

Which of the following statements regarding the equivalent units of production for a processing department is true?

The total equivalent units of production equals the sum of the units completed and transferred out of the processing department plus the number of units in ending work in process inventory.

During any given accounting period, the total equivalent units of production must be the same for both direct materials and conversion costs.

The total equivalent units of production measures the work performed, including both fully completed units and partially completed units, expressed in terms of completed units.

The total equivalent units of production is the numerator of the fraction used to compute a processing department’s cost per equivalent unit for an accounting period.

The total equivalent units of production measures the work performed, including both fully completed units and partially completed units, expressed in terms of completed units.

The amount of “Total Costs to Account For” equals:

Cost of beginning work in process inventory + Cost of units completed and transferred out

Cost of beginning work in process inventory + Cost of ending work in process inventory

Cost of ending work in process inventory + Cost of units completed and transferred out

Cost of ending work in process inventory + Costs added to production during the period

Cost of ending work in process inventory + Cost of units completed and transferred out

The cost per equivalent unit:

Represents the average cost of processing one fully completed unit in a processing department during the accounting period.

Equals the production costs added during the accounting period divided by the units completed and transferred out.

Equals the total costs to account for divided by the units completed and transferred out.

Is computed for conversion costs but is not computed for direct materials if all direct materials are added at the beginning of the process.

Represents the average cost of processing one fully completed unit in a processing department during the accounting period.

In a process costing system, the cost of the units completed and transferred out of a department is computed for each type of production cost, as follows:

Cost of beginning work in process inventory + Costs added during the period

Units completed and transferred out × Cost per equivalent unit

Units in ending work in process inventory × Cost per equivalent unit

Cost of ending work in process inventory − Costs added during the period

Units completed and transferred out × Cost per equivalent unit

Acme Company uses process costing and has two processing departments. Which of the following statements regarding the second processing department is true (check all the statements that are true)?

The total costs to account for include the costs transferred-in from the first processing department.

The cost of units in ending work in process inventory includes only the production costs added in the second department.

The company separately computes the cost per equivalent unit for the costs transferred in from the first processing department.

When computing equivalent units of production, all units are 100% complete with respect to transferred in costs.

The cost of units completed and transferred out to finished goods includes only the production costs added in the second department.

The total costs to account for include the costs transferred-in from the first processing department.

The company separately computes the cost per equivalent unit for the costs transferred in from the first processing department.

When computing equivalent units of production, all units are 100% complete with respect to transferred in costs.