[FUNACC] Chapter 2 | ACCOUNTING PRINCIPLES AND REPORTING STANDARDS

1/35

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No study sessions yet.

36 Terms

Accounting

measures and communicates the economic activities of organizations. Used by businesses, governments, universities, airports, airlines. All organizations need similar financial information to make decisions. Enables evaluation of profitability, liquidity, and solvency

Airline Application:

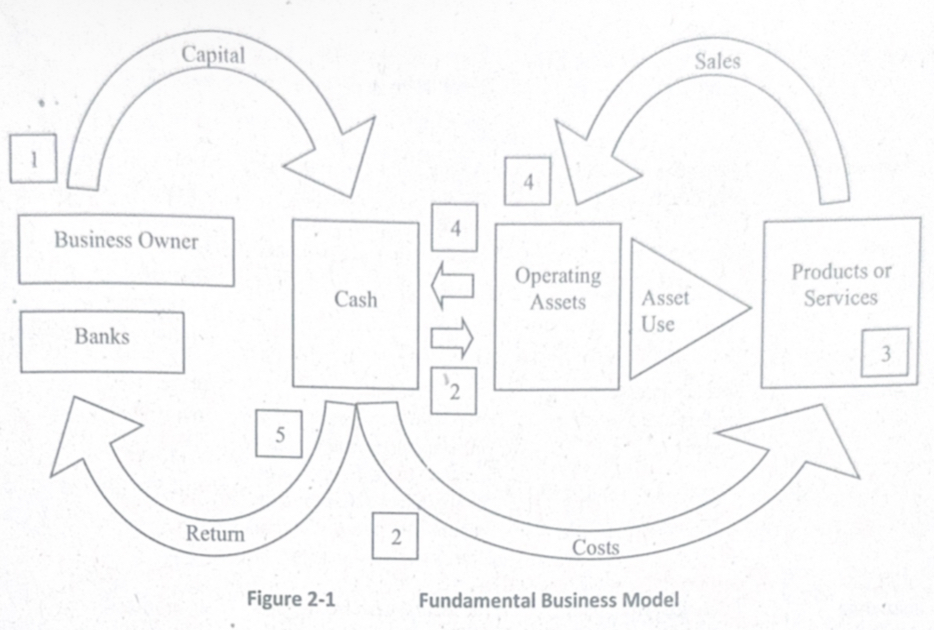

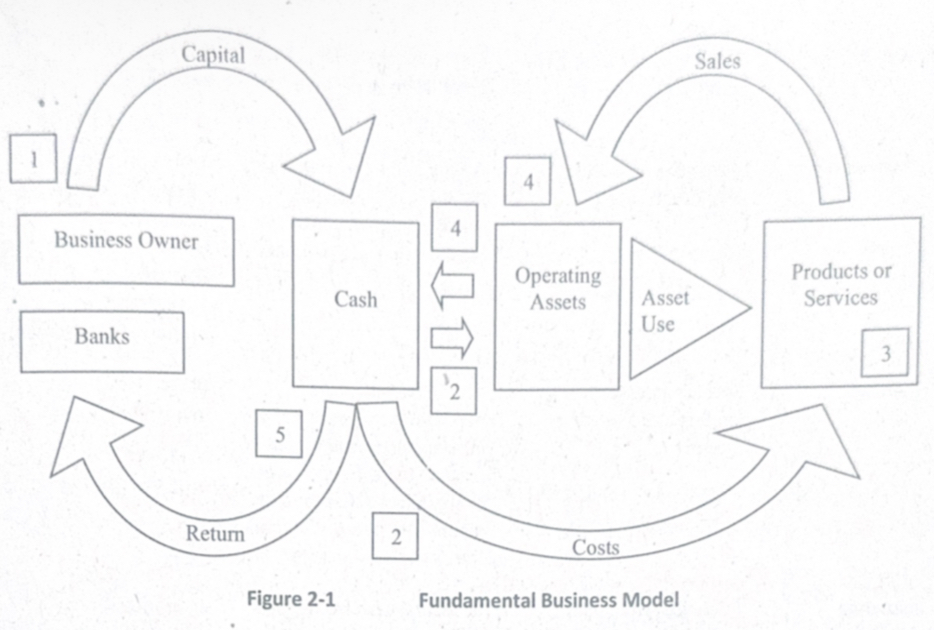

Investors provide funds → purchase aircraft

Airline uses assets (planes, crew, fuel)

Flights operate (service)

Tickets sold → revenue collected

Revenue returns as cash → reinvested in operations

Fundamental Business Model

Airline Application:

Investors provide funds → purchase aircraft

Airline uses assets (planes, crew, fuel)

Flights operate (service)

Tickets sold → revenue collected

Revenue returns as cash → reinvested in operations

Service

[Types of business according to activity]

provides services (e.g., airlines, airports)

Ex: Philippine Airlines, CAAP, MROs

Trading

[Types of business according to activity]

buys and sells goods (e.g., aviation parts suppliers)

Ex: Fuel distributors, in-flight product suppliers

Manufacturing

[Types of business according to activity]

converts raw materials into products (e.g., Airbus, Boeing)

Ex: Aircraft, engine, avionics manufacturers

Sole Proprietorship

[FORMS OF BUSINESS ORGANIZATIONS]

owned by one person

Ex: Small drone photography business

Partnership

[FORMS OF BUSINESS ORGANIZATIONS]

owned by two or more person

Ex: Two pilots running an aviation consultancy

Corporation

[FORMS OF BUSINESS ORGANIZATIONS]

separate legal entity owned by shareholders

Ex: PAL, Cebu Pacific, AirAsia, Clark Airport Corp

RA 9501

Under _________ and updated laws:

Micro: up to ₱3M assets

Small: ₱3M–₱15M assets

Medium: ₱15M–₱100M assets

Micro

Under RA 9501 and updated laws: up to ₱3M assets

Small

Under RA 9501 and updated laws: ₱3M–₱15M assets

Medium

Under RA 9501 and updated laws: ₱15M–₱100M assets

MSMEs IN AVIATION

Common examples:

Small travel agencies

Aviation training centers

Catering and ground support micro businesses

Airport terminal concessionaires

Aviation component sellers

OPERATING

FINANCING

INVESTING

ACTIVITIES OF BUSINESS ORGANIZATIONS (3)

Operating Activities

[ACTIVITIES OF BUSINESS ORGANIZATIONS]

Day-to-day operations

(e.g., ticket sales, fuel purchases, crew salaries)

Investing Activities

[ACTIVITIES OF BUSINESS ORGANIZATIONS]

Buying/disposing long-term assets

(e.g., aircraft acquisition, hangar construction)

Financing Activities

[ACTIVITIES OF BUSINESS ORGANIZATIONS]

Obtaining funds from creditors/owners (e.g., bank loans for aircraft, bond issuance)

Accounting

Purpose of ________ is to:

Produce useful financial information

Support decision-making

Assess profitability, liquidity, and solvency

Assist management and external users

Identifying

Recording

Classifying

Summarizing

Interpreting

PHASES OF ACCOUNTING (5)

INTERNAL USERS

[USERS OF ACCOUNTING]

Managers

Employees

Owners

Board of Directors

EXTERNAL USERS

[USERS OF ACCOUNTING]

Investors

Lenders

Suppliers

Gov’t agencies

Public

CAAP

[USERS IN AVIATION]

regulatory compliance

Airlines

[USERS IN AVIATION]

route profitability

Lessors

[USERS IN AVIATION]

evaluating aircraft lease payments

Investors

[USERS IN AVIATION]

profitability and long term viability

Banks

[USERS IN AVIATION]

loan decisions

Entity Concept

Business is separate from its owners

Periodicity

Business life is divided in to periods such as months or years

Stable Monetary Unit

The company is using a stable/single currency.

Objectivity

They use reliable evidence not opinions. (Ex: receipt)

Revenue Recognition

We record revenue when it is earned when necessarily when the cash is received

FINANCIAL REPORTING

To provide information useful for decision-making

HELP USERS ASSESS:

Economic resources of the entity

Claims against the entity

Changes in resources and claim

FINANCIAL REPORTING

________ SHOULD HELP USERS EVALUATE:

Buying/selling/holding decisions

Providing resources to the entity

Assessing management’s stewardship

Predicting future cash flow

Assets

Liabilities

Equity

Income

Expenses

ELEMENTS OF FINANCIAL STATEMENTS (5)

FINANCIAL STATEMENTS

FUNDAMENTAL:

Relevance

Faithful Representation

ENHANCING:

Comparability

Verifiability

Timeliness

Understandabilit

GOING CONCERN ASSUMPTION

This assumption states that the business will continue to operate indefinitely