Looks like no one added any tags here yet for you.

What does allotment of shares mean?

Company creates shares.

Gives them to existing SH or new SH.

Issue share certificate. Add / amend Register of SH.

What does transfer of shares mean?

SH gives shares to another SH or new SH.

Total no. shares remains same.

Identity of SH changes.

What does buyback of shares mean?

Company buys back shares from SH.

Reverse of allotment. Reabsorbs shares.

What 3 questions must you ask before allotting shares?

Constitutional restrictions on allotment?

Directors have authority to allot shares?

Any pre-emption rights?

How might constitutional restrictions for companies incorporated before and on / after 1 October 2009 be different?

Companies prior 1 October 2009 have ‘ceiling’ on shares (Authorised Share Capital) under memorandum of association.

Can change via ordinary resolution. Exception to requirement for special resolution.

Companies after 1 October 2009 do not have this provision. But may exist in articles.

Can change via special resolution.

File at Companies House.

How may a private company with one class of shares allot new shares?

Post-CA 2006; directors do so via board resolution.

Pre-CA 2006; SH must give permission via ordinary resolution.

How may a PLC or private limited company with more than one class of shares allot new shares?

[S. 551, CA 2006]

Require advance consent of SH via ordinary resolution.

State max number of shares; date authority expires (no more than 5-years).

Check company’s articles for authority. Can amend via ordinary resolution.

NOTE - Latter is exception to rule that articles only amendable via special resolution.

ALSO - File OR at CH. One of few exceptions to do this.

What is a pre-emption right?

Existing SH first refusal over allotment.

Offered % share reflect own share ownership.

Example - John owns 600 shares (60% total shares).

New shares allotted = 100 shares.

John gets 1st refusal on 60 of 100 shares.

How long do SH have for 1st refusal under pre-emption rights?

[S. 562, CA 2006]

Offer must state acceptance period.

Cannot revoke in that time.

Cannot be less than 14-days.

Where will pre-emption rights not be applicable?

Allotment bonus shares (s. 564, CA 2006)

Consideration wholly or partly non-cash (s. 565, CA 2006)

Employee share scheme (s. 566, CA 2006)

NOTE - If consideration not wholly / partly cash may also be a ‘substantial property transaction’. Require OR.

Can a company disapply statutory pre-emption rights under the CA 2006?

Yes.

Do so via company’s articles; or

Special resolution

Can amend also (i.e. alter acceptance period, allotment where non-cash).

How may a private company with one class of shares disapply pre-emption rights?

Do so via special resolution (s. 569, CA 2006).

Only if have authority to allot shares (s. 550, CA 2006)

How may a PLC or private company with more than one class of shares disapply pre-emption rights?

These companies required ordinary resolution for directors to allot (s. 551, CA 2006).

If general authority to allot then special resolution to disapply pre-emption (s. 570, CA 2006).

If specific authority then disapply via special resolution (s. 571, CA 2006).

But require ‘directors’ recommendation’.

What is a directors’ recommendation? What is contained within it? When is it used?

Applies to PLCs, private companies more than one share class.

Directors have specific authority to allot shares.

Need to pass special resolution and issue recommendation to dis-apply pre-emption rights.

Reasons for recommendation;

Amount purchaser will pay;

Justification of amount.

Who is the ‘directors recommendation’ circulated to? Must it be attached to anything?

Circulate to SH + notice of GM.

If written resolution then attach to it (s. 571, CA 2006).

What does MA 21 say about shares being fully paid?

Buyer must pay for shares when received.

Can disapply and accept part-payment.

Share capital = Profit made on allotment of shares (i.e. original price £1 now bought for £1.50).

AKA ‘sold at premium’.

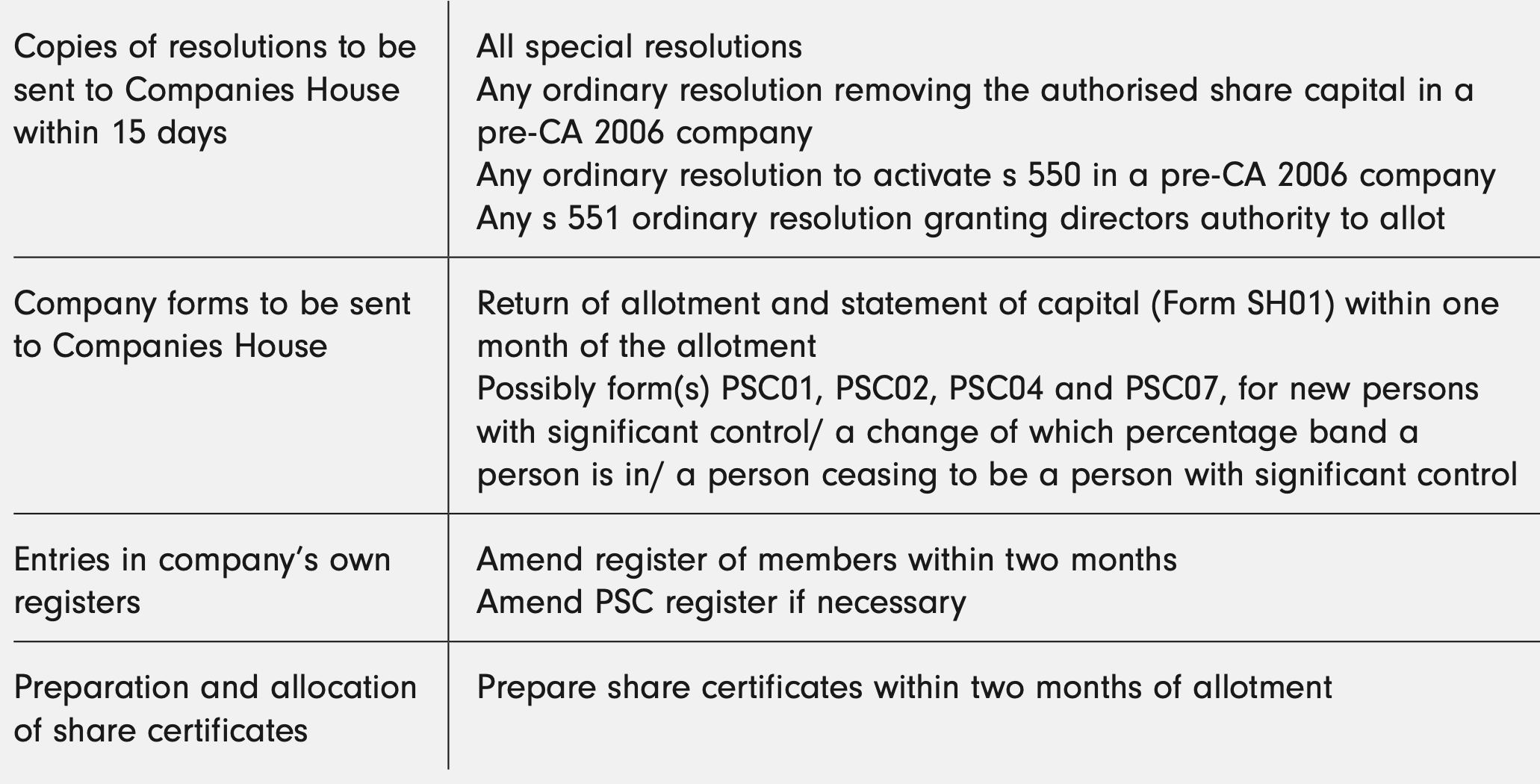

What are the administrative and filing requirements upon allotment of shares?

Why might a SH be wary of people transferring their shares?

No express prohibition within CA 2006.

But can change power dynamic within company.

Company articles usually contain restrictions.

Does MA 26 restrict share transfers in any manner?

Yes.

SH can sell / transfer shares.

BUT not a SH unless on register of members (s. 113, CA 2006).

MA 26 requires board resolution to do so.

Otherwise SH mere beneficial owner. Old SH is legal owner (pay dividends to former; vote as proxy).

How are shares transferred between transferor and transferee?

Transferor sign + complete ‘stock transfer form’ (STF). Give to transferee with share certificate (ss. 770-772, CA 2006).

Transferee pays stamp duty on shares.

Transferee sends share certificate + stamped STF to company.

Directors pass / reject BR of stock transfer. Absolute discretion under MA 26.

Register transfer in ‘Register of Members’. Issue share certificates within 2-months of application.

Update shareholder details annually on ‘Confirmation Statement’ (CS01).

How does the company register the transfer of shares?

Send new SH a new share certificate within 2-months (s. 776, CA 2006).

Enter name on register of members within 2-months (s. 771, CA 2006).

Notify Registrar of Companies when company files annual confirmation statement (CS01).

If a SH dies or goes bankrupt - what happens to their shares?

Automatic process called ‘transmission’.

Pass to PRs if died; or

SH is bankrupt; shares vest in trustee in bankruptcy.

MA 27 - Entitled to dividends. But do not become SH in company.

True or False: Share capital in a company cannot be given back or reduced.

True.

Fund used to repay creditors.

Dividends cannot be paid out of share capital.

Company (generally) can’t purchase own shares.

Exceptions:

Buy back shares using procedure (s. 690, CA 2006).

Court order to payoff unfairly prejudiced SH (s. 994, CA 2006)

Can return capital to SH after payment debts on winding up.

Why might a company buy back shares?

Restrictions on share transfer. Not enough votes for special resolution.

SH cannot find purchaser for shares.

What are the downsides of buying back shares?

Reduces profits available for dividends.

Reduces capital for creditors. Less money for SH on winding up.

Short-term financial benefit over longer term success / plan.

Suspicious. Boost executive pay.

Directors keep duties / responsibilities in mind when doing so.

What are the requirements for a share buyback?

Articles must not forbid buyback (s. 690, CA 2006)

Shares be fully paid (s. 691, CA 2006)

Co. pay for shares at time of purchase (s. 691, CA 2006)

Shares paid from distributable profits or proceeds fresh issue of shares to finance purchase (s. 692, CA 2006).

SH pass ordinary resolution (s. 694, CA 2006)

Copy of buyback contract available for inspection. Available 15-days prior GM and at GM itself. Or sent with proposed written resolution (s. 696, CA 2006).

Copy buyback contract available for inspection at registered office / SAIL once concluded. Period of 10-years from date buyback.

Personal interests do not prevent SH from voting. Is there an exception for SH buyback situations?

Yes.

Ordinary resolution required buyback shares.

Cannot vote under written resolution.

Votes won’t count at GM if make difference between passing or not (s. 695, CA 2006).

Can both private limited companies and PLCs fund a share buyback out of their capital?

Private limited companies - YES

PLCs - NO

Pvt. limited companies must exhaust profits first.

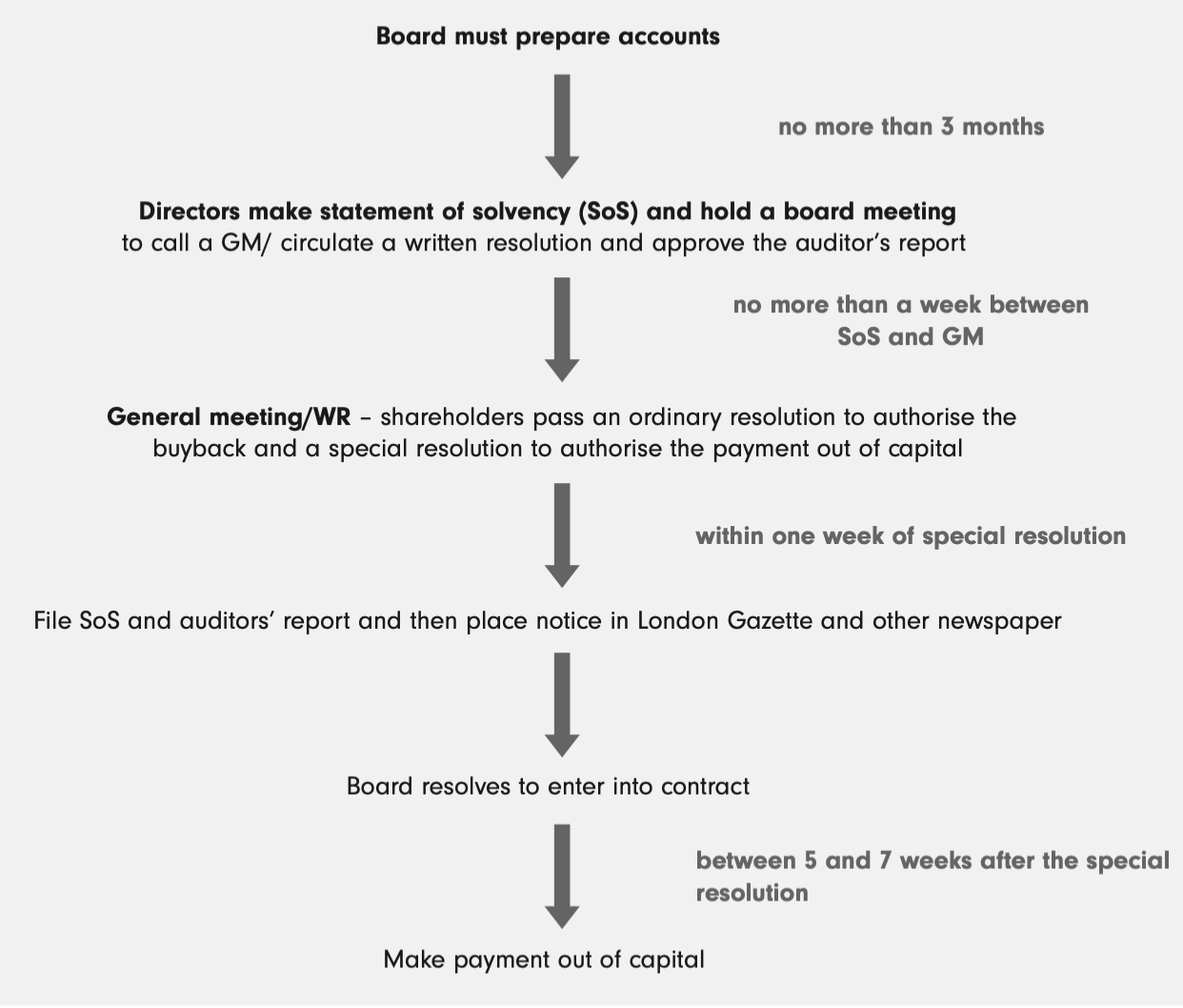

A private limited company wants to fund a share buyback through their capital.

What steps do they need to do?

Below is in addition to steps required for distributable profits.

Directors make solvency statement at least 7-days before GM. State Co. is solvent and will be so for 1-year.

Statement attached to auditor’s report. Confirm opinion is not unreasonable (s. 714, CA 2006).

Payment out of capital must be approved by special resolution. In addition to ordinary resolution to approve buyback contract.

Copy of directors’ statement + auditor’s report available for SH. Attach to written resolution or at GM for inspection.

Publish notice in London Gazette (within 7 days SR). State decision, amount of capital, date of SR, location director’s statement + auditor report (s. 719, CA 2006). Publish further notice in national newspaper or give notice each creditor (s. 719, CA 2006).

Creditors can apply for order to block buyback via capital (s. 721).

Company file director’s statement and auditor report at CH before or same time notices in London Gazette / newspapers.

Statement and report kept for inspection at registered office from 1st notice until 5-week post-SR passing (s. 720, CA 2006).

Creditors don’t object? Hold BM and pass resolution to enter contract. Payment out of capital no earlier than 5-weeks after date of SR to approve buyback. And no later than 7-weeks after date of SR (s. 723, CA 2006).

A company has 100,000 ordinary shares and 50,000 6% fixed cumulative preference shares.

The preference shares carry the right to receive, out of the profits of the company available for distribution and resolved to be distributed and in priority to other shareholders, a fixed cumulative preferential dividend at the rate of 6% per annum on the capital paid up on that share. All the shares have a nominal value of £1 each.

The company has reported profits of £20,000.

How much will the preferential shareholders receive in dividends?

6% of £1 (nominal value of each share).

6p x 50,000 (preferential shares) = £3,000

£20,000 - £3,000 = £17,000 (i.e. sufficient profits).

The three directors of a company have decided that it needs an injection of capital to help fund expansion plans. The directors are the only shareholders of the company and they each own one third of the ordinary shares which have a nominal value of £1 each and which are the only shares in issue. The company has adopted the Companies (Model Articles) Regulations 2008 (unamended) as its articles of association and has not previously passed any resolutions in connection with an allotment of shares.

The proposals are as follows:-

to issue 5,000 x £1 ordinary shares to each of the existing shareholders for £25,000;

to issue 1,000 x £10 cumulative, non-participating 6% preference shares to one of the shareholders;

to borrow £10,000 from one of the other shareholders.

What shareholder resolutions are required, if any, to achieve the above proposals?

An ordinary resolution is required to authorise the directors to allot the shares and a special resolution is required to amend the company’s articles.

Ordinary resolution = Grant directors authority to issue shares. Because more than 1 class of share.

Special resolution = Amend Co’s articles to incorporation new preference shares into constitution. Not previously included.

Why not another SR? Because no need to dis-apply pre-emption rights as already offering to existing shareholders.

Do not need OR to approve loan. Why? Because it is a loan from a director not to a director. Directors’ duties not implicated.

When is stamp duty charged on a sale of shares? How is this calculated?

Sale price of shares over £1000? Pay stamp duty.

Multiply sale value by 0.5%.

Round up to nearest £5.