Micro Theme 1

1/30

Earn XP

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

31 Terms

Ceteris paribus

This is a key term meaning “other things being equal”.

Factors of production

1) Land: raw materials, factory, shop

2) Labour: workers

3) Capital: machinery / technology

4) Enterprise: an entrepreneur successfully combining the three other factors

What is a PPF?

A Production Possibility Frontier shows the maximum output of 2 goods or services that can be produced by an economy at a given point in time with fixed factors of production.

Points on the curve show an efficient means of production while points below the curve show an inefficient means of production

An increase or decrease in either the quantity or quality of the factors of production will cause the PPF to shift out (positive) or shift in (negative).

What is specialisation and the division of labour?

Specialisation refers to where workers focus on producing the goods and services that they are most skilled at producing.

The division of labour is a form of specialisation where tasks are divided among workers.

Advantages and disadvantages of S and DoL

Advantages:

1) Workers can become more skilled in their given tasks which increases productivity

2) Lower costs as there is a higher output and efficiency

3) Increased profitability which allows for higher wages

Disadvantages:

1) Repetitive tasks may lead to job dissatisfaction from workers and they could become bored

2) Increased dependence on workers so any small mishap can halt production

Functions of money

1) Medium of exchange - used to buy and sell

2) Store of value - allows for holding wealth over time

3) Unit of account - common measure for pricing goods and assets

4) Standard of deferred payment - reliable way to settle debts and make future payments

Characteristics of effective money

1) Relative scarcity - to prevent inflation

2) Divisibility - must be easily divisible into smaller denominations

3) Portability - must be easy to carry around

4) Durability - must be able to withstand repeated use

What is rational decision making?

This is the assumption that firms and customers logically choose decisions to maximise their utility (satisfaction).

What is demand?

Demand is the want or need for a product backed by the money to purchase it.

An increase in price causes a contraction in demand (quantity goes down), while a decrease in price causes an extension (quantity goes up).

On a demand-supply curve, when demand shifts decreases (inward shift), price goes down and the quantity demanded goes down.

On a demand-supply curve, when demand increases (outward shift), price goes up and the quantity demanded goes up.

What is supply?

Supply is the quantity of goods producers are able to sell at a given price.

An increase in price causes an extension is supply (quantity goes up), while a decrease in price causes a contraction in supply (quantity goes down).

On a demand-supply curve, when supply shifts decreases (inward shift), price goes up and the quantity demanded goes down.

On a demand-supply curve, when supply shifts increases (outward shift), price goes down and the quantity demanded goes up.

Factors affecting demand and supply

Demand:

1) Price of goods and substitute goods

2) Consumer income

3) Advertisements / health or scientific advice

Supply:

1) Production costs

2) Technology (capital)

3) Number of workers

What is the price mechnism?

The price mechanism operates through the interaction of supply and demand

1) Signalling - price rises and falls to reflect scarcities and surpluses

2) Rationing - price acts to ration scarce resources

3) Incentive - a change in price will affect consumers’ demand for goods

What is the diminishing marginal utility?

This is a principle stating that as you consume more units of a good or service, the extra satisfaction (marginal utility) you get from each additional unit decreases.

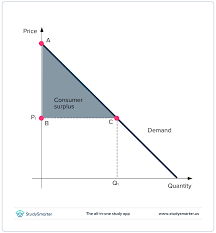

Consumer surplus

This is the extra satisfaction gained by consumers from paying a price for a good less than what they would have been prepared to buy it for.

On a demand-supply graph, this is represented as the triangle shaped area below the demand curve and above the market price.

Producer surplus

This is the extra satisfaction gained by producers from selling a good at a higher price than what they would have been prepared to sell it at.

On a demand-supply graph, this is represented as the triangle shaped area below the demand curve and below the market price.

Price elasticity of demand (PED)

PED measures the sensitivity of the quantity demanded of a good or service to a change in price of a good or service.

PED = (% change in quantity demanded) / (% change in price)

Factors affecting PED

1) Cheaper alternatives

2) Time periods

3) Brand loyalty

4) Income

5) Necessity vs luxury

Elastic good

An elastic good is a product that has it demand changed significantly when its price changes.

Inelastic good

An inelastic good is a product that doesn’t have its demand changed significantly when its price changes.

Elasticity scale

PED > 1 - elastic good (demand is very responsive to price change)

PED = 1 - unitary elastic (% change in demand is equal to % change in price)

PED < 1 - inelastic good (demand is not as responsive to price change)

Income elasticity of demand (YED)

YED measures how responsive the quantity demanded of a good is after a change in income.

YED = (% change in quantity demanded) / (% change in income)

What is a normal good?

A normal good is a good that has its demand rise with an increase in income.

This shows a positive relationship between income and demand.

What is an inferior good?

An inferior good is a good that has its demand fall with an increase in income.

This shows a negative relationship between income and demand.

What is a luxury good?

A luxury good is a good that has its demand increase when the income of a consumer also increases.

They typically have a YED above 1.

What is a necesity?

A necessity is a good whose demand will stay the same regardless of a change of income.

They are essential for survival and typically have a low YED between 0 and 1.

Cross-Price elasticity of demand (XED)

XED measures how the demand for one good changes in response to a price change of another good.

XED = (% change in quantity demanded of good A) / (% change in price of good B)

What is a complementary good?

A complementary good is a product whose demand increases when the price of another product falls.

What is a substitute good?

A substitute good is a product where its demand increases when the price of another product rises.

Price elasticity of supply (PES)

PES measures the sensitivity of quantity supplied of a good or service in response to a change in the market price of the good or service.

PES = (% change in quantity supplied / % change in price)

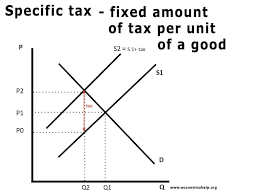

What is a specific (per-unit) tax?

A specific tax is a fixed charge added to each unit of a sold good or service regardless of its initial price.

It only affects the supply curve (paid by the seller), causing a parallel shift.

What is an ad valorem (percaantage) tax?

An ad valorem tax is a charge calculated as a percentage of the item’s value and added on to the initial price.

As the price of the item increases, so does the ad valorem tax.

On the supply curve it shifts and pivots to the left.