economics and the economy

1/31

Earn XP

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

32 Terms

what economics analyses

what to produce

how to produce

for whom to produce for

how economists make choices

act rationally

willingness to pay

opportunity costs

incentives

rationality

use available information to make the best decisions which only occurs if benefits outweigh costs

willingness to pay

maximum amount of money you are willing to pay for something, which represents your benefit from it

opportunity cost

the value of the best alternative you must sacrifice, includes monetary and non monetary costs

market

a set of arrangements by which buyers and sellers are in contact to exchange goods and services

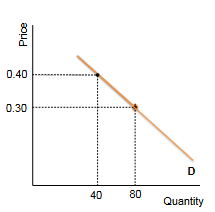

demand

the quantities of a good buyers wish to purchase at each conceivable price

measures relationship between price and quantity for buyers

demand curve

as price increases, quantity demanded decreases

downward curve

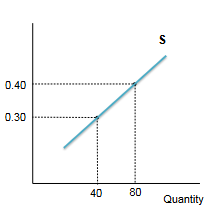

supply

the quantities of a good sellers wish to sell at each conceivable price

measures relationship between price and quantity for sellers

supply curve

as price increases, quantity supplied increases (as less demand due to high price equals more supply)

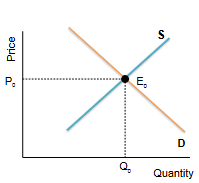

market equilibrium

quantity demanded equals quantity supplied

the equilibrium price is P0 and quantity is Q0

equilibrium price

price at which quantity supplied equals quantity demanded

movements along the supply curve

results from changes in the price of the good

supply shifts

caused by changes in technology,

input costs

government regulations

business expectations