Chapters 2 and 3 AP Econ Test

1/39

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

40 Terms

economic system

a set of institutional arrangements that deal with the economising problem.

what is produced?

how is it produced?

who gets the output?

how to deal with change and promote technology?

who owns factors of production

how to motivate or direct economic activity?

command system

aka social communism

gov own property

decision making is centralized

gov owns firms and directs desicions

capital goods are allocated based on gov plan

market system

aka capitalism

private ownership

markets and prices determine activity

self interest - individuals make choices

competition

decision making is widely dispersed

gov protects private property and operation of market system

laissez faire - “let it be”

ex: mostly everyone else

free enterprise and choice

free to obtain/use resources to produce and sell goods that they choose

consumers are able to buy whatever they want w money

choice

owners can do what they want with property and money

workers can choose their work

consumers buy what they want

self interest

each group tries to achieve its own goal

owners want to maximize profits

workers want to maximize utility

21st century paradox

we are powerful consumers but powerless workers

specializaton

uses resources to produce one specific good and sell/trade it instead of making everything

human specialization = division of labor

ex: chipotle

how do we decide what a dollar is worth?

money is agreed upon social agreement

active but limited government: “the tragedy of the commons”

when there are common resources available, how do you stop people from abusing them?

things that belong to all are cared for by none

Example: ocean and fishing → too much of it to stop the population from doing it

what will be produced?

production will occur when Total Revenue (TR) exceeds Total Costs (TC).

tells you what to make not how many to make

if TR > TC → its profitable → make it

if TR < TC → its not profitable → don’t make it

how will goods/services (g/s) be produced?

cheapest and most efficient way possible

ideal mix of land labor capital

labor is often the most expensive

demand

curve that shows the quantity of a product that consumers are willing and buy at a specific point of time

always willing - not always able

depends on time → must be specific

immediate short run

short run

long run

immediate short run

all factors of production are fixed → no changes can be made

short run

one or more are fixed → can make some changes but not a lot

long run

depends on variable inputs

theoretical construct

period of time long enough to change resources

change in demand

indicates shift on the curve (left or right)

change in price

indicates movement on the curve

law of demand

negative/ inverse relationship

as price rises, demand drops

as price drops, demand rises

law of demand cont.

1) consistent with common sense

2) buyers derive less benefit for each unit consumed (diminished marginal utility -? additional utility only if price is lower)

3) income effect

price of good falls → purchasing power increases → buyers can afford more → Qd rises

4) substitution effect

lower prices makes other products relatively more expensive, so buyers substitute towards the cheaper good

determinants of demand

T - tastes/preferences

I - income

M - market size

E - expectations of consumers

R - prices of RELATED goods

T- tastes/ preferences

favorable change in consumer tastes

shifts curve left or right depending on reaction

I - income

usually as income increases → demand increases

normal goods: when income increases, you buy more of it (new clothes, restaurant meals etc.)

inferior goods: when income increases, you buy less of it (ramen noodles, bus rides, used cars)

depending on the good and my situation, demand will either increase or decrease

M - market size/number of buyers

more buyers = more demand

less buyers = less demand

E - expectations of consumers

what people expect to happen influences their behavior today

when prices are expected to rise soon → they’ll buy now (current demand increases)

when prices are expected to fall soon → they’ll buy later (or after prices have dropped) → the current demand decreases

R - prices of Related goods

substitute goods: goods that can be in place of each other

good 1 (coke): price increases

good 2 (pepsi): demand increases

complementary goods: goods that are used together

good 1 (ice cream): price increases

good 2 ( ice cream cones): demand decreases

supply (upward/ positive relationship)

a curve showing various amounts of a product that producers are willing and able to make available for sale during a period

law of supply (movements)

producers are motivated by profit

price of good rises → selling it would be more profitable → producers supply more of it

price of good falls → selling it would be less profitable → producers supply less of it

determinants of supply

T - technology

O - other goods

N - number of sellers in the market

E - expectactions of producers

R - resource prices

S - subsidies and taxes

T - technology

allows production at a lower cost of inputs

production price drops (bc of tech) → supply rises

O - prices of Other goods ( not on test ?)

substitutes in production

higher price of one → lower supply of other

N- number of sellers

like the demand determinant

if market increases → supply increases

P - producer expectations

much trickier than consumer expectations

what producers think will happen to the price of their product in the future

future price increases → current supply decreases (wait to sell after prices increase)

future price decreases → current supply increases (sell now before prices decrease)

R- resource prices

higher resource prices raise production costs → supply decreases

lower resource prices lower production costs → supply increases

S - Subsidies and taxes

taxes → increase production cost → supply decreases (shifts left)

subsidies → decrease production cost → supply increases (shifts right)

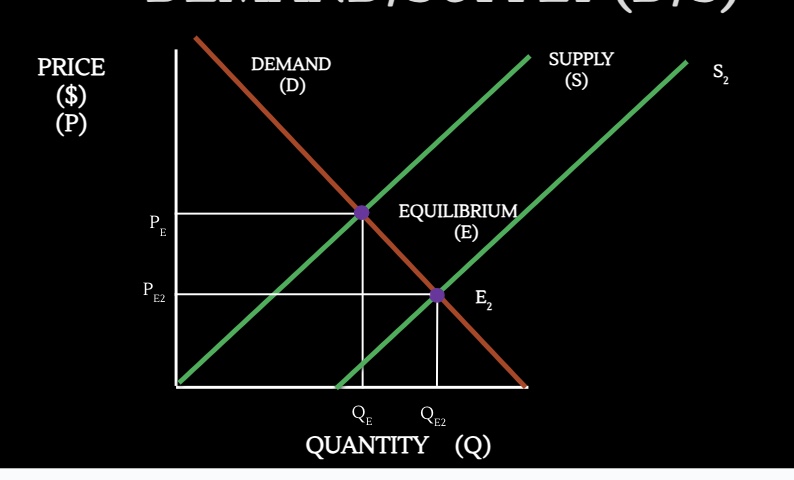

equilibrium price Qd = Qs

price where intention of buyers and sellers match

equilibrium quantity Qd = Qs

quantity demand and quantity supply at equilibrium price

draw a demand/supply graph