Looks like no one added any tags here yet for you.

Definition: Economics as a social science

Economics is the study of the choices that people make in overcoming the problems that arise because resources are limited, while needs and wants are unlimited.

The nine central concepts of IB Economics

It looks good to include these in your answers for Paper 1 and 2. Do not force them in if they don't work.

Concepts:

Scarcity

Choice

Efficiency

Equity

Economics well-being

Sustainability

Change

Interdependence

Intervention

Factors of production

Land:

Land includes all resources provided naturally and may also be referred to as "natural capital".

Labour:

All the human resources that are used in producing goods and services. It may be referred to as "human capital".

Capital:

Anything made by humans, or "physical capital". Buildings, offices, factories, machines, tools, infrastructure and technologies.

Entrepreneurship:

In managing the other factors of production, entrepreneurs take the risk by using their funds and money, and hence they are a factor of production.

Scarcity

There are unlimited needs and wants but limited resources, leading to scarcity.

Since resources are limited, they must be used efficiently and sustainably.

Opportunity cost

Every decision made by an economic agent (government, consumer or producer) has a cost associated with it, called the opportunity cost. This pertains to the idea that the resources used in producing or consuming one product reduce your opportunity to consume or produce another.

Free goods

Free goods are goods that have no opportunity cost in their consumption. Goods such as air have such a high supply that their consumption does not lower the opportunity to consume another.

Basic economics problems

- What should be produced?

The question of where it is best to allocate resources, considering opportunity cost and effects on stakeholders.

- How should it be produced?

Automated or manual labour? Basically, what is the optimal method of production for a given good.

- For whom should it be produced?

Should goods be provided to everyone, or only to those who afford them? How will the national income be distributed, for example?

Means of answering economics questions

Market vs. Government intervention

Free market economies vs. Mixed market economies vs. Planned economies.

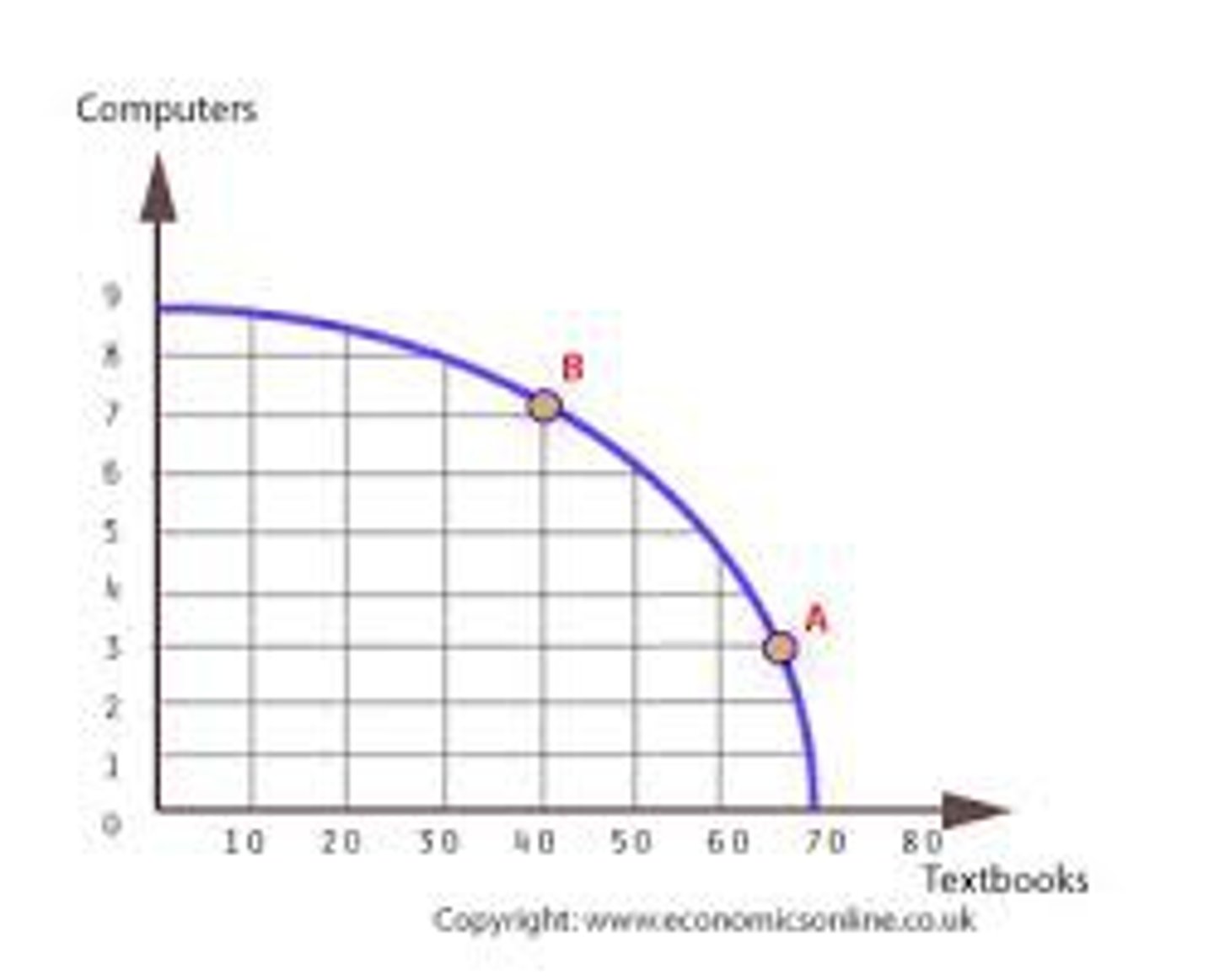

The PPC model assumptions

The economy produces only two goods.

All resources and the state of technology in the economy are fixed.

All the resources in the economy are fully employed.

Increasing opportunity cost

A concave PPC shows an increasing opportunity cost, implying that the more one good is produced, the less the other is, at a non-constant rate.

An example would be agricultural output against manufactured goods, as the FoP requirements are very different.

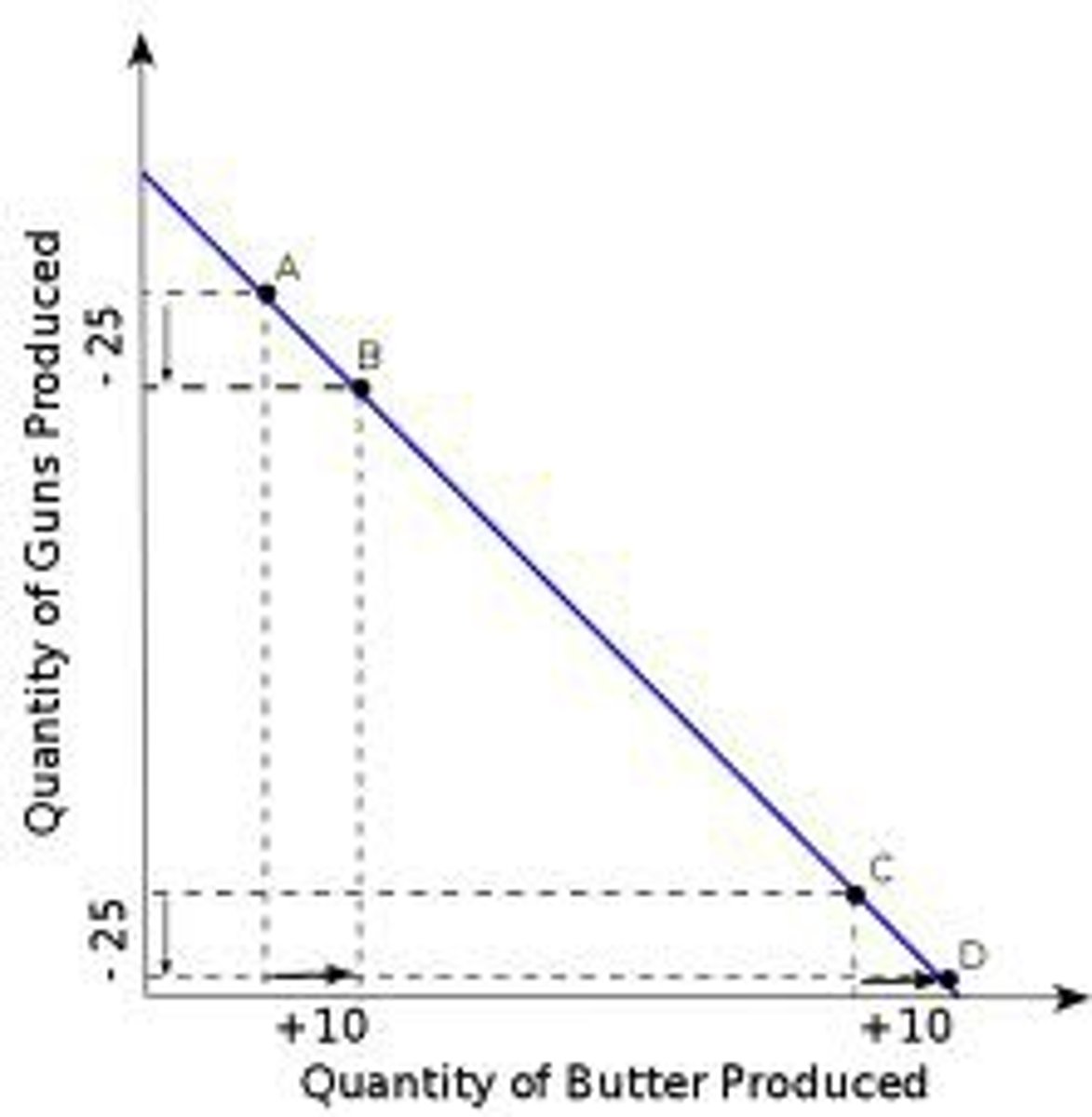

Constant opportunity cost

A constant opportunity cost is shown by a concave PPC curve, showing that resources are easily exchanged between goods.

An example is the production of lemons against oranges, as both use almost identical FoP.

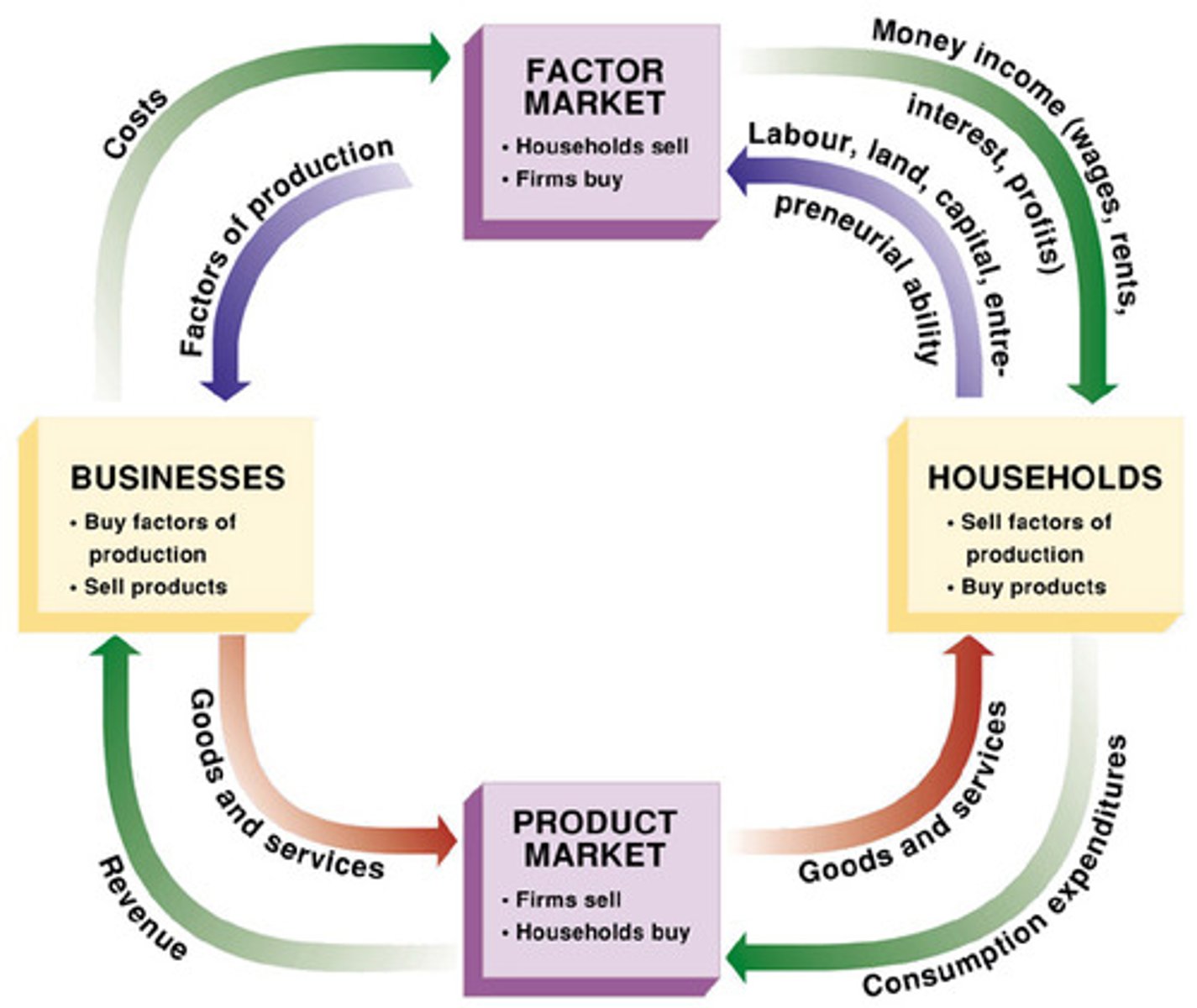

Circular flow model

In a closed economy, there is a circular flow of income.

Firms give households goods and services, wages and rent.

Households give firms FoPs and expenditure on goods and services.

Leakages and Injections

The leakages in an economy represent money leaving an open economy. They are:

Taxes,

Savings,

Imports.

The injections in an economy are responsible for introducing income into the circular flow. They are:

Government spending,

Investments,

Exports.

Economic Thought (Laissez faire - Adam Smith)

The idea of the 'invisible hand'. When left alone, producers are guided by the flow of profit into what they should produce, without any external agency telling them what to do and not do.

Producers also bring jobs, which are favourable for society as they provide people with wages, allowing them to live.

Adam Smith was the leading proponent of this idea, arguing that there should be no intervention whatsoever.

Economic Thought (Say's Theory - Classical Economics)

The idea is that the production of goods is the source of all demand in an economy.

The circular flow model shows that the economic activity of production creates incomes equivalent to the value of the output, which are then used to consume other goods and services. Hence, producers effectively create consumers' purchasing power by supplying goods, creating demand.

The main argument is that there cannot be an overproduction of goods and that economic growth is achieved by focusing on increasing production.

Economic Thought (Neoclassical Economics)

The rejection of the idea that the value of a good is determined by the costs of labour and the proposition that the value placed by the consumers determines the value of the good. Gives rise to the idea of utility, and the theory of diminishing marginal utility.

Economics Thought (Marxism)

A critique of modern economic theory, stating that society's ability to produce would grow faster than its ability to consume, causing growing unemployment, and arguing for the complete governmental provision of goods (communism).

Economic Thought (Keynesian)

Keynes argues that the best way to combat recessions is through government expenditure, going against the notion of 'automatically stabilizing markets'. He argued for budget deficits, demand-side theory and counter-cyclical policies.

Economic Thought (New Classical Economics)

Goes against the Keynesian idea that increasing AD and the money supply is the best approach. Argues that Keynesian thought leads to "too much money chasing too few goods". Argues for the central bank to not manage demand at all, but rather control the growth of the money supply. Theory of 'rational expectations'.

Economics Thought (Behavioural Economics)

The modern idea is that there is no such thing as a rational producer or consumer and that psychology governs economics. The idea of nudge theory - teaching people to make better decisions (such as through education).

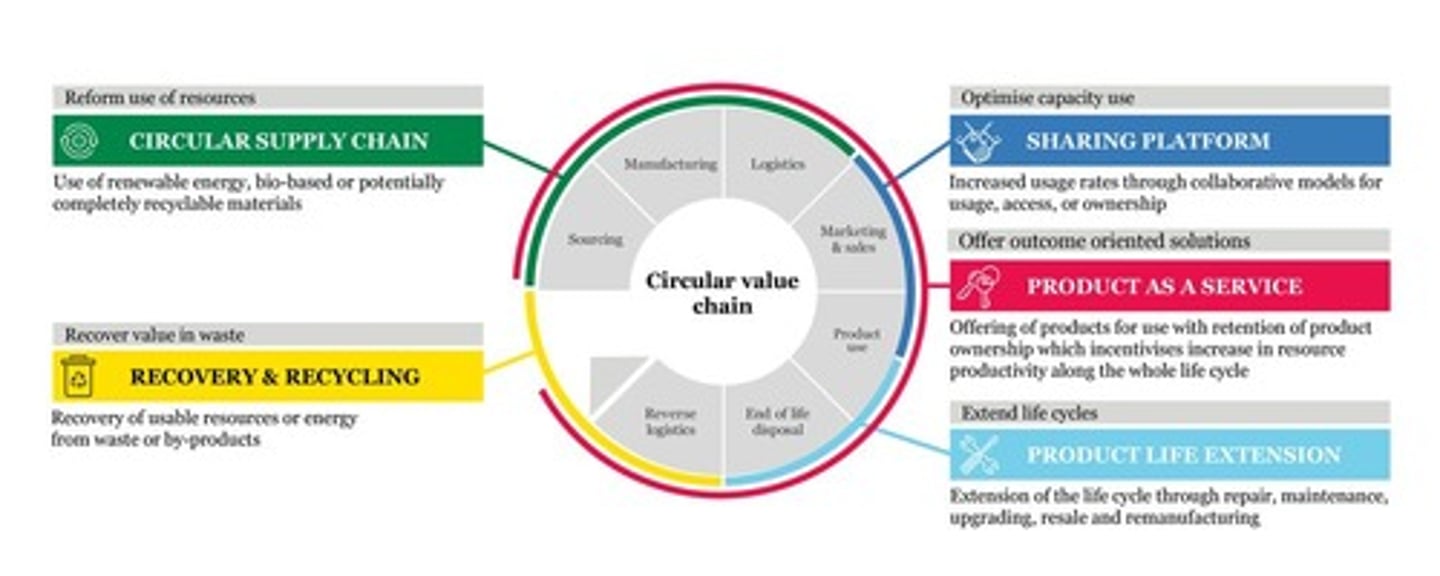

Redefining the circular economy in the 21st century (see diagram).