Tax Lec 6

1/10

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai | Chat |

|---|

No analytics yet

Send a link to your students to track their progress

11 Terms

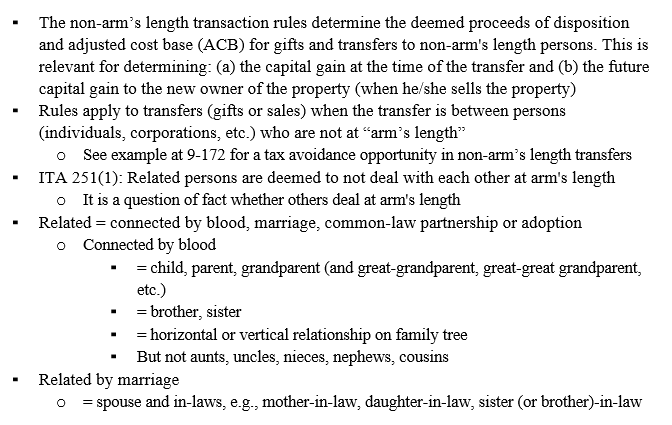

Non-Arm’s Length Transfers

Define what Inadequate consideration mean in NALT

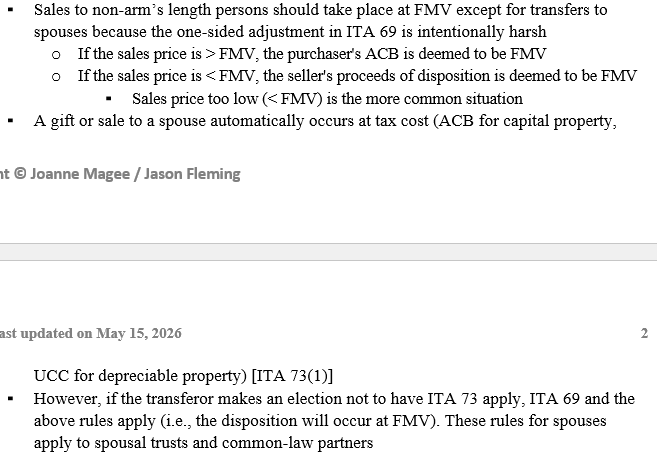

All gifts are deemed dispositions at FMV (even gifts to arm’s length persons) except for gifts to spouses

Sales to non-arm’s length persons

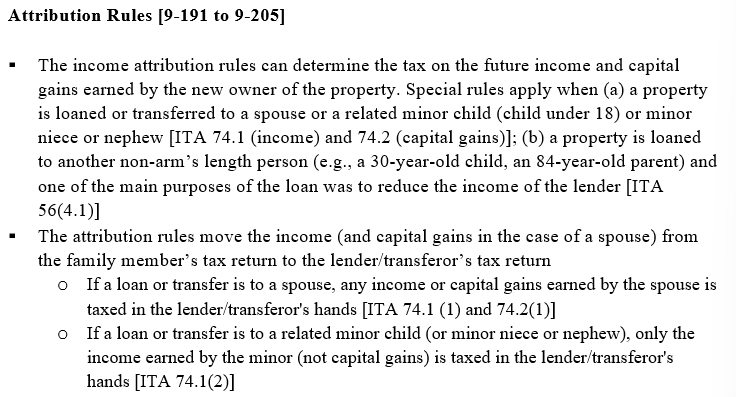

Attribution Rules

TOSI rules

To complete

Gifting family chart

To Complete

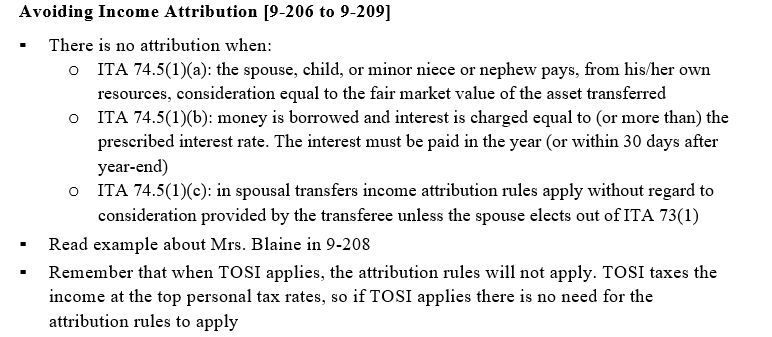

Avoiding Income Attribution Rules

Departure From Canada (Departure Tax)

▪ Taxpayers leaving the country and ceasing to be a resident of Canada must also file a list of properties owned at the time of departure with their tax return so that the CRA can verify that all deemed capital gains have been reported

▪ Five-year rule [ITA 128.1(4)(b)(iv)]

o If you have been resident in Canada less than 60 months in the last 10 years, then the deemed disposition rules will not apply to any property brought to Canada

o This rule was designed to facilitate short-term executive transfers to Canada

▪ When you become a resident of Canada, the cost of each of your capital properties (other than taxable Canadian property) for Canadian tax purposes is deemed to = FMV at the immigration date (the purpose of this rule to ensure that only capital gains accrued while being a resident of Canada are subject to Canadian tax)

![<p><span data-name="black_small_square" data-type="emoji">▪</span><span style="font-family: "Times New Roman"; line-height: normal; font-size: 7pt;"> </span><span>Taxpayers leaving the country and ceasing to be a resident of Canada must also file a list of properties owned at the time of departure with their tax return so that the CRA can verify that all deemed capital gains have been reported</span></p><p class="MsoListParagraph"><span data-name="black_small_square" data-type="emoji">▪</span><span style="font-family: "Times New Roman"; line-height: normal; font-size: 7pt;"> </span><span>Five-year rule [ITA 128.1(4)(b)(iv)]</span></p><p class="MsoListParagraph"><span style="font-family: "Courier New";">o</span><span style="font-family: "Times New Roman"; line-height: normal; font-size: 7pt;"> </span>If you have been resident in Canada less than 60 months in the last 10 years, then the deemed disposition rules will not apply to any property brought to Canada</p><p class="MsoListParagraph"><span>o</span><span style="font-family: "Times New Roman"; line-height: normal; font-size: 7pt;"> </span>This rule was designed to facilitate short-term executive transfers to Canada</p><p class="MsoListParagraph"><span data-name="black_small_square" data-type="emoji">▪</span><span style="font-family: "Times New Roman"; line-height: normal; font-size: 7pt;"> </span><span>When you become a resident of Canada, the cost of each of your capital properties (other than taxable Canadian property) for Canadian tax purposes is deemed to = FMV at the immigration date (the purpose of this rule to ensure that only capital gains accrued while being a resident of Canada are subject to Canadian tax)</span></p>](https://assets.knowt.com/user-attachments/1ac5408c-4280-45f5-81d4-ac5db573846a.png)

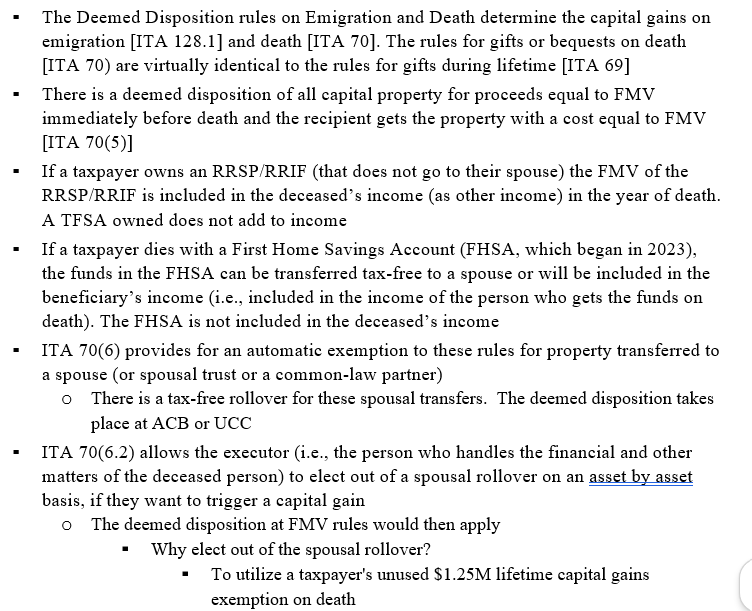

Death of a Taxpayer

Problem case at end