Regression Foundations

1/33

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

34 Terms

What is regression analysis?

A statistical tool to study the relationship between a dependent variable (y) and one or more independent variables (x)

Goal: estimate how changes in x affect y

Difference Correlation vs Causation

Correlation: x and y move together. without implying one produces the other

Example: Ice-cream sales and drownings rise together. The hidden driver is hot weather (a confounder), not ice-cream causing drownings

Causation: A change in X produces a change in Y, holding other factors constant (requires evidence of mechanism and identification)

Example: In a randomized trial, giving a vaccine to one group reduces infection rates compared with a control group—random assignment isolates the causal effect

What is the basic form of the regression model?

y=β0+β1x+u

y: dependent variable (outcome, explained, regressand)

x: independent variable (explanatory, predictor, regressor)

β0: intercept (expected y when x=0)

β1: slope (effect of x on y, holding other factors constant)

u: error term (all other unobserved influences on y)

Why do we need the error term?

Captures all unobserved factors affecting y

Recognizes that models cannot explain y perfectly

Example: Wage = β0 + β1Education + u → u includes ability, effort, luck

What are the SLR assumptions?

Assumption | Meaning | Purpose |

|---|---|---|

SLR.1 | Linearity in parameters | Ensures model can be estimated with OLS |

SLR.2 | Random sampling | Guarantees representative sample |

SLR.3 | Sample variation in x | Prevents division by 0 in β̂1 formula |

SLR.4 | Zero conditional mean (E[u | x]=0) |

SLR.5 | Homoskedasticity (Var(u | x)=σ²) |

Which assumptions ensure unbiasedness of OLS?

SLR.1–SLR.4.

Homoskedasticity (SLR.5) not needed for unbiasedness, only for efficiency

What does the zero conditional mean assumption imply?

E[u|x] = 0 → the error term is uncorrelated with the regressor

Without it, omitted variable bias occurs

Example: if ability (in u) is correlated with education (x), β̂1 is biased

What is the idea of OLS?

Find β̂0 and β̂1 that minimize the sum of squared residuals:

SSR=∑(yi−y^i)

Ensures best linear prediction of y given x.

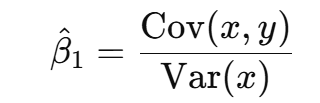

What is the formula for OLS slope in SLR?

β^1=Var(x)/Cov(x,y)

Intuition: slope is the standardized covariance between x and y.

What are the key properties of OLS residuals (with intercept)?

Sum of residuals = 0

Residuals uncorrelated with regressors.

Regression line passes through point (x̄, ȳ)

What does unbiasedness mean for OLS?

On average across repeated samples, β̂ = β

Requires assumptions SLR.1–SLR.4.

What is efficiency under Gauss–Markov?

OLS has minimum variance among all linear unbiased estimators (BLUE).

Requires assumptions SLR.1–SLR.5.

Does OLS require normally distributed errors?

No, only for exact small-sample inference

By CLT, large-sample inference works without normality

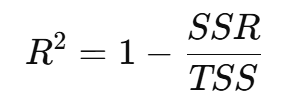

What is R²?

Proportion of variation in y explained by the model

High R² ≠ causality or unbiasedness

What is Adjusted R²?

Penalizes for adding irrelevant regressors

Can decrease when non-informative regressors are added

Can a regression with low R² still be useful?

Yes, if coefficients are unbiased and significant

Low R² common in cross-sectional data

What is the multivariate regression model?

Each βj: ceteris paribus effect of xj on y.

Why add multiple regressors?

To control for confounders

Reduce omitted variable bias

Improve interpretation of coefficients

When does OVB occur?

Omitted variable affects y

Omitted variable is correlated with included regressors

Direction of bias?

Correlation(x, omitted) | Effect of omitted on y | Bias direction |

|---|---|---|

Positive | Positive | Upward |

Positive | Negative | Downward |

Negative | Positive | Downward |

Negative | Negative | Upward |

Example of OVB?

Wage regression with education but not ability

Ability increases wages and correlates with education

Bias: upward estimate of returns to education

Effect of rescaling y by 100?

β and SE scale by 100

t-stats unchanged

R² unchanged

What does centering variables do?

Subtracting mean from x

Makes intercept represent mean outcome

Doesn’t change slope or fit

Why use quadratic terms (x²)?

To capture non-linear effects of x on y

Allows slope to change with x

Example: Wage vs. experience → concave shape.

Why include interaction terms?

To allow effect of one regressor to depend on another

Example: Wage = β0 + β1educ + β2female + β3(educ×female)

β3 = difference in returns to education for women vs me

Does high R² mean model is good?

No, spurious regressions can have high R²

Does OLS require homoskedasticity for unbiasedness?

No, only for efficiency

Does adding regressors always help?

No, irrelevant regressors inflate variance and reduce adjusted R²