PART 9-ADJUSTEMNTS AND CORRECTIONS

1/44

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai | Chat |

|---|

No analytics yet

Send a link to your students to track their progress

45 Terms

Corrections

Before the payment due date

A correction is an amendment made after the CAD is submitted and accepted, but before 11:59 PM ET on the payment due date.

ADJUSTMENT

After the payment due date

An adjustment is used after the CAD has passed its payment due date and is considered finalized.

Denied vs rejected

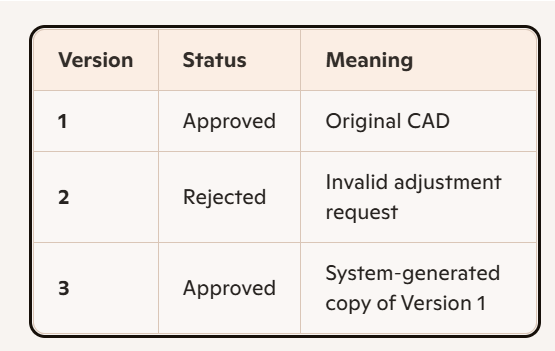

Denied adjustments will be processed similarly to rejected ones. The version submitted by the TCP will be marked as "rejected," and a new version will be created and marked as "approved." The SoAdj will show the reason code to distinguish between rejections and denials.

NO TRIGGER CBSA INTERVENTION

Changed made with the correction period are considered voluntary and interest-free, and they will not trigger CBSA intervention during this time.

Supporting documentation must be submitted

If the correction results in a reduction of the amount owed to CBSA,_____________-_________, but the supporting documents only can be attached through CCP.

Only importers enrolled in the Release prior to payment(RPP) program are eligible to make corrections.

True

CCP

Supporting documents can only be attached through the CCP

Adjustment period -need the supporting documentation

Supporting documentation is required for all changes resulting in refunds during the adjustment period and must be uploaded via the CCP.

TCP

TRADE CHAIN PARTER

Statement of Adjustment(SoAdj)

Adjustments will be reflected on a ________

There are three types of adjustments under the Customs Act:

corrections;

abatements; and

refunds.

Correction under the adjustment -May result in either a payment of addtional duties and taxes, or they may be revenue neutral.

Corrections must be made within 90 days of having “reason to believe

Abatements

An abatement is a reduction, or a decrease in the amount of duties and taxes that must be paid when the goods have suffered damage, deterioration, or destruction.

Abatements are typically a partial refund of the duties and apply to specific goods, such as fragile items and perishables. Within the industry they are referred to as refunds.

Abatements are not mandatory and are legislated under Section 73 and 74 of the Customs Act.

Abatements must be filed within 4 years.

Refunds

A refund is a return of the duties paid to the importer.

While it is permitted under the Customs Act, Sections 74 and 76, it is not mandated.

It is presumed that if monies are to be refunded an importer would be motivated to file the refund.

Refunds must be filed within 4 years.

Subsections 32.2(1); 32.2(2); or 32.2(6) of the Customs Act.

In cases where money is owing to the Receiver of General or the end result is revenue neutral, corrections or adjustments

Customs act-32.2

Applied when there are monies owed to the Receiver General or the correction is revenue neutral.

⚖ Simplified Takeaway

32.2(1): Correct FTA origin errors within 90 days.

32.2(2): Correct any origin, classification, or valuation errors (non-FTA) within 90 days.

32.2(6): Correct when goods fail to meet tariff item conditions (e.g., diverted use)

Section 74 or 76 applied

If monies are to be returned to the importer.

74(1)(a) of the customs Act

A refund cannot be filed for goods damaged after the shipment has been released.

BUT — the CSCB text adds a special rule INSIDE 74(1)(a)-“The amount of abatement allowed for perishable or brittle goods, such as glassware or china, is 85% of the duties paid on the loss in value of the goods.85% abatement for brittle goods, even if the breakage is discovered after release.

Section 74(1)(b)-Refund of Duties for Short-Shipped Goods

Purpose: Provides authority for a refund of duties when fewer goods are released than the quantity upon which duty was originally paid.

Example: Duty paid on 1,000 widgets, but only 100 actually shipped → refund claim possible.

ETA → Missing packages (whole units not shipped).

VI → Short-shipped contents inside packages (partial shortage)

2

A refund on excise tax must be filed with____years after the payment of the excise tax. Indicate your answer numerically.

90

A correction must be filed within ____days of having "reason to believe". Indicate your answer numerically.

4 years

A refund request to change the tariff classification of imported goods must be filed within ________________ of the date of accounting( the date of release)

True

A correction must be submitted electronically

3

There are____types of adjustments under the Customs Act.

SoAdj

Once an adjustment has been processed and a decision has been rendered, the CBSA will issue a

______

60 days

An importer can request a rebate of the GST on unused, importer goods that were exported within ____ days after their release

Match the legislative reference with the reason for the correction or adjustment.

|

|

Section 74

74(1)(a): Damage before release → refund/abatement.

74(1)(b): Short-shipped goods → refund.

74(1)(c): Inferior quality → refund.

74(1)(c.1)/(c.11): Missed preferential tariff treatment → refund with proof of origin.

74(1)(d): Clerical errors → refund.

74(1)(e): Errors in origin/classification/value → refund.

74(1)(f): End-use/end-user change → refund.

74(1)(g): Retroactive tariff change, prohibition, or duplicate duty → refund.

abatement

An______

is a reduction, or decrease in the amount of duties and taxes that must be paid when the goods have suffered damage, deterioration, or destruction.

Section 76(1) vs section 74

Section 76(1)

Legislative authority for an abatement or refund of duty paid on goods that are defective, inferior in quality, or not as ordered. Goods must be disposed of or exported from Canada, which distinguishes it from Section 74 refund claims.

4 years

under Subsection 32.2(4) of the Customs Act, there is still an obligation to make a correction, even after 90 days has passed. That obligation ends _____ after accounting and any corrections made after the 90-day time period and before the four years from the date of accounting are subject to penalties under the AMPS.

Flash Card Summary — GST & Duty Refunds

CBSA vs CRA Roles

CBSA refunds duties (Customs Act s.73, 74, 76).

CRA handles GST/HST rebates (Excise Tax Act s.215.1).

CBSA does not refund GST directly.

GST Registrants

Claim Input Tax Credit (ITC) on GST paid at import.

Processed outside CARM, not shown as credits in importer’s CARM account.

Non‑Registrants

Cannot claim ITCs.

Must file Form GST189 (General Application for Rebate of GST/HST).

Broker can file GST189 with written authority.

Rebate Provisions (Excise Tax Act)

215.1(1): Returned goods → exported back to supplier within 60 days, unused, rebate claim within 2 years.

215.1(2): Damaged/defective goods → CBSA duty refund granted, no warranty replacement, rebate claim within 2 years.

Corrections vs Adjustments (GST context)

Corrections (s.32.2): Mandatory if GST status code was wrong (e.g., taxable vs exempt). Must be filed within 90 days of “reason to believe.”

Adjustments (s.74/76): After payment deadline, within 4 years. Can trigger CRA rebate if CBSA’s duty refund changes GST amount.

Excise Tax Refund (Sections 68 & 69, Excise Tax Act)

Refund of excise taxes paid in error or overpaid, including excise tax on goods later exported.

Claimed using Form N15.

Must be filed within 2 years of excise tax payment.

Filed with CRA (CBSA only collects the tax, CRA administers refunds).

The Voluntary Disclosure Program (VDP)

______________ is a mechanism intended to encourage voluntary compliance with the accounting and payment of duty and tax provisions under the Customs Act, Customs Tariff Act and Excise Tax Act. Its application is limited to penalty and interest charges resulting from infractions of the provisions governing accounting and payment.

Deemed determination/appeals

58(1)-non-commercial goods-officer may determine the origin, tariff classification, and value of imported goods before they are accounted.

58(2)-commercial goods-

59(1) the customs Act-allow an officer to make a re-determination or further re-determination.

59(2)- give notice of the decision

60-President of the CBSA

67-CITT

68(1)-Federal Court of Appeal

68(2)- supreme court of Canada

question of law.

importer may only appeal a CITT decision on a ______

TRUE

Before an importer can dispute a final report, they must first make any necessary corrections and the SoAdj must be paid

False

The Voluntary Disclosure Program (VPD) reduces the amount of duties and taxes owing.

2

A mass adjustment request consists of_____or more transactions. Indicate your answer numerically.

TRUE

A Multi-Program Verification is an example of a targeted audit.

2( Random, targeted)

There are______types of audits that the CBSA may utilize. Indicate your answer numerically.

68(1)

Appeals to the Federal Court of Appeal on questions of law are made under Section ____ of the Customs Act.

30

An importer has up to_____days to respond with additional information once an interim report to an audit has been issued.

After the implementation of CARM, corrections or adjustments file electronically.

YES

CBSA Audits

Types:

Random audits → selected without specific reason.

Targeted audits → focus on high‑risk tariff, origin, or valuation issues (priorities published twice yearly).

Methods: Questionnaire, verification letter, verification visit, or review of importer’s records.

Forms:

Multi‑Program Verification (MPV): On‑site, multiple issues (tariff + origin + valuation).

Single Program Verification (SPV): Usually desk audit, one issue only (e.g., classification of a commodity).

Process: Notice → documentation request (CAD, invoices, permits) → interim report (30 days for response) → final report with findings and corrective measures.

Outcome: Could be no findings, minor errors, refunds, interpretative errors (1 year back corrections), or obvious errors (4 years back corrections + AMPs penalties).