Econ Chapter 5 Elasticity

1/28

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

29 Terms

elasticity

measure of how much one economic variable responds to changes in another economic variable

price elasticity of demand/supply

the responsiveness of the quantity demanded/supplied to a change in price

price elasticity formula

% in quantity demanded or supplied

% change in price

elastic demand or supply

when % change in quantity is GREATER than the % change in price

inelastic demand or supply

when the % change in quantity is LESS than the % change in price

unitary elastic demand or supply

when the % change in quantity EQUALS the % change in price

midpoint formula

for price elasticity

steeper slope

less elastic

flatter slope

more elastic

if a product has MORE substitutes available…

it will have MORE elastic demand

if a product has LESS substitutes available…

it will have LESS elastic demand

the MORE time passes…

the MORE elastic demand for a product becomes

the demand curve for a LUXURY is…

MORE elastic than the demand curve for a NECESSITY

the MORE narrowly a market is defined…

the MORE elastic demand will be

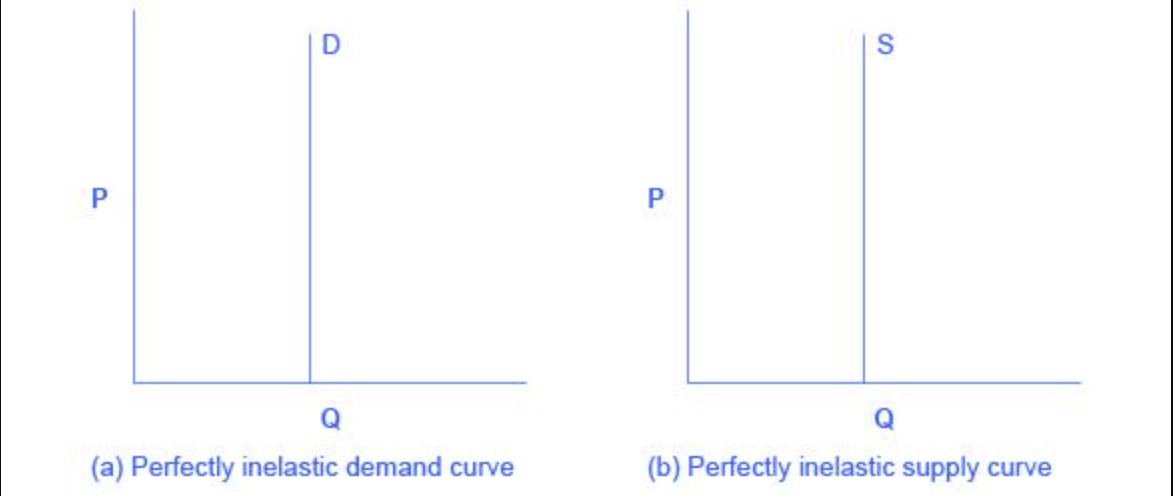

perfectly inelastic demand/supply

when the quantity is completely unresponsive to price and price elasticity = 0

perfectly elastic demand/supply

when quantity is infinitely responsive to price, and the price elasticity = infinity

constant unitary elasticity

when a price change of 1% results in a quantity change of 1%

total revenue

total amount of funds received by a seller of a good or service (Total revenue = Price x Quantity)

excise tax

a wedge between the price paid by consumers and the price received by producers

when demand is more elastic than supply…

the tax incidence on consumers is lower than producers

when supply is more elastic than demand…

the tax incidence on consumers is larger than producers

cross-price elasticity

the % change in quantity demanded of one good divided by the % change in the price of another good

income elasticity

% change in quantity demanded divided by % change in income

if products are substitutes…

the cross price elasticity will be positive

if products are complements…

the cross price elasticity will be negative

if products are unrelated…

the cross price elasticity will be 0

if income elasticity is positive but LESS than 1…

then the good is normal and a necessity

if income elasticity is positive and MORE than 1…

the the good is normal and a luxury

if income elasticity is negative…

then the good is inferior