far F6

1/54

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai | Chat |

|---|

No analytics yet

Send a link to your students to track their progress

55 Terms

goal of NFP reporting

disclose the sources of the NFPs resources & how they were expended

CECL formula weird shi

Beg Balance

-write offs

+recoveries

+credit loss expense

= ending balance

where are unrestricted donations (cash flows) listed on the SCF?

CFO, unlike RESTRICTED donations

can expenses have donor restrictions? (NFPs)

FUH NAH

3 req’d statements for an NFP: (+1 more)

statement of financial position (BS)

statement of activity (IS & statement of changes in RE)

SCF

functional expenses

where should the relationships between functional & natural classifications of expenses be?

face of activities statement, OR

schedule in notes, OR

its own separate FS

functional vs natural expenses

func

program services related to purpose & mission

support services, i.e. mgmt, general, fundraising, etc

natural

regular gaap stuff like rent, salaries, supplies, utilities, etc

what are the 2 main diffs between a regular IS and a statement of activity for NFPs?

reclassification of net assets (AKA equity) is presented

order of accounts (revs, exp) can be presented however they want

where are items that would normally be OCI shown on the statement of activity for NFPs?

below op inc

NFP SCF direct method

unlike for-profit companies, if an NFP uses the direct method on the SCF, they DONT have to reconcile it to the indirect method

where on the SCF are incoming funds listed that are INTERNALLY designated as an investing / financing activity?

CFO until they’re actually used, then it would be CFI/CFF

funds that are EXTERNALLY designated for CFI

CFF, so long as funds are externally restricted, they are CFF

what is in CFI aside from obvious PPE / investment stuff?

purch / sale of art

what is in CFF aside from obvious stuff?

endowment fund stuff

unconditional cntbns (rev or gain?)

REV

part of core ongoing operations of the NFP

GAIN

incidental, not part of the core purpose

when are conditional cntbns rec’d?

only when the condition is met

pledges (conditional vs unconditional?)

CON:

Dr Cash, Cr Refundable advance

UNCON:

rec at NPV if >1yr, FV is <1yr, can be verbal or in writing

placed in service (i.e. donations of PPE) (restricted vs unrestricted?)

RESTRICTED:

basically depr its value over the useful life from restricted net assets to unrestricted net assets

UNRESTRICTED:

just rec as a normal unrestricted asset

allowance for uncollectible pledges

on SoA:

pledge reported net of allowance (i.e. allowance amount not even shown, only net amount is shown)

on SFP:

pledge amount and the allowance amount are shown

split interest agreements (SIAs)

rec’d @ PV as donor restricted asset until the other beneficiaries have received their stuff

big idea here is that all SIAs should be disclosed & any cntbns / value changes are a line item on the SoA

donated services (SOME acronym)

they are only rec’d SOME of the time

S: Specialized skills

O: Otherwise needed by the org (they were going to have to purchase it anyway)

M / E: easily measurable

all of these components must be met, rec’d as nonoperating rev

donation of collected items (when do you not have to rec them?)

dont have to rec when all 3 are met:

1) item is part of a collection of items held for the public / education / research

2) it’s cared for, preserved, and protected

3) org req’s that any proceeds from the sale of the items are used for: reinvesting in other items / support the care of existing items

extraordinary long-lived items

i.e. mona lisa

dont need to depr

donated materials (when rec’d vs not rec’d?)

if used for operations

rec’d @ FV

if passed through to a beneficiary

not rec’d unless its a SUBSTANTIAL amount

unconditional cntbn promises that will be cntbn’d in the future

rec’d as donor restricted (implied time restriction)

rec’d at PV

Dr Pledge receivable, Cr Allowance for doubtful accounts, Cr cntbns - restricted

educational institution revenues

reported net ONLY of any refunded amounts, be careful of scholarships tho

healthcare rev rec

rec the usual & customary fees for services LESS: charitable services

NOTE: do NOT factor in allowance for doubtful accounts for revenue

3 buckets of healthcare rev:

1) patient service rev (obv)

2) other operating rev (gift shop, etc)

3) nonop rev (incl. donated services)

2 treatments for credit losses for healthcare:

Op expense:

when you fail to collect revs that you initially thought you would collect

deducted from rev:

when you fail to collect revs that you never assessed for collectibility

3 primary users of govt FS

citizens, legislative / oversight groups, and investors / creditors

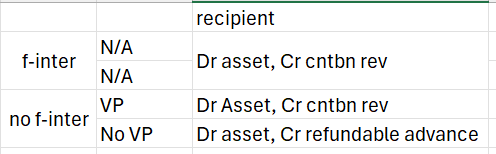

JEs for financial interrelationships (Y/N) and variance power (Y/N)

F, NF, X, X, VP, NVP, AC, AC, A-RA

what is variance power

the ability to override donor instructions without approval

underwater endowment (what is it? +FED acronym, easy)

this is when the FV of an endowment falls below its initial FV

FED (req’d disclosures):

F: FV of the underwater endowment

E: endowment’s original FV

D: deficiency (amount)

what are the 3 main fund types for govt accounting

govt funds

proprietary funds

fiduciary funds

how must fund FS be presented compared to govt-wide FS?

fund FS must be presented separately for all included fund types, alongside the govt wide FS

accounting equation for govt funds

(CAs + deferred outflows) = (CLs + deferred inflows) + fund balance

what funds are incl. in govt funds? (GRaSPP)

General fund

special Revenue fund

(and)

debt Service fund

capital Project fund

Permanent fund

what basis is GRaSPP accounted for in? what makes it different from full accrual?

modified accrual

diff bc it is focused ONLY on current resources, so only CAs and CLs. No PPE / LT debt / obligations

general fund

GRaSPP / govt funds

incl. taxes and other general revs, basically a ‘catch all’

special rev funds

GRaSPP / govt funds

specific taxes, restricted for particular activities

debt service funds

GRaSPP / govt funds

int / principle pmts (unless done by an enterprise fund)

capital project fund

GRaSPP / govt funds

PPE acquisitions and projects, unless done by enterprise fund

permanent fund

GRaSPP / govt funds

like an endowment; principal cant be touched but generated income can be used

statement of revs, expenses, and changes in fund balance equation for funds (basically IS)

revs

less: expenses

less: other financing uses

= net change in fund balance

SE-CIPPOE

proprietary funds

S: internal Services fund

E: enterprise fund

Fiduciary funds (trusts)

C: custodial funds

I: investment trust funds

P: private purpose trust fund

P: pension trust fund

O/E: other employment funds

what are proprietary funds

basically like a business, full accrual basis

focus on economic resource measurement

what are fiduciary funds

AKA trust funds

accounting for assets controlled by a govt on behalf of a beneficiary

full accrual, focused on economic resource measurement

internal services fund

proprietary / full accrual

customers of this fund are primarily internal, i.e. building maintenance dept or something

enterprise fund

proprietary / full accrual

customers mainly external, mainly for the acquisition and operation of PPE. it is mainly self supported by user charges, i.e. airports, transit, etc

incl. anything that supports itself with the fees it charges

custodial funds

fiduciary / full accrual

catch all for fiduciary stuff, incl. taxes collected for another entity

investment trust fund

fiduciary / full accrual

external investment pools

private purpose trust fund

fiduciary / full accrual

basically anything that ISN’T a pension / investment, assets here are protected from creditors

pension trust funds

fiduciary / full accrual

incl. defined benefit plans, cntbn plans, basically any benefit plan.

other employement funds

fiduciary / full accrual

in the name yo!

GRaSPP accounting quirks (AKA modified accrual, when is rev rec’d? what about expenditures?)

rev:

rec’d when AVAILABLE and MEASURABLE

available = collectible within the current period OR soon enough thereafter to pay current period liabs (usually 60d)

expenditures:

generally rec’d when incurred EXCEPT:

debt exp (int & princ) aren’t rec’d until due or paid