Discuss/Analyse/Explain Qs- Reports, Indicators and Costs

1/9

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced |

|---|

No study sessions yet.

10 Terms

Explain, giving two examples, how the business’s Net Profit can be higher than its Net Cash Flow from Operating Activities.

• Payments to account payables > cost of sales.

• GST settlement in August= no effect on profit but it reduces net cash flows from operating activities.

• Profit on disposal of asset increases net profit, but is not an operating activity so no effect.

• Accrued revenue will increase net profit but no corresponding cash inflow is recorded in Operating

Explain why a business may use FIFO.

FIFO inventory cost assignment method allocates the cost of inventory assuming the first inventory to arrive is the first to leave the business.

Type of inventory: identical items but purchase price is different, so inventory can’t be separately identified.

Benefit: easier and cheaper to implement as it does not require the business to separately identify the cost price of each item of inventory when it leaves the business.

Explain the purpose of recording from source documents with reference to one QC.

Verifiability: different knowledgeable and independent observers being able to reach a consensus that a particular depiction of an event is faithfully represented

Cross-checking mechanism.

Explain the purpose of a post-adjustment trial balance.

A post-adjustment trial balance is a list of the debit and credit balances of ledger accounts after recording balance day adjustments.

The purpose is to ensure debits match credits so the trial balance balances, whilst identifying errors in recording.

For instance, the error of recording two debits instead of one debit and one credit will be able to be identified.

However, some errors such as transposition errors that lead to a matching credit and debit entry may not be identified. OR swapping credit and debit entries.

Justify why the accountant is correct in saying a positive net cash flow from operating activities is vital for the business.

What a positive net cash flow from operating is: cash surplus from its day-to-day trading activities.

Important parts: required to fund the purchase of non-current assets, meet the loan repayments of the business and cash for drawings. aka meet short term debts

Describe why we have to rely on Operating: Investing and financing activities may provide surplus cash but it is not sustainable to take out new loans or receive capital contributions

Key term: Justify

Key terms: Analyse

Identify trends and relationships within the data and graphs provided.

Don’t restate stats, just state “increase/decrease” etc.

Key terms: Discuss

Pros and cons- must have one of each

Relate back to non-financial information!!

If it says ethical AND financial considerations- must have one of each

Ethical- think about non-financial information as well

Key terms: Explain

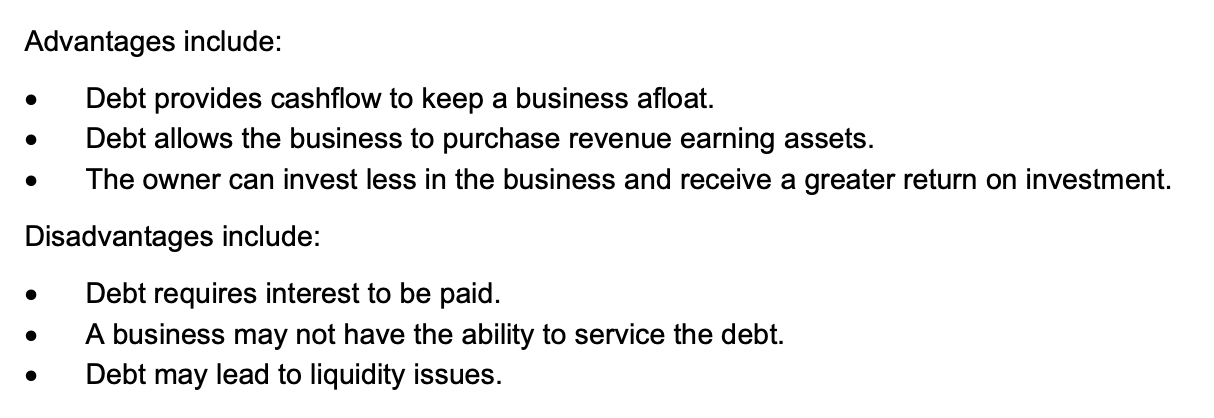

Explain the advantages and disadvantages of taking on debt/having a high debt ratio