ECE 192 - Cash Flow Analysis

1/20

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai | Chat |

|---|

No analytics yet

Send a link to your students to track their progress

21 Terms

single cash flow definition/examples =

non-recurring costs:

purchasing equipment, salvage value, investments

compound amount factor =

(F/P, i, N) = (1 + i)N

gives the future amount F given:

P = present amount

i = interest rate

N = # periods to go to F

present worth factor =

P(F, i, N) = 1/(1 + i)N

gives the present amount P given:

F = future amount

i = interest rate

N = # periods to go BACK to P

compound amount factor is the inverse of =

present worth factor

annuity definition/examples =

uniform series of cash flows over N periods (starts at end of 1st period)

receipts (money in)

rent income

stock dividends

pension

disbursements (money out)

insurance premiums

mortgages

operations and maintenance costs

NOTE: receipt/disbursements represent a SINGLE payment out of the ANNUITY

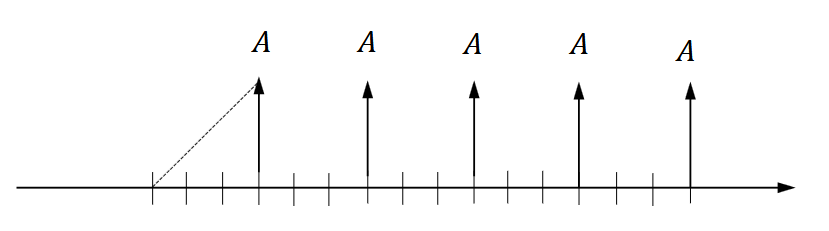

uniform series compound amount factor =

(F/A, i, N) = [(1 + i)N - 1]/i

gives the future value F for an annuity given:

A = amount of a single payment

i = interest rate

N = # of periods

![<p>(F/A, i, N) = [(1 + i)<sup>N</sup> - 1]/i</p><p></p><p>gives the future value F for an annuity given:</p><ul><li><p>A = amount of a single payment</p></li><li><p>i = interest rate</p></li><li><p>N = # of periods</p></li></ul><p></p>](https://assets.knowt.com/user-attachments/9768c2b9-cbf0-44d4-999a-18746d733c7e.png)

sinking fund factor

(A/F, i, N) = i/[(1 + i)N - 1]

gives the size of the receipt/disbursement A that is equivalent to F given:

F = future amount

i = interest rate

N = # of periods

![<p>(A/F, i, N) = i/[(1 + i)<sup>N</sup> - 1]</p><p></p><p>gives the size of the receipt/disbursement A that is equivalent to F given:</p><ul><li><p>F = future amount</p></li><li><p>i = interest rate</p></li><li><p>N = # of periods</p></li></ul><p></p>](https://assets.knowt.com/user-attachments/eb914fe2-44ad-45d5-b047-4acfde94fb2c.png)

uniform series compound factor is the inverse of =

sinking fund factor

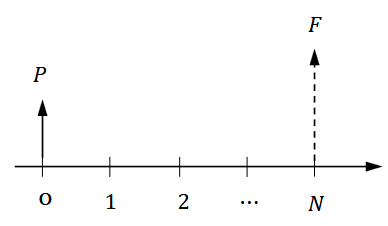

capital recovery factor =

(A/P, i, N) = [i(1 + i)N] / [(1 + i)N - 1]

gives the size of receipt/disbursement A equivalent to P given:

P = present amount

i = interest rate

N = # of periods

“What N payments of A is worth the same as a lump sum of P today, given i% interest yearly?”

![<p>(A/P, i, N) = [i(1 + i)<sup>N</sup>] / [(1 + i)<sup>N</sup> - 1]</p><p></p><p>gives the size of receipt/disbursement A equivalent to P given:</p><ul><li><p>P = present amount</p></li><li><p>i = interest rate</p></li><li><p>N = # of periods </p></li></ul><p></p><p>“What N payments of A is worth the same as a lump sum of P today, given i% interest yearly?”</p>](https://assets.knowt.com/user-attachments/99d276d9-c410-49f2-9df9-96f28306a16b.png)

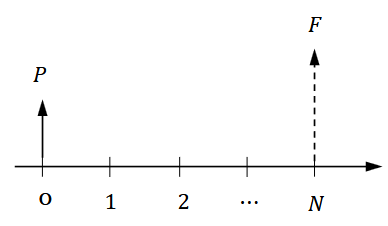

series present worth factor =

(P/A, i, N) = [(1 + i)N - 1] / [i(1 + i)N]

gives the present amount P equivalent to A given:

A = size of receipt/disbursement

i = interest rate

N = # periods

“What lump sum P today is worth the same as N payments of A, given i% interest yearly?”

![<p>(P/A, i, N) = [(1 + i)<sup>N</sup> - 1] / [i(1 + i)<sup>N</sup>] </p><p></p><p>gives the present amount P equivalent to A given:</p><ul><li><p>A = size of receipt/disbursement</p></li><li><p>i = interest rate</p></li><li><p>N = # periods</p></li></ul><p></p><p>“What lump sum P today is worth the same as N payments of A, given i% interest yearly?”</p>](https://assets.knowt.com/user-attachments/6deb6391-585d-450b-ba5d-b9da70d6dfbb.png)

capital recovery factor is the inverse of =

series present worth factor

bisection and linear approximation method to find is =

get function for f(is) = P(is) - P

bisection method

find two intervals that have f(is1) > 0 and f(is2) < 0 respectively

evaluate f([is2 + is1]/ 2)

if > 0, then lower bound is [is2 + is1]/ 2

if < 0, then upper bound is [is2 + is1]/ 2

repeat until f(is) ≈ 0

linear approximation method:

x* = x₁ + (x₂ − x₁) × [y* − y₁] / [y₂ − y₁]

x = Compound interest rate is

y = f(x) = f(is)

y* = 0

can use bisection → linear approximation to save time

![<p>get function for f(i<sub>s</sub>) = P(i<sub>s</sub>) - P</p><p></p><p> bisection method</p><ul><li><p>find two intervals that have f(i<sub>s1</sub>) > 0 and f(i<sub>s2</sub>) < 0 respectively</p></li><li><p>evaluate f([i<sub>s2 </sub>+ i<sub>s1</sub>]/ 2)</p><ul><li><p>if > 0, then lower bound is [i<sub>s2 </sub>+ i<sub>s1</sub>]/ 2</p></li><li><p>if < 0, then upper bound is [i<sub>s2 </sub>+ i<sub>s1</sub>]/ 2</p></li></ul></li><li><p>repeat until f(i<sub>s</sub>) ≈ 0</p></li></ul><p></p><p>linear approximation method:</p><ul><li><p>x* = x₁ + (x₂ − x₁) × [y* − y₁] / [y₂ − y₁]</p><ul><li><p>x = Compound interest rate i<sub>s</sub></p></li><li><p>y = f(x) = f(i<sub>s</sub>)</p></li><li><p>y* = 0</p></li></ul></li></ul><p></p><p>can use bisection → linear approximation to save time</p>](https://assets.knowt.com/user-attachments/6e4e7a73-f068-4b4b-b21f-9520fe4dc061.png)

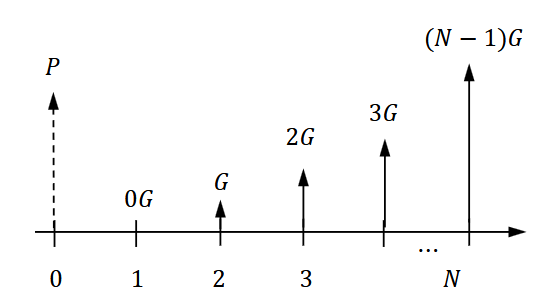

arithmetic gradient series =

series of constantly increasing receipts/disbursements

end of 1st period = 0

arithmetic gradient present value factor =

(P/G, i, N) = [(1+i)N − iN − 1] / [i²(1+i)N]

gives the present amount P equivalent to constantly increasing G per period given:

G = constant increase in receipt/disbursement

i = interest rate

N = # of periods

“What lump sum P is worth the same as a series of payments that starts at 0 in period 1 and increases by a constant amount G each period after, given interest rate i per period over N periods?"

![<p>(P/G, i, N) = [(1+i)<sup>N</sup> − iN − 1] / [i²(1+i)<sup>N</sup>]</p><p></p><p>gives the present amount P equivalent to constantly increasing G per period given:</p><ul><li><p>G = constant increase in receipt/disbursement</p></li><li><p>i = interest rate</p></li><li><p>N = # of periods</p></li></ul><p></p><p>“What lump sum P is worth the same as a series of payments that starts at 0 in period 1 and increases by a constant amount G each period after, given interest rate i per period over <span>N</span> periods?"</p>](https://assets.knowt.com/user-attachments/93b5c21a-5e5f-4dc1-a27e-e9519c5b8dd0.png)

arithmetic gradient uniform series factor =

(A/G, i, N) = [1/i] − [N/((1+i)N − 1)]

gives the annuity A equivalent to arithmetic gradient series G given:

G = constant increase in receipt/disbursements

i = interest rate

N = # of periods

“What annuity A is worth the same as a series of payments that start at 0 in period 1 and increases by a constant G each period after, given interest rate i per period over N periods?”

![<p>(A/G, i, N) = [1/i] − [N/((1+i)<sup>N </sup>− 1)]</p><p></p><p>gives the annuity A equivalent to arithmetic gradient series G given:</p><ul><li><p>G = constant increase in receipt/disbursements</p></li><li><p>i = interest rate</p></li><li><p>N = # of periods</p></li></ul><p></p><p>“What annuity A is worth the same as a series of payments that start at 0 in period 1 and increases by a constant G each period after, given interest rate i per period over N periods?”</p>](https://assets.knowt.com/user-attachments/797ce49b-0d35-4c56-9441-1f5d213bff44.png)

combined annuity =

AT = A' + G[1/i − N/((1+i)N − 1)]

gives the annuity AT equivalent to an annuity A’ and arithmetic gradient series G given:

A’ = annuity

G = constant increase in receipts/disbursements

i = interest rate

N = # of periods

“What total annuity is worth the same as the sum of an annuity and a series of payments that start at 0 and increase by a constant G each period after, given interest rate i and per period over N periods?”

![<p>A<sub>T</sub> = A' + G[1/i − N/((1+i)<sup>N</sup> − 1)]</p><p></p><p>gives the annuity A<sub>T</sub> equivalent to an annuity A’ and arithmetic gradient series G given:</p><ul><li><p>A’ = annuity</p></li><li><p>G = constant increase in receipts/disbursements</p></li><li><p>i = interest rate</p></li><li><p>N = # of periods</p></li></ul><p></p><p>“What total annuity is worth the same as the sum of an annuity and a series of payments that start at 0 and increase by a constant G each period after, given interest rate i and per period over N periods?”</p>](https://assets.knowt.com/user-attachments/442b615b-87a8-47e6-923a-aafc6fcdf80f.png)

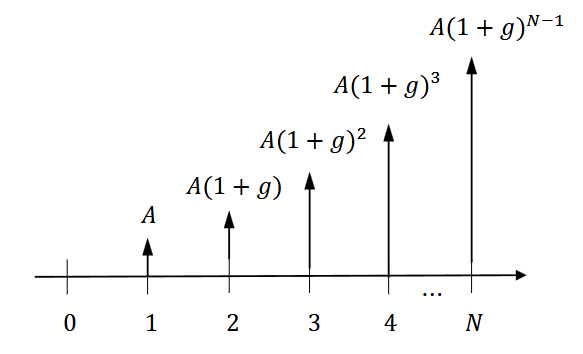

geometric gradient series =

series of cash flows that increase/decrease by a % each period

ex.) inflation/deflation, productivity improvement

base value = A

rate of growth = g

growth adjusted interest rate =

i° = (1+i)/(1+g) − 1

interest rate with growth rate accounted for:

can be used to convert to annuity problem

geometric gradient → present worth factor =

i° = (1+i)/(1+g) − 1

(P/A, g, i, N) = [(P/A, i°, N)] / (1+g) = [((1+i°)N − 1) / (i°(1+i°)N)] × [1/(1+g)]

gives the present amount P equivalent to a geometric gradient series g given:

A = base value of geometric gradient series

g = rate of growth

i = interest rate

N = # of periods

“What lump sum P is worth the same as a geometric gradient series with interest rate i and per period over N periods?”

![<p>i° = (1+i)/(1+g) − 1</p><p>(P/A, g, i, N) = [(P/A, i°, N)] / (1+g) = [((1+i°)<sup>N</sup> − 1) / (i°(1+i°)<sup>N</sup>)] × [1/(1+g)]</p><p></p><p>gives the present amount P equivalent to a geometric gradient series g given:</p><ul><li><p>A = base value of geometric gradient series</p></li><li><p>g = rate of growth</p></li><li><p>i = interest rate</p></li><li><p>N = # of periods</p></li></ul><p></p><p>“What lump sum P is worth the same as a geometric gradient series with interest rate i and per period over N periods?”</p><p></p>](https://assets.knowt.com/user-attachments/27c670af-47b2-490b-a7ee-34f16597fcb0.png)

what happens if compounding and payment periods dont match =

non-standard annuities/gradients

ex.)

interest compounds monthly, but you only make payments quarterly

interest compounds daily, but you make payments annually

3 methods to solve non-standard annuities/gradients =

treat each cash flow in the annuity/gradient individually

convert to standard annuity/gradient by changing compounding period

convert to standard annuity/gradient by finding equivalent standard annuity/gradient for the compounding period