Market Structures and Monopoly: Key Concepts and Strategies

1/27

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced |

|---|

No study sessions yet.

28 Terms

Monopoly

a firm that is the sole seller of a product without close substitutes

-price maker

-arises due to barriers to entry, other firms cant enter the market to compete.

Barriers to Entry

monopoly resources, government regulation, production process: natural monopoly

Competitive Firm Demand Curve

Horizontal (perfectly elastic)

The firm can increase Q without lowering P

MR=P

Monopolist demand curve

to sell a larger Q, the firm must reduce P. Thus, MR ≠ P

profit maximizing price

MR=MC

Marginal Revenue

the change in total revenue from an additional unit sold

Average Revenue

TR/Q

profit

(P-ATC) x Q

Has a supply curve that shows how its Q depends on P

competitive firm

Q and P are jointly determined by MC, MR, and the demand curve

Hence, no supply curve for ______

monopoly

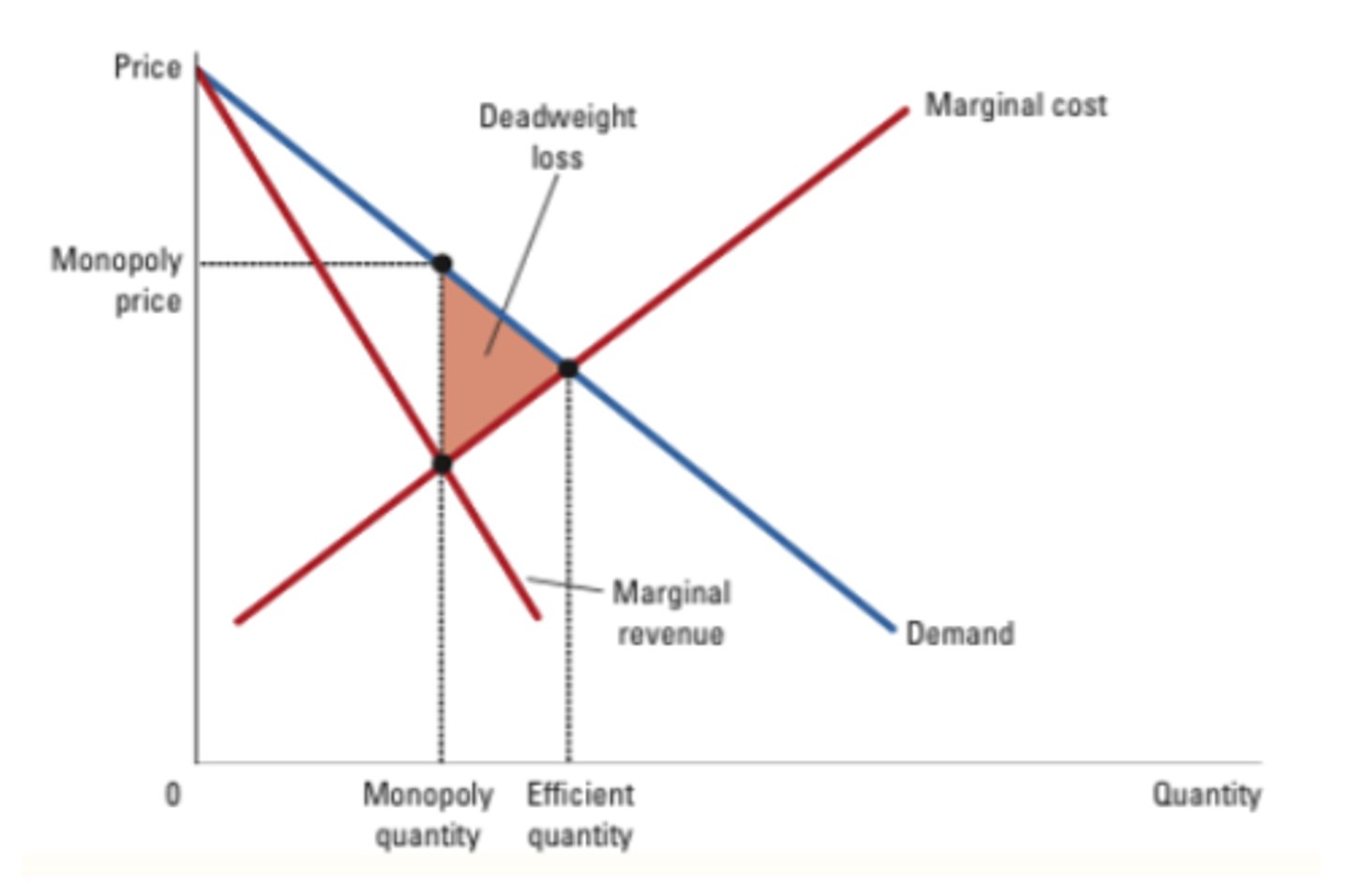

deadweight loss

the reduction in economic surplus resulting from a market not being in competitive equilibrium

Monopolys can be inefficient because

-Monopoly produces Q < efficient quantity

-Deadweight loss

Price discrimination (price customization)

- Sell the same good at different prices to different customers

- A firm can increase profit by charging a higher price to buyers with higher willingness to pay

- Requires the ability to separate customers according to their willingness to pay

- Can raise economic welfare

price discrimination formula

tr 1 + tr2 (q2-q1 * p ) - tc

perfect competition

p=mc

monopoly

p > mc

oligopoly

A market structure in which a few large firms dominate a market

monopolistic competition

a market structure in which many companies sell products that are similar but not identical

Concentration ratio

the percentage of the market's total output supplied by its four largest firms

-less than 50% for most markets

short-run profits

•New firms enter the market

•More product variety available

•Demand for each firm decreases

•Prices fall and profits decline to zero

short-run losses

•Some firms exit the market

•Remaining firms face higher demand

•Prices rise

long run

•Price = Average Total Cost = zero economic profit

•Firms charge a markup over marginal cost

•Firms do not produce at minimum ATC = not fully efficient

When oligopoly's are making decisions they take int o account

P or Q can affect other firms and cause them to react

Game theory

the study of how people behave in strategic situations

Oligopolist make the most profit when they...

cooperate and together act like one big monopolist

duopoly

a market with only 2 sellers

simplest type of oligopoly

collusion

agreement among firms in a market about quantities to produce or prices to charge

cartel

a group of firms acting in unison