Micro economics chapter 10 (The market: good or bad?)

1/20

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced |

|---|

No study sessions yet.

21 Terms

What happens in a pure command system?

A central government determines what should be produced, how production should be organzed, and who receives what goods and services

What problems do command systems face? 2

Information problems: in an advanced economy, a large number of decisions have to be made regarding production and consumption.

Incentive problems: When economic agents compensation is not clearly linked to their effort, they will also tend to put less effort in.

Explain a market system (5)

Production and distribution take place on the basis of the decisions of individual firms and households.

A market system is built on the basic principle of voluntary exchange.

In a market economy decisions of different economic agents are coordinated with prices.

Everyone tries to achieve the best outcome for themselves

Prices respond to changes in the social and economic environment

The signal value of prices is the strength of the market system

What is the signal value of prices?

The signal value of prices refers to how prices convey information to economic agents about the relative scarcity and demand for goods and services, guiding their production and consumption decisions.

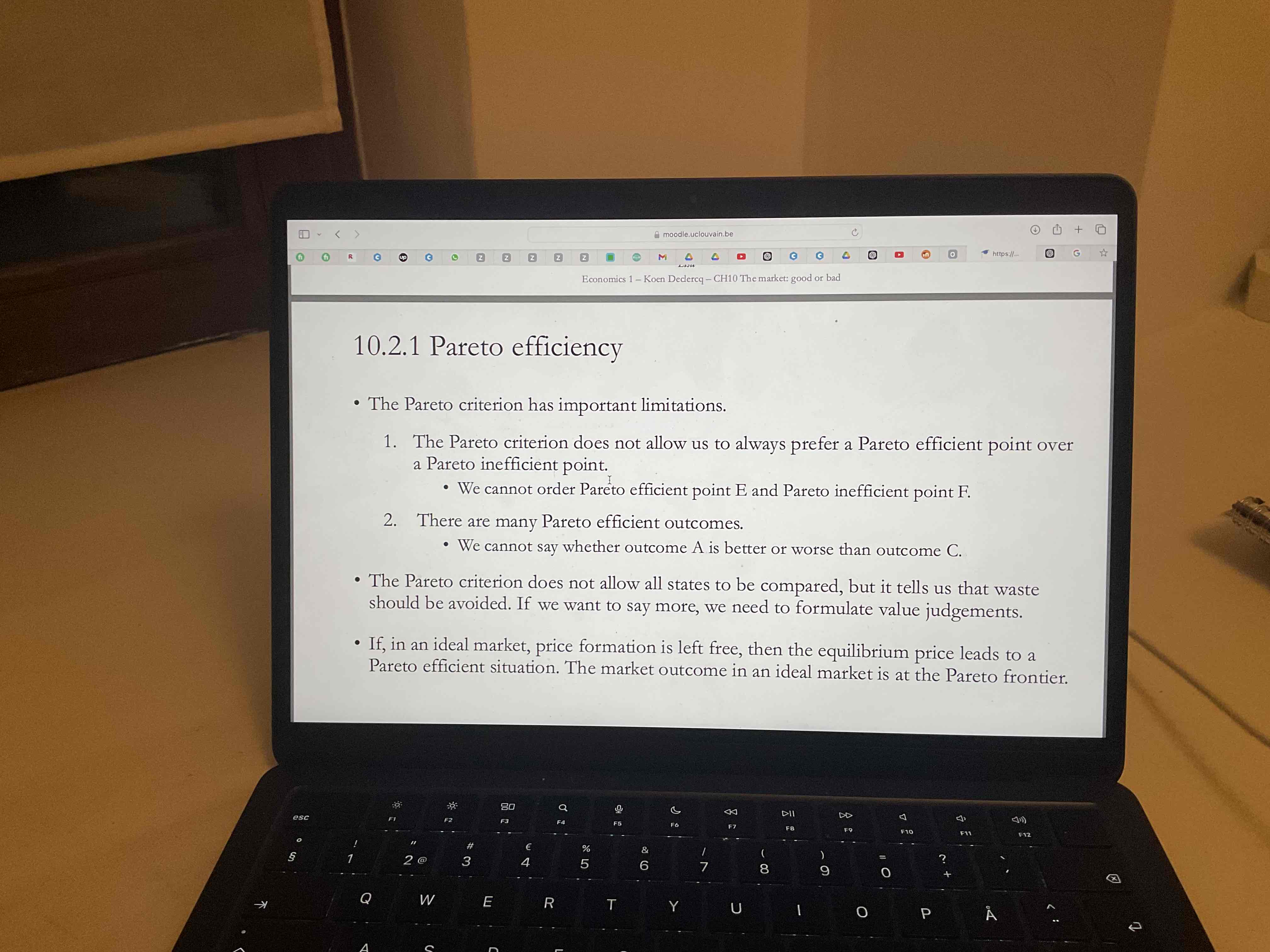

What is Pareto efficiency?

Pareto efficiency, or Pareto optimality, is a state in which resources are allocated in the most efficient manner, such that no individual's situation can be improved without worsening another's situation. This means that any attempt to improve one person's situation would result in a detriment to someone else's. In a Pareto efficient allocation, it is impossible to make someone better off without making someone else worse off, highlighting the trade-offs and opportunity costs involved in resource allocation. Achieving Pareto efficiency does not imply an equitable distribution of resources; rather, it focuses solely on Pareto improvements in welfare.

What are the two important limitations of the Pareto criterion?

What is consumer surplus?

Consumer surplus is the difference between what consumers are willing to pay for a good or service and what they actually pay, representing the benefit to consumers.

What is producer surplus?

Producer surplus is the difference between what producers are willing to accept for a good or service and the actual price they receive, representing the benefit to producers.

What is the first fundamental theorem of welfare economics?

The first fundamental theorem of welfare economics states that under certain conditions (such as complete markets, perfect competition, and rational behavior), any competitive equilibrium will lead to a Pareto efficient allocation of resources. This means that it is impossible to make one individual better off without making another worse off. The theorem highlights the efficiency of market outcomes while also indicating the importance of appropriate market conditions for achieving this efficiency.

What is the social optimum?

The social optimum is the allocation of resources that maximizes overall societal welfare, taking into account both the benefits and costs to all members of society, ensuring that no one can be made better off without making someone else worse off.

What is equitable distribution of welfare?

Equitable distribution of welfare refers to the fair allocation of resources and benefits within a society, ensuring that all individuals or groups have access to an adequate level of welfare without unfair disparities.

What is a monopoly?

A monopoly is a market structure where a single seller or producer controls the entire supply of a good or service, leading to a lack of competition and significant pricing power.

What is a monopsony?

A monopsony is a market structure in which there is only one buyer for a good or service, giving that buyer significant control over the price and supply.

What are private goods

Goods consumed by one consumer ex. Sandwich

What are public goods?

Public goods are goods that are non-excludable and non-rivalrous, meaning that they are available for everyone to consume, and one person's consumption does not reduce availability for others. Examples include clean air and national defense.

When do externalities arise?

When consumers and producers make decisions in a market without considering all the effects of their decisions on other economic agents

What is asymmetric information?

When the exchange transaction is between better and worse informed economic agents. Ex. When buying a used car the seller knows better.

What is the problem of adverse selection?

Adverse selection occurs when one party in a transaction has more information than the other, often leading to market inefficiencies. For example, in the used car market, the seller may have more information about the car's condition than the buyer, resulting in a selection of lower-quality cars being sold.

Give 4 examples of market failures

Imperfect competition, externalities, public goods, asymmetric information

Give three examples of government failures

Political parties not only voice voters preferences but also pursue their own objectives

Instability and internal divisions of governments can lead to inadequate decision making.

Public administrations pursue their own objectives to some extent

What three questions? Should you ask when market failures and government failures need to be weighed against each other?

is there a market problem?

formulate the ideal government intervention and its consequences

decide whether government intervention is desirable