Comprehensive Guide to Accounting and Taxation Principles

1/150

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai | Chat |

|---|

No analytics yet

Send a link to your students to track their progress

151 Terms

International Accounting Standards Board (IASB)

Private-sector body that develops and issues International Financial Reporting Standards (IFRS).

Basic Principle of a Sound Tax System

Fiscal Adequacy: Source of revenue should be sufficient to meet the demands of public expenditures.

Exemption of the Government

Government can but does not tax itself as this will not raise additional funds.

Non-appropriation of Public Funds

Prohibition of using public funds for the benefit of a church or religion.

Flat or fixed rate tax

Tax that subjects all taxpayers with the same rate.

Pension

Specified income payable at stated intervals for a fixed or contingent period.

Tax Deductions

Compensation for damages; forgiveness of debt; bad debt recovery

Individuals Not Allowed to Claim Deductions

Taxpayers earning compensation income from personal services rendered under an employer-employee relationship

Accrued Expense

Unrecorded expenses that have been incurred and for which cash has not been paid.

Fixed Asset/Property, Plant and Equipment

Physical resources that are owned and used by a business and are permanent or have a long life.

Classified Balance Sheet

Balance sheet that was expanded by adding subsections for current assets; property, plant, and equipment; and current liabilities.

Current Asset

Cash and other assets that are expected to be converted into cash within a year or less.

Current Liabilities

Liabilities that will be due within one year or less.

Long-term Liabilities

Liabilities not due for a long time.

Real Account

Where the revenue and expense account balances are transferred to.

The Closing Process

1. Revenues are transferred to Income Summary; 2. Expenses are transferred to Income Summary; 3. Net Income or Net Loss is transferred to owner's capital; 4. Drawing are transferred to owner's capital.

Post-closing Trial Balance

Prepared after the closing entries have been posted.

Accounting Cycle

The accounting process that begins with analyzing and journalizing transactions and ends with preparing the accounting records for the next period's transaction.

Fiscal Year

Annual accounting period adopted by a business.

Business

Integrated set of activities capable of being conducted and managed for providing goods or services to customers.

Types of Businesses

1. Service Business - Provides Service; 2. Merchandising Business - Provides product; 3. Manufacturing Business - Creates product.

Financial Accounting

Provides external users with information.

Luca Pacioli

Father of Accounting.

Generally Accepted Accounting Principles (GAAP)

Financial accountants follow GAAP in preparing reports.

Financial and Sustainability Reporting Standards Council (FSRSC)

Tasked with promulgating generally accepted accounting principles in the Philippines.

Business Entity Concept

Activities of businesses are recorded separately from the activities of its owners, creditors, or other businesses.

Partnership

Owned by two or more individuals; 1% entities in the Philippines.

Corporation

Organized under state or federal statutes as a separate legal taxable entity; generates 90% of business revenue.

Going Concern Concept

A company that has the resources to continue making enough money to stay afloat for the foreseeable future.

Cost Concept

Amounts are initially recorded in the accounting records at their cost or purchase price.

Unit of Measure Concept

Requires that economic data be recorded in Philippine Peso.

Accounting Equation

Assets = Liabilities + Owner's Equity.

Liabilities

Present obligation from past events; settlement is expected to result in outflow.

Owner's Capital

Contribution of the owner to the business.

Owner's Drawing

Withdrawals of the owner in the business.

Income

Increase in economic benefits during the accounting period.

Revenue

Money earned.

Business Transaction

Economic event or condition that directly changes an entity's financial condition or its result of operation.

Financial Statements

Accounting reports providing information.

Net Income / Net Profit

Excess of revenue over the expenses; carried to the statement of owner's equity.

Net Loss

Expenses exceed the revenue.

Balance Sheet

List of assets, liabilities, and owner's equity as of a specific date.

Taxation

An inherent power of the state to enforce a proportional contribution from its subjects for public purpose.

Purpose of Taxation

Primary Purpose: Generate funds for the state to finance the needs of the citizens.

Necessity Theory

Existence of government is necessity; government cannot continue without means to pay its expenses.

Lifeblood Theory of Taxation

Taxes are the lifeblood of the nation through which government agencies continue to operate.

Administrative Feasibility

Laws should be capable of convenient, just and effective administration.

Territoriality of Taxation

Tax can be only imposed within the territory of the state.

Public Purpose

Tax is intended for common good; taxation must be exercised for public purpose.

Non-delegation of the Taxing Power

Legislative taxing power is vested exclusively in congress and is non-delegable.

Due Process of Law

A constitutional limitation ensuring fair legal proceedings.

Uniformity Rule in Taxation

Taxation must be uniform across similar entities.

Stages of Taxation Power

Includes Levying or Imposition, Assessment and Collection, and Payment.

Direct Double Taxation

Occurs when all elements of double taxation exist for both impositions.

Indirect Double Taxation

Occurs when at least one of the secondary elements of double taxation is not common.

Tax Avoidance

Act or trick that reduces or totally escapes taxes by any legally permissible means.

Tax Exemption

Immunity, privilege or freedom from being subject to a tax which others are subject to.

Specific Tax

Tax of a fixed amount imposed on a per unit basis.

Ad Valorem Tax

Tax based on the value of the property.

Excise Tax

Tax imposed on specific goods, often to regulate behavior.

Community Tax

Tax on persons who are residents of a particular place.

Property Tax

Tax on properties.

Real or personal

Refers to types of property or assets.

Real estate tax

Tax imposed on real property.

Income tax

Tax on annual income, gains or profits.

Estate tax

Tax on gratuitous transfer of properties by a decedent upon death.

Direct tax

Tax collected from the person who is intended to pay the same or tax which is non-transferable.

Proportional tax

Tax that emphasizes equality as it subjects all taxpayers to the same rate.

Percentage tax

Tax that is calculated as a percentage of the value.

Progressive or Graduated tax

Tax that imposes increasing rates as the tax base increases.

Regressive tax

Tax that imposes decreasing tax rates as the tax base increases.

Local tax

Tax imposed by the municipal or local government.

Professional tax

Business taxes, fees and charges.

Tax laws

Laws that provide for the assessment and collection of taxes.

Tax exemptions laws

Laws that grant immunity from taxation.

Sources of Taxation Laws

1. Constitution 2. Statutes and presidential decrees 3. Judicial decisions or case laws and conventions with foreign countries 4. Executive orders and batas pambansa 5. Administrative issuances 6. Local ordinances 7. Tax treaties 8. Revenue regulations.

Nature of Philippine Tax Laws

Are civil and not political in nature.

Tax Administration

Refers to the management of the tax system.

Bureau of Internal Revenue (BIR)

The agency entrusted with tax administration under the Department of Finance.

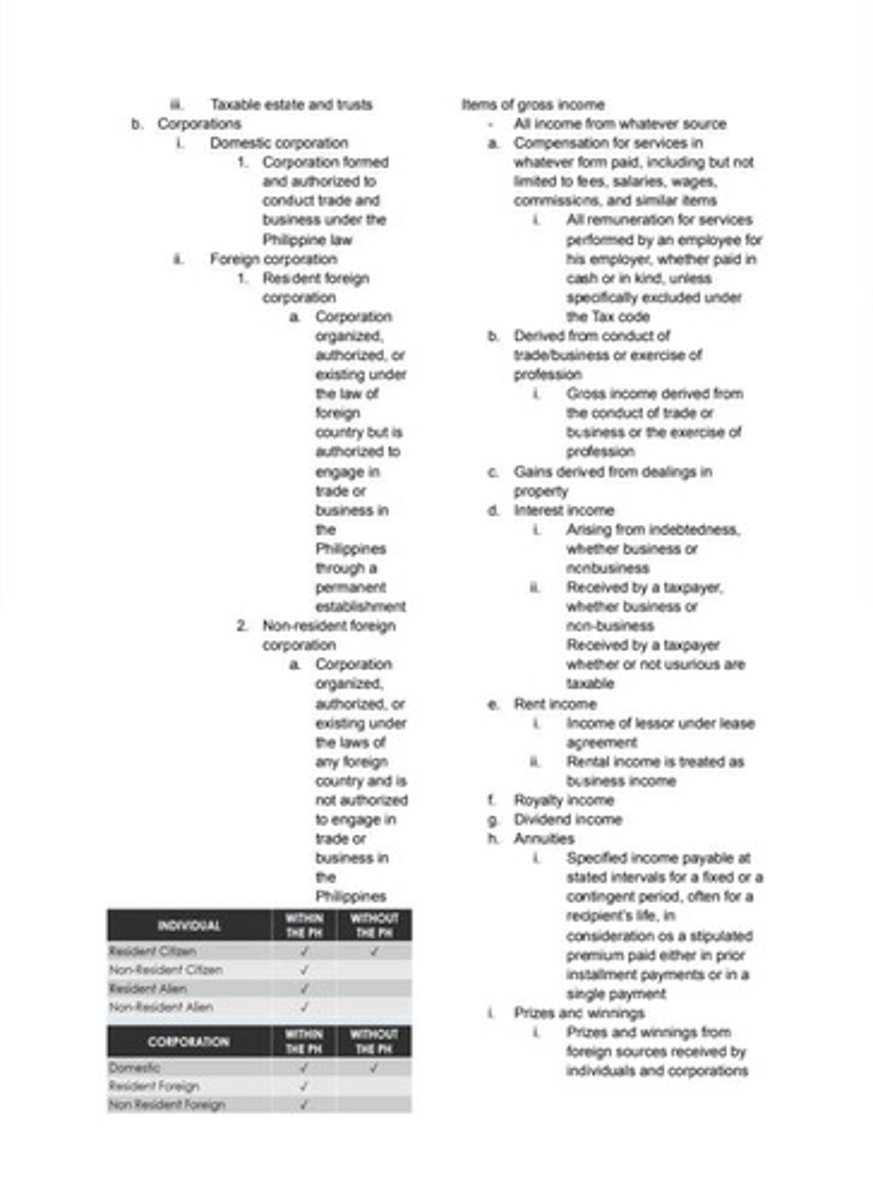

Domestic corporation

Corporation formed and authorized to conduct trade and business under Philippine law.

Resident foreign corporation

Corporation organized under the law of a foreign country but authorized to engage in trade or business in the Philippines.

Non-resident foreign corporation

Corporation organized under the laws of any foreign country and not authorized to engage in trade or business in the Philippines.

Items of gross income

All income from whatever source.

Compensation for services

Includes fees, salaries, wages, commissions, and similar items.

Interest income

Income arising from indebtedness, whether business or non-business.

Prizes and winnings

Prizes and winnings from foreign sources received by individuals and corporations.

Gains arising from exploration of property

Income from illegal business or from embezzlement; damage recovery

Taxable Income

Gross Income - deductions = taxable income / tax due/liability

Gross Income

Amounts allowed by law as provided in the tax code and other special laws

Deductions

To be deducted from the gross income subtracted from the items of gross income

Individuals Allowed to Claim Deductions

Individuals and corporations engaged in business; individuals in the exercise of profession

Requisites for Deductibility

Must be ordinary and necessary; substantiated or supported by sufficient evidences; connected with trade, business or practice of profession; paid or incurred during the taxable year; not against the law, morals, public policy or public order; must have been subjected to withholding tax if applicable

Ordinary and necessary expenses

Salaries and other forms of compensation; travel expense; rental and lease agreements; entertainment, amusement and recreation expense

Taxes

Various taxes that can be deducted

Losses

Incurred in trade, profession or business; property connected with trade, business or profession if the loss arises from fires, storm, shipwreck or other casualties or from robbery, theft or embezzlement

Kind of losses

Ordinary losses; casualty losses; net operating loss carry-over; capital losses and income by the code or other special laws

Bad debts

Deductible only if it is a valid business-related debt, not between related parties, proven worthless and uncollectible, and properly written off in the taxpayer's books by year-end

Charitable and other contributions

Donations to the government or political subdivisions including fully owned government corporations

Research and development

Expenses related to research and development can be deducted

Pension trusts

Contributions to pension trusts can be deducted