Looks like no one added any tags here yet for you.

Economics

the study of how resources are allocated as a result of unlimited wants and desires, paired with limited resources

Scarcity

a condition in which there is not enough natural resources to fulfill the needs and wants of citizens

Shortage

a condition when there is excessive demand and limited supply. This is typically a reaction to prices being too low and excessive consumption (increase price to fix it)

Surplus

a condition when there is excessive supply and limited demand. This is typically a reaction to prices being too high and low consumption. (decrease price to fix it)

Marginal Cost

The cost associated with each additional unit consumed

Marginal Benefit

The benefit associated with each additional unit consumed

Three fundamental economic questions

What to make, How to make it, Who to sell it to

Factors of production

Labor, Capital, Entrepreneurship, Land

Opportunity Cost

the loss of potential gain from other alternatives when one alternative is chosen. Example: idle cash balances represent an opportunity cost in terms of lost interest on possible money made from investment

Simple terms: It is what you are giving up as a result of the choice you are making

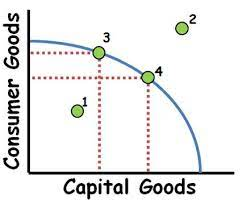

Production Possibility Frontier

Used to illustrate the trade-off scenario when explaining opportunity cost.

Comparative Advantage

doing what you’re best at compared to others; producing things with the least amount of trade-offs or sacrifices.

How do suppliers know which good they should specialize in?

which supplier, has the lowest opportunity cost should make that product

Absolute Advantage

When one country produces more of each product

What does point 1 tell?

Inefficient - not working at full potential, but no trade offs needed

What does point 3 or 4 tell?

Full Potential

What does point 2 tell?

Unattainable with resources available - if you get to that point, economic growth occurred (PPC curve moves right)

Determinants

these are shifters of demand, such as the number of consumers and future expectations

Substitutes

Ex. Pepsi and coke (interchangeable)

Compliments

Goods that go together, such as cars and gas

Inelastic goods

A good that consumers will still buy regardless of the price (ex. gas, inhaler)

Shortage

Leads to excess demand, fix by raising price

Surplus

Excess supply, fix by lowering price

Price ceilings

Max legal price that can be charged for a product

Price floor

Lowest price that goods/service can be paid for (ex. Farming, min wage)

equilibrium

There is no shortage or surplus

Market disequilibrium

There is either a shortage or a surplus of goods