AP Microeconomics Unit 2

5.0(1)

Studied by 37 peopleCard Sorting

1/56

Earn XP

Last updated 3:08 AM on 2/4/23

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

57 Terms

1

New cards

Change in Demand

a shift of the demand curve, which changes the quantity demanded at any given price.

2

New cards

Change in Supply

a shift of the supply curve, which changes the quantity supplied at any given price.

3

New cards

Competitive Market

a market in which there are many buyers and sellers of the same good or service, none of whom can influence the price at which the good or service is sold.

4

New cards

Complements

two goods (often consumed together) for which a rise in the price of one of the goods leads to a decrease in the demand for the other good.

5

New cards

Consumer Surplus

the net gain received from purchasing a good or service; often used to refer to both individual and total

6

New cards

Consumption Bundles

Typical groups of goods and/or services purchased

7

New cards

Cross-Price Elasticity of Demand

(between two goods) measures the effect of the change in one good’s price on the quantity demanded of another good; is equal to the percent change in the quantity demanded of one good divided by the percent change in the other good’s price.

8

New cards

Deadweight Loss

the value of foregone mutually beneficial transactions; (from a tax) the decrease in total surplus resulting from the tax, minus the tax revenues generated.

9

New cards

Demand Curve

a graphical representation of the demand schedule; shows the relationship between quantity demanded and price.

10

New cards

Demand Schedule

table that shows how much of a good or service consumers will be willing and able to buy at different prices.

11

New cards

Determinants of Demand

Income of consumers, related goods or prices, expectations of future prices, number of consumers in the market, and tastes and preferences are all

12

New cards

Determinants of Supply

Cost of productive resources, opportunities for revenue from other goods/services, number of producers in the market, technology, expectations of future prices, subsidies, and taxes are all

13

New cards

Elastic Demand

when the price elasticity of demand is greater than 1

14

New cards

Elastic Supply

when the price elasticity of supply is greater than 1

15

New cards

Equilibrium Price and Quantity

The price (also known as market-clearing price) and quantity where quantity supplied and demanded are equal.

16

New cards

Factor/Resource Market

where resources, especially capital and labor, are bought and sold.

17

New cards

Income

money received, especially on a regular basis, for work or through investments

18

New cards

Income Effect

the change in the quantity of a good demanded that results from a change in the consumer’s purchasing power when the price of the good changes.

19

New cards

Income Elasticity

the percent change in the quantity of a good demanded when a consumer’s income changes divided by the percent change in the consumer’s income;

\

it measures how changes in income affect the demand for a good.

\

it measures how changes in income affect the demand for a good.

20

New cards

Inelastic Demand

When changes in price don’t heavily affect the quantity demanded

21

New cards

Inelastic Supply

When changes in price don’t heavily affect the quantity supplied

22

New cards

Inferior Good

when a rise in income decreases the demand for a good;

usually considered less desirable than more expensive alternatives.

usually considered less desirable than more expensive alternatives.

23

New cards

Input

a good or service that is used to produce another good or service.

24

New cards

Law of Demand

states that a higher price for a good or service, other things being equal, leads people to demand a smaller quantity of that good or service.

25

New cards

Law of Diminishing Marginal Utility

states that each successive unit of a good or service consumed adds less to total utility than does the previous unit.

26

New cards

Law of Supply

states that, other things being equal, the price and quantity supplied of a good are positively related.

27

New cards

Lump-Sum Tax

a tax of a fixed amount paid by all taxpayers, independent of the taxpayer’s income.

28

New cards

Market-Clearing Price

Alternative name for equilibrium price

29

New cards

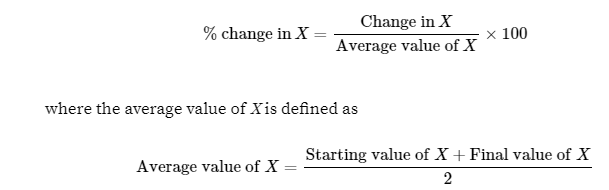

Midpoint Formula

a technique for calculating the percent change by dividing the change in a variable by the average, or midpoint, of the initial and final values of that variable.

30

New cards

Normal Good

a type of good in which a rise in income increases the demand for it; most goods are these type of good

31

New cards

Perfectly Elastic

Elasticity where price change causes an infinite change in quantity (demanded or supplied) (horizontal line on graph)

32

New cards

Perfectly Inelastic

Elasticity where a price change causes zero change in quantity (demanded or supplied) (vertical line on graph)

33

New cards

Price Ceiling

a maximum price that sellers are allowed to charge for a good or service.

34

New cards

Price Controls

legal restrictions on how high or low a market price may go; typically take the form of either a price ceiling or a price floor.

35

New cards

Price Elasticity of Demand

the ratio of the percent change in the quantity demanded to the percent change in the price as we move along the demand curve (dropping the minus sign).

36

New cards

Price Floor

a minimum price that buyers are required to pay for a good or service.

37

New cards

Producer Surplus

refers to both individual and total surplus of sellers in a market

38

New cards

Product Market

where goods and services are bought and sold.

39

New cards

Profit

typically total revenue - total cost; difference between amount earned and amount spent in buying

40

New cards

Quantity Demanded

the actual amount of a good or service consumers are willing and able to buy at some specific price; shown as a single point in the demand schedule or along a demand curve.

41

New cards

Quantity Supplied

the actual amount of a good or service people are willing to sell at some specific price.

42

New cards

Quota

an upper limit on the quantity of some good that can be bought or sold; also known as a quantity control.

43

New cards

Revenue

the value of output sold, either marginal or total

44

New cards

Shortage

when the quantity of a good or service demanded exceeds the quantity supplied; occurs when the price is below its equilibrium level; also known as excess demand.

45

New cards

Subsidies

government payments to individuals and businesses: used to offset market failures and externalities to achieve greater economic efficiency.

46

New cards

Substitutes

two goods for which a rise in the price of one of the goods leads to an increase in the demand for the other good.

47

New cards

Substitution Effect

the change in the quantity of a good demanded as the consumer substitutes the good that has become relatively cheaper for the good that has become relatively more expensive.

48

New cards

Supply

the actual amount of a good or service people are willing to sell at various prices, rather than one specific price

49

New cards

Supply Curve

curve that shows the relationship between the quantity supplied and the price.

50

New cards

Supply Schedule

table that shows how much of a good or service producers would supply at different prices.

51

New cards

Surplus

when the quantity supplied of a good or service exceeds the quantity demanded; occurs when the price is above its equilibrium level; also known as excess supply.

52

New cards

Tariff

a tax on imports.

53

New cards

Tax Incidence

the distribution of the tax burden (tax burden is basically where money for paying a tax comes from.)

54

New cards

Total Surplus

the total net gain to consumers and producers from trading in a market; the sum of consumer surplus and producer surplus.

55

New cards

Unit Elastic

Elasticty where price elasticity is equal to 1: the percent change in price equals the percent change in quantity

56

New cards

Utility

a measure of personal satisfaction.

57

New cards

World Price

The price of a good that prevails in the world market