Looks like no one added any tags here yet for you.

What is Audit Risk?

The risk that an auditor expresses an inappropriate audit opinion when the financial statements are materially misstated

Can audit risk ever be zero?

No!

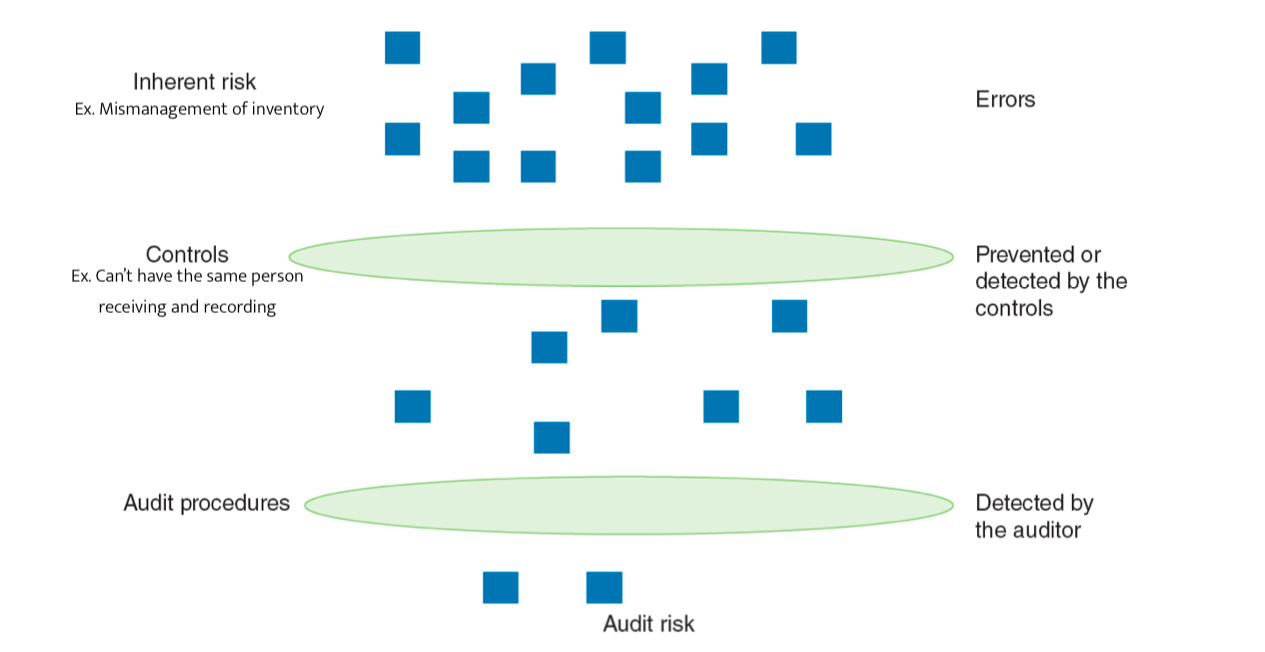

What are the 3 stages of audit risk minimization?

Identification of accounts and related assertions most at risk of material misstatement (inherent risk)

Assessment of client’s system of internal controls (control risk)

Auditor plans to undertake detailed testing of each identified account to the extent deemed necessary

What are some factors that make risks more significant?

Fraud

Transactions where subjectivity is involved

Accounting estimates with high estimation uncertainty or complexity

Complexity in data collection and/or processing

Mergers and acquisitions

Audit Risk Formula: AR =

AR = Inherent Risk x Control Risk x Detection Risk

What is Inherent Risk?

Risk that material misstatement could occur

What is Control Risk?

Risk that the client’s system of internal controls will not prevent or detect such a material misstatement

What is Detection Risk?

Risk that the auditor’s testing procedures will not be effective in detecting a material misstatement, should there be one

Describe the Audit Risk Model

Errors are reduced through each stage (top to bottom)

What are the two common relationship patterns between IR, CR, and DR?

If IR and CR are high, DR is low → more testing

If IR and CR are low, DR is high → less testing

Define Materiality

Materiality guides audit planning, testing, and assessment of information in the financial statements

What make information “material?”

Information is material if it impacts on the decision-making process of users of the financial statements

Information could be considered material because of its qualitative or quantitative characteristics

What is performance materiality?

an amount less than planning materiality, to reduce the likelihood that a misstatement in a particular account balance, class of transactions, or disclosures does not in total exceed overall materiality

What are 3 things we know about an audit strategy?

It sets scope, timing, and direction of the audit

It provides basis for developing detailed audit plan

It is based on preliminary assessments of IR and CR

When CR is high, what kind of audit strategy is commonly used?

A predominantly substantive approach (less testing of controls)

When CR is low and DR is high, what kind of audit strategy is most commonly used?

A combined audit strategy (extensive testing of controls + detailed understanding of internal controls)

What are two common client performance measures?

Profitability and Liquidity

What is an analytical procedure?

Evaluation of financial information by studying plausible links among both financial and non-financial data

How can an analytical procedure be conducted?

Risk assessment

Risk response

Reporting

What are some common examples of analytical procedures?

Simple comparisons

Trend analysis

Common-size analysis (vertical analysis)

Ratio analysis