Lesson 2.5: Costs of Production

1/10

Earn XP

Description and Tags

Flashcards made from a presentation segment created as a lesson on the costs of production.

Name | Mastery | Learn | Test | Matching | Spaced |

|---|

No study sessions yet.

11 Terms

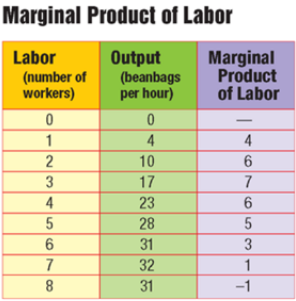

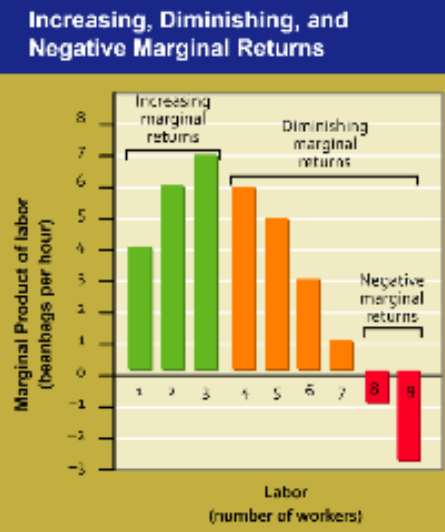

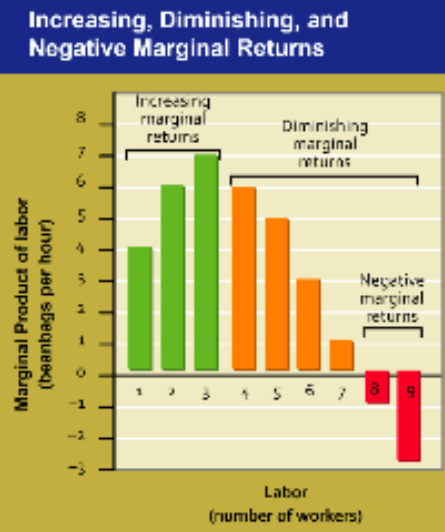

Marginal product of labor

The change in output from hiring one additional unit of labor

How much more of a product can be produced by hiring one more worker

Specialization

The focus of one worker on a specific task for greater efficiency per worker by reducing the time spent switching and performing different tasks

Increasing marginal returns

Level of production in which the marginal product of labor increases as the number of workers increases, thus reaping the benefits of specialization

Diminishing marginal returns

Level of production in which the marginal product of labor decreases as the number of workers increase

Insufficient work is being distrubted to effectively specialize the labor needed

This can be limited by fixed capital, where workers may be unable to simultaneously use a machine at one time

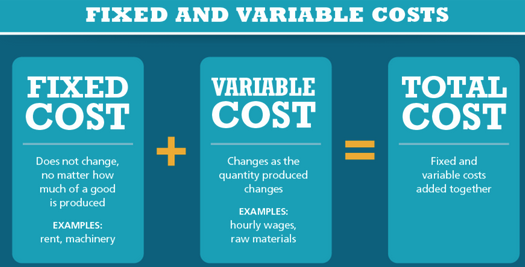

Fixed cost

A cost that does not change periodically, no matter how much of a good is produced

Mainly involves production facility, cost of building, and equipment

Examples include rent, machine repairs, and property taxes

Variable cost

A cost that rises or falls depending on how much is produced

Includes raw materials and some labor, electricity, and heating bills

Total cost

The sum of the fixed and variable costs in making a product

Profit maximization

A firm’s primary goal through increasing revenue and reducing operating costs

Highest profitability comes from more revenue and lower costs (a bigger gap)

Total revenue

The total proceeds from the sale of a good

Marginal revenue (market price)

The additional income of selling one more unit of a good or service, typically determined by the market

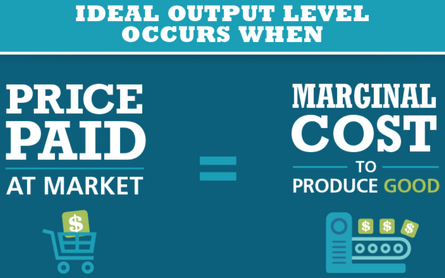

Marginal cost

The cost of adding one more unit

Efficiency occurs when the price paid at market equals this to produce a good in order to maximize net revenue and resource allocation