IGCSE Business 0450 C1

1/65

Earn XP

Description and Tags

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

66 Terms

Define the concept need and give examples

Goods or services essential for survival. e.g. food, water, shelter, clothing

Define the concept want and give examples

Goods or services not essential, but desired to improve quality of life. e.g. Mobile phones, holidays, branded clothes.

Unlimited, but resources to fulfil them are limited.

Define the concept scarcity

A shortage of resources to meet all wants and needs.

Define the concept opportunity cost

The next best alternative foregone when making a choice.

Helps in resource allocation

- Forces decision-makers to weigh alternatives carefully

e.g. A student has £10. They buy a book instead of going to the cinema. the opportunity cost is the cinema experience

Explain why the economic problem exists

- Unlimited wants (phones, cars, luxury items…)

- Limited resources (factors of production)

- Result: Scarcity → people must make choices

- Every choice involves an opportunity cost

Define the factors of production and examples

Land: All natural resources, e.g. minerals, ores, gas, fields

Labour: Number of people available to work , e.g. employees , teachers

Capital: Machinery, equipment and finance (money) needed , e.g. machines

Enterprise: The person who has an idea for a new business and takes the financial risks of starting up and managing it in the hope of making profit, entrepreneurs

Entrepreneurs do what when creating a business?

- Combines the other 3 factors of production

- Takes financial risks

- Aims to make a profit

Describe the main objectives of business activity

- Businesses produce different types of goods and services:

- Satisfy consumer needs and wants

- Combine factors of production to produce goods/services

- Add value to resources

- Create employment

- Generate profit

- Improve living standards

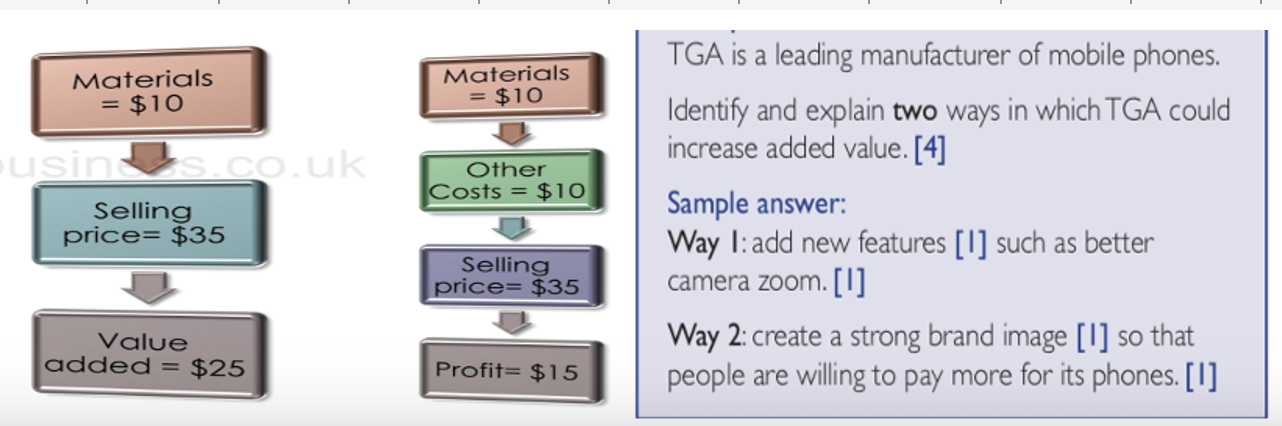

Define adding value and state the formula for it

more than it cost to produce it, in order to gain more profits

Added Value = Selling Price – Cost of Materials

Describe how businesses add value

Branding → Nike, Apple

Design/features → Smartwatch with fitness tracking

Quality → Durable shoes, reliable tech

Customer service → Easy returns, personalised support

Packaging → Eco-friendly or eye-catching designs

Convenience → Delivery services, mobile apps

Describe the importance of added value

- Supports higher pricing

- Builds customer loyalty

- Increases profitability (earns profit)

- Essential in competitive markets

Define specialization

When individuals, firms, or regions focus on specific tasks they are talented in to improve efficiency.

Specialisation makes the best use of limited resources.

Define division of labour

A form of specialisation where production is split into separate tasks, each done by a different worker.

Outline the advantages/disadvantages of division of labour

Advantages: - Increased efficiency, work faster so produce more products

- Workers become more skilled at their task

- Lower costs for businesses

- Higher product quality

- Shorter training time

Disadvantages: - Boredom from repetition - Lack of flexibility – workers can’t easily switch tasks

- Dependency – if one worker is absent, production may stop

- Lower motivation → higher turnover, absenteeism

State the 3 sectors , what they involve and examples of each one

Primary: Using natural resources. e.g. Farming, fishing, forestry, mining.

Secondary: Using natural resources. e.g. Car manufacturing, construction, food canning, furniture making.

Tertiary: Providing services. e.g. Shops, banks, transport, restaurants, hotels, insurance

State the name given to the sectors which are connected

Chain of production:

1) Primary sector provides raw materials.

2) Secondary sector processes them.

3) Tertiary sector sells or supports the products.

Explain the changing importance of sectors

- Developing Countries (e.g., Rwanda, Vietnam)

- Primary sector is largest.

- People work in agriculture.

- Low demand for services.

- Developed Countries (e.g., UK, USA)

- Tertiary sector is largest.

- High income = more demand for services.

- Goods are often imported.

- Emerging Economies (e.g., China, India)

- Growing secondary and tertiary sectors.

- Rapid industrialisation.

State the reasons for sector changes

- Industrialisation: Shift from primary → secondary.

- De-industrialisation: Shift from secondary → tertiary.

- Raw materials running out (e.g. deforestation).

- People want more services (e.g. holidays, insurance).

- Cheaper goods imported from abroad.

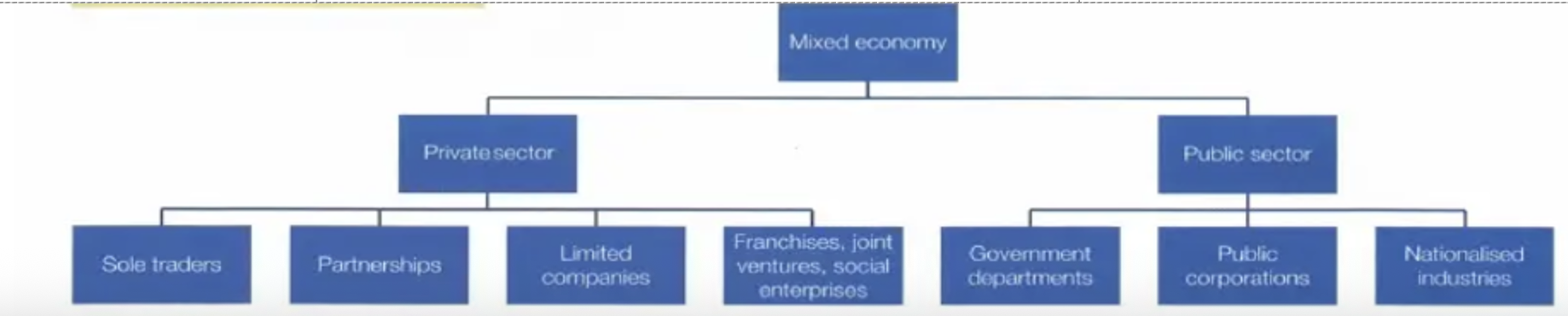

Describe what a mixed economy contains

- Private sector (owned by individuals).

- Public sector (owned by the government).

Explain the private sector including advantages and disadvantages

Owned: By individuals or companies.

Goal: Make profit.

Makes decisions based on:

What people want to buy.

How to produce at low cost.

Advantages:

More efficient (profit-driven).

Better quality due to competition.

More investment from owners.

Disadvantages:

Less focus on social benefits.

May cut jobs to save money.

Explain the public sector

- Owned: By government.

- Goal: Provide essential services e.g. education, healthcare, roads, public transport, defence

- Paid for: By taxes.

- Often free or low-cost for users.

Define entrepreneur and state the advantages and disadvantages of becoming one

An entrepreneur is a person who:

Has an idea for a business

Takes the financial risk of starting and running it

Aims to make profit

Organises the factors of production (land, labour, capital)

Advantages:

Keep all profits

Make own decisions (independence)

Flexible work and follow personal interests

Might earn more than being an employee

Disadvantages:

Risk of failure and losing money

May lose income from other jobs (opportunity cost)

Hard to get loans/finance from banks

Need a wide range of skills/experience

Explain the key characteristics of a successful entrepreneur and why it matters

Innovative → Think of new ideas and products

Risk-taker → Willing to take calculated risks

Decision-maker → Makes important business choices

Leader → Motivates others, communicates clearly

Determined → Keeps going when things get tough

Self-confident → Believes in themselves and the idea

Multi-skilled → Understands all areas (finance, HR, etc.)

Hard-working → Puts in long hours to make the business work

Define business plan

It is a document that explains how a business will work and succeed and used to attract investors and plan operations

describe the main parts of a business plan

- Business details – idea, owner, employees needed

- Location – where and why it’s a good place

- Objectives – clear goals

- Market research – customer needs, size of market, competitors

- Marketing plan – how the product will be promoted and sold

- Financial info – expected sales, costs, revenue, profits

- Sources of finance – savings, loans, etc.

- Cash flow forecast

State how business plans help entrepreneurs:

- Attract finance (banks, investors)

- Identify risks and weaknesses

- Help with decision making

- Give direction and set SMART objectives

- Improve chance of success

State why governments support start-ups:

- Create jobs → reduce unemployment

- Encourage competition → better quality and lower prices

- Help grow the economy

- Start-ups may grow → pay more taxes

- Offer cheaper products due to low costs

State governments support start-ups:

- Advice and training

- Grants for capital or training workers

- Low-interest loans

- Tax reductions in early years

- Free/cheap premises

Explain why it is important to compare business size

- Investors – to decide where to invest.

- Banks – bigger = safer to lend to.

- Competitors – to compare performance.

- Suppliers – prefer large businesses (buy more).

- Government – for taxes.

- Workers – job security.

Explain the ways to measure business size and its limitation

Number of employees → Bigger firms usually employ more workers.

But → Not accurate if businesses use machines instead of people.

Capital employed → More money spent on buildings, machines, etc.

But → Different industries need different capital amounts.

Value of output → How much they produce (in money).

But → Some small businesses sell expensive items (e.g., luxury goods).

Market share → % of sales in the total market.

But → May not reflect actual size (e.g., niche market with big market share).

Explain why businesses should grow

- Higher profits = more reinvestment, more dividends.

- Easier to borrow – big firms are seen as safer.

- Avoid takeovers – big firms are harder to buy.

- Increase market share – stronger brand, more power.

- Benefit from economies of scale – lower costs per unit.

- Personal reasons – power, success.

- Diversification – reduce risk by entering new markets.

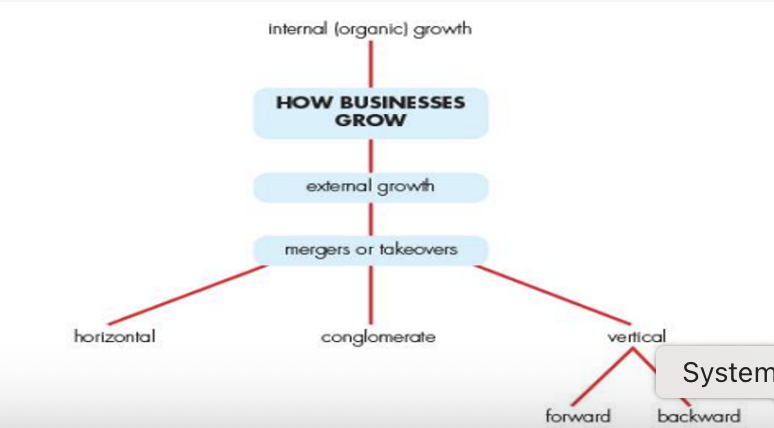

Explain different ways in which businesses can grow, e.g. internal/external

Internal (Organic) Growth

- Open new shops or expand to new areas/countries.

- Launch new products.

- Invest in technology/machinery.

- Advertise more.

External Growth (Mergers & Takeovers) - Merger = Two businesses join.

- Takeover = One business buys another.

Explain the types of external growth (integration)

Horizontal → Same industry & same stage. e.g. 2 banks merge

Vertical – Forward → Later stage (closer to customer). e.g. manufacturer buys retailer

Vertical – Backward → Earlier stage (closer to raw materials). e.g. retailer buys supplier

Conglomerate (Diversification) → Different industries. e.g. Cosmetic firm buys drink company

Explain the problems linked to business growth and how these might be overcome

Internal:

Slower growth

Cash flow problems

Lack of capital or tech

Hard to manage more staff

External:

Conflict between staff from different businesses

Lack of expertise to manage larger business

Poor communication in large firms

Lose control (e.g., in a partnership)

State the solutions for the problems linked to business growth

- Grow slowly using profits

- Hire skilled managers

- Communicate well

- Plan growth carefully

Explain the reasons of why businesses stay small and give examples

Owner’s choice → Wants full control, personal service, low risk.

Small market → Only serves a local area or niche market.

Type of business → Personal services (hairdresser, plumber).

Lack of capital → Banks won’t lend easily to small/new firms.

State 4 advantages and disadvantages of keeping a business small

Advantages:

Closer customer relationships

Quick to adapt to changes

Unique/premium products

Low costs (e.g., work from home)

Disadvantages:No economies of scale

Harder to compete

Tough to hire top talent

Limited resources

Explain the main causes of business failure

Poor planning/objectives → No clear goals or business plan.

Liquidity problems → Not enough cash to pay expenses.

Wrong location → Far from customers.

Poor management → Lack of experience = bad decisions.

No investment in tech → Can’t compete in price/quality.

No change/adaptation → Doesn’t respond to trends/fashion.

Poor marketing → No research = no customers.

Lack of finance → Can’t borrow enough money to grow.

Strong competition → Bigger firms offer better/cheaper products.

Economic conditions → Recession, taxes, inflation reduce customer spending.

Over-expansion —> Growing too fast without enough resources.

State why new businesses fail more often

- Lack of experience/skills

- No customer base yet

- Hard to raise finance

- Tough competition

- Weak marketing

- Cash flow issues

- No clear objectives

Define sole trader

- One owner, runs and controls the business

- Keeps all profits

Explain the advantages and disadvantages of being a sole trader

Advantages:

Easy and cheap to set up

Full control and quick decision-making

All profits go to the owner

Disadvantages:Unlimited liability (personally responsible for debts)

Difficult to raise finance

Heavy workload and no continuity (ends if owner dies)

Define the term partnership

- 2 to 20 people share ownership

- Share profits and responsibilities

- Have a partnership agreement

Explain the advantages and disadvantages of a partnership

Advantages:

More capital available

Shared workload and decisions

Different skills and expertise

Disadvantages:Unlimited liability

Profits shared

Possible disagreements

No continuity if a partner leaves

Define the term Private Limited Company

- Shares sold privately (e.g., to family or friends)

- Limited liability (owners are not personally responsible for debts)

- Has a separate legal identity

Explain the advantages and disadvantages of a Private Limited Company

Advantages:

Limited liability

Can raise capital by selling shares

Continuity (business survives if a shareholder dies)

Disadvantages:

Can’t sell shares to the public

More legal requirements and costs

Must publish annual accounts

Define the term Public Limited Company

- Can sell shares to the public (stock exchange)

- Large businesses

Explain the advantages and disadvantages of a Public Limited Company

Advantages: Can raise large capital

Limited liability

Continuity

Disadvantages: Expensive and complicated to set up

Risk of takeover

Less control for original owners

Must publish accounts

Explain the term franchise

- A franchise is a business where the franchisee buys the right to use the franchisor’s brand, products, and business system.

- The franchisee runs the business but must follow the franchisor’s rules.

- The franchisor provides support like training, marketing, and a proven business model.

- The franchisee usually pays fees or royalties to the franchisor.

- Example: Opening a McDonald's outlet as a franchisee.

List the advantages and disadvantages of a franchisee

Advantages: - Uses a well-known brand (easier to get customers)

- Training and support from franchisor

- Lower risk of failure (business model is already proven)

Disadvantages: - Expensive to start (franchise fee + setup costs) - Little freedom to make your own decisions

- You must share your profits with the franchisor

List the advantages and disadvantages of a franchisor

Advantages: - Can expand the business quickly without spending much

- Earns money through fees and a % of franchisee’s profits

Disadvantages: - Loses some control over how each franchise is run - If a franchisee gives bad service, it can hurt your brand

Define joint venture

Two or more businesses work together on a project, sharing costs, profits, and risks

List the advantages and disadvantages of joint ventures

Advantages: - Shared risks and costs

- Local knowledge

- Access to new markets

Disadvantages: - Profits shared - Conflict in decision-making

- Mistakes affect all partners

Explain the differences between unincorporated and incoporated

Unicorporated:

Legal identity is same as owner

Liability is unlimited

E.g. sole trader, partnership

No continuity

Setup is quick and easy

Incorporated:

Legal identity separate from owner

Liability is limited

E.g. private Ltd, public Ltd

Continuity

Setup is complex (legal documents…)

Define ownership and who it applies to

Person or people who legally own and control the business

Determines control and responsibility

Applies to Sole traders, Partnerships, (private) Ltd, (public) Plc

Define unlimited liability and who it applies to

Owner is personally responsible for all business debts and risks personal assets to pay depts

Applies to: Sole traders, Partnerships

Define limited liability and who it applies to

Owner only loses money invested in the business

Personal assets protected if business fails

Applies to: Private and Public Limited Companies

Define risk and who it applies to

Chance of losing money or assets due to business failure

Lower in limited liability businesses

Applies to: All business ownerse

Explain what choosing the right business form depends on

- Number of owners

- How fast it needs to start

- How much capital is needed

- Willingness to risk personal wealth

- Size and future growth plans

Illustrate a business growth stage

New small business → Sole Trader

More owners → Partnership

Growing business → Private Limited Company (Ltd)

Very large → Public Limited Company (PLC)

Define business objective

A specific target a business wants to achieve.

Explain why business objectives are so important

- Gives direction and motivation.

- Helps managers make decisions.

- Aligns everyone towards the same goal.

- Measures success and progress.

- Helps with planning and using resources efficiently.

Explain 5 common business objectives

- Survival: Short-term goal, especially for new or struggling businesses.

- Profit: Key for established businesses to reward owners and grow.

- Growth: Helps reduce costs, build brand, and expand.

- Market Share: Increases influence, revenue, and competitive advantage.

- Corporate Social Responsibility (CSR): Focus on social, ethical, and environmental responsibility.

Explain why objectives change and include examples of objectives

Business change because of:

- Business size and stage.

- Market or economic changes (e.g. COVID).

- Competition.

- Social Enterprises:

- Private businesses with social aims.

- Profits are reinvested to support social causes.

Objectives include: - Social (e.g. helping disadvantaged people)

- Environmental (e.g. protecting the planet)

- Financial (e.g. reinvesting profits)

State what a stakeholder is including what types there are and their objectives

Stakeholders are people or groups interested in a business.

2 types of stakeholders:

Internal: Owners, managers, employees.

External: Lenders, suppliers, customers, government, local community.

Their objectives are:

- Owners/Shareholders: High profit and share value.

- Managers: High salary, job security, company success.

- Employees: Fair pay, job security, safe conditions.

- Lenders: Loan repayment with interest.

- Suppliers: On-time payment and long-term contracts.

- Customers: Good quality, fair prices, good service.

- Government: Jobs, tax revenue, economic growth.

- Local Community: Jobs, environmental care, local support.

Explain 3 main conflicts between skateholders

- Owners want high profit; employees want higher wages.

- Customers want low prices; producers want high prices.

- Local communities want clean environment; factories may cause pollution.

Explain the differences between public and private sector objectives

Private Sector Objectives:

- Profit

- Survival

- Growth

- Market share

- Reward to shareholders

- Customer service

- Public Sector Objectives:

- Provide essential services to the public:

- Accessible

- Affordable

- Inclusive

- Do not focus on survival or profit